United Bank Business Model Canvas

Unlock the strategic blueprint of a leading bank business model preview

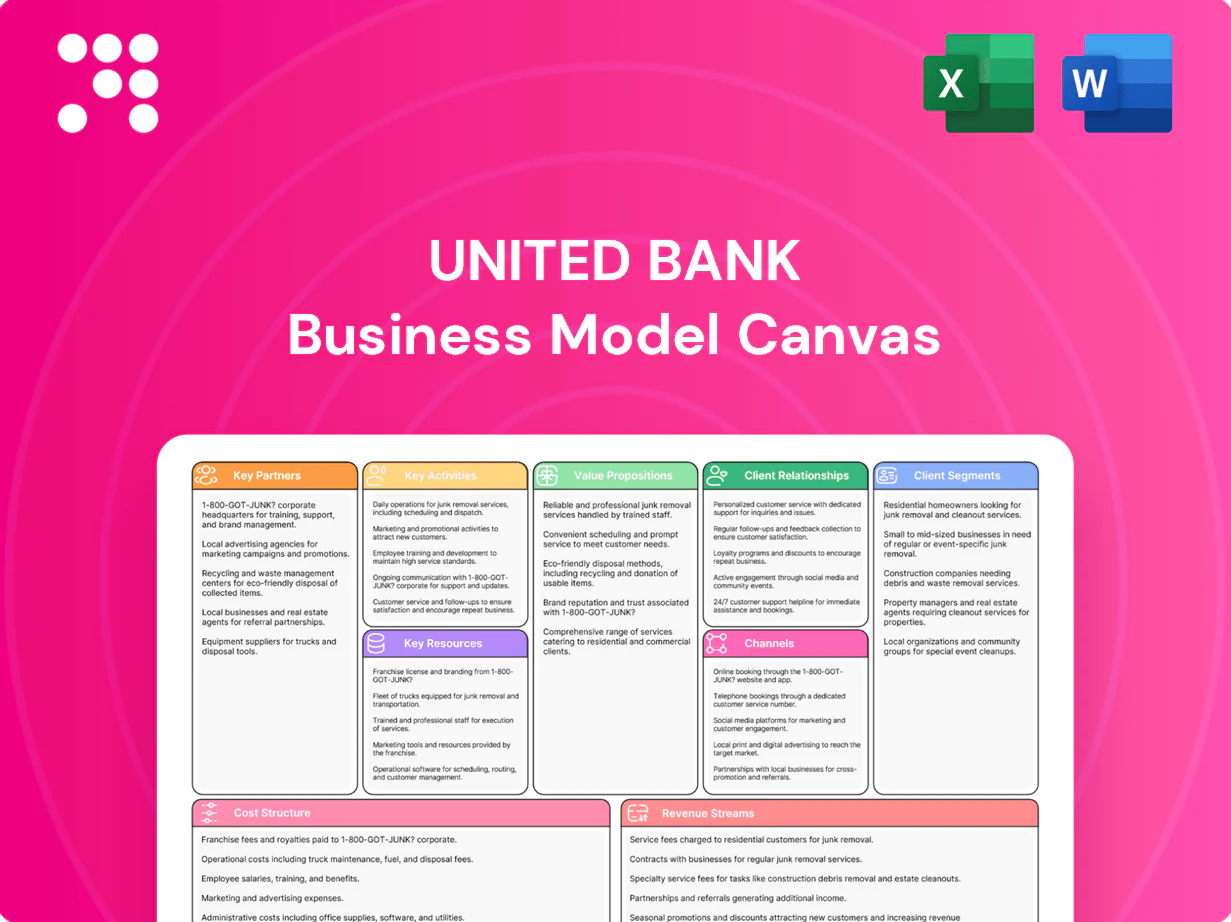

Unlock the strategic blueprint of United Bank's business model with our concise preview. The full Business Model Canvas reveals customer segments, revenue drivers, key partnerships and cost structure to inform investments and strategy. Purchase the complete, editable canvas to analyze, benchmark and apply these actionable insights.

