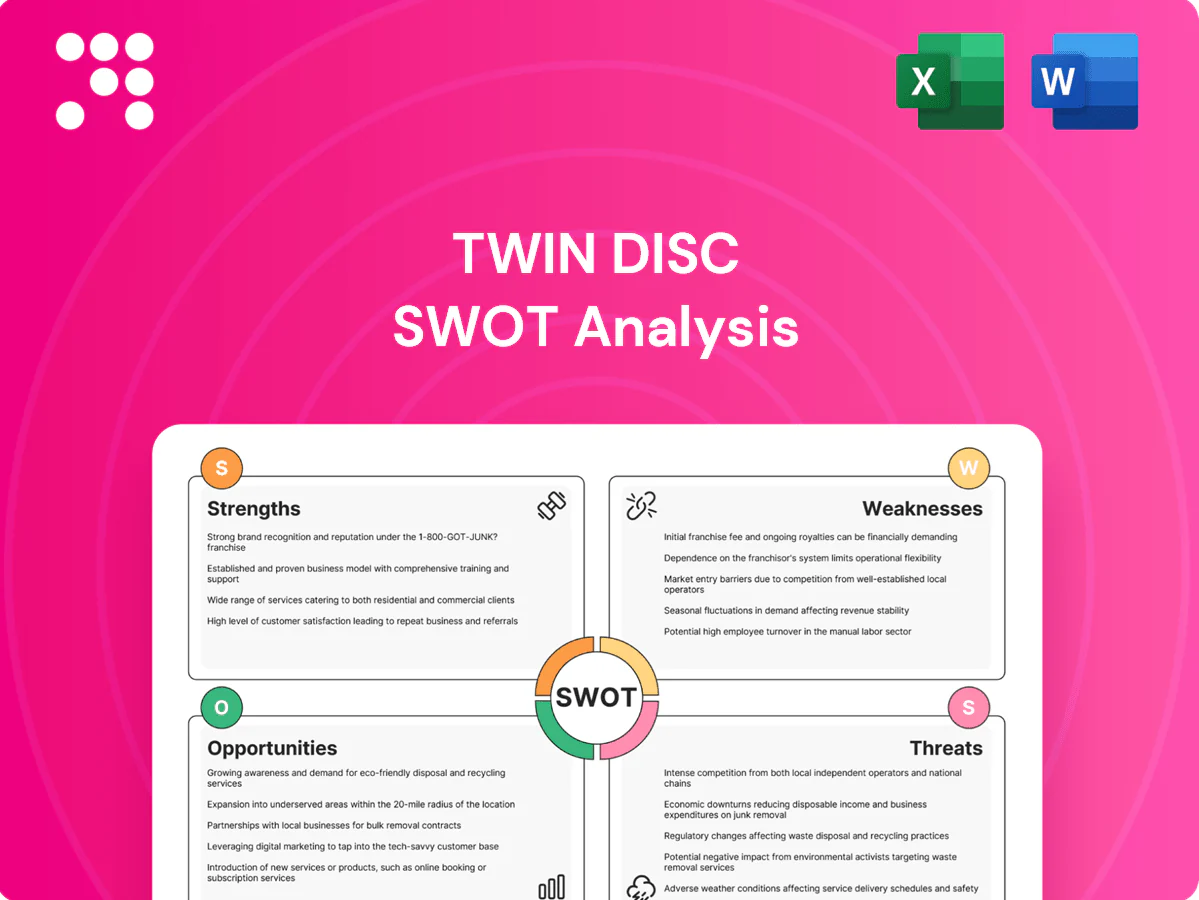

Twin Disc SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Twin Disc’s SWOT snapshot highlights robust marine and off‑highway market positions, supply-chain sensitivities, and growth opportunities in electrification and aftermarket services. Want deeper competitive, financial, and strategic analysis? Purchase the full SWOT to receive a research‑backed, editable Word report and Excel matrix—ready for investor pitches, planning, or due diligence.

Strengths

Heavy-duty engineering pedigree

Founded in 1918, Twin Disc's century-plus specialization in high-torque, harsh-environment power transmission builds strong credibility with marine, energy and off-highway customers. Proven reliability in mission-critical applications reduces lifecycle costs and supports aftermarket repeat business. The engineering moat is hard for generalists to replicate and underpins premium pricing for Twin Disc (ticker TWIN on NASDAQ).

