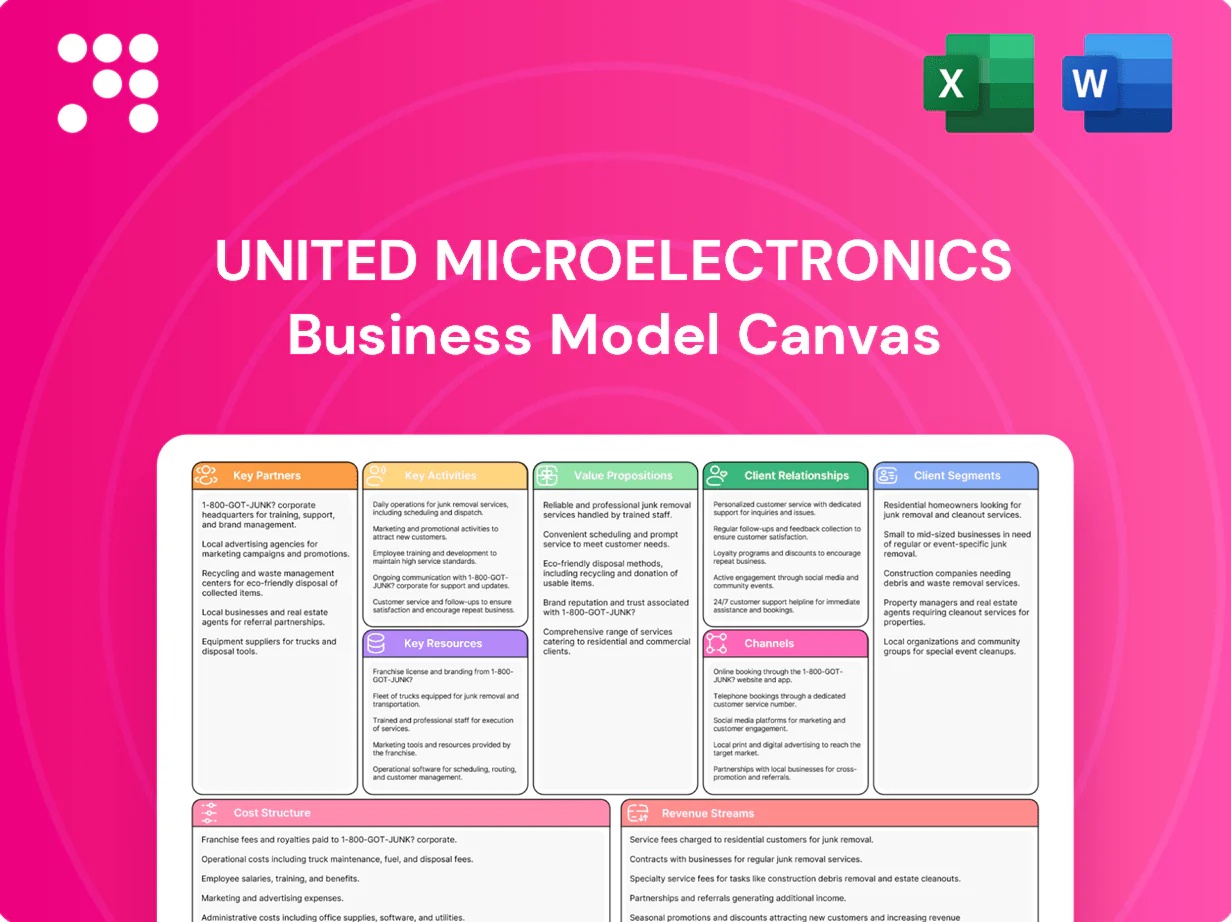

United Microelectronics Business Model Canvas

Fab-Centric Business Model Canvas — Downloadable Template for Investors and Strategists

Unlock the full Business Model Canvas for United Microelectronics and see how its fab-centric value proposition, strategic partnerships, and revenue streams drive semiconductor competitiveness. This concise, downloadable canvas (Word & Excel) is perfect for investors, strategists, and founders seeking actionable, ready-to-use insights to benchmark and scale. Purchase the complete template to map opportunities and risks with precision.

