UiPath Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

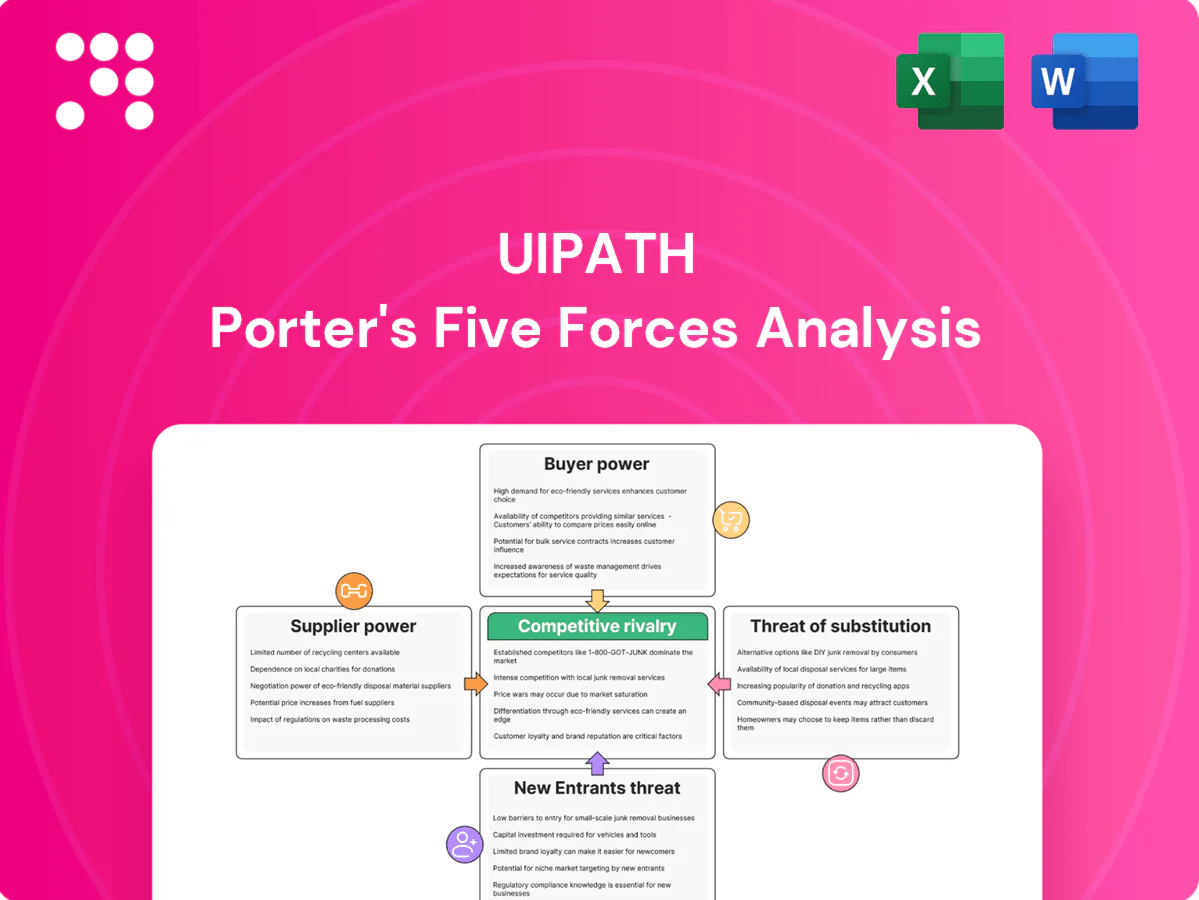

UiPath faces intense competitive rivalry, rising buyer sophistication, and moderate supplier leverage as automation platforms commoditize; threats from new entrants and substitutes hinge on AI integration and low-cost RPA alternatives. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for informed decisions.

