Unicharm Porter's Five Forces Analysis

Don't Miss the Bigger Picture

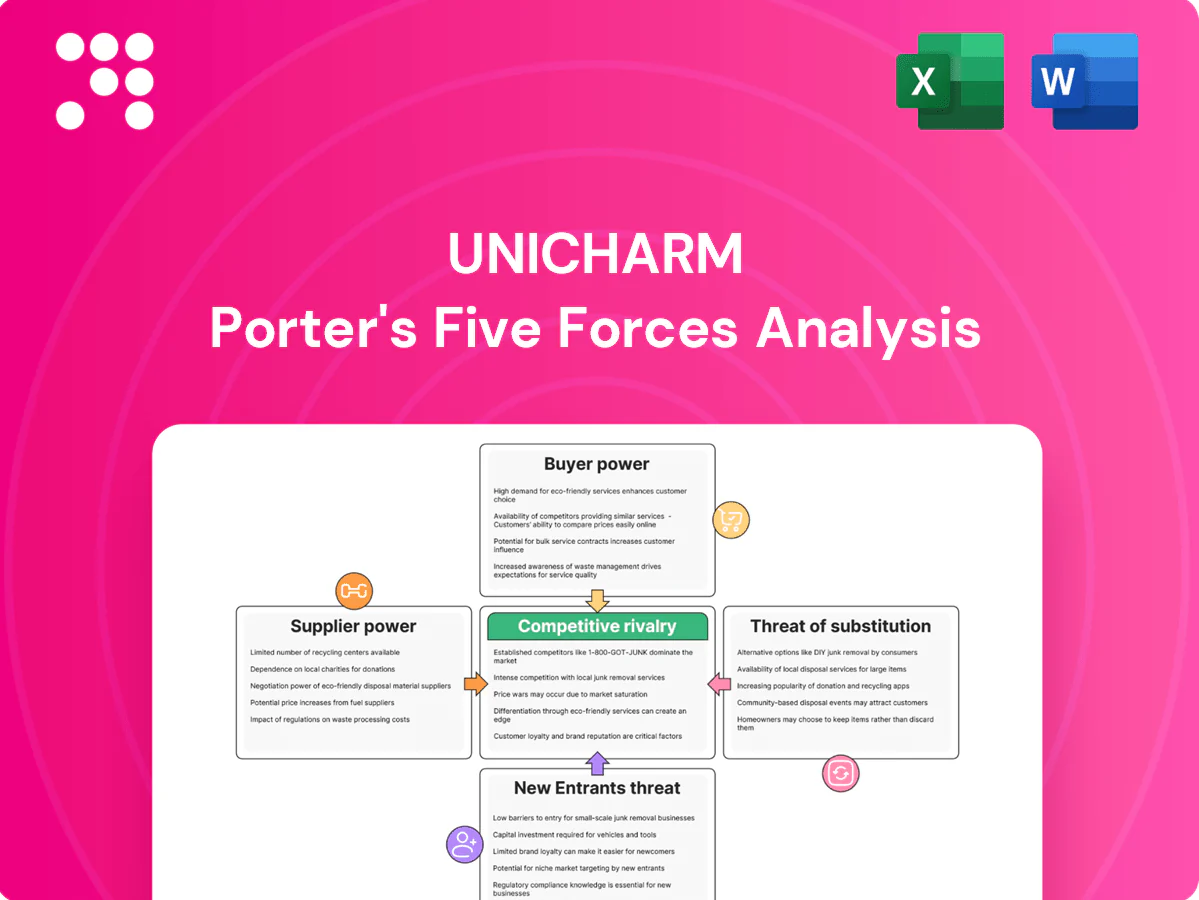

Unicharm’s Porter’s Five Forces snapshot highlights intense buyer power, moderate supplier influence, high rivalry, low threat of new entrants, and evolving substitute risks due to innovation in hygiene products. This brief overview teases strategic implications and competitive pressures. Unlock the full Porter's Five Forces Analysis to explore Unicharm’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs—fluff pulp, SAP, nonwovens, films and adhesives—are sourced from a concentrated group of global petrochemical and pulp players, with the global SAP market valued at about USD 5 billion in 2024 and dominated by roughly five major producers. Supplier consolidation in SAP and specialty nonwovens raises switching costs and limits alternatives, giving key suppliers price-setting influence. Unicharm mitigates this through multi-sourcing and scale purchasing, leveraging its large regional volumes to negotiate better terms.

