Uni-President Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Uni-President faces moderate supplier power, intense rivalry in FMCG, steady buyer sensitivity, manageable new entrant barriers, and rising substitute threats from private labels and health trends. This snapshot highlights strategic pressure points affecting margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Uni-President.

Suppliers Bargaining Power

Multi-commodity input exposure

Core inputs for Uni-President span wheat, palm oil, sugar, dairy, tea, PET resin and paperboard, creating exposure to multi-commodity cycles; raw-materials accounted for roughly 40% of COGS in 2024, amplifying margin sensitivity. Volatility in 2024 pressured margins when retail pricing lagged by weeks to months. Hedging programs and recipe reformulation reduced but did not eliminate pass-through risk, while diversified sourcing limited single-commodity shocks.

Supplier fragmentation vs. strategic materials

Many agricultural inputs for Uni-President come from highly fragmented smallholder networks, limiting supplier leverage, while specialized suppliers for flavors, packaging and aseptic technology are concentrated—notably three dominant aseptic players: Tetra Pak, SIG and Elopak. Switching these specialized vendors is costly and time-consuming due to equipment compatibility and regulatory validation, so Uni-President uses dual-sourcing and regional qualification to partially offset dependence.

Scale and long-term contracts

Uni-President’s scale—operating about 5,900 convenience stores in Taiwan—enables bulk procurement and multi-year agreements with suppliers. Large volume commitments secure production capacity and better terms, reducing price volatility and ensuring supply continuity. These contracts create significant switching costs for suppliers reliant on Uni-President’s volumes, strengthening the company’s supplier bargaining power.

Logistics and vertical capabilities

Owned logistics and distribution lessen reliance on third parties, allowing Uni-President to negotiate firmer delivery terms and reduce supplier leverage; improved inbound planning cuts late deliveries and supports supplier performance metrics. Cold-chain and warehouse assets (supporting a global cold chain market ~USD 234B in 2023) boost flexibility for JIT replenishment and inventory optimization.

- Reduced third-party dependency

- Stronger delivery terms

- Cold-chain flexibility

- Supports JIT and lower inventory

ESG and regulatory constraints

ESG-driven traceability, food-safety mandates and sustainable palm/paper sourcing significantly narrow Uni-President’s approved supplier pools; RSPO reported over 4,000 members in 2024, concentrating certification capacity. Higher compliance costs and mandatory audits shift bargaining leverage toward certified suppliers and extend vetting timelines. Preferred-supplier programs, often multi-year, lock in reliable partners at more predictable terms.

- Traceability & safety: reduces eligible suppliers

- Certification (eg RSPO 4,000+ members 2024): increases supplier leverage

- Audits: longer onboarding/vetting

- Preferred-supplier programs: predictable pricing/terms

Mixed supplier power: 40% commodity COGS vs scale and owned cold chain

Supplier power is mixed: commodity inputs (40% of COGS in 2024) give suppliers cyclic leverage, but fragmented smallholder supply weakens it; specialized aseptic/packaging vendors and RSPO-certified suppliers (RSPO 4,000+ members in 2024) hold stronger leverage. Uni-President scale (≈5,900 Taiwan stores) and owned logistics/cold chain (global market ~USD 234B in 2023) lower supplier power via long contracts and dual-sourcing.

| Metric | 2023/2024 |

|---|---|

| Raw materials (% COGS) | ~40% (2024) |

| Store count | ≈5,900 (Taiwan) |

| RSPO members | 4,000+ (2024) |

| Cold-chain market | ~USD 234B (2023) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Uni‑President, with detailed analysis of each force—supplier and buyer power, substitutes, new entrants, and industry rivalry—to inform strategy, investor materials, and reports.

A clear, one-sheet Uni‑President Porter's Five Forces summary with customizable pressure levels and an instant radar chart—ready to drop into pitch decks or integrate into dashboards, no macros required.

