UniCredit PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political, economic, social, technological, legal and environmental forces are shaping UniCredit’s strategy and risk profile in our concise PESTLE snapshot. Ideal for investors, consultants and executives, this analysis highlights hidden threats and growth levers you can act on today. Buy the full, editable PESTLE to get detailed evidence, scenarios and actionable recommendations—download instantly to sharpen your decisions.

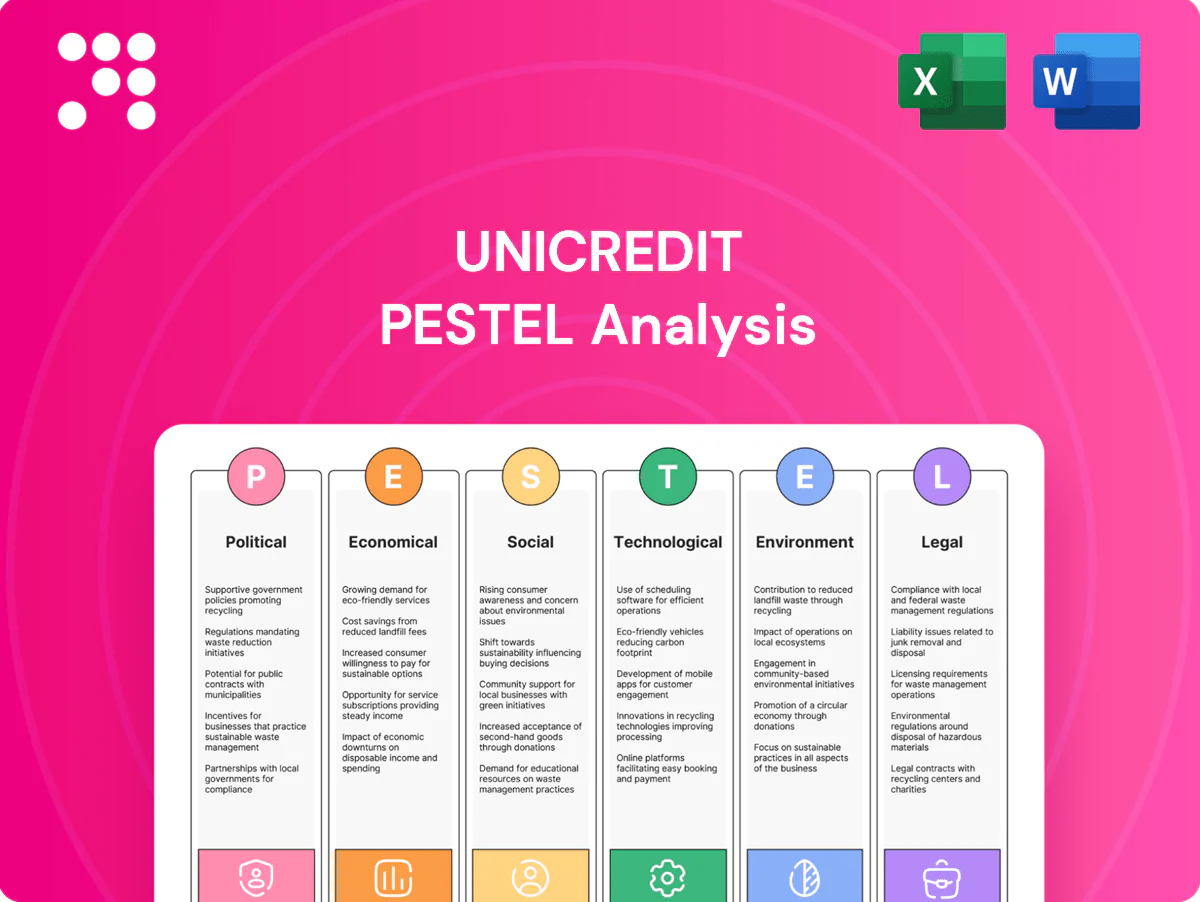

Political factors

EU policy and integration

EU policymaking shapes capital, competition and state-aid rules that govern UniCredit’s core markets; euro area GDP (~€12 trillion in 2024) and single-market passporting underpin cross-border franchise and revenues. Progress on banking-union measures (EDIS not yet fully mutualised, SRM enhancements under EU debate in 2024–25) could change risk-sharing and wholesale funding spreads. Policy fragmentation would raise compliance costs and limit synergies.