Broad product portfolio

Marine transmissions, azimuth drives, clutches, power-shift transmissions and electronic controls let Twin Disc address multiple drive-line needs across commercial and recreational markets; the company reported approximately $184.1 million in net sales for fiscal 2024, underscoring product reach. Cross-selling across platforms deepens wallet share and integrated mechanical-electronic solutions simplify OEM procurement. Portfolio breadth buffers single-product volatility.

Global, multi-industry reach

Twin Disc's exposure to marine, land-based industrial and energy sectors diversifies demand across cyclical end markets, reducing revenue concentration risk. Its geographic footprint and aftermarket service network mitigate regional downturns and regulatory shocks while supporting uptime-sensitive customers. Scale in niche power transmission segments strengthens supplier negotiating leverage and margin resilience.

Aftermarket and service revenues

Installed base drives recurring parts and service demand, creating a steady revenue stream for Twin Disc.

Higher-margin aftermarket and service sales help smooth revenue through equipment cycles and improve overall margins.

Technical support and field service increase customer stickiness, reducing churn and enabling upsell opportunities.

Field feedback creates a loop that informs product improvements and shortens R&D cycles.

- installed-base recurring demand

- higher-margin aftermarket smoothing

- technical support strengthens stickiness

- feedback informs product R&D

Reputation in harsh environments

Twin Disc (NASDAQ: TWIN) is differentiated by proven reliability in offshore, mining and heavy-construction applications, where uptime trumps lowest upfront cost. Certifications from DNV and ABS and documented operator field hours support performance claims. Reference wins in high-stress projects in 2024 accelerated entry into adjacent applications.

- Reliability: offshore/mining/construction

- Certifications: DNV, ABS

- Value: reduced downtime over price

- 2024 reference wins fuel expansion

105+ years of high-torque drivetrain expertise; recurring aftermarket sales; FY2024 $184.1M

Twin Disc's 105+ years of specialization in high-torque, harsh-environment power transmission underpins strong credibility and premium pricing. Proven reliability and installed base drive recurring aftermarket sales; fiscal 2024 net sales were $184.1 million. Broad portfolio serves marine, energy and off-highway markets with DNV and ABS certifications.

| Founded | FY2024 Net Sales | Key Sectors | Certifications |

|---|---|---|---|

| 1918 | $184.1M | Marine, Energy, Off-highway | DNV, ABS |

What is included in the product

Delivers a strategic overview of Twin Disc’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess competitive positioning, growth drivers and risks shaping its marine and industrial drivetrain and control systems business.

Provides a concise Twin Disc SWOT matrix that quickly surfaces strengths, weaknesses, opportunities, and threats to relieve strategic analysis bottlenecks and speed stakeholder alignment.

Weaknesses

Cyclical end-market exposure

Marine and energy capital spending is highly volatile, leaving Twin Disc exposed to cyclical swings as project-driven orders produce lumpy revenue and uneven capacity utilization; OEM budget freezes frequently delay large orders and complicate cash flow timing, while forecasting and inventory management become more complex and error-prone during downturns.

Limited scale vs. larger competitors

Smaller R&D and marketing budgets at Twin Disc (Nasdaq: TWIN) — a company with market cap under $1 billion and annual revenue below $500 million — constrain speed in adopting new propulsion and control technologies. Weaker purchasing power raises input costs amid 2024 US CPI ~3.4%, squeezing sourcing versus larger OEMs. Thinner global distribution in emerging markets limits aftermarket growth, and competing on price pressures already-tight margins.

Concentration in heavy equipment niches

Dependence on heavy-duty marine and off-highway segments (notably highlighted in Twin Disc's FY2024 disclosures) limits diversification into faster-growing light-industrial markets, constraining revenue mix flexibility. Demand shocks in these core niches can disproportionately swing quarterly results and margins. Specialized, highly customized drivetrain designs lengthen development cycles and raise engineering and aftermarket support overhead.

Exposure to commodity and freight costs

Exposure to commodity and freight costs drives volatility for Twin Disc as steel and precision components account for a large share of input spend; supply-chain disruptions persisted into 2024, raising lead times and expedite fees. Attempts to pass surcharges risk customer friction and contract churn, while fixed-price agreements create margin compression when input or freight costs spike.

- Steel/precision inputs: high volatility

- Long chains → delays & expedite fees

- Surcharges risk customer pushback

- Fixed-price contracts cause margin squeeze

Legacy platform complexity

Supporting a broad set of legacy Twin Disc models in 2024–25 continues to strain engineering resources and parts inventories, increasing sourcing complexity and lead times.

Active obsolescence management has pushed working capital requirements higher as slow-moving stock and parts redesigns absorb cash.

Backward compatibility demands slow design modernization and global documentation and training burdens persist across service networks.