Commodity price volatility

Commodity price volatility in 2024—notably pulp and petrochemical-linked inputs tied to global cycles and energy—pressured Unicharm’s margins as suppliers passed cost spikes through index-linked contracts. Suppliers can transmit increases quickly while Unicharm’s pricing adjustments lag, creating timing gaps. Hedging programs and formula-based pricing partially mitigate but do not eliminate exposure.

Quality and compliance requirements

Hygiene products require stringent absorbency, skin-safety and traceability standards enforced via certifications and audits such as ISO, OEKO-TEX and EcoVadis, which only a limited subset of global suppliers meet at scale. Qualification cycles commonly take 6–18 months, raising switching frictions and increasing supplier leverage. Unicharm’s supplier development programs aim to broaden the qualified base and mitigate concentration risks.

Logistics and regional exposure

Unicharm’s Asian footprint depends on steady regional logistics for bulky raw materials; FY2024 consolidated sales were ¥856.1bn, concentrating procurement needs in Asia and raising supplier leverage if shipping is disrupted.

Port congestion or capacity tightness shifts power to nearby suppliers with stock; localizing production cuts leverage but needs capex, while dual-sourcing across regions cushions shocks.

- Logistics risk: high — FY2024 sales ¥856.1bn

- Mitigation: localize (capex) + dual-sourcing

- Supplier leverage rises with regional capacity tightness

Sustainability and ESG pressures

Sustainability and ESG pressures shrink supplier choice as demand for FSC-certified pulp, recyclable packaging and lower-carbon resins rose sharply in 2024, with certified pulp trading at roughly a 5% price premium that boosted supplier pricing power.

Unicharm’s public 2024 sustainability commitments increase reliance on compliant vendors, while multi-year partnerships secure priority allocations and improved terms amid tightening supply.

- FSC pulp premium ~5% (2024)

- Higher ESG-driven supplier leverage

- Long-term contracts = priority allocations

- Unicharm 2024 targets raise vendor dependence

Concentrated SAP supply (USD 5bn) tightens pricing; scale buying mitigates

Core inputs concentrated (SAP market ~USD 5bn, ~5 major producers) raise supplier pricing power; Unicharm offsets via scale procurement. Commodity volatility and index-linked contracts compressed margins despite hedging. ESG-driven certified pulp trades ~+5% premium, tightening qualified supplier pool. Regional logistics exposure (FY2024 sales ¥856.1bn) increases supplier leverage.

| Metric | 2024 figure | Impact |

|---|---|---|

| SAP market | USD 5bn | Concentrated suppliers |

| Unicharm sales | ¥856.1bn | Regional procurement scale |

| FSC pulp premium | ~5% | Higher supplier pricing |

| Supplier qualification | 6–18 months | Switching friction |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Unicharm, evaluating supplier and buyer power, threat of substitutes and new entrants, and the intensity of rivalry to reveal strategic vulnerabilities and growth opportunities.

A clear, one-sheet summary of Unicharm's five forces—perfect for quick strategic decisions across hygiene and babycare markets, with customizable pressure levels to reflect supply chain shifts or regulatory changes.

Customers Bargaining Power

Modern retail and e-commerce leverage

Large retailers and marketplaces (global e-commerce ~22.3% of retail sales in 2024; Amazon ~38% of US online sales) command slotting, promotion and data fees, forcing Unicharm to cede margins for shelf space and visibility. Rising private label penetration accelerates price pressure, while Unicharm’s presence in 80+ countries lets it negotiate via joint business planning, exclusive SKUs and volume-linked promotions to rebalance power.

Low switching costs for consumers

Diapers, femcare and incontinence categories feature many comparable branded options, with high trialability and low switching costs—promo-led buying drives frequent brand switching and trial. Buyers thus wield power to demand value and faster innovation, pressuring margins. Brand equity and verified performance claims are crucial for retention; Unicharm held roughly 50% of Japan's baby diaper market and the global adult diaper market was about $17.6B in 2024.