Partnerships

Core Banking Vendors

Partnerships with core banking software providers ensure reliable deposit, loan and ledger processing and support scalability to handle millions of transactions daily. These vendors enable security and regulatory reporting, with SLAs commonly set at 99.9%+ availability. Joint roadmaps accelerate new product rollouts and digital features, while regular compliance audits preserve uptime and data integrity.

Payment Networks

Ties with Visa and Mastercard (covering roughly 80% of global card volume), ACH (30+ billion transactions annually in 2023), RTP (200+ participating banks by 2024) and wire networks (Fedwire avg daily value ~$3.8 trillion in 2023) enable United Bank to issue cards, accept merchants and move funds. These links boost transaction speed and client convenience. Network incentives optimize interchange and fraud tools. Ongoing certification ensures compliance and resilience.

Fintech Integrations

API partnerships with fintechs add P2P payments, personal finance tools and lending analytics, leveraging the open-banking ecosystem that by 2024 processed trillions of dollars in API-enabled transactions globally.

These integrations accelerate time-to-market—often cutting development timelines by roughly half—without heavy in-house build and enable co-branding that broadens reach among digital-first users.

Rigorous due diligence, vendor controls and model-risk frameworks are essential to manage third-party and analytics model risk.

Correspondent Banks

United Bank's correspondent bank relationships deliver liquidity, syndication access, foreign exchange execution and niche trade services, extending product breadth for business and wealth clients and enabling cross-border cash management and FX hedging.

Participation and syndication arrangements diversify credit exposure while negotiated pricing with correspondents enhances client competitiveness on fees and execution.

- Liquidity lines and syndications

- Expanded FX and trade services

- Credit diversification via participation

- Preferential pricing improves client rates

Regulators and Compliance Advisors

Constructive engagement with the OCC, FDIC and Fed underpins safe operations, aligning United Bank with Basel III capital norms (CET1 minimum 4.5% as of 2024) and FDIC deposit insurance limits of 250,000 per depositor. External legal and audit advisors support evolving rule adherence, reducing compliance risk and remediation costs, while proactive dialogue enables timely policy and control updates ahead of stress-test and supervisory expectations for banks above 100 billion in assets.

- Regulatory alignment: CET1 ≥ 4.5% (2024)

- Deposit protection: FDIC limit 250,000

- Supervisory focus: Fed stress tests for >100B banks

Banking partnerships enable payments scale: core SLA 99.9%, cards ~80%

Partnerships with core banking vendors secure deposit, loan and ledger processing with SLAs typically 99.9%+. Card and network ties (Visa/Mastercard ~80% of card volume) plus ACH (30B txns in 2023), RTP (200+ banks by 2024) and Fedwire ($3.8T avg daily value in 2023) enable payments and liquidity. Correspondent banks, syndications and regulators (CET1 ≥4.5% 2024; FDIC limit 250,000) broaden products and reduce risk.

| Partner | Role | Key metric |

|---|---|---|

| Core banking | Processing/scale | SLA 99.9%+ |

| Card networks | Payments | ~80% volume |

| ACH | Clearing | 30B txns (2023) |

| RTP | Real‑time payments | 200+ banks (2024) |

| Fedwire | Wholesale transfer | $3.8T/day (2023) |

| Regulators | Stability/compliance | CET1 ≥4.5% (2024); FDIC 250,000 |

What is included in the product

A concise, pre-built Business Model Canvas for United Bank detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with competitive analysis, SWOT-linked insights and presentation-ready narratives for investors and analysts.

High-level, editable one-page canvas that maps United Bank’s value propositions, channels, and revenue streams—relieves pain by saving hours on structuring models and enabling fast comparisons, collaboration, and executive-ready summaries.

Activities

Deposit Gathering

United Bank focuses on attracting checking, savings, and time deposits to fund loan growth at competitive costs, using targeted community outreach and campaigns to build stable balances. Pricing, promotions, and streamlined digital onboarding accelerate acquisition and lower onboarding costs. Ongoing relationship management and cross-selling improve retention and deposit mix.

