TXT e-solutions Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

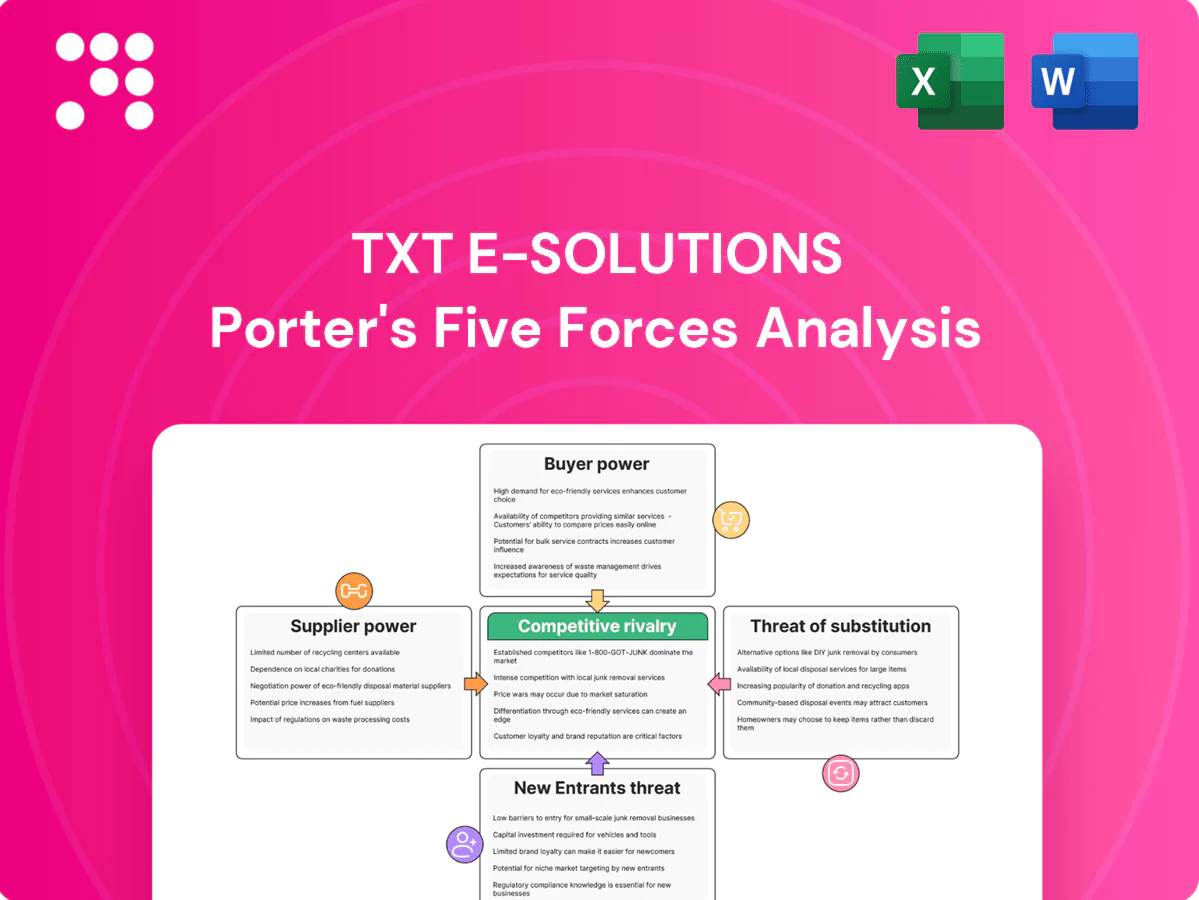

This snapshot highlights key competitive pressures facing TXT e-solutions—buyer and supplier power, rivalry, substitutes and entry threats. It flags strategic levers TXT can use to protect margins and grow. Ready for deeper, force-by-force ratings, visuals and implications? Unlock the full Porter's Five Forces Analysis for the complete, consultant-grade report.

Suppliers Bargaining Power

Scarce certified talent

DO-178C/DO-254 and security-cleared engineers remain scarce, increasing supplier leverage; ISC2 reported a 2023 cybersecurity workforce gap of about 3.4 million, underscoring talent tightness. Wage inflation and retention premiums lift delivery costs and compress margins. TXT offsets this with training pipelines and mixed on/near/offshore staffing, but sudden attrition spikes can still disrupt project schedules.

