Ultra Clean Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

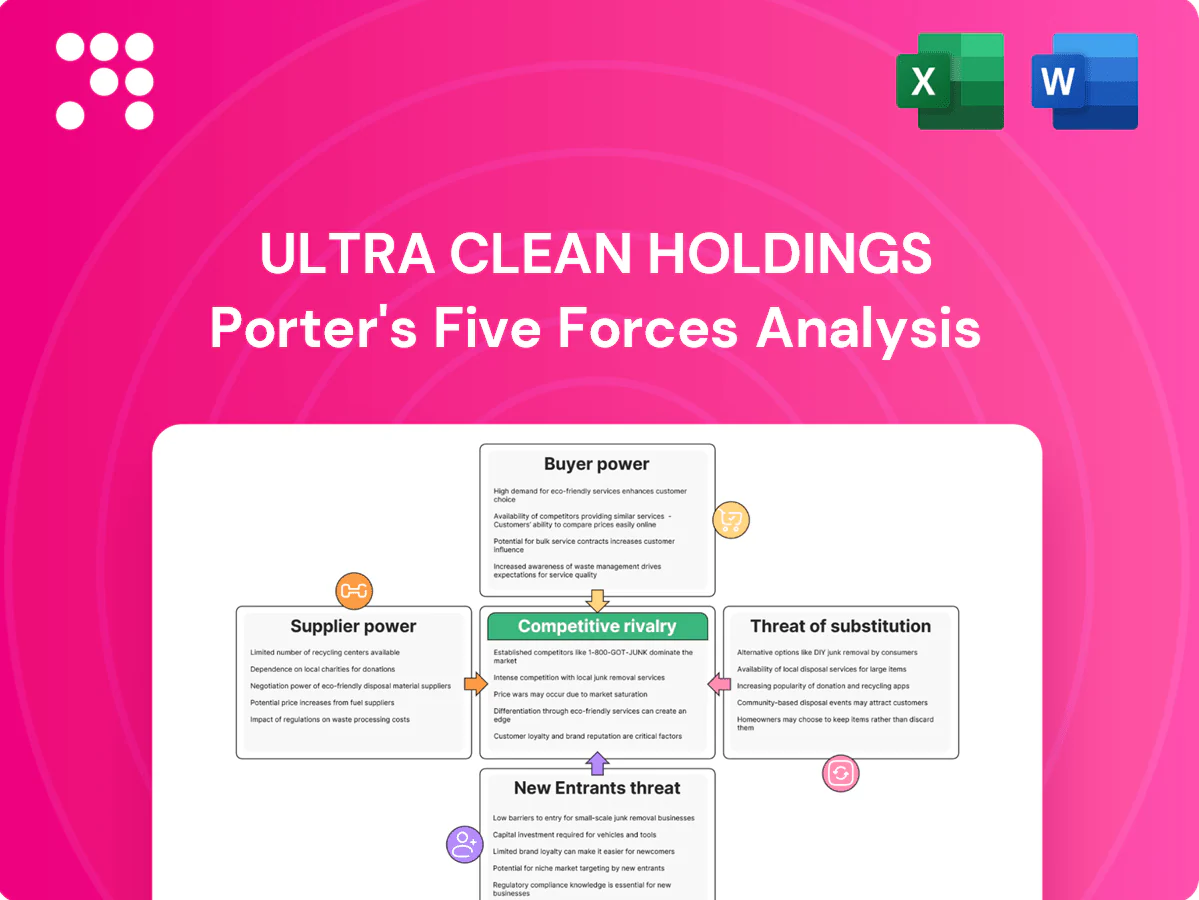

Ultra Clean Holdings faces intense supplier concentration, strong buyer bargaining in semiconductor capital equipment, moderate substitute threats, and high technical/barrier costs that limit new entrants—producing a mixed but competitive landscape. Strategic positioning relies on scale, IP and customer ties. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore UCTT’s forces in detail.

Suppliers Bargaining Power

Concentrated specialty inputs

UCT depends on ultra-high-purity metals, valves, MFCs, seals and specialty polymers from a narrow group of qualified vendors, giving suppliers leverage on price and allocations during upcycles. Single-source components amplify production risk and can trigger supply disruptions. Qualification cycles typically take 6–18 months, making rapid supplier switches difficult and costly.