Partnerships

Equipment and Materials Suppliers

Strategic ties with lithography, deposition and etch vendors secure both leading-edge and mature-node capability, supporting UMC’s 2024 capital expansion (capex ~US$2.8B) and ~7% global foundry share. Preferred supply agreements for photoresists, specialty gases, wafers and chemicals stabilize yields and cost, targeting >99.9% supply SLA performance. Joint roadmaps align tool upgrades with process shrinks and specialty nodes, while service SLAs minimize downtime and accelerate volume ramps.

EDA and IP Ecosystem Partners

UMC’s partnerships with major EDA vendors (Cadence, Synopsys) and IP providers (Arm, others) deliver validated PDKs, reference flows and verified IP blocks that shorten customer design cycles and lower tape-out risk. Industry EDA market size reached about $13 billion in 2024, underscoring ecosystem importance for tool and IP investment. Joint enablement embeds design-for-manufacturability into flows, while continuous certification sustains multi-node compatibility.

OSAT and Packaging/Test Providers

Alliances with leading OSATs enable seamless wafer-to-package transitions, leveraging a 2024 global OSAT market of roughly US$36 billion to scale WLCSP, flip-chip and SiP production. Co-qualified flows include AEC-Q100 automotive-grade test and synchronized process handoffs. Coordinated planning shortens cycle time and stabilizes yield, while shared quality data tightens outgoing reliability.

Key Fabless and IDM Customers

Long-term agreements with anchor fabless and IDM customers stabilize wafer loading and guide UMCs node investments; in 2024 UMC emphasized multi-year contracts to smooth capacity planning. Co-development projects align specialty processes with customer roadmaps, while early engagement improves design kits and accelerates yield learning cycles. Volume commitments underpin predictable capacity allocation and investment timing.

- Anchor contracts: multi-year capacity stability

- Co-development: process-roadmap alignment

- Early engagement: DKT and yield improvement

- Volume commitments: capacity planning

Universities and Research Institutes

Universities and research institutes drive UMC’s specialty roadmaps by co-developing RF, eNVM, BCD and HV process modules, shortening time-to-prototype and improving yield via shared labs and joint grants in 2024.

These partnerships supply a steady talent pipeline—many hires come from partner programs—and peer-reviewed publications from 2024 collaborations increased technology credibility and ecosystem adoption.

- R&D focus: RF, eNVM, BCD, HV

- De-risking: shared labs + grants

- Talent: pipeline strengthens engineering depth

- Evidence: 2024 publications boosted adoption

Supplier alliances back US$2.8B capex, boost tape-outs and packaging

Supplier alliances back UMC’s 2024 capex ~US$2.8B and ~7% global foundry share. EDA/IP and OSAT partners (EDA ~US$13B, OSAT ~US$36B in 2024) speed tape-outs and package ramps. Multi-year customer contracts and university R&D de-risk specialty nodes and supply of talent.

| Partnership | 2024 metric | Impact |

|---|---|---|

| Suppliers | Capex US$2.8B | Capacity & yield |

| EDA/IP | EDA US$13B | Faster design-to-volume |

| OSAT | OSAT US$36B | Package scale |

| Customers/Academia | Multi-year deals & grants | De-risking & talent |

What is included in the product

A comprehensive Business Model Canvas for United Microelectronics detailing customer segments, channels, value propositions, key partners and resources, revenue streams and cost structure, with SWOT-linked insights and real-world operational alignment for investor and strategic use.

High-level view of United Microelectronics’ business model with editable cells—quickly map UMC’s foundry capabilities, customer segments, and cost structure to remove ambiguity and accelerate strategic decisions.

Activities

Wafer Fabrication and Operations

High-volume manufacturing on UMCs 200mm (8-inch) and 300mm (12-inch) lines anchors operations; SPC, APC and MES frameworks monitor >95% of process steps to sustain yields and cycle times. Continuous tool matching and recipe optimization lower variability across fabs, while logistics and production planning deliver to diverse market SLAs with industry-grade on-time delivery performance.

Process Development and Qualification

Development of logic, mixed-signal, RF, eNVM and specialty nodes underpins UMCs differentiation, driving node roadmaps and customer wins; as the third-largest pure-play foundry as of 2024, UMC targets niche segments. Automotive and industrial qualifications ensure reliability for long-life cycles and safety standards. Design rules, PDKs and IP enablement flow directly from process qualification. Continuous platform updates keep nodes competitive in 2024 markets.