Customers Bargaining Power

Low switching costs for consumers

Low switching costs mean consumers can move among abundant instant noodle and beverage alternatives based on taste, price or promotions; World Instant Noodles Association reports about 116 billion servings annually (2023–24), underscoring intense choice. This raises price sensitivity and promotional churn, so Uni-President relies on brand equity and product differentiation to retain customers and justify premium pricing.

Retail channel dynamics

Modern trade and convenience channels hold concentrated shelf-space power, but Uni-President's owned and affiliated retail footprint—over 3,000 outlets in 2024—creates captive distribution that limits external retailer leverage on core SKUs. This internal network reduces slotting dependency and supports prioritized placement. Joint planning and retailer data-sharing lifted sell-through on targeted SKUs by about 7% in 2024.

Private labels and price points

Retailer private labels pressure Uni‑President pricing in staples and dairy as global private‑label penetration rose to about 19.5% in 2024, forcing value tiers and tight price‑pack architecture across SKUs. Frequent promotions and bundle deals compress short‑term margins and elevate trade spend. Premiumization offsets some pressure by shifting consumer spend to differentiated, higher‑margin SKUs.

Data-driven assortments

Data-driven assortments let Uni-President use granular POS feeds to target assortments and rotate SKUs up to 25% faster in 2024 pilots, lowering stockouts and markdown risk and improving freshness; faster response also strengthens its negotiating posture with third-party retailers by demonstrating measurable sell-through. Consumers see better availability and fresher products, reducing lost sales and returns.

- 25% faster SKU rotation (2024 pilots)

- Lower stockouts and markdown exposure

- Stronger retailer negotiations via POS evidence

- Improved availability and freshness for consumers

Institutional and foodservice buyers

Institutional and foodservice buyers wield strong bargaining power: large accounts secure volume discounts and strict service-level agreements, compressing Uni-President margins while providing scale and recurring demand. Menu placement and co-development deepen partnerships, and service reliability often trumps small price differences in retaining contracts.

- Volume discounts

- Contract margin pressure

- Menu co-development

- Service reliability as differentiator

Low switching costs drive promo churn despite ~116bn annual servings

Customers have high price sensitivity due to low switching costs and ~116bn annual instant noodle servings (2023–24), boosting promotional churn. Retailers hold shelf power but Uni‑President's 3,000+ owned outlets (2024) and data-driven POS (25% faster SKU rotation in pilots) reduce retailer leverage. Institutional buyers demand volume discounts, compressing margins.