- legacy inventory pressure

- higher working capital

- slower product modernization

- ongoing global training/documentation costs

Cyclic marine/energy demand makes revenue lumpy; small OEM <$1B, revenue <$500M

Twin Disc (TWIN) faces cyclic marine/energy demand, creating lumpy revenue and uneven capacity utilization. Market cap under $1B and annual revenue below $500M limit R&D, sourcing scale and margin resilience versus larger OEMs. Legacy model support raises inventory and working capital needs, while steel/precision input volatility and freight disrupt costs and delivery.

| Metric | Value |

|---|---|

| Market cap | <$1B |

| Annual revenue | <$500M |

| US CPI 2024 | ~3.4% |

Preview Before You Purchase

Twin Disc SWOT Analysis

This is the actual Twin Disc SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable file with full details, structured findings, and actionable insights for strategic decision-making.

Make Insightful Decisions Backed by Expert Research

Twin Disc’s SWOT snapshot highlights robust marine and off‑highway market positions, supply-chain sensitivities, and growth opportunities in electrification and aftermarket services. Want deeper competitive, financial, and strategic analysis? Purchase the full SWOT to receive a research‑backed, editable Word report and Excel matrix—ready for investor pitches, planning, or due diligence.

Strengths

Heavy-duty engineering pedigree

Founded in 1918, Twin Disc's century-plus specialization in high-torque, harsh-environment power transmission builds strong credibility with marine, energy and off-highway customers. Proven reliability in mission-critical applications reduces lifecycle costs and supports aftermarket repeat business. The engineering moat is hard for generalists to replicate and underpins premium pricing for Twin Disc (ticker TWIN on NASDAQ).

Broad product portfolio

Marine transmissions, azimuth drives, clutches, power-shift transmissions and electronic controls let Twin Disc address multiple drive-line needs across commercial and recreational markets; the company reported approximately $184.1 million in net sales for fiscal 2024, underscoring product reach. Cross-selling across platforms deepens wallet share and integrated mechanical-electronic solutions simplify OEM procurement. Portfolio breadth buffers single-product volatility.

Global, multi-industry reach

Twin Disc's exposure to marine, land-based industrial and energy sectors diversifies demand across cyclical end markets, reducing revenue concentration risk. Its geographic footprint and aftermarket service network mitigate regional downturns and regulatory shocks while supporting uptime-sensitive customers. Scale in niche power transmission segments strengthens supplier negotiating leverage and margin resilience.

Aftermarket and service revenues

Installed base drives recurring parts and service demand, creating a steady revenue stream for Twin Disc.

Higher-margin aftermarket and service sales help smooth revenue through equipment cycles and improve overall margins.

Technical support and field service increase customer stickiness, reducing churn and enabling upsell opportunities.

Field feedback creates a loop that informs product improvements and shortens R&D cycles.

- installed-base recurring demand

- higher-margin aftermarket smoothing

- technical support strengthens stickiness

- feedback informs product R&D

Reputation in harsh environments

Twin Disc (NASDAQ: TWIN) is differentiated by proven reliability in offshore, mining and heavy-construction applications, where uptime trumps lowest upfront cost. Certifications from DNV and ABS and documented operator field hours support performance claims. Reference wins in high-stress projects in 2024 accelerated entry into adjacent applications.

- Reliability: offshore/mining/construction

- Certifications: DNV, ABS

- Value: reduced downtime over price

- 2024 reference wins fuel expansion

105+ years of high-torque drivetrain expertise; recurring aftermarket sales; FY2024 $184.1M

Twin Disc's 105+ years of specialization in high-torque, harsh-environment power transmission underpins strong credibility and premium pricing. Proven reliability and installed base drive recurring aftermarket sales; fiscal 2024 net sales were $184.1 million. Broad portfolio serves marine, energy and off-highway markets with DNV and ABS certifications.

| Founded | FY2024 Net Sales | Key Sectors | Certifications |

|---|---|---|---|

| 1918 | $184.1M | Marine, Energy, Off-highway | DNV, ABS |

What is included in the product

Delivers a strategic overview of Twin Disc’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess competitive positioning, growth drivers and risks shaping its marine and industrial drivetrain and control systems business.

Provides a concise Twin Disc SWOT matrix that quickly surfaces strengths, weaknesses, opportunities, and threats to relieve strategic analysis bottlenecks and speed stakeholder alignment.

