Unicaja Banco Business Model Canvas

Concise banking Business Model Canvas: customers, value, revenue and partnerships

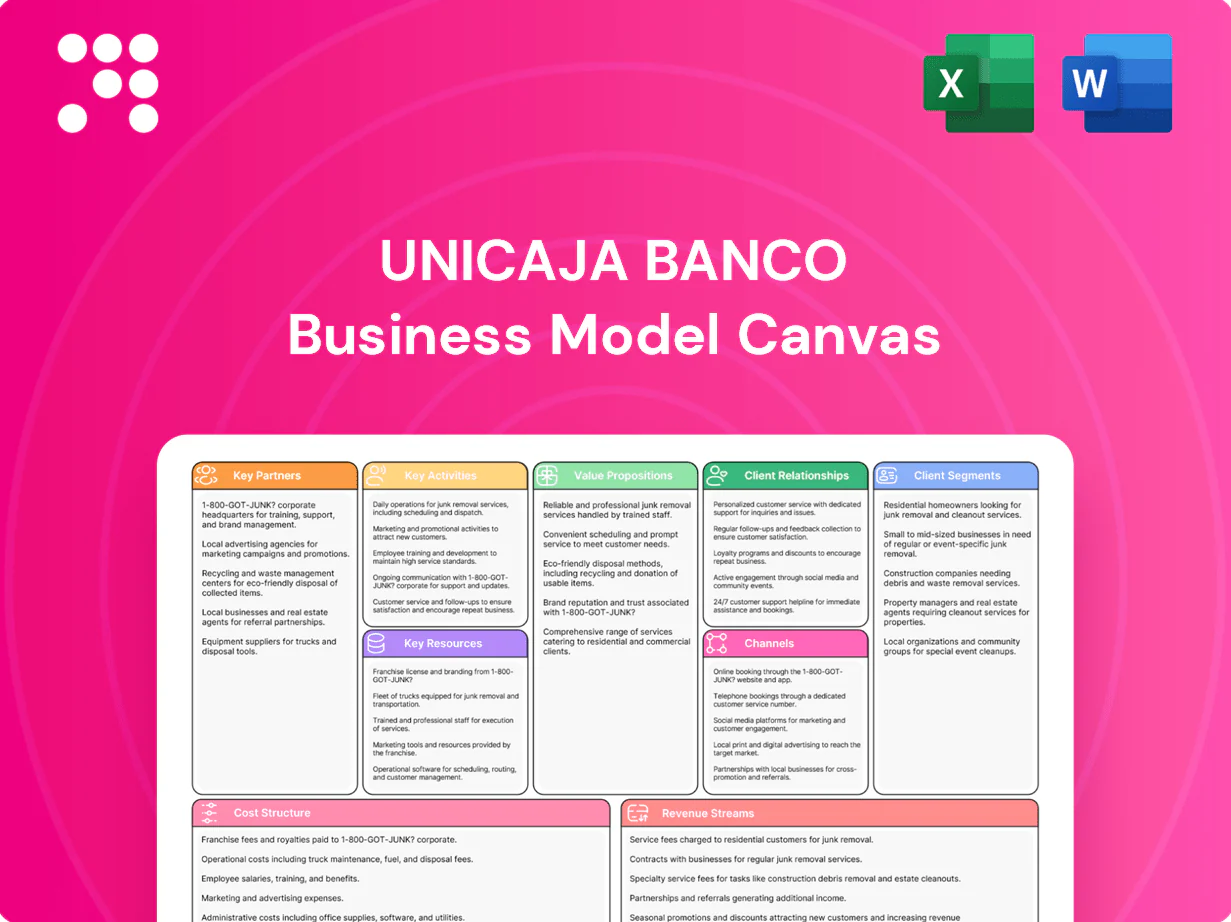

Discover Unicaja Banco’s strategic blueprint with our concise Business Model Canvas—revealing customer segments, core value propositions, revenue streams and key partnerships that drive profitability. This actionable snapshot is perfect for investors, advisors and entrepreneurs seeking practical insights. Purchase the full editable Word/Excel canvas to unlock section-by-section analysis and apply it to your strategy or due diligence.