Yield Engineering and Reliability

Defect reduction via focused FA and YMS analytics drives yield ramps by pinpointing root causes and enabling statistical process control across nodes. HALT/HASS and extended stress testing simulate multi-year wear to assure long-term reliability before production release. Closed-loop learning converts FA findings and customer returns data into process fixes and control-plan updates to reduce escapes and improve field returns handling.

Capacity Planning and Supply Chain Management

Forecasting translates customer demand into fab loading and capex timing, aligning wafer starts and equipment investments to meet prioritized nodes. Multi-sourcing of critical materials mitigates supplier disruptions and secures long-lead items. Cycle-time management balances product mix and priority lots while inventory policies protect target service levels.

- Forecasting: demand→fab loading, capex timing

- Multi-sourcing: reduce supply disruption risk

- Cycle-time: mix vs priority lot balance

- Inventory: safeguard service levels

Customer Enablement and Tape-Out Support

UMC delivers validated PDKs and DRC/LVS sign-off to accelerate customer tape-outs; 2024 MPW shuttles cut prototype mask cost by up to 90% and often shorten lead time to 6–12 weeks. Proactive DFM reviews reduce re-spin rates and NREs, mask-data prep and reticle logistics ensure smooth starts, and joint debug shortens time-to-yield.

- PDK delivery

- DRC/LVS sign-off

- MPW shuttles: -90% mask cost, 6–12w

- DFM reviews cut re-spins

- Mask prep & reticle logistics

- Joint debug → faster yield

200/300mm fabs: >95% SPC/APC/MES; MPW cuts mask cost 90%; prototypes 6-12 weeks

High-volume 200/300mm fabs with SPC/APC/MES monitoring >95% of process steps; MPW shuttles cut mask cost ~90% and shorten prototype lead times to 6–12 weeks. Node development (logic, RF, eNVM) supports automotive/industrial qualifications as the third-largest pure-play foundry in 2024. Forecasting, multi-sourcing and closed-loop FA reduce escapes and stabilize cycle-time.

| Metric | Value |

|---|---|

| Process monitoring | >95% |

| MPW mask cost | -90% |

| Prototype LT | 6–12 weeks |

| Rank (2024) | #3 pure-play |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for United Microelectronics you’re previewing is the actual deliverable, not a mockup. When you purchase, you’ll receive this same document—complete and editable—formatted for immediate use in Word and Excel. No placeholders, no omissions; what you see is what you’ll download.

Fab-Centric Business Model Canvas — Downloadable Template for Investors and Strategists

Unlock the full Business Model Canvas for United Microelectronics and see how its fab-centric value proposition, strategic partnerships, and revenue streams drive semiconductor competitiveness. This concise, downloadable canvas (Word & Excel) is perfect for investors, strategists, and founders seeking actionable, ready-to-use insights to benchmark and scale. Purchase the complete template to map opportunities and risks with precision.

Partnerships

Equipment and Materials Suppliers

Strategic ties with lithography, deposition and etch vendors secure both leading-edge and mature-node capability, supporting UMC’s 2024 capital expansion (capex ~US$2.8B) and ~7% global foundry share. Preferred supply agreements for photoresists, specialty gases, wafers and chemicals stabilize yields and cost, targeting >99.9% supply SLA performance. Joint roadmaps align tool upgrades with process shrinks and specialty nodes, while service SLAs minimize downtime and accelerate volume ramps.

EDA and IP Ecosystem Partners

UMC’s partnerships with major EDA vendors (Cadence, Synopsys) and IP providers (Arm, others) deliver validated PDKs, reference flows and verified IP blocks that shorten customer design cycles and lower tape-out risk. Industry EDA market size reached about $13 billion in 2024, underscoring ecosystem importance for tool and IP investment. Joint enablement embeds design-for-manufacturability into flows, while continuous certification sustains multi-node compatibility.

OSAT and Packaging/Test Providers

Alliances with leading OSATs enable seamless wafer-to-package transitions, leveraging a 2024 global OSAT market of roughly US$36 billion to scale WLCSP, flip-chip and SiP production. Co-qualified flows include AEC-Q100 automotive-grade test and synchronized process handoffs. Coordinated planning shortens cycle time and stabilizes yield, while shared quality data tightens outgoing reliability.