High switching and requalification costs

Materials/components for UHP fabs must meet stringent specs and process quals, so switching suppliers typically requires months to 6–18 months of requalification as of 2024. Any change can trigger OEM tool revalidation, discouraging turnover and giving key suppliers pricing and delivery leverage. Ultra Clean mitigates this by pursuing dual-qualification where feasible to reduce single-source exposure.

Geopolitical and logistics exposure

Global supply chains across the US, Europe and Asia expose Ultra Clean to export controls, tariffs and shipping disruptions, and 2024 trade-policy shifts increased compliance costs for semiconductor-equipment suppliers. Lead-time volatility for precision parts and specialty chemicals in 2024 continued to strain production cycles. Suppliers have used scarcity to push less favorable terms; buffer inventory and localized sourcing have partially offset these pressures.

Scale provides counter-leverage

Ultra Clean’s scale—2024 revenue ~$1.2B—lets volume buying and long-term agreements secure priority, rebates and improved payment/lead-time terms. Aggregating demand across subsystems and services strengthens leverage with suppliers, while collaborative forecasting cuts bullwhip effects and inventory swings. Vendor-managed inventory and consignment programs further rebalance supplier power.

- Volume buying: priority access, rebates

- Aggregated demand: stronger negotiation

- Collaborative forecasting: lower bullwhip

- VMI/consignment: shifts inventory risk

Partial vertical capabilities

Partial vertical capabilities give Ultra Clean reduced supplier dependency: in 2024 its in-house fabrication, assembly and cleaning/analytics let engineering teams implement design-for-supply choices, though niche wafer-handling and specialty materials remain supplier bottlenecks, so selective make-versus-buy decisions limit supplier leverage.

- In-house fabs enable DfS flexibility

- Niche components retain supplier clout

- Make-versus-buy moderates risk

2024 revenue $1.2B provides leverage; suppliers have 6–18 month requalification

UCT relies on a narrow set of qualified vendors for UHP metals and specialty parts, giving suppliers price/allocation leverage; requalification takes 6–18 months. 2024 revenue ~$1.2B provides volume leverage, VMI and long-term contracts to mitigate risk. In-house fabs and selective make-vs-buy reduce dependency but niche components remain bottlenecks.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.2B |

| Supplier requalification | 6–18 months |

| Primary mitigations | VMI, long-term contracts, in-house fabs |

What is included in the product

Tailored Porter's Five Forces analysis for Ultra Clean Holdings, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats with strategic commentary to inform investor and management decisions.

One-sheet Porter's Five Forces for Ultra Clean Holdings—clear, slide-ready view that lets you customize pressure levels and instantly spot strategic risks with a compact spider chart.

Customers Bargaining Power

Highly concentrated OEM customer base

Semicap OEMs accounted for roughly 55% of Ultra Clean Holdings revenue in 2024, concentrating buying power and giving those customers strong negotiating leverage. A handful of large buyers can extract cost-downs, longer payment terms and volume guarantees that compress margins. Losing a single top OEM would hit revenue and utilization in double-digit percentage terms, so deep technical relationships and consistent on-time quality are critical to retention.

High switching costs but dual-sourcing

Subsystems and cleaning services for semiconductor and display OEMs are tightly qualified, making supplier switching risky and slow and often requiring lengthy requalification cycles. OEMs nonetheless maintain dual sourcing to hedge supply and pricing risk, creating constant share-of-wallet competition between incumbents. Superior delivery performance and higher yield rates can lock in advantage and protect margin share.

Cyclical demand and volume volatility

Semicap cycles shift bargaining power to buyers in downturns; SEMI reported a global equipment book-to-bill below 1 through much of 2024, giving OEMs leverage to extract concessions. OEMs use slack capacity to pressure pricing and push inventory back, intensifying discounts and payment stretches. In upturns allocation priority can soften price pressure as demand outstrips capacity. Ultra Clean’s flexible capacity and service model help defend margins by reallocating production to higher-margin customers.

Performance and uptime criticality

Buyers prioritize contamination control, reliability and rapid turn times over price, so Ultra Clean’s ability to demonstrate yield improvements and shorten tool installs materially reduces buyer leverage.

Service-level agreements tied to uptime and penalty clauses become clear differentiators, while data-backed analytics and remote monitoring increase customer stickiness and raise switching costs.