Concentrated software tooling

Core PLM/CAD/ALM stacks are highly concentrated—Siemens, Dassault and PTC together control roughly 60%+ of enterprise PLM market share in 2024—creating dependency and price stickiness. License terms, complex integrations and typical seat costs of $5k–$25k drive switching costs and renewal leverage. Multi-vendor competence and negotiated enterprise agreements can moderate supplier power, but certification and validated‑version requirements often lock firms to specific vendors and releases.

Specialized testing hardware

HIL rigs, avionics benches and compliance labs are niche with 2024 industry averages showing HIL lead times of 6–9 months and test-facility utilization above 85%, boosting supplier leverage. Bespoke setups commonly add ~20% to equipment cost and extend timelines, so early booking and framework agreements are used to secure slots. Despite contracts, project delays still occur from bottlenecked test resources.

Cloud and cybersecurity providers

Secure cloud, DevSecOps and sovereign hosting are mandatory in defense, sharply limiting supplier alternatives; Flexera 2024 reports 93% enterprise multi-cloud adoption but defense often restricts to certified sovereign providers. Providers can embed price escalators and egress fees (AWS egress ~$0.09/GB for first 10TB). Reserved instances reduce dependence, offering up to 72% compute savings.

- Compliance narrows substitution options

- Sovereign hosting required in defense

- Multi-cloud adoption 93% (Flexera 2024)

- Reserved instances save up to 72%

- Egress fees ~0.09 USD/GB

Subcontractors and niche SMEs

Peak-load delivery depends on specialized SMEs for subsystems and certifications; 99.8% of EU firms were SMEs in 2024 (Eurostat), concentrating niche capabilities and allowing higher per-hour rates and scheduling leverage. Long-term call-offs and preferred-vendor lists can reduce costs and secure capacity, but strict quality oversight is essential to avoid costly rework.

- SME concentration: 99.8% of EU firms (Eurostat 2024)

- Preferred vendors: lower rates, improved availability

- Quality oversight: reduces rework risk

Supplier power high: talent gap ~3.4M, PLM oligopoly

Supplier power is high: certified DO-178C/DO-254 engineers scarce with 2023 cyber gap ~3.4M, driving wage inflation and attrition risk. PLM vendors (Siemens/Dassault/PTC) hold 60%+ market share, raising switching costs. HIL lead times 6–9 months and cloud egress ~$0.09/GB concentrate leverage.

| Metric | Value | Source |

|---|---|---|

| Cyber workforce gap | 3.4M | ISC2 2023 |

| PLM market share | 60%+ | 2024 market data |

| HIL lead time | 6–9 months | 2024 industry avg |

| Cloud egress | $0.09/GB | AWS 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for TXT e-solutions that uncovers key drivers of competition, customer influence, and market entry risks specific to its software and services niche. Detailed evaluation identifies disruptive threats, supplier/buyer power, substitute pressures, and barriers protecting incumbency to inform strategic decisions and investor materials.

A one-sheet Porter's Five Forces summary for TXT e-solutions that visualizes competitive pressure with an editable spider chart and customizable scores—ready to drop into decks, adapt for scenario analysis, and use without complex code.

Customers Bargaining Power

Large OEM and defense primes

Large OEMs and defense primes are few, highly sophisticated buyers (eg Lockheed Martin, Raytheon, BAE), giving them strong negotiating leverage and driving competitive RFPs that force price-by-volume dynamics and strict penalty clauses.

They routinely demand volume discounts and liquidated-damages provisions; access to high-profile programs and referenceability enables suppliers to charge sharper pricing despite pressure.

Deep relationships and proven past performance often soften price concessions, preserving margin on strategic contracts.

High switching costs but disciplined buyers

Integration, IP ownership, and certification track records (ISO/AS standards) raise switching costs after 12–18 months of engagement, but institutionalized buyer rotations (typically every 3–5 years) limit lock-in. Multi-year MSAs (3–5 years) set pricing guardrails while enforcing tough SLAs; value must be tied to schedule, quality, and compliance KPIs to justify premium pricing.

Outcome-based contracts

Outcome-based contracts shift performance risk to vendors, with 2024 industry surveys showing ~35% of enterprise deals tying fees to milestones or outcomes; underbids and scope creep can erode margins by up to 15% if unmanaged. Robust change control and earned value tracking are critical to protect margins and cash flow. Differentiation via domain accelerators raises win rates and reduces the need for deep discounts, preserving average contract value.