Geopolitical tensions in CEE

Operations across Central and Eastern Europe expose UniCredit to sanctions, trade disruptions and security risks following Russia’s full-scale invasion of Ukraine in Feb 2022; Russia supplied about 40% of EU gas pre-war and pipeline flows were largely halted by 2023. The conflict and energy shifts helped push euro-area HICP to a 10.6% peak in Oct 2022, squeezing growth, raising inflation and pressuring asset quality. Political volatility tightens credit conditions and remittance flows regionally; diversification reduces but does not eliminate correlated CEE shocks.

Government fiscal stance

Italy public debt remains elevated at about 140% of GDP (IMF 2024), and Italy–Germany 10y spreads have hovered near 160 bps in 2025, affecting UniCredit funding costs. Fiscal expansion in Germany and Austria in 2024–25 supports credit demand but can lift long-term risk premia. Austerity would damp growth yet may compress yields. The sovereign–bank nexus stays a key political sensitivity for balance-sheet resilience.

Regulatory agenda direction

Political priorities shape timelines for Basel finalisation, EU resolution reforms and the Capital Markets Union; the 2024 European Parliament elections in June 2024 and the 2024 European Commission work programme prioritising CMU create potential acceleration or delay. Leadership changes at EU institutions often shift rulemaking cadence, while national discretions increase operational uncertainty for UniCredit subsidiaries; predictable agendas aid capital allocation and strategic planning.

- June 2024: EP elections altered rulemaking pace

- Commission 2024: CMU prioritised

- National discretions: increased country-level variance

- Predictability: supports capital planning

Sanctions and foreign policy

Evolving EU/US sanctions regimes since 2022 have tightened correspondent banking, trade finance and corporate client access, increasing UniCredit’s screening and transaction-monitoring workloads; banks have paid over $26bn in sanctions/AML fines since 2008. Rapid policy shifts can strand exposures or force exits, while strong governance limits enforcement and reputational risk.

- Higher compliance costs: screening, due diligence, monitoring

- Operational risk: stranded exposures, forced exits

- Governance mitigates fines/reputational damage

EU rules, CMU, sanctions raise crossborder funding and compliance risks; Italy debt strains

EU rulemaking (EDIS not fully mutualised) and CMU progress shape cross-border franchise and capital rules, while sanctions and post‑2022 energy shocks raise compliance and credit risks. Italy’s public debt ≈140% of GDP (IMF 2024) and ITA‑GER 10y spread ≈160bps (2025) lift funding costs; banks have paid >$26bn in sanctions/AML fines since 2008.

| Metric | Value |

|---|---|

| Euro area GDP (2024) | ≈€12 tn |

| Italy public debt (2024) | ≈140% GDP |

| Italy‑Germany 10y spread (2025) | ≈160 bps |

| Sanctions/AML fines (since 2008) | >$26 bn |

| EDIS status (2024–25) | Not fully mutualised |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact UniCredit, combining data-backed trends and regional regulatory context to identify risks and opportunities, deliver forward-looking insights for executives, investors and strategy teams.

A concise, visually segmented UniCredit PESTLE summary that speeds up meeting prep and decision-making by highlighting key political, economic, social, technological, legal and environmental factors at a glance; editable and shareable for quick alignment across teams or client reports.

Economic factors

ECB rates and liquidity

Net interest income for UniCredit tracks the ECB policy path—ECB deposit rate stood at 4.00% in June 2024—so rate cuts compress margins but can boost loan volumes and lower funding costs. Balance sheet sensitivity, deposit betas and hedging strategies determine earnings impact. TLTRO expiries (roughly €1.0tn outstanding into 2024–25) and ECB quantitative tightening shrink excess liquidity, pressuring wholesale spreads and competition for deposits.

Growth in core markets

GDP trajectories—Italy ~+0.6% 2024, Germany ~+0.3% 2024 amid industrial softness, Austria ~+1.0% and CEE ~+3–4%—drive UniCredit loan demand and credit quality differences across markets. Services resilience outside Germany supports fee income and offsets weaker manufacturing lending. Divergent growth widens cross-market returns, forcing resource reallocation toward faster-growing CEE. A broad European footprint provides cyclical offset and diversification.