Partnerships

Regulators and payment networks

Partnerships with Banco de España and the ECB secure regulatory compliance, access to central-bank liquidity facilities and consumer trust, supporting Unicaja Banco’s balance-sheet resilience. Ties with Visa, Mastercard and SEPA operators—which together handle over 80% of card and euro payments—enable seamless domestic and cross‑border transactions. These links underpin core transaction services, reduce operational risk and improve interoperability across Spain and the EU.

Technology and core-banking vendors

Alliances with core-banking, cloud, cybersecurity and analytics vendors power Unicaja Banco’s digital channels and ops, supporting uptime, scalability and rapid feature delivery. Vendor co-development has accelerated digital onboarding and AI-driven servicing, lowering time-to-market and managing tech risk. Post-merger pro forma assets reached about 115 billion EUR, underpinning ongoing tech investment.

Bancassurance and asset management partners

Insurance carriers and asset management partners extend Unicaja Banco beyond deposits and loans, leveraging the bank’s c.6.2 million customers and €91bn in assets (2024) to widen product breadth. Co-branded insurance and fund distribution added roughly 10% of non-interest fee income in 2024, boosting recurring commissions. Partners supply underwriting, product design and risk transfer, allowing Unicaja to scale offerings without underwriting exposure. Customers receive integrated protection and investment solutions through one distribution channel.

Corporate, SME, and public-sector ecosystems

Unicaja Banco, headquartered in Málaga and the largest regional bank in Andalusia, leverages local chambers, business associations, and municipalities to extend outreach across Andalusia (population ~8.4 million in 2024) and other regions. Collaboration supports SME financing programs and public projects, strengthening lending pipelines and guarantees while embedding the bank in regional economic development.

- regional-presence

- sme-finance

- public-projects

- lending-pipeline

- economic-development

Real estate and payment/fintech collaborators

In 2024 agreements with appraisers, servicers and real‑estate platforms underpin Unicaja Banco mortgage origination and collateral management, while fintech partners provide onboarding, KYC and alternative data to enhance credit models. Co‑innovation with payment and fintech collaborators improves UX, accelerates credit decisions and broadens distribution, lowering acquisition costs.

- Partnerships: appraisers, servicers, portals

- Fintech roles: onboarding, KYC, alternative data

- Benefits: faster decisions, improved UX, lower acquisition costs

Regulator-fintech-insurer ties secure liquidity, AI onboarding and €115bn assets

Partnerships with regulators, Visa/Mastercard and SEPA secure liquidity, compliance and 80%+ payments interoperability, supporting resilience. Tech and fintech vendors accelerate digital onboarding and AI servicing, leveraging pro‑forma €115bn assets and €91bn CET1-linked balance (2024) to cut time‑to‑market. Insurance, AM and servicers expand product reach across 6.2m customers, adding ~10% of non‑interest fees (2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Liquidity/compliance | €115bn pro‑forma |

| Fintechs/vendors | Digital/KYC/AI | 6.2m customers |

| Insurers/AM | Distribution | ~10% fees |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Unicaja Banco covering customer segments, channels, value propositions, revenue streams, key resources, activities, partners, cost structure and customer relationships with integrated SWOT insights; designed to reflect real-world operations and support presentations, investor discussions and strategic decision-making.

High-level, editable Business Model Canvas for Unicaja Banco that condenses strategy into a one-page snapshot, saving hours of structuring while enabling quick comparisons, team collaboration, and boardroom-ready executive summaries to pinpoint and relieve strategic pain points.

Activities

Deposit gathering and lending

Unicaja Banco focuses on attracting retail and corporate deposits to drive balance-sheet growth, reporting deposits of €64.8bn and gross loans of €48.2bn as of June 2024. Lending covers mortgages, consumer, SME and corporate credit, with pricing and term structures aligned to market rates and the bank’s risk appetite. Active portfolio monitoring and early-warning controls preserve asset quality, supporting a stable non-performing exposure ratio in 2024.

Risk, compliance, and capital management

Credit, market, liquidity and operational risk frameworks steer lending, trading and treasury limits, with Unicaja Banco maintaining a CET1 ratio of 12.4% and an LCR comfortably above the 100% regulatory minimum in 2024.