| Metric | 2024 |

|---|---|

| Instant servings | ~116bn |

| Owned outlets | 3,000+ |

| SKU rotation speed | +25% |

| Private label share | 19.5% |

Preview Before You Purchase

Uni-President Porter's Five Forces Analysis

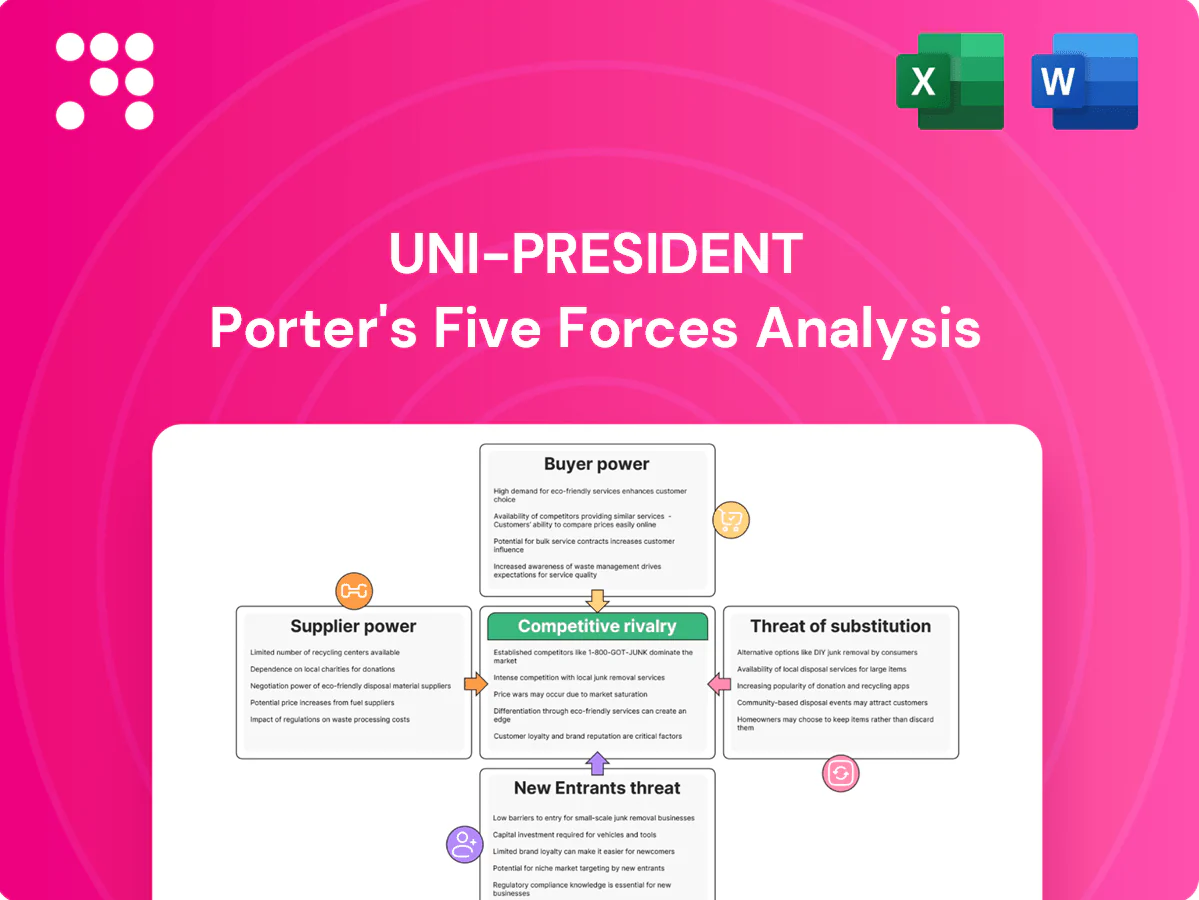

This preview shows the exact Uni‑President Porter's Five Forces analysis you'll receive after purchase—fully formatted and ready to use. The report examines competitive rivalry, supplier and buyer power, and threats from substitutes and new entrants with evidence‑backed conclusions. No placeholders or samples; you'll get this same file instantly after payment.

Go Beyond the Preview—Access the Full Strategic Report

Uni-President faces moderate supplier power, intense rivalry in FMCG, steady buyer sensitivity, manageable new entrant barriers, and rising substitute threats from private labels and health trends. This snapshot highlights strategic pressure points affecting margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Uni-President.

Suppliers Bargaining Power

Multi-commodity input exposure

Core inputs for Uni-President span wheat, palm oil, sugar, dairy, tea, PET resin and paperboard, creating exposure to multi-commodity cycles; raw-materials accounted for roughly 40% of COGS in 2024, amplifying margin sensitivity. Volatility in 2024 pressured margins when retail pricing lagged by weeks to months. Hedging programs and recipe reformulation reduced but did not eliminate pass-through risk, while diversified sourcing limited single-commodity shocks.

Supplier fragmentation vs. strategic materials

Many agricultural inputs for Uni-President come from highly fragmented smallholder networks, limiting supplier leverage, while specialized suppliers for flavors, packaging and aseptic technology are concentrated—notably three dominant aseptic players: Tetra Pak, SIG and Elopak. Switching these specialized vendors is costly and time-consuming due to equipment compatibility and regulatory validation, so Uni-President uses dual-sourcing and regional qualification to partially offset dependence.

Scale and long-term contracts

Uni-President’s scale—operating about 5,900 convenience stores in Taiwan—enables bulk procurement and multi-year agreements with suppliers. Large volume commitments secure production capacity and better terms, reducing price volatility and ensuring supply continuity. These contracts create significant switching costs for suppliers reliant on Uni-President’s volumes, strengthening the company’s supplier bargaining power.