Credit Underwriting

Evaluating commercial, consumer, and mortgage credit drives risk-adjusted returns by prioritizing yield versus impairment. Robust policies and machine-learning scoring models maintain portfolio quality and aim to keep losses below peer medians. Continuous monitoring and proactive servicing contain delinquencies amid 2024 US unemployment near 4.0%. Regular stress testing incorporates end-2024 Fed funds at 5.25–5.50% to align risk appetite with macro scenarios.

Wealth and Trust Advisory

Delivering investment management, fiduciary and estate services deepens client relationships and supports retention as wealth management AUM surpassed $100 trillion globally in 2024. Goals-based advice aligns portfolios to long-term outcomes, improving plan adherence and outcomes. Rigorous platform due diligence ensures product suitability and cost efficiency, while regular reviews sustain retention and increase share of wallet.

Digital Banking Operations

- 24/7

- cybersecurity

- UX-optimization

- data-analytics

Regulatory and Risk Management

Compliance, BSA/AML, and operational risk programs protect the franchise by preventing fines and illicit activity; model risk governance oversees credit, pricing, and liquidity tools to ensure decision integrity; internal audit validates control effectiveness through regular testing; capital planning maintains CET1 above the 4.5% regulatory minimum and liquidity planning targets LCR ≥100% per supervisory expectations.

- Compliance & BSA/AML: ongoing monitoring, SAR filing metrics

- Model risk: governance over credit, pricing, liquidity models

- Internal audit: periodic validation of key controls

- Capital & liquidity: CET1 ≥4.5%, LCR ≥100%

Digital deposits 65%, digital transactions 70%, NPLs target 1.1%

United Bank acquires low-cost deposits (65% of loan funding in 2024) via digital onboarding and community campaigns, lowering cost of funds. ML-driven credit scoring and stress testing aim to keep NPLs below 1.1% peer median; Fed funds modeled at 5.25–5.50% (end-2024). Wealth/advisory and digital channels (70% retail digital transactions in 2024) grow fee income and retention.

| Metric | 2024 |

|---|---|

| Deposit funding % | 65% |

| Digital txn share | 70% |

| Peer NPL median | 1.1% |

| Fed funds (modeled) | 5.25–5.50% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact United Bank Business Model Canvas you'll receive after purchase, not a mockup. When you complete your order you'll get the full, editable file formatted exactly as shown. It's ready for immediate download, editing, presenting, or analysis.

Unlock the strategic blueprint of a leading bank business model preview

Unlock the strategic blueprint of United Bank's business model with our concise preview. The full Business Model Canvas reveals customer segments, revenue drivers, key partnerships and cost structure to inform investments and strategy. Purchase the complete, editable canvas to analyze, benchmark and apply these actionable insights.

Partnerships

Core Banking Vendors

Partnerships with core banking software providers ensure reliable deposit, loan and ledger processing and support scalability to handle millions of transactions daily. These vendors enable security and regulatory reporting, with SLAs commonly set at 99.9%+ availability. Joint roadmaps accelerate new product rollouts and digital features, while regular compliance audits preserve uptime and data integrity.

Payment Networks

Ties with Visa and Mastercard (covering roughly 80% of global card volume), ACH (30+ billion transactions annually in 2023), RTP (200+ participating banks by 2024) and wire networks (Fedwire avg daily value ~$3.8 trillion in 2023) enable United Bank to issue cards, accept merchants and move funds. These links boost transaction speed and client convenience. Network incentives optimize interchange and fraud tools. Ongoing certification ensures compliance and resilience.

Fintech Integrations

API partnerships with fintechs add P2P payments, personal finance tools and lending analytics, leveraging the open-banking ecosystem that by 2024 processed trillions of dollars in API-enabled transactions globally.

These integrations accelerate time-to-market—often cutting development timelines by roughly half—without heavy in-house build and enable co-branding that broadens reach among digital-first users.

Rigorous due diligence, vendor controls and model-risk frameworks are essential to manage third-party and analytics model risk.