- Buyer preference: reliability over price

- Yield gains cut leverage

- SLA penalties differentiate

- Analytics boost retention

Global service proximity expectations

- local hubs: Taiwan, South Korea, US, China

- capacity share: ~70% Asia (2023–24)

- turnaround: 24–48h expectations

- footprint gaps = buyer leverage

OEM concentration, yield analytics and Asia footprint dictate pricing, service and switching risk

Semicap OEMs (~55% of 2024 revenue) concentrate buying power, enabling price/term pressure and single-customer risk. Tight requalification and SLAs raise switching costs; yield improvements and analytics reduce buyer leverage. Asia ~70% capacity (2023–24) plus 24–48h service expectations make local footprint decisive.

| Metric | Value |

|---|---|

| 2024 rev from OEMs | ~55% |

| Asia capacity | ~70% |

| Service TAT | 24–48h |

What You See Is What You Get

Ultra Clean Holdings Porter's Five Forces Analysis

This preview shows the exact Ultra Clean Holdings Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and strategic implications for margins and growth. It's fully formatted and ready for download.

Don't Miss the Bigger Picture

Ultra Clean Holdings faces intense supplier concentration, strong buyer bargaining in semiconductor capital equipment, moderate substitute threats, and high technical/barrier costs that limit new entrants—producing a mixed but competitive landscape. Strategic positioning relies on scale, IP and customer ties. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore UCTT’s forces in detail.

Suppliers Bargaining Power

Concentrated specialty inputs

UCT depends on ultra-high-purity metals, valves, MFCs, seals and specialty polymers from a narrow group of qualified vendors, giving suppliers leverage on price and allocations during upcycles. Single-source components amplify production risk and can trigger supply disruptions. Qualification cycles typically take 6–18 months, making rapid supplier switches difficult and costly.

High switching and requalification costs

Materials/components for UHP fabs must meet stringent specs and process quals, so switching suppliers typically requires months to 6–18 months of requalification as of 2024. Any change can trigger OEM tool revalidation, discouraging turnover and giving key suppliers pricing and delivery leverage. Ultra Clean mitigates this by pursuing dual-qualification where feasible to reduce single-source exposure.

Geopolitical and logistics exposure

Global supply chains across the US, Europe and Asia expose Ultra Clean to export controls, tariffs and shipping disruptions, and 2024 trade-policy shifts increased compliance costs for semiconductor-equipment suppliers. Lead-time volatility for precision parts and specialty chemicals in 2024 continued to strain production cycles. Suppliers have used scarcity to push less favorable terms; buffer inventory and localized sourcing have partially offset these pressures.

Scale provides counter-leverage

Ultra Clean’s scale—2024 revenue ~$1.2B—lets volume buying and long-term agreements secure priority, rebates and improved payment/lead-time terms. Aggregating demand across subsystems and services strengthens leverage with suppliers, while collaborative forecasting cuts bullwhip effects and inventory swings. Vendor-managed inventory and consignment programs further rebalance supplier power.

- Volume buying: priority access, rebates

- Aggregated demand: stronger negotiation

- Collaborative forecasting: lower bullwhip

- VMI/consignment: shifts inventory risk

Partial vertical capabilities

Partial vertical capabilities give Ultra Clean reduced supplier dependency: in 2024 its in-house fabrication, assembly and cleaning/analytics let engineering teams implement design-for-supply choices, though niche wafer-handling and specialty materials remain supplier bottlenecks, so selective make-versus-buy decisions limit supplier leverage.

- In-house fabs enable DfS flexibility

- Niche components retain supplier clout

- Make-versus-buy moderates risk

2024 revenue $1.2B provides leverage; suppliers have 6–18 month requalification

UCT relies on a narrow set of qualified vendors for UHP metals and specialty parts, giving suppliers price/allocation leverage; requalification takes 6–18 months. 2024 revenue ~$1.2B provides volume leverage, VMI and long-term contracts to mitigate risk. In-house fabs and selective make-vs-buy reduce dependency but niche components remain bottlenecks.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.2B |

| Supplier requalification | 6–18 months |

| Primary mitigations | VMI, long-term contracts, in-house fabs |

What is included in the product

Tailored Porter's Five Forces analysis for Ultra Clean Holdings, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats with strategic commentary to inform investor and management decisions.

One-sheet Porter's Five Forces for Ultra Clean Holdings—clear, slide-ready view that lets you customize pressure levels and instantly spot strategic risks with a compact spider chart.