Logistics and vertical capabilities

Owned logistics and distribution lessen reliance on third parties, allowing Uni-President to negotiate firmer delivery terms and reduce supplier leverage; improved inbound planning cuts late deliveries and supports supplier performance metrics. Cold-chain and warehouse assets (supporting a global cold chain market ~USD 234B in 2023) boost flexibility for JIT replenishment and inventory optimization.

- Reduced third-party dependency

- Stronger delivery terms

- Cold-chain flexibility

- Supports JIT and lower inventory

ESG and regulatory constraints

ESG-driven traceability, food-safety mandates and sustainable palm/paper sourcing significantly narrow Uni-President’s approved supplier pools; RSPO reported over 4,000 members in 2024, concentrating certification capacity. Higher compliance costs and mandatory audits shift bargaining leverage toward certified suppliers and extend vetting timelines. Preferred-supplier programs, often multi-year, lock in reliable partners at more predictable terms.

- Traceability & safety: reduces eligible suppliers

- Certification (eg RSPO 4,000+ members 2024): increases supplier leverage

- Audits: longer onboarding/vetting

- Preferred-supplier programs: predictable pricing/terms

Mixed supplier power: 40% commodity COGS vs scale and owned cold chain

Supplier power is mixed: commodity inputs (40% of COGS in 2024) give suppliers cyclic leverage, but fragmented smallholder supply weakens it; specialized aseptic/packaging vendors and RSPO-certified suppliers (RSPO 4,000+ members in 2024) hold stronger leverage. Uni-President scale (≈5,900 Taiwan stores) and owned logistics/cold chain (global market ~USD 234B in 2023) lower supplier power via long contracts and dual-sourcing.

| Metric | 2023/2024 |

|---|---|

| Raw materials (% COGS) | ~40% (2024) |

| Store count | ≈5,900 (Taiwan) |

| RSPO members | 4,000+ (2024) |

| Cold-chain market | ~USD 234B (2023) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Uni‑President, with detailed analysis of each force—supplier and buyer power, substitutes, new entrants, and industry rivalry—to inform strategy, investor materials, and reports.

A clear, one-sheet Uni‑President Porter's Five Forces summary with customizable pressure levels and an instant radar chart—ready to drop into pitch decks or integrate into dashboards, no macros required.

Customers Bargaining Power

Low switching costs for consumers

Low switching costs mean consumers can move among abundant instant noodle and beverage alternatives based on taste, price or promotions; World Instant Noodles Association reports about 116 billion servings annually (2023–24), underscoring intense choice. This raises price sensitivity and promotional churn, so Uni-President relies on brand equity and product differentiation to retain customers and justify premium pricing.

Retail channel dynamics

Modern trade and convenience channels hold concentrated shelf-space power, but Uni-President's owned and affiliated retail footprint—over 3,000 outlets in 2024—creates captive distribution that limits external retailer leverage on core SKUs. This internal network reduces slotting dependency and supports prioritized placement. Joint planning and retailer data-sharing lifted sell-through on targeted SKUs by about 7% in 2024.

Private labels and price points

Retailer private labels pressure Uni‑President pricing in staples and dairy as global private‑label penetration rose to about 19.5% in 2024, forcing value tiers and tight price‑pack architecture across SKUs. Frequent promotions and bundle deals compress short‑term margins and elevate trade spend. Premiumization offsets some pressure by shifting consumer spend to differentiated, higher‑margin SKUs.

Data-driven assortments

Data-driven assortments let Uni-President use granular POS feeds to target assortments and rotate SKUs up to 25% faster in 2024 pilots, lowering stockouts and markdown risk and improving freshness; faster response also strengthens its negotiating posture with third-party retailers by demonstrating measurable sell-through. Consumers see better availability and fresher products, reducing lost sales and returns.

- 25% faster SKU rotation (2024 pilots)

- Lower stockouts and markdown exposure

- Stronger retailer negotiations via POS evidence

- Improved availability and freshness for consumers

Institutional and foodservice buyers

Institutional and foodservice buyers wield strong bargaining power: large accounts secure volume discounts and strict service-level agreements, compressing Uni-President margins while providing scale and recurring demand. Menu placement and co-development deepen partnerships, and service reliability often trumps small price differences in retaining contracts.