Digital transformation and IT operations

Maintaining mobile, online and core platforms is continuous for Unicaja Banco, supporting over 3 million digital users post-merger; agile delivery ships features and boosts reliability with biweekly sprints; data analytics powers personalization and fraud prevention, analyzing millions of transactions monthly; cybersecurity defends customers and infrastructure with continuous monitoring and regulatory compliance (PSD2, GDPR) and annual IT investment growth in recent years.

Wealth, investment, and insurance distribution

Advisory distributes funds, managed portfolios and pension products through dedicated wealth teams, while bancassurance cross-sells protection for retail customers and SMEs to boost retention and coverage.

Suitability checks and ESG preferences are embedded in recommendations to align risk and sustainability; recurring advisory and fee-based revenues diversify income streams and reduce interest-rate sensitivity.

- Advisory: funds, portfolios, pensions

- Bancassurance: retail + SME protection

- Advice shaped by suitability & ESG

- Recurring fees diversify revenues

Treasury and balance-sheet optimization

Treasury and balance-sheet optimization at Unicaja Banco uses ALM to manage interest-rate risk, liquidity buffers and funding costs, supporting securities portfolios that generate income and provide collateral; hedging programs stabilise net interest income and capital, underpinning profitability and solvency while complying with regulatory LCR >100% in 2024.

- ALM: interest-rate risk, liquidity, funding

- Securities: income & collateral

- Hedging: stabilises NII & capital

- Outcome: supports profitability & solvency

€64.8bn deposits, €48.2bn loans; CET1 12.4%, 3m+ users

Unicaja Banco drives growth by attracting €64.8bn deposits and deploying €48.2bn gross loans (Jun 2024), while lending spans mortgages, consumer, SME and corporate credit with active portfolio monitoring. Risk frameworks keep CET1 at 12.4% and LCR above 100% in 2024. Digital and advisory channels serve 3m+ users, cross-selling bancassurance and fee-based products to diversify revenues.

| Metric | 2024 |

|---|---|

| Deposits | €64.8bn |

| Gross loans | €48.2bn |

| CET1 ratio | 12.4% |

| LCR | >100% |

| Digital users | 3m+ |

What You See Is What You Get

Business Model Canvas

The Unicaja Banco Business Model Canvas shown here is the actual deliverable, not a mockup; it’s a direct excerpt from the file you’ll receive after purchase. When you complete your order, you’ll get the same comprehensive document in editable Word and Excel formats. It’s fully structured and ready to present, edit, or share—no surprises, just the exact canvas you see now.

Concise banking Business Model Canvas: customers, value, revenue and partnerships

Discover Unicaja Banco’s strategic blueprint with our concise Business Model Canvas—revealing customer segments, core value propositions, revenue streams and key partnerships that drive profitability. This actionable snapshot is perfect for investors, advisors and entrepreneurs seeking practical insights. Purchase the full editable Word/Excel canvas to unlock section-by-section analysis and apply it to your strategy or due diligence.

Partnerships

Regulators and payment networks

Partnerships with Banco de España and the ECB secure regulatory compliance, access to central-bank liquidity facilities and consumer trust, supporting Unicaja Banco’s balance-sheet resilience. Ties with Visa, Mastercard and SEPA operators—which together handle over 80% of card and euro payments—enable seamless domestic and cross‑border transactions. These links underpin core transaction services, reduce operational risk and improve interoperability across Spain and the EU.

Technology and core-banking vendors

Alliances with core-banking, cloud, cybersecurity and analytics vendors power Unicaja Banco’s digital channels and ops, supporting uptime, scalability and rapid feature delivery. Vendor co-development has accelerated digital onboarding and AI-driven servicing, lowering time-to-market and managing tech risk. Post-merger pro forma assets reached about 115 billion EUR, underpinning ongoing tech investment.

Bancassurance and asset management partners

Insurance carriers and asset management partners extend Unicaja Banco beyond deposits and loans, leveraging the bank’s c.6.2 million customers and €91bn in assets (2024) to widen product breadth. Co-branded insurance and fund distribution added roughly 10% of non-interest fee income in 2024, boosting recurring commissions. Partners supply underwriting, product design and risk transfer, allowing Unicaja to scale offerings without underwriting exposure. Customers receive integrated protection and investment solutions through one distribution channel.