Correspondent Banks

United Bank's correspondent bank relationships deliver liquidity, syndication access, foreign exchange execution and niche trade services, extending product breadth for business and wealth clients and enabling cross-border cash management and FX hedging.

Participation and syndication arrangements diversify credit exposure while negotiated pricing with correspondents enhances client competitiveness on fees and execution.

- Liquidity lines and syndications

- Expanded FX and trade services

- Credit diversification via participation

- Preferential pricing improves client rates

Regulators and Compliance Advisors

Constructive engagement with the OCC, FDIC and Fed underpins safe operations, aligning United Bank with Basel III capital norms (CET1 minimum 4.5% as of 2024) and FDIC deposit insurance limits of 250,000 per depositor. External legal and audit advisors support evolving rule adherence, reducing compliance risk and remediation costs, while proactive dialogue enables timely policy and control updates ahead of stress-test and supervisory expectations for banks above 100 billion in assets.

- Regulatory alignment: CET1 ≥ 4.5% (2024)

- Deposit protection: FDIC limit 250,000

- Supervisory focus: Fed stress tests for >100B banks

Banking partnerships enable payments scale: core SLA 99.9%, cards ~80%

Partnerships with core banking vendors secure deposit, loan and ledger processing with SLAs typically 99.9%+. Card and network ties (Visa/Mastercard ~80% of card volume) plus ACH (30B txns in 2023), RTP (200+ banks by 2024) and Fedwire ($3.8T avg daily value in 2023) enable payments and liquidity. Correspondent banks, syndications and regulators (CET1 ≥4.5% 2024; FDIC limit 250,000) broaden products and reduce risk.

| Partner | Role | Key metric |

|---|---|---|

| Core banking | Processing/scale | SLA 99.9%+ |

| Card networks | Payments | ~80% volume |

| ACH | Clearing | 30B txns (2023) |

| RTP | Real‑time payments | 200+ banks (2024) |

| Fedwire | Wholesale transfer | $3.8T/day (2023) |

| Regulators | Stability/compliance | CET1 ≥4.5% (2024); FDIC 250,000 |

What is included in the product

A concise, pre-built Business Model Canvas for United Bank detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with competitive analysis, SWOT-linked insights and presentation-ready narratives for investors and analysts.

High-level, editable one-page canvas that maps United Bank’s value propositions, channels, and revenue streams—relieves pain by saving hours on structuring models and enabling fast comparisons, collaboration, and executive-ready summaries.

Activities

Deposit Gathering

United Bank focuses on attracting checking, savings, and time deposits to fund loan growth at competitive costs, using targeted community outreach and campaigns to build stable balances. Pricing, promotions, and streamlined digital onboarding accelerate acquisition and lower onboarding costs. Ongoing relationship management and cross-selling improve retention and deposit mix.

Credit Underwriting

Evaluating commercial, consumer, and mortgage credit drives risk-adjusted returns by prioritizing yield versus impairment. Robust policies and machine-learning scoring models maintain portfolio quality and aim to keep losses below peer medians. Continuous monitoring and proactive servicing contain delinquencies amid 2024 US unemployment near 4.0%. Regular stress testing incorporates end-2024 Fed funds at 5.25–5.50% to align risk appetite with macro scenarios.

Wealth and Trust Advisory

Delivering investment management, fiduciary and estate services deepens client relationships and supports retention as wealth management AUM surpassed $100 trillion globally in 2024. Goals-based advice aligns portfolios to long-term outcomes, improving plan adherence and outcomes. Rigorous platform due diligence ensures product suitability and cost efficiency, while regular reviews sustain retention and increase share of wallet.

Digital Banking Operations

- 24/7

- cybersecurity

- UX-optimization

- data-analytics

Regulatory and Risk Management

Compliance, BSA/AML, and operational risk programs protect the franchise by preventing fines and illicit activity; model risk governance oversees credit, pricing, and liquidity tools to ensure decision integrity; internal audit validates control effectiveness through regular testing; capital planning maintains CET1 above the 4.5% regulatory minimum and liquidity planning targets LCR ≥100% per supervisory expectations.