Vendor consolidation trends

Primes are consolidating suppliers to tighten governance and security, pressuring margins as larger deals shift volume to fewer partners; the global IT outsourcing market approached 400 billion USD in 2024, amplifying buyer leverage. Cross-portfolio capabilities and demonstrable secure, compliant global delivery footprints are now table stakes for TXT.

- Supply consolidation: higher volume, lower pricing

- Security/compliance: NIS2 and global standards demand

- Capability: cross-portfolio delivery required

- TXT focus: prove secure, global delivery

Security and compliance demands

Defense-grade infosec and export controls (NIST SP 800-171, DFARS; CMMC 2.0 rollout in 2024) plus mandatory audits raise delivery costs for TXT e-solutions and are routinely flowed down by buyers through contracts and ITAR/DFARS clauses. Certifications like ISO 27001 and CMMI are treated as prerequisites rather than differentiators; proactive compliance reduces buyers' renegotiation leverage and bid disqualification risk.

- Mandatory standards: NIST SP 800-171, DFARS, CMMC 2.0 (2024)

- Common prerequisites: ISO 27001, CMMI (vendor minimums)

- Buyer leverage lowered when vendors maintain proactive, audited compliance

Certifications, IP and multi-year MSAs guard margins as outcome-based deals reach 35%

Large, sophisticated OEMs (few buyers) exert strong price leverage; TXT must win via certifications, IP and multi-year MSAs to protect margins. 2024: outcome-based deals ~35%, global IT outsourcing ~$400B; underbids/scope creep can cut margins up to 15%. Supplier consolidation and mandatory standards (CMMC 2.0, NIST SP 800-171) raise switching costs and compliance spend.

| Metric | 2024 |

|---|---|

| Outcome-based deals | ~35% |

| Global IT outsourcing | ~400B USD |

| Margin erosion risk | Up to 15% |

| Key standards | CMMC 2.0, NIST SP 800-171, ISO 27001 |

Preview Before You Purchase

TXT e-solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for TXT e-solutions you'll receive after purchase—fully formatted, professionally written, and ready for immediate use. It contains the same in-depth competitive assessment, force-by-force scoring, and actionable implications included in the delivered file. No samples or placeholders: buy and download this exact document instantly.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights key competitive pressures facing TXT e-solutions—buyer and supplier power, rivalry, substitutes and entry threats. It flags strategic levers TXT can use to protect margins and grow. Ready for deeper, force-by-force ratings, visuals and implications? Unlock the full Porter's Five Forces Analysis for the complete, consultant-grade report.

Suppliers Bargaining Power

Scarce certified talent

DO-178C/DO-254 and security-cleared engineers remain scarce, increasing supplier leverage; ISC2 reported a 2023 cybersecurity workforce gap of about 3.4 million, underscoring talent tightness. Wage inflation and retention premiums lift delivery costs and compress margins. TXT offsets this with training pipelines and mixed on/near/offshore staffing, but sudden attrition spikes can still disrupt project schedules.

Concentrated software tooling

Core PLM/CAD/ALM stacks are highly concentrated—Siemens, Dassault and PTC together control roughly 60%+ of enterprise PLM market share in 2024—creating dependency and price stickiness. License terms, complex integrations and typical seat costs of $5k–$25k drive switching costs and renewal leverage. Multi-vendor competence and negotiated enterprise agreements can moderate supplier power, but certification and validated‑version requirements often lock firms to specific vendors and releases.

Specialized testing hardware

HIL rigs, avionics benches and compliance labs are niche with 2024 industry averages showing HIL lead times of 6–9 months and test-facility utilization above 85%, boosting supplier leverage. Bespoke setups commonly add ~20% to equipment cost and extend timelines, so early booking and framework agreements are used to secure slots. Despite contracts, project delays still occur from bottlenecked test resources.

Cloud and cybersecurity providers

Secure cloud, DevSecOps and sovereign hosting are mandatory in defense, sharply limiting supplier alternatives; Flexera 2024 reports 93% enterprise multi-cloud adoption but defense often restricts to certified sovereign providers. Providers can embed price escalators and egress fees (AWS egress ~$0.09/GB for first 10TB). Reserved instances reduce dependence, offering up to 72% compute savings.