Suppliers Bargaining Power

Hyperscale cloud dependency

UiPath depends on AWS, Azure and GCP—which together hold roughly 66% of the global cloud market— for hosting, AI services and global delivery, concentrating supplier power. Price hikes or reserved-capacity constraints by hyperscalers can compress margins and degrade SLAs, a material risk given UiPath reported FY2024 revenue of about $1.32B. Multi-cloud support reduces single-vendor exposure but raises integration complexity and switching friction. Strategic partnerships can soften pricing pressure but seldom remove it entirely.

AI/ML model providers

Major LLM vendors such as OpenAI, Google and Anthropic largely determine access to foundation models and NLP services, with API pricing, rate limits and model availability directly shaping UiPath’s AI feature set. Dependence raises supplier power since enterprise API costs and throttling can constrain deployments. Building proprietary models cuts reliance but typically requires hundreds of millions in data, compute and talent. Contractual SLAs and fine‑tuning rights are essential negotiation levers.

Third-party components and OSS

UiPath relies on open-source libraries and third-party SDKs, creating licensing and security dependencies that in 2024 coincided with a 15% rise in software supply-chain incidents; license changes or disclosed vulnerabilities can force rework and support costs against UiPath’s 2024 revenue of roughly $1.1 billion. Vendor-managed components risk version lock-in, while a robust SBOM and dual-sourcing program reduce supplier leverage and remediation time.

Global partner ecosystem

Implementation partners, system integrators, and resellers materially affect UiPath sales velocity and delivery quality; leading GSIs such as Accenture, Deloitte, and EY frequently negotiate margin-sharing and co-selling concessions. Partner certifications and enablement programs broaden the partner base and reduce concentration risk, yet top-tier integrators keep leverage from originating large enterprise deals.

- Implementation partners drive go-to-market and delivery

- Top GSIs extract margin/co-sell concessions

- Certifications lower concentration risk

- Deal origination preserves integrator bargaining power

Specialized data services

Training data, labeling, and domain ontologies for UiPath automation and AI features are often sourced from niche vendors, and limited substitutes for compliant, high-quality datasets increase supplier leverage in regulated sectors; UiPath reported FY2024 revenue of $1.39 billion, highlighting business sensitivity to supplier-driven cost shocks. Contracting for data rights and portability reduces lock-in, while building internal data pipelines progressively lowers dependence.

- High leverage: niche suppliers for regulated datasets

- Risk: limited substitutes → price/control pressure

- Mitigation: contractual data rights and portability

- Long-term: internal pipelines reduce supplier dependence

Supplier concentration: hyperscalers 66% & incidents +15%

UiPath faces concentrated supplier power from hyperscalers (AWS/Azure/GCP ~66% cloud share), LLM/API vendors, niche data providers and top GSIs; FY2024 revenue exposure cited ~$1.32B–$1.39B and a 15% rise in supply‑chain incidents—mitigations: multi‑cloud, contractual SLAs, SBOMs and partner enablement.

| Supplier | 2024 metric | Risk | Mitigation |

|---|---|---|---|

| Hyperscalers | 66% cloud share | Price/capacity | Multi‑cloud |

| LLM vendors | API limits/pricing | Feature/cost | Contracts/proprietary models |

| Data vendors | 15% supply‑chain incidents | Compliance/cost | Data rights/own pipelines |

| GSIs | Deal origination | Margin concessions | Certifications/co‑sell |

What is included in the product

Concise Porter's Five Forces assessment for UiPath identifying competitive rivalry, buyer/supplier power, entry barriers, substitute threats, and strategic levers to protect market share and margins.

Clear one-sheet Porter's Five Forces for UiPath that turns complex competitive dynamics into actionable insights—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Enterprise procurement clout

Large enterprises wield significant procurement clout, negotiating multi-year contracts and volume discounts with UiPath, with many strategic deals commonly exceeding $1 million ARR and multi-year commitments in 2024.

Competitive bake-offs against Microsoft and Automation Anywhere in 2024 intensified price pressure and forced concessioning on term flexibility and TCO.

Security, compliance certifications and clear ROI proof points became table stakes in 2024 procurement evaluations.

Ongoing vendor consolidation in 2024 amplified buyer leverage, enabling enterprises to demand bundling, deeper discounts and centralized support guarantees.