Customers Bargaining Power

Highly concentrated OEM customer base

Semicap OEMs accounted for roughly 55% of Ultra Clean Holdings revenue in 2024, concentrating buying power and giving those customers strong negotiating leverage. A handful of large buyers can extract cost-downs, longer payment terms and volume guarantees that compress margins. Losing a single top OEM would hit revenue and utilization in double-digit percentage terms, so deep technical relationships and consistent on-time quality are critical to retention.

High switching costs but dual-sourcing

Subsystems and cleaning services for semiconductor and display OEMs are tightly qualified, making supplier switching risky and slow and often requiring lengthy requalification cycles. OEMs nonetheless maintain dual sourcing to hedge supply and pricing risk, creating constant share-of-wallet competition between incumbents. Superior delivery performance and higher yield rates can lock in advantage and protect margin share.

Cyclical demand and volume volatility

Semicap cycles shift bargaining power to buyers in downturns; SEMI reported a global equipment book-to-bill below 1 through much of 2024, giving OEMs leverage to extract concessions. OEMs use slack capacity to pressure pricing and push inventory back, intensifying discounts and payment stretches. In upturns allocation priority can soften price pressure as demand outstrips capacity. Ultra Clean’s flexible capacity and service model help defend margins by reallocating production to higher-margin customers.

Performance and uptime criticality

Buyers prioritize contamination control, reliability and rapid turn times over price, so Ultra Clean’s ability to demonstrate yield improvements and shorten tool installs materially reduces buyer leverage.

Service-level agreements tied to uptime and penalty clauses become clear differentiators, while data-backed analytics and remote monitoring increase customer stickiness and raise switching costs.

- Buyer preference: reliability over price

- Yield gains cut leverage

- SLA penalties differentiate

- Analytics boost retention

Global service proximity expectations

- local hubs: Taiwan, South Korea, US, China

- capacity share: ~70% Asia (2023–24)

- turnaround: 24–48h expectations

- footprint gaps = buyer leverage

OEM concentration, yield analytics and Asia footprint dictate pricing, service and switching risk

Semicap OEMs (~55% of 2024 revenue) concentrate buying power, enabling price/term pressure and single-customer risk. Tight requalification and SLAs raise switching costs; yield improvements and analytics reduce buyer leverage. Asia ~70% capacity (2023–24) plus 24–48h service expectations make local footprint decisive.

| Metric | Value |

|---|---|

| 2024 rev from OEMs | ~55% |

| Asia capacity | ~70% |

| Service TAT | 24–48h |

What You See Is What You Get

Ultra Clean Holdings Porter's Five Forces Analysis

This preview shows the exact Ultra Clean Holdings Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and strategic implications for margins and growth. It's fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ultra Clean Holdings faces intense supplier concentration, strong buyer bargaining in semiconductor capital equipment, moderate substitute threats, and high technical/barrier costs that limit new entrants—producing a mixed but competitive landscape. Strategic positioning relies on scale, IP and customer ties. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore UCTT’s forces in detail.

Suppliers Bargaining Power

Concentrated specialty inputs

UCT depends on ultra-high-purity metals, valves, MFCs, seals and specialty polymers from a narrow group of qualified vendors, giving suppliers leverage on price and allocations during upcycles. Single-source components amplify production risk and can trigger supply disruptions. Qualification cycles typically take 6–18 months, making rapid supplier switches difficult and costly.

High switching and requalification costs

Materials/components for UHP fabs must meet stringent specs and process quals, so switching suppliers typically requires months to 6–18 months of requalification as of 2024. Any change can trigger OEM tool revalidation, discouraging turnover and giving key suppliers pricing and delivery leverage. Ultra Clean mitigates this by pursuing dual-qualification where feasible to reduce single-source exposure.

Geopolitical and logistics exposure

Global supply chains across the US, Europe and Asia expose Ultra Clean to export controls, tariffs and shipping disruptions, and 2024 trade-policy shifts increased compliance costs for semiconductor-equipment suppliers. Lead-time volatility for precision parts and specialty chemicals in 2024 continued to strain production cycles. Suppliers have used scarcity to push less favorable terms; buffer inventory and localized sourcing have partially offset these pressures.

Scale provides counter-leverage

Ultra Clean’s scale—2024 revenue ~$1.2B—lets volume buying and long-term agreements secure priority, rebates and improved payment/lead-time terms. Aggregating demand across subsystems and services strengthens leverage with suppliers, while collaborative forecasting cuts bullwhip effects and inventory swings. Vendor-managed inventory and consignment programs further rebalance supplier power.