- Compliance narrows substitution options

- Sovereign hosting required in defense

- Multi-cloud adoption 93% (Flexera 2024)

- Reserved instances save up to 72%

- Egress fees ~0.09 USD/GB

Subcontractors and niche SMEs

Peak-load delivery depends on specialized SMEs for subsystems and certifications; 99.8% of EU firms were SMEs in 2024 (Eurostat), concentrating niche capabilities and allowing higher per-hour rates and scheduling leverage. Long-term call-offs and preferred-vendor lists can reduce costs and secure capacity, but strict quality oversight is essential to avoid costly rework.

- SME concentration: 99.8% of EU firms (Eurostat 2024)

- Preferred vendors: lower rates, improved availability

- Quality oversight: reduces rework risk

Supplier power high: talent gap ~3.4M, PLM oligopoly

Supplier power is high: certified DO-178C/DO-254 engineers scarce with 2023 cyber gap ~3.4M, driving wage inflation and attrition risk. PLM vendors (Siemens/Dassault/PTC) hold 60%+ market share, raising switching costs. HIL lead times 6–9 months and cloud egress ~$0.09/GB concentrate leverage.

| Metric | Value | Source |

|---|---|---|

| Cyber workforce gap | 3.4M | ISC2 2023 |

| PLM market share | 60%+ | 2024 market data |

| HIL lead time | 6–9 months | 2024 industry avg |

| Cloud egress | $0.09/GB | AWS 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for TXT e-solutions that uncovers key drivers of competition, customer influence, and market entry risks specific to its software and services niche. Detailed evaluation identifies disruptive threats, supplier/buyer power, substitute pressures, and barriers protecting incumbency to inform strategic decisions and investor materials.

A one-sheet Porter's Five Forces summary for TXT e-solutions that visualizes competitive pressure with an editable spider chart and customizable scores—ready to drop into decks, adapt for scenario analysis, and use without complex code.

Customers Bargaining Power

Large OEM and defense primes

Large OEMs and defense primes are few, highly sophisticated buyers (eg Lockheed Martin, Raytheon, BAE), giving them strong negotiating leverage and driving competitive RFPs that force price-by-volume dynamics and strict penalty clauses.

They routinely demand volume discounts and liquidated-damages provisions; access to high-profile programs and referenceability enables suppliers to charge sharper pricing despite pressure.

Deep relationships and proven past performance often soften price concessions, preserving margin on strategic contracts.

High switching costs but disciplined buyers

Integration, IP ownership, and certification track records (ISO/AS standards) raise switching costs after 12–18 months of engagement, but institutionalized buyer rotations (typically every 3–5 years) limit lock-in. Multi-year MSAs (3–5 years) set pricing guardrails while enforcing tough SLAs; value must be tied to schedule, quality, and compliance KPIs to justify premium pricing.

Outcome-based contracts

Outcome-based contracts shift performance risk to vendors, with 2024 industry surveys showing ~35% of enterprise deals tying fees to milestones or outcomes; underbids and scope creep can erode margins by up to 15% if unmanaged. Robust change control and earned value tracking are critical to protect margins and cash flow. Differentiation via domain accelerators raises win rates and reduces the need for deep discounts, preserving average contract value.

Vendor consolidation trends

Primes are consolidating suppliers to tighten governance and security, pressuring margins as larger deals shift volume to fewer partners; the global IT outsourcing market approached 400 billion USD in 2024, amplifying buyer leverage. Cross-portfolio capabilities and demonstrable secure, compliant global delivery footprints are now table stakes for TXT.

- Supply consolidation: higher volume, lower pricing

- Security/compliance: NIS2 and global standards demand

- Capability: cross-portfolio delivery required

- TXT focus: prove secure, global delivery

Security and compliance demands

Defense-grade infosec and export controls (NIST SP 800-171, DFARS; CMMC 2.0 rollout in 2024) plus mandatory audits raise delivery costs for TXT e-solutions and are routinely flowed down by buyers through contracts and ITAR/DFARS clauses. Certifications like ISO 27001 and CMMI are treated as prerequisites rather than differentiators; proactive compliance reduces buyers' renegotiation leverage and bid disqualification risk.