Weaknesses

Cyclical end-market exposure

Marine and energy capital spending is highly volatile, leaving Twin Disc exposed to cyclical swings as project-driven orders produce lumpy revenue and uneven capacity utilization; OEM budget freezes frequently delay large orders and complicate cash flow timing, while forecasting and inventory management become more complex and error-prone during downturns.

Limited scale vs. larger competitors

Smaller R&D and marketing budgets at Twin Disc (Nasdaq: TWIN) — a company with market cap under $1 billion and annual revenue below $500 million — constrain speed in adopting new propulsion and control technologies. Weaker purchasing power raises input costs amid 2024 US CPI ~3.4%, squeezing sourcing versus larger OEMs. Thinner global distribution in emerging markets limits aftermarket growth, and competing on price pressures already-tight margins.

Concentration in heavy equipment niches

Dependence on heavy-duty marine and off-highway segments (notably highlighted in Twin Disc's FY2024 disclosures) limits diversification into faster-growing light-industrial markets, constraining revenue mix flexibility. Demand shocks in these core niches can disproportionately swing quarterly results and margins. Specialized, highly customized drivetrain designs lengthen development cycles and raise engineering and aftermarket support overhead.

Exposure to commodity and freight costs

Exposure to commodity and freight costs drives volatility for Twin Disc as steel and precision components account for a large share of input spend; supply-chain disruptions persisted into 2024, raising lead times and expedite fees. Attempts to pass surcharges risk customer friction and contract churn, while fixed-price agreements create margin compression when input or freight costs spike.

- Steel/precision inputs: high volatility

- Long chains → delays & expedite fees

- Surcharges risk customer pushback

- Fixed-price contracts cause margin squeeze

Legacy platform complexity

Supporting a broad set of legacy Twin Disc models in 2024–25 continues to strain engineering resources and parts inventories, increasing sourcing complexity and lead times.

Active obsolescence management has pushed working capital requirements higher as slow-moving stock and parts redesigns absorb cash.

Backward compatibility demands slow design modernization and global documentation and training burdens persist across service networks.

- legacy inventory pressure

- higher working capital

- slower product modernization

- ongoing global training/documentation costs

Cyclic marine/energy demand makes revenue lumpy; small OEM <$1B, revenue <$500M

Twin Disc (TWIN) faces cyclic marine/energy demand, creating lumpy revenue and uneven capacity utilization. Market cap under $1B and annual revenue below $500M limit R&D, sourcing scale and margin resilience versus larger OEMs. Legacy model support raises inventory and working capital needs, while steel/precision input volatility and freight disrupt costs and delivery.

| Metric | Value |

|---|---|

| Market cap | <$1B |

| Annual revenue | <$500M |

| US CPI 2024 | ~3.4% |

Preview Before You Purchase

Twin Disc SWOT Analysis

This is the actual Twin Disc SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable file with full details, structured findings, and actionable insights for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Twin Disc’s SWOT snapshot highlights robust marine and off‑highway market positions, supply-chain sensitivities, and growth opportunities in electrification and aftermarket services. Want deeper competitive, financial, and strategic analysis? Purchase the full SWOT to receive a research‑backed, editable Word report and Excel matrix—ready for investor pitches, planning, or due diligence.

Strengths

Heavy-duty engineering pedigree

Founded in 1918, Twin Disc's century-plus specialization in high-torque, harsh-environment power transmission builds strong credibility with marine, energy and off-highway customers. Proven reliability in mission-critical applications reduces lifecycle costs and supports aftermarket repeat business. The engineering moat is hard for generalists to replicate and underpins premium pricing for Twin Disc (ticker TWIN on NASDAQ).

Broad product portfolio

Marine transmissions, azimuth drives, clutches, power-shift transmissions and electronic controls let Twin Disc address multiple drive-line needs across commercial and recreational markets; the company reported approximately $184.1 million in net sales for fiscal 2024, underscoring product reach. Cross-selling across platforms deepens wallet share and integrated mechanical-electronic solutions simplify OEM procurement. Portfolio breadth buffers single-product volatility.

Global, multi-industry reach

Twin Disc's exposure to marine, land-based industrial and energy sectors diversifies demand across cyclical end markets, reducing revenue concentration risk. Its geographic footprint and aftermarket service network mitigate regional downturns and regulatory shocks while supporting uptime-sensitive customers. Scale in niche power transmission segments strengthens supplier negotiating leverage and margin resilience.

Aftermarket and service revenues

Installed base drives recurring parts and service demand, creating a steady revenue stream for Twin Disc.

Higher-margin aftermarket and service sales help smooth revenue through equipment cycles and improve overall margins.

Technical support and field service increase customer stickiness, reducing churn and enabling upsell opportunities.