Switching costs vs standardization

Automation estates embed workflows, bots and governance that create meaningful switching costs, yet buyers push for tool and cloud standardization enabling credible switching threats. UiPath reported >12,000 customers and FY2024 revenue around $1.31B, while migration services and dual-running practices increasingly lower friction. Clear TCO advantages can flip platforms despite inertia.

Outcome-based pricing demands

Buyers increasingly demand consumption- and outcome-based pricing tied to business results, pressuring UiPath to accept models that can compress margins if productivity gains are uncertain. UiPath reported roughly $1.3B revenue in FY2024 with net retention above 120%, so transparent ROI dashboards are used to defend pricing and prove value. Competitive flexibility on terms is required while preserving unit economics.

Security and compliance requirements

Regulated industries demand certifications, strict data residency and granular governance, giving customers leverage to delay or demand discounts if controls are insufficient; strong audit tooling and integrated compliance features reduce these objections and speed procurement. Localized hosting options and certified controls can unlock pricing power and reduce churn.

- Certification focus: finance, healthcare, government

- Controls reduce deal friction

- Local hosting = pricing leverage

Integration with existing stacks

Buyers demand seamless interoperability with ERP, CRM, ITSM and CI/CD; deep connectors and APIs lower perceived risk and speed time-to-value, easing pricing pressure. Integration gaps push customers to fund custom work or switch vendors, while UiPath’s FY2024 revenue of $1.26 billion reflects strong adoption driven by ecosystem strength. Prebuilt templates and marketplace assets improve retention and upsell.

- Integration reduces churn

- Gaps = custom spend or migration

- APIs lower procurement friction

- Marketplace assets boost account stickiness

Enterprises force discounts, outcome-based pricing, and multi-year >$1M automation deals

Enterprise buyers exert strong leverage through multi-year, >$1M ARR deals and vendor consolidation, forcing discounts and term flexibility; UiPath reported FY2024 revenue $1.31B and >12,000 customers with net retention >120%. Buyers push outcome-based pricing and strict compliance, raising procurement demands and pressuring margins, while embedded automation estates create switching costs that are mitigated by migration services.

| Metric | 2024 |

|---|---|

| FY revenue | $1.31B |

| Customers | >12,000 |

| Net retention | >120% |

Same Document Delivered

UiPath Porter's Five Forces Analysis

This preview shows the exact UiPath Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. Once paid, you get instant access to this identical file, ready for download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

UiPath faces intense competitive rivalry, rising buyer sophistication, and moderate supplier leverage as automation platforms commoditize; threats from new entrants and substitutes hinge on AI integration and low-cost RPA alternatives. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for informed decisions.

Suppliers Bargaining Power

Hyperscale cloud dependency

UiPath depends on AWS, Azure and GCP—which together hold roughly 66% of the global cloud market— for hosting, AI services and global delivery, concentrating supplier power. Price hikes or reserved-capacity constraints by hyperscalers can compress margins and degrade SLAs, a material risk given UiPath reported FY2024 revenue of about $1.32B. Multi-cloud support reduces single-vendor exposure but raises integration complexity and switching friction. Strategic partnerships can soften pricing pressure but seldom remove it entirely.

AI/ML model providers

Major LLM vendors such as OpenAI, Google and Anthropic largely determine access to foundation models and NLP services, with API pricing, rate limits and model availability directly shaping UiPath’s AI feature set. Dependence raises supplier power since enterprise API costs and throttling can constrain deployments. Building proprietary models cuts reliance but typically requires hundreds of millions in data, compute and talent. Contractual SLAs and fine‑tuning rights are essential negotiation levers.

Third-party components and OSS

UiPath relies on open-source libraries and third-party SDKs, creating licensing and security dependencies that in 2024 coincided with a 15% rise in software supply-chain incidents; license changes or disclosed vulnerabilities can force rework and support costs against UiPath’s 2024 revenue of roughly $1.1 billion. Vendor-managed components risk version lock-in, while a robust SBOM and dual-sourcing program reduce supplier leverage and remediation time.