- Mandatory standards: NIST SP 800-171, DFARS, CMMC 2.0 (2024)

- Common prerequisites: ISO 27001, CMMI (vendor minimums)

- Buyer leverage lowered when vendors maintain proactive, audited compliance

Certifications, IP and multi-year MSAs guard margins as outcome-based deals reach 35%

Large, sophisticated OEMs (few buyers) exert strong price leverage; TXT must win via certifications, IP and multi-year MSAs to protect margins. 2024: outcome-based deals ~35%, global IT outsourcing ~$400B; underbids/scope creep can cut margins up to 15%. Supplier consolidation and mandatory standards (CMMC 2.0, NIST SP 800-171) raise switching costs and compliance spend.

| Metric | 2024 |

|---|---|

| Outcome-based deals | ~35% |

| Global IT outsourcing | ~400B USD |

| Margin erosion risk | Up to 15% |

| Key standards | CMMC 2.0, NIST SP 800-171, ISO 27001 |

Preview Before You Purchase

TXT e-solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for TXT e-solutions you'll receive after purchase—fully formatted, professionally written, and ready for immediate use. It contains the same in-depth competitive assessment, force-by-force scoring, and actionable implications included in the delivered file. No samples or placeholders: buy and download this exact document instantly.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot highlights key competitive pressures facing TXT e-solutions—buyer and supplier power, rivalry, substitutes and entry threats. It flags strategic levers TXT can use to protect margins and grow. Ready for deeper, force-by-force ratings, visuals and implications? Unlock the full Porter's Five Forces Analysis for the complete, consultant-grade report.

Suppliers Bargaining Power

Scarce certified talent

DO-178C/DO-254 and security-cleared engineers remain scarce, increasing supplier leverage; ISC2 reported a 2023 cybersecurity workforce gap of about 3.4 million, underscoring talent tightness. Wage inflation and retention premiums lift delivery costs and compress margins. TXT offsets this with training pipelines and mixed on/near/offshore staffing, but sudden attrition spikes can still disrupt project schedules.

Concentrated software tooling

Core PLM/CAD/ALM stacks are highly concentrated—Siemens, Dassault and PTC together control roughly 60%+ of enterprise PLM market share in 2024—creating dependency and price stickiness. License terms, complex integrations and typical seat costs of $5k–$25k drive switching costs and renewal leverage. Multi-vendor competence and negotiated enterprise agreements can moderate supplier power, but certification and validated‑version requirements often lock firms to specific vendors and releases.

Specialized testing hardware

HIL rigs, avionics benches and compliance labs are niche with 2024 industry averages showing HIL lead times of 6–9 months and test-facility utilization above 85%, boosting supplier leverage. Bespoke setups commonly add ~20% to equipment cost and extend timelines, so early booking and framework agreements are used to secure slots. Despite contracts, project delays still occur from bottlenecked test resources.

Cloud and cybersecurity providers

Secure cloud, DevSecOps and sovereign hosting are mandatory in defense, sharply limiting supplier alternatives; Flexera 2024 reports 93% enterprise multi-cloud adoption but defense often restricts to certified sovereign providers. Providers can embed price escalators and egress fees (AWS egress ~$0.09/GB for first 10TB). Reserved instances reduce dependence, offering up to 72% compute savings.

- Compliance narrows substitution options

- Sovereign hosting required in defense

- Multi-cloud adoption 93% (Flexera 2024)

- Reserved instances save up to 72%

- Egress fees ~0.09 USD/GB

Subcontractors and niche SMEs

Peak-load delivery depends on specialized SMEs for subsystems and certifications; 99.8% of EU firms were SMEs in 2024 (Eurostat), concentrating niche capabilities and allowing higher per-hour rates and scheduling leverage. Long-term call-offs and preferred-vendor lists can reduce costs and secure capacity, but strict quality oversight is essential to avoid costly rework.