- Volume discounts

- Contract margin pressure

- Menu co-development

- Service reliability as differentiator

Low switching costs drive promo churn despite ~116bn annual servings

Customers have high price sensitivity due to low switching costs and ~116bn annual instant noodle servings (2023–24), boosting promotional churn. Retailers hold shelf power but Uni‑President's 3,000+ owned outlets (2024) and data-driven POS (25% faster SKU rotation in pilots) reduce retailer leverage. Institutional buyers demand volume discounts, compressing margins.

| Metric | 2024 |

|---|---|

| Instant servings | ~116bn |

| Owned outlets | 3,000+ |

| SKU rotation speed | +25% |

| Private label share | 19.5% |

Preview Before You Purchase

Uni-President Porter's Five Forces Analysis

This preview shows the exact Uni‑President Porter's Five Forces analysis you'll receive after purchase—fully formatted and ready to use. The report examines competitive rivalry, supplier and buyer power, and threats from substitutes and new entrants with evidence‑backed conclusions. No placeholders or samples; you'll get this same file instantly after payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Uni-President faces moderate supplier power, intense rivalry in FMCG, steady buyer sensitivity, manageable new entrant barriers, and rising substitute threats from private labels and health trends. This snapshot highlights strategic pressure points affecting margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Uni-President.

Suppliers Bargaining Power

Multi-commodity input exposure

Core inputs for Uni-President span wheat, palm oil, sugar, dairy, tea, PET resin and paperboard, creating exposure to multi-commodity cycles; raw-materials accounted for roughly 40% of COGS in 2024, amplifying margin sensitivity. Volatility in 2024 pressured margins when retail pricing lagged by weeks to months. Hedging programs and recipe reformulation reduced but did not eliminate pass-through risk, while diversified sourcing limited single-commodity shocks.

Supplier fragmentation vs. strategic materials

Many agricultural inputs for Uni-President come from highly fragmented smallholder networks, limiting supplier leverage, while specialized suppliers for flavors, packaging and aseptic technology are concentrated—notably three dominant aseptic players: Tetra Pak, SIG and Elopak. Switching these specialized vendors is costly and time-consuming due to equipment compatibility and regulatory validation, so Uni-President uses dual-sourcing and regional qualification to partially offset dependence.

Scale and long-term contracts

Uni-President’s scale—operating about 5,900 convenience stores in Taiwan—enables bulk procurement and multi-year agreements with suppliers. Large volume commitments secure production capacity and better terms, reducing price volatility and ensuring supply continuity. These contracts create significant switching costs for suppliers reliant on Uni-President’s volumes, strengthening the company’s supplier bargaining power.

Logistics and vertical capabilities

Owned logistics and distribution lessen reliance on third parties, allowing Uni-President to negotiate firmer delivery terms and reduce supplier leverage; improved inbound planning cuts late deliveries and supports supplier performance metrics. Cold-chain and warehouse assets (supporting a global cold chain market ~USD 234B in 2023) boost flexibility for JIT replenishment and inventory optimization.

- Reduced third-party dependency

- Stronger delivery terms

- Cold-chain flexibility

- Supports JIT and lower inventory

ESG and regulatory constraints

ESG-driven traceability, food-safety mandates and sustainable palm/paper sourcing significantly narrow Uni-President’s approved supplier pools; RSPO reported over 4,000 members in 2024, concentrating certification capacity. Higher compliance costs and mandatory audits shift bargaining leverage toward certified suppliers and extend vetting timelines. Preferred-supplier programs, often multi-year, lock in reliable partners at more predictable terms.