- Compliance & BSA/AML: ongoing monitoring, SAR filing metrics

- Model risk: governance over credit, pricing, liquidity models

- Internal audit: periodic validation of key controls

- Capital & liquidity: CET1 ≥4.5%, LCR ≥100%

Digital deposits 65%, digital transactions 70%, NPLs target 1.1%

United Bank acquires low-cost deposits (65% of loan funding in 2024) via digital onboarding and community campaigns, lowering cost of funds. ML-driven credit scoring and stress testing aim to keep NPLs below 1.1% peer median; Fed funds modeled at 5.25–5.50% (end-2024). Wealth/advisory and digital channels (70% retail digital transactions in 2024) grow fee income and retention.

| Metric | 2024 |

|---|---|

| Deposit funding % | 65% |

| Digital txn share | 70% |

| Peer NPL median | 1.1% |

| Fed funds (modeled) | 5.25–5.50% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact United Bank Business Model Canvas you'll receive after purchase, not a mockup. When you complete your order you'll get the full, editable file formatted exactly as shown. It's ready for immediate download, editing, presenting, or analysis.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic blueprint of a leading bank business model preview

Unlock the strategic blueprint of United Bank's business model with our concise preview. The full Business Model Canvas reveals customer segments, revenue drivers, key partnerships and cost structure to inform investments and strategy. Purchase the complete, editable canvas to analyze, benchmark and apply these actionable insights.

Partnerships

Core Banking Vendors

Partnerships with core banking software providers ensure reliable deposit, loan and ledger processing and support scalability to handle millions of transactions daily. These vendors enable security and regulatory reporting, with SLAs commonly set at 99.9%+ availability. Joint roadmaps accelerate new product rollouts and digital features, while regular compliance audits preserve uptime and data integrity.

Payment Networks

Ties with Visa and Mastercard (covering roughly 80% of global card volume), ACH (30+ billion transactions annually in 2023), RTP (200+ participating banks by 2024) and wire networks (Fedwire avg daily value ~$3.8 trillion in 2023) enable United Bank to issue cards, accept merchants and move funds. These links boost transaction speed and client convenience. Network incentives optimize interchange and fraud tools. Ongoing certification ensures compliance and resilience.

Fintech Integrations

API partnerships with fintechs add P2P payments, personal finance tools and lending analytics, leveraging the open-banking ecosystem that by 2024 processed trillions of dollars in API-enabled transactions globally.

These integrations accelerate time-to-market—often cutting development timelines by roughly half—without heavy in-house build and enable co-branding that broadens reach among digital-first users.

Rigorous due diligence, vendor controls and model-risk frameworks are essential to manage third-party and analytics model risk.

Correspondent Banks

United Bank's correspondent bank relationships deliver liquidity, syndication access, foreign exchange execution and niche trade services, extending product breadth for business and wealth clients and enabling cross-border cash management and FX hedging.

Participation and syndication arrangements diversify credit exposure while negotiated pricing with correspondents enhances client competitiveness on fees and execution.

- Liquidity lines and syndications

- Expanded FX and trade services

- Credit diversification via participation

- Preferential pricing improves client rates

Regulators and Compliance Advisors

Constructive engagement with the OCC, FDIC and Fed underpins safe operations, aligning United Bank with Basel III capital norms (CET1 minimum 4.5% as of 2024) and FDIC deposit insurance limits of 250,000 per depositor. External legal and audit advisors support evolving rule adherence, reducing compliance risk and remediation costs, while proactive dialogue enables timely policy and control updates ahead of stress-test and supervisory expectations for banks above 100 billion in assets.