- SME concentration: 99.8% of EU firms (Eurostat 2024)

- Preferred vendors: lower rates, improved availability

- Quality oversight: reduces rework risk

Supplier power high: talent gap ~3.4M, PLM oligopoly

Supplier power is high: certified DO-178C/DO-254 engineers scarce with 2023 cyber gap ~3.4M, driving wage inflation and attrition risk. PLM vendors (Siemens/Dassault/PTC) hold 60%+ market share, raising switching costs. HIL lead times 6–9 months and cloud egress ~$0.09/GB concentrate leverage.

| Metric | Value | Source |

|---|---|---|

| Cyber workforce gap | 3.4M | ISC2 2023 |

| PLM market share | 60%+ | 2024 market data |

| HIL lead time | 6–9 months | 2024 industry avg |

| Cloud egress | $0.09/GB | AWS 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for TXT e-solutions that uncovers key drivers of competition, customer influence, and market entry risks specific to its software and services niche. Detailed evaluation identifies disruptive threats, supplier/buyer power, substitute pressures, and barriers protecting incumbency to inform strategic decisions and investor materials.

A one-sheet Porter's Five Forces summary for TXT e-solutions that visualizes competitive pressure with an editable spider chart and customizable scores—ready to drop into decks, adapt for scenario analysis, and use without complex code.

Customers Bargaining Power

Large OEM and defense primes

Large OEMs and defense primes are few, highly sophisticated buyers (eg Lockheed Martin, Raytheon, BAE), giving them strong negotiating leverage and driving competitive RFPs that force price-by-volume dynamics and strict penalty clauses.

They routinely demand volume discounts and liquidated-damages provisions; access to high-profile programs and referenceability enables suppliers to charge sharper pricing despite pressure.

Deep relationships and proven past performance often soften price concessions, preserving margin on strategic contracts.

High switching costs but disciplined buyers

Integration, IP ownership, and certification track records (ISO/AS standards) raise switching costs after 12–18 months of engagement, but institutionalized buyer rotations (typically every 3–5 years) limit lock-in. Multi-year MSAs (3–5 years) set pricing guardrails while enforcing tough SLAs; value must be tied to schedule, quality, and compliance KPIs to justify premium pricing.

Outcome-based contracts

Outcome-based contracts shift performance risk to vendors, with 2024 industry surveys showing ~35% of enterprise deals tying fees to milestones or outcomes; underbids and scope creep can erode margins by up to 15% if unmanaged. Robust change control and earned value tracking are critical to protect margins and cash flow. Differentiation via domain accelerators raises win rates and reduces the need for deep discounts, preserving average contract value.

Vendor consolidation trends

Primes are consolidating suppliers to tighten governance and security, pressuring margins as larger deals shift volume to fewer partners; the global IT outsourcing market approached 400 billion USD in 2024, amplifying buyer leverage. Cross-portfolio capabilities and demonstrable secure, compliant global delivery footprints are now table stakes for TXT.

- Supply consolidation: higher volume, lower pricing

- Security/compliance: NIS2 and global standards demand

- Capability: cross-portfolio delivery required

- TXT focus: prove secure, global delivery

Security and compliance demands

Defense-grade infosec and export controls (NIST SP 800-171, DFARS; CMMC 2.0 rollout in 2024) plus mandatory audits raise delivery costs for TXT e-solutions and are routinely flowed down by buyers through contracts and ITAR/DFARS clauses. Certifications like ISO 27001 and CMMI are treated as prerequisites rather than differentiators; proactive compliance reduces buyers' renegotiation leverage and bid disqualification risk.

- Mandatory standards: NIST SP 800-171, DFARS, CMMC 2.0 (2024)

- Common prerequisites: ISO 27001, CMMI (vendor minimums)

- Buyer leverage lowered when vendors maintain proactive, audited compliance

Certifications, IP and multi-year MSAs guard margins as outcome-based deals reach 35%

Large, sophisticated OEMs (few buyers) exert strong price leverage; TXT must win via certifications, IP and multi-year MSAs to protect margins. 2024: outcome-based deals ~35%, global IT outsourcing ~$400B; underbids/scope creep can cut margins up to 15%. Supplier consolidation and mandatory standards (CMMC 2.0, NIST SP 800-171) raise switching costs and compliance spend.

| Metric | 2024 |

|---|---|

| Outcome-based deals | ~35% |

| Global IT outsourcing | ~400B USD |

| Margin erosion risk | Up to 15% |

| Key standards | CMMC 2.0, NIST SP 800-171, ISO 27001 |

Preview Before You Purchase

TXT e-solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for TXT e-solutions you'll receive after purchase—fully formatted, professionally written, and ready for immediate use. It contains the same in-depth competitive assessment, force-by-force scoring, and actionable implications included in the delivered file. No samples or placeholders: buy and download this exact document instantly.