Price sensitivity in emerging Asia

In emerging Asia, tight household budgets drive pronounced price sensitivity: a 2024 regional consumer survey found about 55% of households prioritize value over brand when buying FMCG, increasing propensity to downtrade to economy brands or smaller pack sizes and boosting buyer power. Unicharm must deploy tiered pricing and lean pack architecture to protect margins. Loyalty programs and subscription models can reduce short-term elasticity and stabilize volume.

Institutional and tender channels

Institutional buyers—nursing homes, clinics and government programs—purchase large volumes and negotiate aggressively; Japan’s 65+ population ~29% in 2024 underpins steady institutional demand. Specification-based tenders compress margins and lock prices, while strict compliance and service SLAs are essential to win. Multi-year contracts lower volatility but cap upside.

- High volume leverage

- Tenders compress margins

- Compliance/SLA critical

- Multi-year = stability, limited upside

Information transparency

Information transparency via online reviews, price-comparison sites and influencer content in 2024 substantially reduces asymmetry: consumers can benchmark Unicharm SKUs and promotions in minutes, amplifying pressure on price and quality across categories. Real-time review aggregation and comparison tools raise switching likelihood, while Unicharm's data-driven personalization and loyalty programs help defend share.

- ~minutes to benchmark: faster buyer decisions

- Price/quality pressure: higher switching risk

- Personalization: key defensive lever for Unicharm

Retail and e-commerce fees squeeze margins as promo-led switching meets institutional volume

Large retailers and e-commerce (~22.3% of retail sales in 2024; Amazon ~38% US online) extract fees and visibility, forcing margin concessions. High brand substitutability and promo-led buying (55% Asia value-first 2024) raise switching risk despite Unicharm’s 80+ country reach and ~50% Japan baby share. Institutional tenders (Japan 65+ = 29% 2024) compress prices but grant volume stability.

| Metric | 2024 |

|---|---|

| E‑commerce share | 22.3% |

| Amazon US online | 38% |

| Unicharm country reach | 80+ |

| Japan baby share | ~50% |

| Adult diaper market | $17.6B |

What You See Is What You Get

Unicharm Porter's Five Forces Analysis

This preview shows the exact Unicharm Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you complete payment. What you see here is precisely the deliverable you'll get, instantly available for your needs.

Don't Miss the Bigger Picture

Unicharm’s Porter’s Five Forces snapshot highlights intense buyer power, moderate supplier influence, high rivalry, low threat of new entrants, and evolving substitute risks due to innovation in hygiene products. This brief overview teases strategic implications and competitive pressures. Unlock the full Porter's Five Forces Analysis to explore Unicharm’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs—fluff pulp, SAP, nonwovens, films and adhesives—are sourced from a concentrated group of global petrochemical and pulp players, with the global SAP market valued at about USD 5 billion in 2024 and dominated by roughly five major producers. Supplier consolidation in SAP and specialty nonwovens raises switching costs and limits alternatives, giving key suppliers price-setting influence. Unicharm mitigates this through multi-sourcing and scale purchasing, leveraging its large regional volumes to negotiate better terms.

Commodity price volatility

Commodity price volatility in 2024—notably pulp and petrochemical-linked inputs tied to global cycles and energy—pressured Unicharm’s margins as suppliers passed cost spikes through index-linked contracts. Suppliers can transmit increases quickly while Unicharm’s pricing adjustments lag, creating timing gaps. Hedging programs and formula-based pricing partially mitigate but do not eliminate exposure.

Quality and compliance requirements

Hygiene products require stringent absorbency, skin-safety and traceability standards enforced via certifications and audits such as ISO, OEKO-TEX and EcoVadis, which only a limited subset of global suppliers meet at scale. Qualification cycles commonly take 6–18 months, raising switching frictions and increasing supplier leverage. Unicharm’s supplier development programs aim to broaden the qualified base and mitigate concentration risks.