Key Fabless and IDM Customers

Long-term agreements with anchor fabless and IDM customers stabilize wafer loading and guide UMCs node investments; in 2024 UMC emphasized multi-year contracts to smooth capacity planning. Co-development projects align specialty processes with customer roadmaps, while early engagement improves design kits and accelerates yield learning cycles. Volume commitments underpin predictable capacity allocation and investment timing.

- Anchor contracts: multi-year capacity stability

- Co-development: process-roadmap alignment

- Early engagement: DKT and yield improvement

- Volume commitments: capacity planning

Universities and Research Institutes

Universities and research institutes drive UMC’s specialty roadmaps by co-developing RF, eNVM, BCD and HV process modules, shortening time-to-prototype and improving yield via shared labs and joint grants in 2024.

These partnerships supply a steady talent pipeline—many hires come from partner programs—and peer-reviewed publications from 2024 collaborations increased technology credibility and ecosystem adoption.

- R&D focus: RF, eNVM, BCD, HV

- De-risking: shared labs + grants

- Talent: pipeline strengthens engineering depth

- Evidence: 2024 publications boosted adoption

Supplier alliances back US$2.8B capex, boost tape-outs and packaging

Supplier alliances back UMC’s 2024 capex ~US$2.8B and ~7% global foundry share. EDA/IP and OSAT partners (EDA ~US$13B, OSAT ~US$36B in 2024) speed tape-outs and package ramps. Multi-year customer contracts and university R&D de-risk specialty nodes and supply of talent.

| Partnership | 2024 metric | Impact |

|---|---|---|

| Suppliers | Capex US$2.8B | Capacity & yield |

| EDA/IP | EDA US$13B | Faster design-to-volume |

| OSAT | OSAT US$36B | Package scale |

| Customers/Academia | Multi-year deals & grants | De-risking & talent |

What is included in the product

A comprehensive Business Model Canvas for United Microelectronics detailing customer segments, channels, value propositions, key partners and resources, revenue streams and cost structure, with SWOT-linked insights and real-world operational alignment for investor and strategic use.

High-level view of United Microelectronics’ business model with editable cells—quickly map UMC’s foundry capabilities, customer segments, and cost structure to remove ambiguity and accelerate strategic decisions.

Activities

Wafer Fabrication and Operations

High-volume manufacturing on UMCs 200mm (8-inch) and 300mm (12-inch) lines anchors operations; SPC, APC and MES frameworks monitor >95% of process steps to sustain yields and cycle times. Continuous tool matching and recipe optimization lower variability across fabs, while logistics and production planning deliver to diverse market SLAs with industry-grade on-time delivery performance.

Process Development and Qualification

Development of logic, mixed-signal, RF, eNVM and specialty nodes underpins UMCs differentiation, driving node roadmaps and customer wins; as the third-largest pure-play foundry as of 2024, UMC targets niche segments. Automotive and industrial qualifications ensure reliability for long-life cycles and safety standards. Design rules, PDKs and IP enablement flow directly from process qualification. Continuous platform updates keep nodes competitive in 2024 markets.

Yield Engineering and Reliability

Defect reduction via focused FA and YMS analytics drives yield ramps by pinpointing root causes and enabling statistical process control across nodes. HALT/HASS and extended stress testing simulate multi-year wear to assure long-term reliability before production release. Closed-loop learning converts FA findings and customer returns data into process fixes and control-plan updates to reduce escapes and improve field returns handling.

Capacity Planning and Supply Chain Management

Forecasting translates customer demand into fab loading and capex timing, aligning wafer starts and equipment investments to meet prioritized nodes. Multi-sourcing of critical materials mitigates supplier disruptions and secures long-lead items. Cycle-time management balances product mix and priority lots while inventory policies protect target service levels.

- Forecasting: demand→fab loading, capex timing

- Multi-sourcing: reduce supply disruption risk

- Cycle-time: mix vs priority lot balance

- Inventory: safeguard service levels

Customer Enablement and Tape-Out Support

UMC delivers validated PDKs and DRC/LVS sign-off to accelerate customer tape-outs; 2024 MPW shuttles cut prototype mask cost by up to 90% and often shorten lead time to 6–12 weeks. Proactive DFM reviews reduce re-spin rates and NREs, mask-data prep and reticle logistics ensure smooth starts, and joint debug shortens time-to-yield.