Inflation and wage dynamics

Moderating Eurozone inflation, around 2.3% y/y in May 2025, eases credit-loss and operating-cost pressures for UniCredit, while Italian nominal wages rising roughly 3.0% y/y in 2024 push expense lines and shape consumer borrowing capacity. Sticky services inflation near 3.5% may delay full ECB policy normalization, making pricing discipline and announced efficiency programs key levers to protect margins and capital ratios.

Credit cycle and NPLs

Tightening or easing credit standards feed through to defaults with a lag across retail and SME books; sectoral stress in real estate and energy‑intensive industries can elevate Stage 2 exposures. UniCredit reported a gross NPE ratio of 2.7% and coverage ~61% at end‑2024, and robust provisioning plus recovery platforms mitigate realised losses. Macroprudential measures may cap riskier growth.

- lagged defaults: retail/SME

- sector stress: real estate, energy

- gross NPE 2.7% (end‑2024)

- coverage ~61%: strong provisions

- macroprudential caps on risky growth

FX and cross-border flows

Exposure to non-euro CEE currencies drives translation and transaction risk for UniCredit, with CEE operations accounting for roughly 40% of 2024 pre-tax profit and thus magnifying FX impacts on reported earnings.

FX volatility in 2024 raised client hedging demand and influenced capital ratios and RWAs; UniCredit reported a c.20% increase in hedging volumes versus 2023, helping protect margins.

Balanced local-currency funding in core CEE markets has reduced currency mismatches, while shifts in trade and FDI — global FDI at about 1.2 trillion USD in 2024 per UNCTAD estimates — directly affect corporate and investment banking fee income.

- CEE share ~40% of 2024 pre-tax profit

- Hedging volumes +20% YoY (2024)

- Local-currency funding lowers mismatches

- Global FDI ~1.2tn USD (UNCTAD 2024)

EU rules, CMU, sanctions raise crossborder funding and compliance risks; Italy debt strains

UniCredit earnings remain tied to ECB policy (deposit rate 4.00% June 2024) and TLTRO runoff (~€1.0tn) while Eurozone inflation ~2.3% (May 2025) and Italy wage growth (~3.0% 2024) shape margins and credit demand. Credit quality shows gross NPE 2.7% (end‑2024) with 61% coverage; CEE contributes ~40% of 2024 pre‑tax profit, amplifying FX and growth exposure.

| Metric | Value |

|---|---|

| ECB deposit rate | 4.00% (Jun 2024) |

| Eurozone inflation | 2.3% (May 2025) |

| Gross NPE | 2.7% (end‑2024) |

| Coverage | ~61% (end‑2024) |

| CEE pre‑tax profit share | ~40% (2024) |

| TLTRO outstanding | ~€1.0tn (2024–25) |

| Hedging volumes | +20% YoY (2024) |

Preview Before You Purchase

UniCredit PESTLE Analysis

The preview shown here is the exact UniCredit PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real, finished file with complete content and structure, not a placeholder or teaser. After checkout you’ll be able to download this same professionally structured report immediately.

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political, economic, social, technological, legal and environmental forces are shaping UniCredit’s strategy and risk profile in our concise PESTLE snapshot. Ideal for investors, consultants and executives, this analysis highlights hidden threats and growth levers you can act on today. Buy the full, editable PESTLE to get detailed evidence, scenarios and actionable recommendations—download instantly to sharpen your decisions.

Political factors

EU policy and integration

EU policymaking shapes capital, competition and state-aid rules that govern UniCredit’s core markets; euro area GDP (~€12 trillion in 2024) and single-market passporting underpin cross-border franchise and revenues. Progress on banking-union measures (EDIS not yet fully mutualised, SRM enhancements under EU debate in 2024–25) could change risk-sharing and wholesale funding spreads. Policy fragmentation would raise compliance costs and limit synergies.

Geopolitical tensions in CEE

Operations across Central and Eastern Europe expose UniCredit to sanctions, trade disruptions and security risks following Russia’s full-scale invasion of Ukraine in Feb 2022; Russia supplied about 40% of EU gas pre-war and pipeline flows were largely halted by 2023. The conflict and energy shifts helped push euro-area HICP to a 10.6% peak in Oct 2022, squeezing growth, raising inflation and pressuring asset quality. Political volatility tightens credit conditions and remittance flows regionally; diversification reduces but does not eliminate correlated CEE shocks.