- Regulatory alignment: CET1 ≥ 4.5% (2024)

- Deposit protection: FDIC limit 250,000

- Supervisory focus: Fed stress tests for >100B banks

Banking partnerships enable payments scale: core SLA 99.9%, cards ~80%

Partnerships with core banking vendors secure deposit, loan and ledger processing with SLAs typically 99.9%+. Card and network ties (Visa/Mastercard ~80% of card volume) plus ACH (30B txns in 2023), RTP (200+ banks by 2024) and Fedwire ($3.8T avg daily value in 2023) enable payments and liquidity. Correspondent banks, syndications and regulators (CET1 ≥4.5% 2024; FDIC limit 250,000) broaden products and reduce risk.

| Partner | Role | Key metric |

|---|---|---|

| Core banking | Processing/scale | SLA 99.9%+ |

| Card networks | Payments | ~80% volume |

| ACH | Clearing | 30B txns (2023) |

| RTP | Real‑time payments | 200+ banks (2024) |

| Fedwire | Wholesale transfer | $3.8T/day (2023) |

| Regulators | Stability/compliance | CET1 ≥4.5% (2024); FDIC 250,000 |

What is included in the product

A concise, pre-built Business Model Canvas for United Bank detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with competitive analysis, SWOT-linked insights and presentation-ready narratives for investors and analysts.

High-level, editable one-page canvas that maps United Bank’s value propositions, channels, and revenue streams—relieves pain by saving hours on structuring models and enabling fast comparisons, collaboration, and executive-ready summaries.

Activities

Deposit Gathering

United Bank focuses on attracting checking, savings, and time deposits to fund loan growth at competitive costs, using targeted community outreach and campaigns to build stable balances. Pricing, promotions, and streamlined digital onboarding accelerate acquisition and lower onboarding costs. Ongoing relationship management and cross-selling improve retention and deposit mix.

Credit Underwriting

Evaluating commercial, consumer, and mortgage credit drives risk-adjusted returns by prioritizing yield versus impairment. Robust policies and machine-learning scoring models maintain portfolio quality and aim to keep losses below peer medians. Continuous monitoring and proactive servicing contain delinquencies amid 2024 US unemployment near 4.0%. Regular stress testing incorporates end-2024 Fed funds at 5.25–5.50% to align risk appetite with macro scenarios.

Wealth and Trust Advisory

Delivering investment management, fiduciary and estate services deepens client relationships and supports retention as wealth management AUM surpassed $100 trillion globally in 2024. Goals-based advice aligns portfolios to long-term outcomes, improving plan adherence and outcomes. Rigorous platform due diligence ensures product suitability and cost efficiency, while regular reviews sustain retention and increase share of wallet.

Digital Banking Operations

- 24/7

- cybersecurity

- UX-optimization

- data-analytics

Regulatory and Risk Management

Compliance, BSA/AML, and operational risk programs protect the franchise by preventing fines and illicit activity; model risk governance oversees credit, pricing, and liquidity tools to ensure decision integrity; internal audit validates control effectiveness through regular testing; capital planning maintains CET1 above the 4.5% regulatory minimum and liquidity planning targets LCR ≥100% per supervisory expectations.

- Compliance & BSA/AML: ongoing monitoring, SAR filing metrics

- Model risk: governance over credit, pricing, liquidity models

- Internal audit: periodic validation of key controls

- Capital & liquidity: CET1 ≥4.5%, LCR ≥100%

Digital deposits 65%, digital transactions 70%, NPLs target 1.1%

United Bank acquires low-cost deposits (65% of loan funding in 2024) via digital onboarding and community campaigns, lowering cost of funds. ML-driven credit scoring and stress testing aim to keep NPLs below 1.1% peer median; Fed funds modeled at 5.25–5.50% (end-2024). Wealth/advisory and digital channels (70% retail digital transactions in 2024) grow fee income and retention.

| Metric | 2024 |

|---|---|

| Deposit funding % | 65% |

| Digital txn share | 70% |

| Peer NPL median | 1.1% |

| Fed funds (modeled) | 5.25–5.50% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the exact United Bank Business Model Canvas you'll receive after purchase, not a mockup. When you complete your order you'll get the full, editable file formatted exactly as shown. It's ready for immediate download, editing, presenting, or analysis.