- Volume buying: priority access, rebates

- Aggregated demand: stronger negotiation

- Collaborative forecasting: lower bullwhip

- VMI/consignment: shifts inventory risk

Partial vertical capabilities

Partial vertical capabilities give Ultra Clean reduced supplier dependency: in 2024 its in-house fabrication, assembly and cleaning/analytics let engineering teams implement design-for-supply choices, though niche wafer-handling and specialty materials remain supplier bottlenecks, so selective make-versus-buy decisions limit supplier leverage.

- In-house fabs enable DfS flexibility

- Niche components retain supplier clout

- Make-versus-buy moderates risk

2024 revenue $1.2B provides leverage; suppliers have 6–18 month requalification

UCT relies on a narrow set of qualified vendors for UHP metals and specialty parts, giving suppliers price/allocation leverage; requalification takes 6–18 months. 2024 revenue ~$1.2B provides volume leverage, VMI and long-term contracts to mitigate risk. In-house fabs and selective make-vs-buy reduce dependency but niche components remain bottlenecks.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.2B |

| Supplier requalification | 6–18 months |

| Primary mitigations | VMI, long-term contracts, in-house fabs |

What is included in the product

Tailored Porter's Five Forces analysis for Ultra Clean Holdings, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats with strategic commentary to inform investor and management decisions.

One-sheet Porter's Five Forces for Ultra Clean Holdings—clear, slide-ready view that lets you customize pressure levels and instantly spot strategic risks with a compact spider chart.

Customers Bargaining Power

Highly concentrated OEM customer base

Semicap OEMs accounted for roughly 55% of Ultra Clean Holdings revenue in 2024, concentrating buying power and giving those customers strong negotiating leverage. A handful of large buyers can extract cost-downs, longer payment terms and volume guarantees that compress margins. Losing a single top OEM would hit revenue and utilization in double-digit percentage terms, so deep technical relationships and consistent on-time quality are critical to retention.

High switching costs but dual-sourcing

Subsystems and cleaning services for semiconductor and display OEMs are tightly qualified, making supplier switching risky and slow and often requiring lengthy requalification cycles. OEMs nonetheless maintain dual sourcing to hedge supply and pricing risk, creating constant share-of-wallet competition between incumbents. Superior delivery performance and higher yield rates can lock in advantage and protect margin share.

Cyclical demand and volume volatility

Semicap cycles shift bargaining power to buyers in downturns; SEMI reported a global equipment book-to-bill below 1 through much of 2024, giving OEMs leverage to extract concessions. OEMs use slack capacity to pressure pricing and push inventory back, intensifying discounts and payment stretches. In upturns allocation priority can soften price pressure as demand outstrips capacity. Ultra Clean’s flexible capacity and service model help defend margins by reallocating production to higher-margin customers.

Performance and uptime criticality

Buyers prioritize contamination control, reliability and rapid turn times over price, so Ultra Clean’s ability to demonstrate yield improvements and shorten tool installs materially reduces buyer leverage.

Service-level agreements tied to uptime and penalty clauses become clear differentiators, while data-backed analytics and remote monitoring increase customer stickiness and raise switching costs.

- Buyer preference: reliability over price

- Yield gains cut leverage

- SLA penalties differentiate

- Analytics boost retention

Global service proximity expectations

- local hubs: Taiwan, South Korea, US, China

- capacity share: ~70% Asia (2023–24)

- turnaround: 24–48h expectations

- footprint gaps = buyer leverage

OEM concentration, yield analytics and Asia footprint dictate pricing, service and switching risk

Semicap OEMs (~55% of 2024 revenue) concentrate buying power, enabling price/term pressure and single-customer risk. Tight requalification and SLAs raise switching costs; yield improvements and analytics reduce buyer leverage. Asia ~70% capacity (2023–24) plus 24–48h service expectations make local footprint decisive.

| Metric | Value |

|---|---|

| 2024 rev from OEMs | ~55% |

| Asia capacity | ~70% |

| Service TAT | 24–48h |

What You See Is What You Get

Ultra Clean Holdings Porter's Five Forces Analysis

This preview shows the exact Ultra Clean Holdings Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The report evaluates supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and strategic implications for margins and growth. It's fully formatted and ready for download.