Government fiscal stance

Italy public debt remains elevated at about 140% of GDP (IMF 2024), and Italy–Germany 10y spreads have hovered near 160 bps in 2025, affecting UniCredit funding costs. Fiscal expansion in Germany and Austria in 2024–25 supports credit demand but can lift long-term risk premia. Austerity would damp growth yet may compress yields. The sovereign–bank nexus stays a key political sensitivity for balance-sheet resilience.

Regulatory agenda direction

Political priorities shape timelines for Basel finalisation, EU resolution reforms and the Capital Markets Union; the 2024 European Parliament elections in June 2024 and the 2024 European Commission work programme prioritising CMU create potential acceleration or delay. Leadership changes at EU institutions often shift rulemaking cadence, while national discretions increase operational uncertainty for UniCredit subsidiaries; predictable agendas aid capital allocation and strategic planning.

- June 2024: EP elections altered rulemaking pace

- Commission 2024: CMU prioritised

- National discretions: increased country-level variance

- Predictability: supports capital planning

Sanctions and foreign policy

Evolving EU/US sanctions regimes since 2022 have tightened correspondent banking, trade finance and corporate client access, increasing UniCredit’s screening and transaction-monitoring workloads; banks have paid over $26bn in sanctions/AML fines since 2008. Rapid policy shifts can strand exposures or force exits, while strong governance limits enforcement and reputational risk.

- Higher compliance costs: screening, due diligence, monitoring

- Operational risk: stranded exposures, forced exits

- Governance mitigates fines/reputational damage

EU rules, CMU, sanctions raise crossborder funding and compliance risks; Italy debt strains

EU rulemaking (EDIS not fully mutualised) and CMU progress shape cross-border franchise and capital rules, while sanctions and post‑2022 energy shocks raise compliance and credit risks. Italy’s public debt ≈140% of GDP (IMF 2024) and ITA‑GER 10y spread ≈160bps (2025) lift funding costs; banks have paid >$26bn in sanctions/AML fines since 2008.

| Metric | Value |

|---|---|

| Euro area GDP (2024) | ≈€12 tn |

| Italy public debt (2024) | ≈140% GDP |

| Italy‑Germany 10y spread (2025) | ≈160 bps |

| Sanctions/AML fines (since 2008) | >$26 bn |

| EDIS status (2024–25) | Not fully mutualised |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact UniCredit, combining data-backed trends and regional regulatory context to identify risks and opportunities, deliver forward-looking insights for executives, investors and strategy teams.

A concise, visually segmented UniCredit PESTLE summary that speeds up meeting prep and decision-making by highlighting key political, economic, social, technological, legal and environmental factors at a glance; editable and shareable for quick alignment across teams or client reports.

Economic factors

ECB rates and liquidity

Net interest income for UniCredit tracks the ECB policy path—ECB deposit rate stood at 4.00% in June 2024—so rate cuts compress margins but can boost loan volumes and lower funding costs. Balance sheet sensitivity, deposit betas and hedging strategies determine earnings impact. TLTRO expiries (roughly €1.0tn outstanding into 2024–25) and ECB quantitative tightening shrink excess liquidity, pressuring wholesale spreads and competition for deposits.

Growth in core markets

GDP trajectories—Italy ~+0.6% 2024, Germany ~+0.3% 2024 amid industrial softness, Austria ~+1.0% and CEE ~+3–4%—drive UniCredit loan demand and credit quality differences across markets. Services resilience outside Germany supports fee income and offsets weaker manufacturing lending. Divergent growth widens cross-market returns, forcing resource reallocation toward faster-growing CEE. A broad European footprint provides cyclical offset and diversification.

Inflation and wage dynamics

Moderating Eurozone inflation, around 2.3% y/y in May 2025, eases credit-loss and operating-cost pressures for UniCredit, while Italian nominal wages rising roughly 3.0% y/y in 2024 push expense lines and shape consumer borrowing capacity. Sticky services inflation near 3.5% may delay full ECB policy normalization, making pricing discipline and announced efficiency programs key levers to protect margins and capital ratios.

Credit cycle and NPLs

Tightening or easing credit standards feed through to defaults with a lag across retail and SME books; sectoral stress in real estate and energy‑intensive industries can elevate Stage 2 exposures. UniCredit reported a gross NPE ratio of 2.7% and coverage ~61% at end‑2024, and robust provisioning plus recovery platforms mitigate realised losses. Macroprudential measures may cap riskier growth.