- PDK delivery

- DRC/LVS sign-off

- MPW shuttles: -90% mask cost, 6–12w

- DFM reviews cut re-spins

- Mask prep & reticle logistics

- Joint debug → faster yield

200/300mm fabs: >95% SPC/APC/MES; MPW cuts mask cost 90%; prototypes 6-12 weeks

High-volume 200/300mm fabs with SPC/APC/MES monitoring >95% of process steps; MPW shuttles cut mask cost ~90% and shorten prototype lead times to 6–12 weeks. Node development (logic, RF, eNVM) supports automotive/industrial qualifications as the third-largest pure-play foundry in 2024. Forecasting, multi-sourcing and closed-loop FA reduce escapes and stabilize cycle-time.

| Metric | Value |

|---|---|

| Process monitoring | >95% |

| MPW mask cost | -90% |

| Prototype LT | 6–12 weeks |

| Rank (2024) | #3 pure-play |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for United Microelectronics you’re previewing is the actual deliverable, not a mockup. When you purchase, you’ll receive this same document—complete and editable—formatted for immediate use in Word and Excel. No placeholders, no omissions; what you see is what you’ll download.

Original: $10.00

-65%$10.00

$3.50Description

Fab-Centric Business Model Canvas — Downloadable Template for Investors and Strategists

Unlock the full Business Model Canvas for United Microelectronics and see how its fab-centric value proposition, strategic partnerships, and revenue streams drive semiconductor competitiveness. This concise, downloadable canvas (Word & Excel) is perfect for investors, strategists, and founders seeking actionable, ready-to-use insights to benchmark and scale. Purchase the complete template to map opportunities and risks with precision.

Partnerships

Equipment and Materials Suppliers

Strategic ties with lithography, deposition and etch vendors secure both leading-edge and mature-node capability, supporting UMC’s 2024 capital expansion (capex ~US$2.8B) and ~7% global foundry share. Preferred supply agreements for photoresists, specialty gases, wafers and chemicals stabilize yields and cost, targeting >99.9% supply SLA performance. Joint roadmaps align tool upgrades with process shrinks and specialty nodes, while service SLAs minimize downtime and accelerate volume ramps.

EDA and IP Ecosystem Partners

UMC’s partnerships with major EDA vendors (Cadence, Synopsys) and IP providers (Arm, others) deliver validated PDKs, reference flows and verified IP blocks that shorten customer design cycles and lower tape-out risk. Industry EDA market size reached about $13 billion in 2024, underscoring ecosystem importance for tool and IP investment. Joint enablement embeds design-for-manufacturability into flows, while continuous certification sustains multi-node compatibility.

OSAT and Packaging/Test Providers

Alliances with leading OSATs enable seamless wafer-to-package transitions, leveraging a 2024 global OSAT market of roughly US$36 billion to scale WLCSP, flip-chip and SiP production. Co-qualified flows include AEC-Q100 automotive-grade test and synchronized process handoffs. Coordinated planning shortens cycle time and stabilizes yield, while shared quality data tightens outgoing reliability.

Key Fabless and IDM Customers

Long-term agreements with anchor fabless and IDM customers stabilize wafer loading and guide UMCs node investments; in 2024 UMC emphasized multi-year contracts to smooth capacity planning. Co-development projects align specialty processes with customer roadmaps, while early engagement improves design kits and accelerates yield learning cycles. Volume commitments underpin predictable capacity allocation and investment timing.

- Anchor contracts: multi-year capacity stability

- Co-development: process-roadmap alignment

- Early engagement: DKT and yield improvement

- Volume commitments: capacity planning

Universities and Research Institutes

Universities and research institutes drive UMC’s specialty roadmaps by co-developing RF, eNVM, BCD and HV process modules, shortening time-to-prototype and improving yield via shared labs and joint grants in 2024.

These partnerships supply a steady talent pipeline—many hires come from partner programs—and peer-reviewed publications from 2024 collaborations increased technology credibility and ecosystem adoption.