Global partner ecosystem

Implementation partners, system integrators, and resellers materially affect UiPath sales velocity and delivery quality; leading GSIs such as Accenture, Deloitte, and EY frequently negotiate margin-sharing and co-selling concessions. Partner certifications and enablement programs broaden the partner base and reduce concentration risk, yet top-tier integrators keep leverage from originating large enterprise deals.

- Implementation partners drive go-to-market and delivery

- Top GSIs extract margin/co-sell concessions

- Certifications lower concentration risk

- Deal origination preserves integrator bargaining power

Specialized data services

Training data, labeling, and domain ontologies for UiPath automation and AI features are often sourced from niche vendors, and limited substitutes for compliant, high-quality datasets increase supplier leverage in regulated sectors; UiPath reported FY2024 revenue of $1.39 billion, highlighting business sensitivity to supplier-driven cost shocks. Contracting for data rights and portability reduces lock-in, while building internal data pipelines progressively lowers dependence.

- High leverage: niche suppliers for regulated datasets

- Risk: limited substitutes → price/control pressure

- Mitigation: contractual data rights and portability

- Long-term: internal pipelines reduce supplier dependence

Supplier concentration: hyperscalers 66% & incidents +15%

UiPath faces concentrated supplier power from hyperscalers (AWS/Azure/GCP ~66% cloud share), LLM/API vendors, niche data providers and top GSIs; FY2024 revenue exposure cited ~$1.32B–$1.39B and a 15% rise in supply‑chain incidents—mitigations: multi‑cloud, contractual SLAs, SBOMs and partner enablement.

| Supplier | 2024 metric | Risk | Mitigation |

|---|---|---|---|

| Hyperscalers | 66% cloud share | Price/capacity | Multi‑cloud |

| LLM vendors | API limits/pricing | Feature/cost | Contracts/proprietary models |

| Data vendors | 15% supply‑chain incidents | Compliance/cost | Data rights/own pipelines |

| GSIs | Deal origination | Margin concessions | Certifications/co‑sell |

What is included in the product

Concise Porter's Five Forces assessment for UiPath identifying competitive rivalry, buyer/supplier power, entry barriers, substitute threats, and strategic levers to protect market share and margins.

Clear one-sheet Porter's Five Forces for UiPath that turns complex competitive dynamics into actionable insights—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Enterprise procurement clout

Large enterprises wield significant procurement clout, negotiating multi-year contracts and volume discounts with UiPath, with many strategic deals commonly exceeding $1 million ARR and multi-year commitments in 2024.

Competitive bake-offs against Microsoft and Automation Anywhere in 2024 intensified price pressure and forced concessioning on term flexibility and TCO.

Security, compliance certifications and clear ROI proof points became table stakes in 2024 procurement evaluations.

Ongoing vendor consolidation in 2024 amplified buyer leverage, enabling enterprises to demand bundling, deeper discounts and centralized support guarantees.

Switching costs vs standardization

Automation estates embed workflows, bots and governance that create meaningful switching costs, yet buyers push for tool and cloud standardization enabling credible switching threats. UiPath reported >12,000 customers and FY2024 revenue around $1.31B, while migration services and dual-running practices increasingly lower friction. Clear TCO advantages can flip platforms despite inertia.

Outcome-based pricing demands

Buyers increasingly demand consumption- and outcome-based pricing tied to business results, pressuring UiPath to accept models that can compress margins if productivity gains are uncertain. UiPath reported roughly $1.3B revenue in FY2024 with net retention above 120%, so transparent ROI dashboards are used to defend pricing and prove value. Competitive flexibility on terms is required while preserving unit economics.

Security and compliance requirements

Regulated industries demand certifications, strict data residency and granular governance, giving customers leverage to delay or demand discounts if controls are insufficient; strong audit tooling and integrated compliance features reduce these objections and speed procurement. Localized hosting options and certified controls can unlock pricing power and reduce churn.

- Certification focus: finance, healthcare, government

- Controls reduce deal friction

- Local hosting = pricing leverage

Integration with existing stacks

Buyers demand seamless interoperability with ERP, CRM, ITSM and CI/CD; deep connectors and APIs lower perceived risk and speed time-to-value, easing pricing pressure. Integration gaps push customers to fund custom work or switch vendors, while UiPath’s FY2024 revenue of $1.26 billion reflects strong adoption driven by ecosystem strength. Prebuilt templates and marketplace assets improve retention and upsell.