- lagged defaults: retail/SME

- sector stress: real estate, energy

- gross NPE 2.7% (end‑2024)

- coverage ~61%: strong provisions

- macroprudential caps on risky growth

FX and cross-border flows

Exposure to non-euro CEE currencies drives translation and transaction risk for UniCredit, with CEE operations accounting for roughly 40% of 2024 pre-tax profit and thus magnifying FX impacts on reported earnings.

FX volatility in 2024 raised client hedging demand and influenced capital ratios and RWAs; UniCredit reported a c.20% increase in hedging volumes versus 2023, helping protect margins.

Balanced local-currency funding in core CEE markets has reduced currency mismatches, while shifts in trade and FDI — global FDI at about 1.2 trillion USD in 2024 per UNCTAD estimates — directly affect corporate and investment banking fee income.

- CEE share ~40% of 2024 pre-tax profit

- Hedging volumes +20% YoY (2024)

- Local-currency funding lowers mismatches

- Global FDI ~1.2tn USD (UNCTAD 2024)

EU rules, CMU, sanctions raise crossborder funding and compliance risks; Italy debt strains

UniCredit earnings remain tied to ECB policy (deposit rate 4.00% June 2024) and TLTRO runoff (~€1.0tn) while Eurozone inflation ~2.3% (May 2025) and Italy wage growth (~3.0% 2024) shape margins and credit demand. Credit quality shows gross NPE 2.7% (end‑2024) with 61% coverage; CEE contributes ~40% of 2024 pre‑tax profit, amplifying FX and growth exposure.

| Metric | Value |

|---|---|

| ECB deposit rate | 4.00% (Jun 2024) |

| Eurozone inflation | 2.3% (May 2025) |

| Gross NPE | 2.7% (end‑2024) |

| Coverage | ~61% (end‑2024) |

| CEE pre‑tax profit share | ~40% (2024) |

| TLTRO outstanding | ~€1.0tn (2024–25) |

| Hedging volumes | +20% YoY (2024) |

Preview Before You Purchase

UniCredit PESTLE Analysis

The preview shown here is the exact UniCredit PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real, finished file with complete content and structure, not a placeholder or teaser. After checkout you’ll be able to download this same professionally structured report immediately.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political, economic, social, technological, legal and environmental forces are shaping UniCredit’s strategy and risk profile in our concise PESTLE snapshot. Ideal for investors, consultants and executives, this analysis highlights hidden threats and growth levers you can act on today. Buy the full, editable PESTLE to get detailed evidence, scenarios and actionable recommendations—download instantly to sharpen your decisions.

Political factors

EU policy and integration

EU policymaking shapes capital, competition and state-aid rules that govern UniCredit’s core markets; euro area GDP (~€12 trillion in 2024) and single-market passporting underpin cross-border franchise and revenues. Progress on banking-union measures (EDIS not yet fully mutualised, SRM enhancements under EU debate in 2024–25) could change risk-sharing and wholesale funding spreads. Policy fragmentation would raise compliance costs and limit synergies.

Geopolitical tensions in CEE

Operations across Central and Eastern Europe expose UniCredit to sanctions, trade disruptions and security risks following Russia’s full-scale invasion of Ukraine in Feb 2022; Russia supplied about 40% of EU gas pre-war and pipeline flows were largely halted by 2023. The conflict and energy shifts helped push euro-area HICP to a 10.6% peak in Oct 2022, squeezing growth, raising inflation and pressuring asset quality. Political volatility tightens credit conditions and remittance flows regionally; diversification reduces but does not eliminate correlated CEE shocks.

Government fiscal stance

Italy public debt remains elevated at about 140% of GDP (IMF 2024), and Italy–Germany 10y spreads have hovered near 160 bps in 2025, affecting UniCredit funding costs. Fiscal expansion in Germany and Austria in 2024–25 supports credit demand but can lift long-term risk premia. Austerity would damp growth yet may compress yields. The sovereign–bank nexus stays a key political sensitivity for balance-sheet resilience.

Regulatory agenda direction

Political priorities shape timelines for Basel finalisation, EU resolution reforms and the Capital Markets Union; the 2024 European Parliament elections in June 2024 and the 2024 European Commission work programme prioritising CMU create potential acceleration or delay. Leadership changes at EU institutions often shift rulemaking cadence, while national discretions increase operational uncertainty for UniCredit subsidiaries; predictable agendas aid capital allocation and strategic planning.