Field feedback creates a loop that informs product improvements and shortens R&D cycles.

- installed-base recurring demand

- higher-margin aftermarket smoothing

- technical support strengthens stickiness

- feedback informs product R&D

Reputation in harsh environments

Twin Disc (NASDAQ: TWIN) is differentiated by proven reliability in offshore, mining and heavy-construction applications, where uptime trumps lowest upfront cost. Certifications from DNV and ABS and documented operator field hours support performance claims. Reference wins in high-stress projects in 2024 accelerated entry into adjacent applications.

- Reliability: offshore/mining/construction

- Certifications: DNV, ABS

- Value: reduced downtime over price

- 2024 reference wins fuel expansion

105+ years of high-torque drivetrain expertise; recurring aftermarket sales; FY2024 $184.1M

Twin Disc's 105+ years of specialization in high-torque, harsh-environment power transmission underpins strong credibility and premium pricing. Proven reliability and installed base drive recurring aftermarket sales; fiscal 2024 net sales were $184.1 million. Broad portfolio serves marine, energy and off-highway markets with DNV and ABS certifications.

| Founded | FY2024 Net Sales | Key Sectors | Certifications |

|---|---|---|---|

| 1918 | $184.1M | Marine, Energy, Off-highway | DNV, ABS |

What is included in the product

Delivers a strategic overview of Twin Disc’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess competitive positioning, growth drivers and risks shaping its marine and industrial drivetrain and control systems business.

Provides a concise Twin Disc SWOT matrix that quickly surfaces strengths, weaknesses, opportunities, and threats to relieve strategic analysis bottlenecks and speed stakeholder alignment.

Weaknesses

Cyclical end-market exposure

Marine and energy capital spending is highly volatile, leaving Twin Disc exposed to cyclical swings as project-driven orders produce lumpy revenue and uneven capacity utilization; OEM budget freezes frequently delay large orders and complicate cash flow timing, while forecasting and inventory management become more complex and error-prone during downturns.

Limited scale vs. larger competitors

Smaller R&D and marketing budgets at Twin Disc (Nasdaq: TWIN) — a company with market cap under $1 billion and annual revenue below $500 million — constrain speed in adopting new propulsion and control technologies. Weaker purchasing power raises input costs amid 2024 US CPI ~3.4%, squeezing sourcing versus larger OEMs. Thinner global distribution in emerging markets limits aftermarket growth, and competing on price pressures already-tight margins.

Concentration in heavy equipment niches

Dependence on heavy-duty marine and off-highway segments (notably highlighted in Twin Disc's FY2024 disclosures) limits diversification into faster-growing light-industrial markets, constraining revenue mix flexibility. Demand shocks in these core niches can disproportionately swing quarterly results and margins. Specialized, highly customized drivetrain designs lengthen development cycles and raise engineering and aftermarket support overhead.

Exposure to commodity and freight costs

Exposure to commodity and freight costs drives volatility for Twin Disc as steel and precision components account for a large share of input spend; supply-chain disruptions persisted into 2024, raising lead times and expedite fees. Attempts to pass surcharges risk customer friction and contract churn, while fixed-price agreements create margin compression when input or freight costs spike.

- Steel/precision inputs: high volatility

- Long chains → delays & expedite fees

- Surcharges risk customer pushback

- Fixed-price contracts cause margin squeeze

Legacy platform complexity

Supporting a broad set of legacy Twin Disc models in 2024–25 continues to strain engineering resources and parts inventories, increasing sourcing complexity and lead times.

Active obsolescence management has pushed working capital requirements higher as slow-moving stock and parts redesigns absorb cash.

Backward compatibility demands slow design modernization and global documentation and training burdens persist across service networks.

- legacy inventory pressure

- higher working capital

- slower product modernization

- ongoing global training/documentation costs

Cyclic marine/energy demand makes revenue lumpy; small OEM <$1B, revenue <$500M

Twin Disc (TWIN) faces cyclic marine/energy demand, creating lumpy revenue and uneven capacity utilization. Market cap under $1B and annual revenue below $500M limit R&D, sourcing scale and margin resilience versus larger OEMs. Legacy model support raises inventory and working capital needs, while steel/precision input volatility and freight disrupt costs and delivery.

| Metric | Value |

|---|---|

| Market cap | <$1B |

| Annual revenue | <$500M |

| US CPI 2024 | ~3.4% |

Preview Before You Purchase

Twin Disc SWOT Analysis

This is the actual Twin Disc SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable file with full details, structured findings, and actionable insights for strategic decision-making.