Logistics and regional exposure

Unicharm’s Asian footprint depends on steady regional logistics for bulky raw materials; FY2024 consolidated sales were ¥856.1bn, concentrating procurement needs in Asia and raising supplier leverage if shipping is disrupted.

Port congestion or capacity tightness shifts power to nearby suppliers with stock; localizing production cuts leverage but needs capex, while dual-sourcing across regions cushions shocks.

- Logistics risk: high — FY2024 sales ¥856.1bn

- Mitigation: localize (capex) + dual-sourcing

- Supplier leverage rises with regional capacity tightness

Sustainability and ESG pressures

Sustainability and ESG pressures shrink supplier choice as demand for FSC-certified pulp, recyclable packaging and lower-carbon resins rose sharply in 2024, with certified pulp trading at roughly a 5% price premium that boosted supplier pricing power.

Unicharm’s public 2024 sustainability commitments increase reliance on compliant vendors, while multi-year partnerships secure priority allocations and improved terms amid tightening supply.

- FSC pulp premium ~5% (2024)

- Higher ESG-driven supplier leverage

- Long-term contracts = priority allocations

- Unicharm 2024 targets raise vendor dependence

Concentrated SAP supply (USD 5bn) tightens pricing; scale buying mitigates

Core inputs concentrated (SAP market ~USD 5bn, ~5 major producers) raise supplier pricing power; Unicharm offsets via scale procurement. Commodity volatility and index-linked contracts compressed margins despite hedging. ESG-driven certified pulp trades ~+5% premium, tightening qualified supplier pool. Regional logistics exposure (FY2024 sales ¥856.1bn) increases supplier leverage.

| Metric | 2024 figure | Impact |

|---|---|---|

| SAP market | USD 5bn | Concentrated suppliers |

| Unicharm sales | ¥856.1bn | Regional procurement scale |

| FSC pulp premium | ~5% | Higher supplier pricing |

| Supplier qualification | 6–18 months | Switching friction |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Unicharm, evaluating supplier and buyer power, threat of substitutes and new entrants, and the intensity of rivalry to reveal strategic vulnerabilities and growth opportunities.

A clear, one-sheet summary of Unicharm's five forces—perfect for quick strategic decisions across hygiene and babycare markets, with customizable pressure levels to reflect supply chain shifts or regulatory changes.

Customers Bargaining Power

Modern retail and e-commerce leverage

Large retailers and marketplaces (global e-commerce ~22.3% of retail sales in 2024; Amazon ~38% of US online sales) command slotting, promotion and data fees, forcing Unicharm to cede margins for shelf space and visibility. Rising private label penetration accelerates price pressure, while Unicharm’s presence in 80+ countries lets it negotiate via joint business planning, exclusive SKUs and volume-linked promotions to rebalance power.

Low switching costs for consumers

Diapers, femcare and incontinence categories feature many comparable branded options, with high trialability and low switching costs—promo-led buying drives frequent brand switching and trial. Buyers thus wield power to demand value and faster innovation, pressuring margins. Brand equity and verified performance claims are crucial for retention; Unicharm held roughly 50% of Japan's baby diaper market and the global adult diaper market was about $17.6B in 2024.

Price sensitivity in emerging Asia

In emerging Asia, tight household budgets drive pronounced price sensitivity: a 2024 regional consumer survey found about 55% of households prioritize value over brand when buying FMCG, increasing propensity to downtrade to economy brands or smaller pack sizes and boosting buyer power. Unicharm must deploy tiered pricing and lean pack architecture to protect margins. Loyalty programs and subscription models can reduce short-term elasticity and stabilize volume.

Institutional and tender channels

Institutional buyers—nursing homes, clinics and government programs—purchase large volumes and negotiate aggressively; Japan’s 65+ population ~29% in 2024 underpins steady institutional demand. Specification-based tenders compress margins and lock prices, while strict compliance and service SLAs are essential to win. Multi-year contracts lower volatility but cap upside.

- High volume leverage

- Tenders compress margins

- Compliance/SLA critical

- Multi-year = stability, limited upside

Information transparency

Information transparency via online reviews, price-comparison sites and influencer content in 2024 substantially reduces asymmetry: consumers can benchmark Unicharm SKUs and promotions in minutes, amplifying pressure on price and quality across categories. Real-time review aggregation and comparison tools raise switching likelihood, while Unicharm's data-driven personalization and loyalty programs help defend share.