- R&D focus: RF, eNVM, BCD, HV

- De-risking: shared labs + grants

- Talent: pipeline strengthens engineering depth

- Evidence: 2024 publications boosted adoption

Supplier alliances back US$2.8B capex, boost tape-outs and packaging

Supplier alliances back UMC’s 2024 capex ~US$2.8B and ~7% global foundry share. EDA/IP and OSAT partners (EDA ~US$13B, OSAT ~US$36B in 2024) speed tape-outs and package ramps. Multi-year customer contracts and university R&D de-risk specialty nodes and supply of talent.

| Partnership | 2024 metric | Impact |

|---|---|---|

| Suppliers | Capex US$2.8B | Capacity & yield |

| EDA/IP | EDA US$13B | Faster design-to-volume |

| OSAT | OSAT US$36B | Package scale |

| Customers/Academia | Multi-year deals & grants | De-risking & talent |

What is included in the product

A comprehensive Business Model Canvas for United Microelectronics detailing customer segments, channels, value propositions, key partners and resources, revenue streams and cost structure, with SWOT-linked insights and real-world operational alignment for investor and strategic use.

High-level view of United Microelectronics’ business model with editable cells—quickly map UMC’s foundry capabilities, customer segments, and cost structure to remove ambiguity and accelerate strategic decisions.

Activities

Wafer Fabrication and Operations

High-volume manufacturing on UMCs 200mm (8-inch) and 300mm (12-inch) lines anchors operations; SPC, APC and MES frameworks monitor >95% of process steps to sustain yields and cycle times. Continuous tool matching and recipe optimization lower variability across fabs, while logistics and production planning deliver to diverse market SLAs with industry-grade on-time delivery performance.

Process Development and Qualification

Development of logic, mixed-signal, RF, eNVM and specialty nodes underpins UMCs differentiation, driving node roadmaps and customer wins; as the third-largest pure-play foundry as of 2024, UMC targets niche segments. Automotive and industrial qualifications ensure reliability for long-life cycles and safety standards. Design rules, PDKs and IP enablement flow directly from process qualification. Continuous platform updates keep nodes competitive in 2024 markets.

Yield Engineering and Reliability

Defect reduction via focused FA and YMS analytics drives yield ramps by pinpointing root causes and enabling statistical process control across nodes. HALT/HASS and extended stress testing simulate multi-year wear to assure long-term reliability before production release. Closed-loop learning converts FA findings and customer returns data into process fixes and control-plan updates to reduce escapes and improve field returns handling.

Capacity Planning and Supply Chain Management

Forecasting translates customer demand into fab loading and capex timing, aligning wafer starts and equipment investments to meet prioritized nodes. Multi-sourcing of critical materials mitigates supplier disruptions and secures long-lead items. Cycle-time management balances product mix and priority lots while inventory policies protect target service levels.

- Forecasting: demand→fab loading, capex timing

- Multi-sourcing: reduce supply disruption risk

- Cycle-time: mix vs priority lot balance

- Inventory: safeguard service levels

Customer Enablement and Tape-Out Support

UMC delivers validated PDKs and DRC/LVS sign-off to accelerate customer tape-outs; 2024 MPW shuttles cut prototype mask cost by up to 90% and often shorten lead time to 6–12 weeks. Proactive DFM reviews reduce re-spin rates and NREs, mask-data prep and reticle logistics ensure smooth starts, and joint debug shortens time-to-yield.

- PDK delivery

- DRC/LVS sign-off

- MPW shuttles: -90% mask cost, 6–12w

- DFM reviews cut re-spins

- Mask prep & reticle logistics

- Joint debug → faster yield

200/300mm fabs: >95% SPC/APC/MES; MPW cuts mask cost 90%; prototypes 6-12 weeks

High-volume 200/300mm fabs with SPC/APC/MES monitoring >95% of process steps; MPW shuttles cut mask cost ~90% and shorten prototype lead times to 6–12 weeks. Node development (logic, RF, eNVM) supports automotive/industrial qualifications as the third-largest pure-play foundry in 2024. Forecasting, multi-sourcing and closed-loop FA reduce escapes and stabilize cycle-time.

| Metric | Value |

|---|---|

| Process monitoring | >95% |

| MPW mask cost | -90% |

| Prototype LT | 6–12 weeks |

| Rank (2024) | #3 pure-play |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for United Microelectronics you’re previewing is the actual deliverable, not a mockup. When you purchase, you’ll receive this same document—complete and editable—formatted for immediate use in Word and Excel. No placeholders, no omissions; what you see is what you’ll download.