Corporate, SME, and public-sector ecosystems

Unicaja Banco, headquartered in Málaga and the largest regional bank in Andalusia, leverages local chambers, business associations, and municipalities to extend outreach across Andalusia (population ~8.4 million in 2024) and other regions. Collaboration supports SME financing programs and public projects, strengthening lending pipelines and guarantees while embedding the bank in regional economic development.

- regional-presence

- sme-finance

- public-projects

- lending-pipeline

- economic-development

Real estate and payment/fintech collaborators

In 2024 agreements with appraisers, servicers and real‑estate platforms underpin Unicaja Banco mortgage origination and collateral management, while fintech partners provide onboarding, KYC and alternative data to enhance credit models. Co‑innovation with payment and fintech collaborators improves UX, accelerates credit decisions and broadens distribution, lowering acquisition costs.

- Partnerships: appraisers, servicers, portals

- Fintech roles: onboarding, KYC, alternative data

- Benefits: faster decisions, improved UX, lower acquisition costs

Regulator-fintech-insurer ties secure liquidity, AI onboarding and €115bn assets

Partnerships with regulators, Visa/Mastercard and SEPA secure liquidity, compliance and 80%+ payments interoperability, supporting resilience. Tech and fintech vendors accelerate digital onboarding and AI servicing, leveraging pro‑forma €115bn assets and €91bn CET1-linked balance (2024) to cut time‑to‑market. Insurance, AM and servicers expand product reach across 6.2m customers, adding ~10% of non‑interest fees (2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Liquidity/compliance | €115bn pro‑forma |

| Fintechs/vendors | Digital/KYC/AI | 6.2m customers |

| Insurers/AM | Distribution | ~10% fees |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Unicaja Banco covering customer segments, channels, value propositions, revenue streams, key resources, activities, partners, cost structure and customer relationships with integrated SWOT insights; designed to reflect real-world operations and support presentations, investor discussions and strategic decision-making.

High-level, editable Business Model Canvas for Unicaja Banco that condenses strategy into a one-page snapshot, saving hours of structuring while enabling quick comparisons, team collaboration, and boardroom-ready executive summaries to pinpoint and relieve strategic pain points.

Activities

Deposit gathering and lending

Unicaja Banco focuses on attracting retail and corporate deposits to drive balance-sheet growth, reporting deposits of €64.8bn and gross loans of €48.2bn as of June 2024. Lending covers mortgages, consumer, SME and corporate credit, with pricing and term structures aligned to market rates and the bank’s risk appetite. Active portfolio monitoring and early-warning controls preserve asset quality, supporting a stable non-performing exposure ratio in 2024.

Risk, compliance, and capital management

Credit, market, liquidity and operational risk frameworks steer lending, trading and treasury limits, with Unicaja Banco maintaining a CET1 ratio of 12.4% and an LCR comfortably above the 100% regulatory minimum in 2024.

Digital transformation and IT operations

Maintaining mobile, online and core platforms is continuous for Unicaja Banco, supporting over 3 million digital users post-merger; agile delivery ships features and boosts reliability with biweekly sprints; data analytics powers personalization and fraud prevention, analyzing millions of transactions monthly; cybersecurity defends customers and infrastructure with continuous monitoring and regulatory compliance (PSD2, GDPR) and annual IT investment growth in recent years.

Wealth, investment, and insurance distribution

Advisory distributes funds, managed portfolios and pension products through dedicated wealth teams, while bancassurance cross-sells protection for retail customers and SMEs to boost retention and coverage.

Suitability checks and ESG preferences are embedded in recommendations to align risk and sustainability; recurring advisory and fee-based revenues diversify income streams and reduce interest-rate sensitivity.

- Advisory: funds, portfolios, pensions

- Bancassurance: retail + SME protection

- Advice shaped by suitability & ESG

- Recurring fees diversify revenues

Treasury and balance-sheet optimization

Treasury and balance-sheet optimization at Unicaja Banco uses ALM to manage interest-rate risk, liquidity buffers and funding costs, supporting securities portfolios that generate income and provide collateral; hedging programs stabilise net interest income and capital, underpinning profitability and solvency while complying with regulatory LCR >100% in 2024.