- ~minutes to benchmark: faster buyer decisions

- Price/quality pressure: higher switching risk

- Personalization: key defensive lever for Unicharm

Retail and e-commerce fees squeeze margins as promo-led switching meets institutional volume

Large retailers and e-commerce (~22.3% of retail sales in 2024; Amazon ~38% US online) extract fees and visibility, forcing margin concessions. High brand substitutability and promo-led buying (55% Asia value-first 2024) raise switching risk despite Unicharm’s 80+ country reach and ~50% Japan baby share. Institutional tenders (Japan 65+ = 29% 2024) compress prices but grant volume stability.

| Metric | 2024 |

|---|---|

| E‑commerce share | 22.3% |

| Amazon US online | 38% |

| Unicharm country reach | 80+ |

| Japan baby share | ~50% |

| Adult diaper market | $17.6B |

What You See Is What You Get

Unicharm Porter's Five Forces Analysis

This preview shows the exact Unicharm Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you complete payment. What you see here is precisely the deliverable you'll get, instantly available for your needs.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Unicharm’s Porter’s Five Forces snapshot highlights intense buyer power, moderate supplier influence, high rivalry, low threat of new entrants, and evolving substitute risks due to innovation in hygiene products. This brief overview teases strategic implications and competitive pressures. Unlock the full Porter's Five Forces Analysis to explore Unicharm’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs—fluff pulp, SAP, nonwovens, films and adhesives—are sourced from a concentrated group of global petrochemical and pulp players, with the global SAP market valued at about USD 5 billion in 2024 and dominated by roughly five major producers. Supplier consolidation in SAP and specialty nonwovens raises switching costs and limits alternatives, giving key suppliers price-setting influence. Unicharm mitigates this through multi-sourcing and scale purchasing, leveraging its large regional volumes to negotiate better terms.

Commodity price volatility

Commodity price volatility in 2024—notably pulp and petrochemical-linked inputs tied to global cycles and energy—pressured Unicharm’s margins as suppliers passed cost spikes through index-linked contracts. Suppliers can transmit increases quickly while Unicharm’s pricing adjustments lag, creating timing gaps. Hedging programs and formula-based pricing partially mitigate but do not eliminate exposure.

Quality and compliance requirements

Hygiene products require stringent absorbency, skin-safety and traceability standards enforced via certifications and audits such as ISO, OEKO-TEX and EcoVadis, which only a limited subset of global suppliers meet at scale. Qualification cycles commonly take 6–18 months, raising switching frictions and increasing supplier leverage. Unicharm’s supplier development programs aim to broaden the qualified base and mitigate concentration risks.

Logistics and regional exposure

Unicharm’s Asian footprint depends on steady regional logistics for bulky raw materials; FY2024 consolidated sales were ¥856.1bn, concentrating procurement needs in Asia and raising supplier leverage if shipping is disrupted.

Port congestion or capacity tightness shifts power to nearby suppliers with stock; localizing production cuts leverage but needs capex, while dual-sourcing across regions cushions shocks.

- Logistics risk: high — FY2024 sales ¥856.1bn

- Mitigation: localize (capex) + dual-sourcing

- Supplier leverage rises with regional capacity tightness

Sustainability and ESG pressures

Sustainability and ESG pressures shrink supplier choice as demand for FSC-certified pulp, recyclable packaging and lower-carbon resins rose sharply in 2024, with certified pulp trading at roughly a 5% price premium that boosted supplier pricing power.

Unicharm’s public 2024 sustainability commitments increase reliance on compliant vendors, while multi-year partnerships secure priority allocations and improved terms amid tightening supply.