- Integration reduces churn

- Gaps = custom spend or migration

- APIs lower procurement friction

- Marketplace assets boost account stickiness

Enterprises force discounts, outcome-based pricing, and multi-year >$1M automation deals

Enterprise buyers exert strong leverage through multi-year, >$1M ARR deals and vendor consolidation, forcing discounts and term flexibility; UiPath reported FY2024 revenue $1.31B and >12,000 customers with net retention >120%. Buyers push outcome-based pricing and strict compliance, raising procurement demands and pressuring margins, while embedded automation estates create switching costs that are mitigated by migration services.

| Metric | 2024 |

|---|---|

| FY revenue | $1.31B |

| Customers | >12,000 |

| Net retention | >120% |

Same Document Delivered

UiPath Porter's Five Forces Analysis

This preview shows the exact UiPath Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. Once paid, you get instant access to this identical file, ready for download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

UiPath faces intense competitive rivalry, rising buyer sophistication, and moderate supplier leverage as automation platforms commoditize; threats from new entrants and substitutes hinge on AI integration and low-cost RPA alternatives. This snapshot highlights strategic pressure points and growth levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for informed decisions.

Suppliers Bargaining Power

Hyperscale cloud dependency

UiPath depends on AWS, Azure and GCP—which together hold roughly 66% of the global cloud market— for hosting, AI services and global delivery, concentrating supplier power. Price hikes or reserved-capacity constraints by hyperscalers can compress margins and degrade SLAs, a material risk given UiPath reported FY2024 revenue of about $1.32B. Multi-cloud support reduces single-vendor exposure but raises integration complexity and switching friction. Strategic partnerships can soften pricing pressure but seldom remove it entirely.

AI/ML model providers

Major LLM vendors such as OpenAI, Google and Anthropic largely determine access to foundation models and NLP services, with API pricing, rate limits and model availability directly shaping UiPath’s AI feature set. Dependence raises supplier power since enterprise API costs and throttling can constrain deployments. Building proprietary models cuts reliance but typically requires hundreds of millions in data, compute and talent. Contractual SLAs and fine‑tuning rights are essential negotiation levers.

Third-party components and OSS

UiPath relies on open-source libraries and third-party SDKs, creating licensing and security dependencies that in 2024 coincided with a 15% rise in software supply-chain incidents; license changes or disclosed vulnerabilities can force rework and support costs against UiPath’s 2024 revenue of roughly $1.1 billion. Vendor-managed components risk version lock-in, while a robust SBOM and dual-sourcing program reduce supplier leverage and remediation time.

Global partner ecosystem

Implementation partners, system integrators, and resellers materially affect UiPath sales velocity and delivery quality; leading GSIs such as Accenture, Deloitte, and EY frequently negotiate margin-sharing and co-selling concessions. Partner certifications and enablement programs broaden the partner base and reduce concentration risk, yet top-tier integrators keep leverage from originating large enterprise deals.

- Implementation partners drive go-to-market and delivery

- Top GSIs extract margin/co-sell concessions

- Certifications lower concentration risk

- Deal origination preserves integrator bargaining power

Specialized data services

Training data, labeling, and domain ontologies for UiPath automation and AI features are often sourced from niche vendors, and limited substitutes for compliant, high-quality datasets increase supplier leverage in regulated sectors; UiPath reported FY2024 revenue of $1.39 billion, highlighting business sensitivity to supplier-driven cost shocks. Contracting for data rights and portability reduces lock-in, while building internal data pipelines progressively lowers dependence.