- Traceability & safety: reduces eligible suppliers

- Certification (eg RSPO 4,000+ members 2024): increases supplier leverage

- Audits: longer onboarding/vetting

- Preferred-supplier programs: predictable pricing/terms

Mixed supplier power: 40% commodity COGS vs scale and owned cold chain

Supplier power is mixed: commodity inputs (40% of COGS in 2024) give suppliers cyclic leverage, but fragmented smallholder supply weakens it; specialized aseptic/packaging vendors and RSPO-certified suppliers (RSPO 4,000+ members in 2024) hold stronger leverage. Uni-President scale (≈5,900 Taiwan stores) and owned logistics/cold chain (global market ~USD 234B in 2023) lower supplier power via long contracts and dual-sourcing.

| Metric | 2023/2024 |

|---|---|

| Raw materials (% COGS) | ~40% (2024) |

| Store count | ≈5,900 (Taiwan) |

| RSPO members | 4,000+ (2024) |

| Cold-chain market | ~USD 234B (2023) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Uni‑President, with detailed analysis of each force—supplier and buyer power, substitutes, new entrants, and industry rivalry—to inform strategy, investor materials, and reports.

A clear, one-sheet Uni‑President Porter's Five Forces summary with customizable pressure levels and an instant radar chart—ready to drop into pitch decks or integrate into dashboards, no macros required.

Customers Bargaining Power

Low switching costs for consumers

Low switching costs mean consumers can move among abundant instant noodle and beverage alternatives based on taste, price or promotions; World Instant Noodles Association reports about 116 billion servings annually (2023–24), underscoring intense choice. This raises price sensitivity and promotional churn, so Uni-President relies on brand equity and product differentiation to retain customers and justify premium pricing.

Retail channel dynamics

Modern trade and convenience channels hold concentrated shelf-space power, but Uni-President's owned and affiliated retail footprint—over 3,000 outlets in 2024—creates captive distribution that limits external retailer leverage on core SKUs. This internal network reduces slotting dependency and supports prioritized placement. Joint planning and retailer data-sharing lifted sell-through on targeted SKUs by about 7% in 2024.

Private labels and price points

Retailer private labels pressure Uni‑President pricing in staples and dairy as global private‑label penetration rose to about 19.5% in 2024, forcing value tiers and tight price‑pack architecture across SKUs. Frequent promotions and bundle deals compress short‑term margins and elevate trade spend. Premiumization offsets some pressure by shifting consumer spend to differentiated, higher‑margin SKUs.

Data-driven assortments

Data-driven assortments let Uni-President use granular POS feeds to target assortments and rotate SKUs up to 25% faster in 2024 pilots, lowering stockouts and markdown risk and improving freshness; faster response also strengthens its negotiating posture with third-party retailers by demonstrating measurable sell-through. Consumers see better availability and fresher products, reducing lost sales and returns.

- 25% faster SKU rotation (2024 pilots)

- Lower stockouts and markdown exposure

- Stronger retailer negotiations via POS evidence

- Improved availability and freshness for consumers

Institutional and foodservice buyers

Institutional and foodservice buyers wield strong bargaining power: large accounts secure volume discounts and strict service-level agreements, compressing Uni-President margins while providing scale and recurring demand. Menu placement and co-development deepen partnerships, and service reliability often trumps small price differences in retaining contracts.

- Volume discounts

- Contract margin pressure

- Menu co-development

- Service reliability as differentiator

Low switching costs drive promo churn despite ~116bn annual servings

Customers have high price sensitivity due to low switching costs and ~116bn annual instant noodle servings (2023–24), boosting promotional churn. Retailers hold shelf power but Uni‑President's 3,000+ owned outlets (2024) and data-driven POS (25% faster SKU rotation in pilots) reduce retailer leverage. Institutional buyers demand volume discounts, compressing margins.

| Metric | 2024 |

|---|---|

| Instant servings | ~116bn |

| Owned outlets | 3,000+ |

| SKU rotation speed | +25% |

| Private label share | 19.5% |

Preview Before You Purchase

Uni-President Porter's Five Forces Analysis

This preview shows the exact Uni‑President Porter's Five Forces analysis you'll receive after purchase—fully formatted and ready to use. The report examines competitive rivalry, supplier and buyer power, and threats from substitutes and new entrants with evidence‑backed conclusions. No placeholders or samples; you'll get this same file instantly after payment.