- FSC pulp premium ~5% (2024)

- Higher ESG-driven supplier leverage

- Long-term contracts = priority allocations

- Unicharm 2024 targets raise vendor dependence

Concentrated SAP supply (USD 5bn) tightens pricing; scale buying mitigates

Core inputs concentrated (SAP market ~USD 5bn, ~5 major producers) raise supplier pricing power; Unicharm offsets via scale procurement. Commodity volatility and index-linked contracts compressed margins despite hedging. ESG-driven certified pulp trades ~+5% premium, tightening qualified supplier pool. Regional logistics exposure (FY2024 sales ¥856.1bn) increases supplier leverage.

| Metric | 2024 figure | Impact |

|---|---|---|

| SAP market | USD 5bn | Concentrated suppliers |

| Unicharm sales | ¥856.1bn | Regional procurement scale |

| FSC pulp premium | ~5% | Higher supplier pricing |

| Supplier qualification | 6–18 months | Switching friction |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Unicharm, evaluating supplier and buyer power, threat of substitutes and new entrants, and the intensity of rivalry to reveal strategic vulnerabilities and growth opportunities.

A clear, one-sheet summary of Unicharm's five forces—perfect for quick strategic decisions across hygiene and babycare markets, with customizable pressure levels to reflect supply chain shifts or regulatory changes.

Customers Bargaining Power

Modern retail and e-commerce leverage

Large retailers and marketplaces (global e-commerce ~22.3% of retail sales in 2024; Amazon ~38% of US online sales) command slotting, promotion and data fees, forcing Unicharm to cede margins for shelf space and visibility. Rising private label penetration accelerates price pressure, while Unicharm’s presence in 80+ countries lets it negotiate via joint business planning, exclusive SKUs and volume-linked promotions to rebalance power.

Low switching costs for consumers

Diapers, femcare and incontinence categories feature many comparable branded options, with high trialability and low switching costs—promo-led buying drives frequent brand switching and trial. Buyers thus wield power to demand value and faster innovation, pressuring margins. Brand equity and verified performance claims are crucial for retention; Unicharm held roughly 50% of Japan's baby diaper market and the global adult diaper market was about $17.6B in 2024.

Price sensitivity in emerging Asia

In emerging Asia, tight household budgets drive pronounced price sensitivity: a 2024 regional consumer survey found about 55% of households prioritize value over brand when buying FMCG, increasing propensity to downtrade to economy brands or smaller pack sizes and boosting buyer power. Unicharm must deploy tiered pricing and lean pack architecture to protect margins. Loyalty programs and subscription models can reduce short-term elasticity and stabilize volume.

Institutional and tender channels

Institutional buyers—nursing homes, clinics and government programs—purchase large volumes and negotiate aggressively; Japan’s 65+ population ~29% in 2024 underpins steady institutional demand. Specification-based tenders compress margins and lock prices, while strict compliance and service SLAs are essential to win. Multi-year contracts lower volatility but cap upside.

- High volume leverage

- Tenders compress margins

- Compliance/SLA critical

- Multi-year = stability, limited upside

Information transparency

Information transparency via online reviews, price-comparison sites and influencer content in 2024 substantially reduces asymmetry: consumers can benchmark Unicharm SKUs and promotions in minutes, amplifying pressure on price and quality across categories. Real-time review aggregation and comparison tools raise switching likelihood, while Unicharm's data-driven personalization and loyalty programs help defend share.

- ~minutes to benchmark: faster buyer decisions

- Price/quality pressure: higher switching risk

- Personalization: key defensive lever for Unicharm

Retail and e-commerce fees squeeze margins as promo-led switching meets institutional volume

Large retailers and e-commerce (~22.3% of retail sales in 2024; Amazon ~38% US online) extract fees and visibility, forcing margin concessions. High brand substitutability and promo-led buying (55% Asia value-first 2024) raise switching risk despite Unicharm’s 80+ country reach and ~50% Japan baby share. Institutional tenders (Japan 65+ = 29% 2024) compress prices but grant volume stability.

| Metric | 2024 |

|---|---|

| E‑commerce share | 22.3% |

| Amazon US online | 38% |

| Unicharm country reach | 80+ |

| Japan baby share | ~50% |

| Adult diaper market | $17.6B |

What You See Is What You Get

Unicharm Porter's Five Forces Analysis

This preview shows the exact Unicharm Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you complete payment. What you see here is precisely the deliverable you'll get, instantly available for your needs.