- High leverage: niche suppliers for regulated datasets

- Risk: limited substitutes → price/control pressure

- Mitigation: contractual data rights and portability

- Long-term: internal pipelines reduce supplier dependence

Supplier concentration: hyperscalers 66% & incidents +15%

UiPath faces concentrated supplier power from hyperscalers (AWS/Azure/GCP ~66% cloud share), LLM/API vendors, niche data providers and top GSIs; FY2024 revenue exposure cited ~$1.32B–$1.39B and a 15% rise in supply‑chain incidents—mitigations: multi‑cloud, contractual SLAs, SBOMs and partner enablement.

| Supplier | 2024 metric | Risk | Mitigation |

|---|---|---|---|

| Hyperscalers | 66% cloud share | Price/capacity | Multi‑cloud |

| LLM vendors | API limits/pricing | Feature/cost | Contracts/proprietary models |

| Data vendors | 15% supply‑chain incidents | Compliance/cost | Data rights/own pipelines |

| GSIs | Deal origination | Margin concessions | Certifications/co‑sell |

What is included in the product

Concise Porter's Five Forces assessment for UiPath identifying competitive rivalry, buyer/supplier power, entry barriers, substitute threats, and strategic levers to protect market share and margins.

Clear one-sheet Porter's Five Forces for UiPath that turns complex competitive dynamics into actionable insights—customize pressure levels, swap in your data, and visualize strategic intensity instantly with a spider chart ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Enterprise procurement clout

Large enterprises wield significant procurement clout, negotiating multi-year contracts and volume discounts with UiPath, with many strategic deals commonly exceeding $1 million ARR and multi-year commitments in 2024.

Competitive bake-offs against Microsoft and Automation Anywhere in 2024 intensified price pressure and forced concessioning on term flexibility and TCO.

Security, compliance certifications and clear ROI proof points became table stakes in 2024 procurement evaluations.

Ongoing vendor consolidation in 2024 amplified buyer leverage, enabling enterprises to demand bundling, deeper discounts and centralized support guarantees.

Switching costs vs standardization

Automation estates embed workflows, bots and governance that create meaningful switching costs, yet buyers push for tool and cloud standardization enabling credible switching threats. UiPath reported >12,000 customers and FY2024 revenue around $1.31B, while migration services and dual-running practices increasingly lower friction. Clear TCO advantages can flip platforms despite inertia.

Outcome-based pricing demands

Buyers increasingly demand consumption- and outcome-based pricing tied to business results, pressuring UiPath to accept models that can compress margins if productivity gains are uncertain. UiPath reported roughly $1.3B revenue in FY2024 with net retention above 120%, so transparent ROI dashboards are used to defend pricing and prove value. Competitive flexibility on terms is required while preserving unit economics.

Security and compliance requirements

Regulated industries demand certifications, strict data residency and granular governance, giving customers leverage to delay or demand discounts if controls are insufficient; strong audit tooling and integrated compliance features reduce these objections and speed procurement. Localized hosting options and certified controls can unlock pricing power and reduce churn.

- Certification focus: finance, healthcare, government

- Controls reduce deal friction

- Local hosting = pricing leverage

Integration with existing stacks

Buyers demand seamless interoperability with ERP, CRM, ITSM and CI/CD; deep connectors and APIs lower perceived risk and speed time-to-value, easing pricing pressure. Integration gaps push customers to fund custom work or switch vendors, while UiPath’s FY2024 revenue of $1.26 billion reflects strong adoption driven by ecosystem strength. Prebuilt templates and marketplace assets improve retention and upsell.

- Integration reduces churn

- Gaps = custom spend or migration

- APIs lower procurement friction

- Marketplace assets boost account stickiness

Enterprises force discounts, outcome-based pricing, and multi-year >$1M automation deals

Enterprise buyers exert strong leverage through multi-year, >$1M ARR deals and vendor consolidation, forcing discounts and term flexibility; UiPath reported FY2024 revenue $1.31B and >12,000 customers with net retention >120%. Buyers push outcome-based pricing and strict compliance, raising procurement demands and pressuring margins, while embedded automation estates create switching costs that are mitigated by migration services.

| Metric | 2024 |

|---|---|

| FY revenue | $1.31B |

| Customers | >12,000 |

| Net retention | >120% |

Same Document Delivered

UiPath Porter's Five Forces Analysis

This preview shows the exact UiPath Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. Once paid, you get instant access to this identical file, ready for download and use.