- ALM: interest-rate risk, liquidity, funding

- Securities: income & collateral

- Hedging: stabilises NII & capital

- Outcome: supports profitability & solvency

€64.8bn deposits, €48.2bn loans; CET1 12.4%, 3m+ users

Unicaja Banco drives growth by attracting €64.8bn deposits and deploying €48.2bn gross loans (Jun 2024), while lending spans mortgages, consumer, SME and corporate credit with active portfolio monitoring. Risk frameworks keep CET1 at 12.4% and LCR above 100% in 2024. Digital and advisory channels serve 3m+ users, cross-selling bancassurance and fee-based products to diversify revenues.

| Metric | 2024 |

|---|---|

| Deposits | €64.8bn |

| Gross loans | €48.2bn |

| CET1 ratio | 12.4% |

| LCR | >100% |

| Digital users | 3m+ |

What You See Is What You Get

Business Model Canvas

The Unicaja Banco Business Model Canvas shown here is the actual deliverable, not a mockup; it’s a direct excerpt from the file you’ll receive after purchase. When you complete your order, you’ll get the same comprehensive document in editable Word and Excel formats. It’s fully structured and ready to present, edit, or share—no surprises, just the exact canvas you see now.

Original: $10.00

-65%$10.00

$3.50Description

Concise banking Business Model Canvas: customers, value, revenue and partnerships

Discover Unicaja Banco’s strategic blueprint with our concise Business Model Canvas—revealing customer segments, core value propositions, revenue streams and key partnerships that drive profitability. This actionable snapshot is perfect for investors, advisors and entrepreneurs seeking practical insights. Purchase the full editable Word/Excel canvas to unlock section-by-section analysis and apply it to your strategy or due diligence.

Partnerships

Regulators and payment networks

Partnerships with Banco de España and the ECB secure regulatory compliance, access to central-bank liquidity facilities and consumer trust, supporting Unicaja Banco’s balance-sheet resilience. Ties with Visa, Mastercard and SEPA operators—which together handle over 80% of card and euro payments—enable seamless domestic and cross‑border transactions. These links underpin core transaction services, reduce operational risk and improve interoperability across Spain and the EU.

Technology and core-banking vendors

Alliances with core-banking, cloud, cybersecurity and analytics vendors power Unicaja Banco’s digital channels and ops, supporting uptime, scalability and rapid feature delivery. Vendor co-development has accelerated digital onboarding and AI-driven servicing, lowering time-to-market and managing tech risk. Post-merger pro forma assets reached about 115 billion EUR, underpinning ongoing tech investment.

Bancassurance and asset management partners

Insurance carriers and asset management partners extend Unicaja Banco beyond deposits and loans, leveraging the bank’s c.6.2 million customers and €91bn in assets (2024) to widen product breadth. Co-branded insurance and fund distribution added roughly 10% of non-interest fee income in 2024, boosting recurring commissions. Partners supply underwriting, product design and risk transfer, allowing Unicaja to scale offerings without underwriting exposure. Customers receive integrated protection and investment solutions through one distribution channel.

Corporate, SME, and public-sector ecosystems

Unicaja Banco, headquartered in Málaga and the largest regional bank in Andalusia, leverages local chambers, business associations, and municipalities to extend outreach across Andalusia (population ~8.4 million in 2024) and other regions. Collaboration supports SME financing programs and public projects, strengthening lending pipelines and guarantees while embedding the bank in regional economic development.

- regional-presence

- sme-finance

- public-projects

- lending-pipeline

- economic-development

Real estate and payment/fintech collaborators

In 2024 agreements with appraisers, servicers and real‑estate platforms underpin Unicaja Banco mortgage origination and collateral management, while fintech partners provide onboarding, KYC and alternative data to enhance credit models. Co‑innovation with payment and fintech collaborators improves UX, accelerates credit decisions and broadens distribution, lowering acquisition costs.

- Partnerships: appraisers, servicers, portals

- Fintech roles: onboarding, KYC, alternative data

- Benefits: faster decisions, improved UX, lower acquisition costs

Regulator-fintech-insurer ties secure liquidity, AI onboarding and €115bn assets

Partnerships with regulators, Visa/Mastercard and SEPA secure liquidity, compliance and 80%+ payments interoperability, supporting resilience. Tech and fintech vendors accelerate digital onboarding and AI servicing, leveraging pro‑forma €115bn assets and €91bn CET1-linked balance (2024) to cut time‑to‑market. Insurance, AM and servicers expand product reach across 6.2m customers, adding ~10% of non‑interest fees (2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Regulators | Liquidity/compliance | €115bn pro‑forma |

| Fintechs/vendors | Digital/KYC/AI | 6.2m customers |

| Insurers/AM | Distribution | ~10% fees |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Unicaja Banco covering customer segments, channels, value propositions, revenue streams, key resources, activities, partners, cost structure and customer relationships with integrated SWOT insights; designed to reflect real-world operations and support presentations, investor discussions and strategic decision-making.

High-level, editable Business Model Canvas for Unicaja Banco that condenses strategy into a one-page snapshot, saving hours of structuring while enabling quick comparisons, team collaboration, and boardroom-ready executive summaries to pinpoint and relieve strategic pain points.

Activities

Deposit gathering and lending

Unicaja Banco focuses on attracting retail and corporate deposits to drive balance-sheet growth, reporting deposits of €64.8bn and gross loans of €48.2bn as of June 2024. Lending covers mortgages, consumer, SME and corporate credit, with pricing and term structures aligned to market rates and the bank’s risk appetite. Active portfolio monitoring and early-warning controls preserve asset quality, supporting a stable non-performing exposure ratio in 2024.

Risk, compliance, and capital management

Credit, market, liquidity and operational risk frameworks steer lending, trading and treasury limits, with Unicaja Banco maintaining a CET1 ratio of 12.4% and an LCR comfortably above the 100% regulatory minimum in 2024.

Digital transformation and IT operations

Maintaining mobile, online and core platforms is continuous for Unicaja Banco, supporting over 3 million digital users post-merger; agile delivery ships features and boosts reliability with biweekly sprints; data analytics powers personalization and fraud prevention, analyzing millions of transactions monthly; cybersecurity defends customers and infrastructure with continuous monitoring and regulatory compliance (PSD2, GDPR) and annual IT investment growth in recent years.

Wealth, investment, and insurance distribution

Advisory distributes funds, managed portfolios and pension products through dedicated wealth teams, while bancassurance cross-sells protection for retail customers and SMEs to boost retention and coverage.

Suitability checks and ESG preferences are embedded in recommendations to align risk and sustainability; recurring advisory and fee-based revenues diversify income streams and reduce interest-rate sensitivity.

- Advisory: funds, portfolios, pensions

- Bancassurance: retail + SME protection

- Advice shaped by suitability & ESG

- Recurring fees diversify revenues

Treasury and balance-sheet optimization

Treasury and balance-sheet optimization at Unicaja Banco uses ALM to manage interest-rate risk, liquidity buffers and funding costs, supporting securities portfolios that generate income and provide collateral; hedging programs stabilise net interest income and capital, underpinning profitability and solvency while complying with regulatory LCR >100% in 2024.

- ALM: interest-rate risk, liquidity, funding

- Securities: income & collateral

- Hedging: stabilises NII & capital

- Outcome: supports profitability & solvency

€64.8bn deposits, €48.2bn loans; CET1 12.4%, 3m+ users

Unicaja Banco drives growth by attracting €64.8bn deposits and deploying €48.2bn gross loans (Jun 2024), while lending spans mortgages, consumer, SME and corporate credit with active portfolio monitoring. Risk frameworks keep CET1 at 12.4% and LCR above 100% in 2024. Digital and advisory channels serve 3m+ users, cross-selling bancassurance and fee-based products to diversify revenues.

| Metric | 2024 |

|---|---|

| Deposits | €64.8bn |

| Gross loans | €48.2bn |

| CET1 ratio | 12.4% |

| LCR | >100% |

| Digital users | 3m+ |

What You See Is What You Get

Business Model Canvas

The Unicaja Banco Business Model Canvas shown here is the actual deliverable, not a mockup; it’s a direct excerpt from the file you’ll receive after purchase. When you complete your order, you’ll get the same comprehensive document in editable Word and Excel formats. It’s fully structured and ready to present, edit, or share—no surprises, just the exact canvas you see now.