- June 2024: EP elections altered rulemaking pace

- Commission 2024: CMU prioritised

- National discretions: increased country-level variance

- Predictability: supports capital planning

Sanctions and foreign policy

Evolving EU/US sanctions regimes since 2022 have tightened correspondent banking, trade finance and corporate client access, increasing UniCredit’s screening and transaction-monitoring workloads; banks have paid over $26bn in sanctions/AML fines since 2008. Rapid policy shifts can strand exposures or force exits, while strong governance limits enforcement and reputational risk.

- Higher compliance costs: screening, due diligence, monitoring

- Operational risk: stranded exposures, forced exits

- Governance mitigates fines/reputational damage

EU rules, CMU, sanctions raise crossborder funding and compliance risks; Italy debt strains

EU rulemaking (EDIS not fully mutualised) and CMU progress shape cross-border franchise and capital rules, while sanctions and post‑2022 energy shocks raise compliance and credit risks. Italy’s public debt ≈140% of GDP (IMF 2024) and ITA‑GER 10y spread ≈160bps (2025) lift funding costs; banks have paid >$26bn in sanctions/AML fines since 2008.

| Metric | Value |

|---|---|

| Euro area GDP (2024) | ≈€12 tn |

| Italy public debt (2024) | ≈140% GDP |

| Italy‑Germany 10y spread (2025) | ≈160 bps |

| Sanctions/AML fines (since 2008) | >$26 bn |

| EDIS status (2024–25) | Not fully mutualised |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact UniCredit, combining data-backed trends and regional regulatory context to identify risks and opportunities, deliver forward-looking insights for executives, investors and strategy teams.

A concise, visually segmented UniCredit PESTLE summary that speeds up meeting prep and decision-making by highlighting key political, economic, social, technological, legal and environmental factors at a glance; editable and shareable for quick alignment across teams or client reports.

Economic factors

ECB rates and liquidity

Net interest income for UniCredit tracks the ECB policy path—ECB deposit rate stood at 4.00% in June 2024—so rate cuts compress margins but can boost loan volumes and lower funding costs. Balance sheet sensitivity, deposit betas and hedging strategies determine earnings impact. TLTRO expiries (roughly €1.0tn outstanding into 2024–25) and ECB quantitative tightening shrink excess liquidity, pressuring wholesale spreads and competition for deposits.

Growth in core markets

GDP trajectories—Italy ~+0.6% 2024, Germany ~+0.3% 2024 amid industrial softness, Austria ~+1.0% and CEE ~+3–4%—drive UniCredit loan demand and credit quality differences across markets. Services resilience outside Germany supports fee income and offsets weaker manufacturing lending. Divergent growth widens cross-market returns, forcing resource reallocation toward faster-growing CEE. A broad European footprint provides cyclical offset and diversification.

Inflation and wage dynamics

Moderating Eurozone inflation, around 2.3% y/y in May 2025, eases credit-loss and operating-cost pressures for UniCredit, while Italian nominal wages rising roughly 3.0% y/y in 2024 push expense lines and shape consumer borrowing capacity. Sticky services inflation near 3.5% may delay full ECB policy normalization, making pricing discipline and announced efficiency programs key levers to protect margins and capital ratios.

Credit cycle and NPLs

Tightening or easing credit standards feed through to defaults with a lag across retail and SME books; sectoral stress in real estate and energy‑intensive industries can elevate Stage 2 exposures. UniCredit reported a gross NPE ratio of 2.7% and coverage ~61% at end‑2024, and robust provisioning plus recovery platforms mitigate realised losses. Macroprudential measures may cap riskier growth.

- lagged defaults: retail/SME

- sector stress: real estate, energy

- gross NPE 2.7% (end‑2024)

- coverage ~61%: strong provisions

- macroprudential caps on risky growth

FX and cross-border flows

Exposure to non-euro CEE currencies drives translation and transaction risk for UniCredit, with CEE operations accounting for roughly 40% of 2024 pre-tax profit and thus magnifying FX impacts on reported earnings.

FX volatility in 2024 raised client hedging demand and influenced capital ratios and RWAs; UniCredit reported a c.20% increase in hedging volumes versus 2023, helping protect margins.

Balanced local-currency funding in core CEE markets has reduced currency mismatches, while shifts in trade and FDI — global FDI at about 1.2 trillion USD in 2024 per UNCTAD estimates — directly affect corporate and investment banking fee income.

- CEE share ~40% of 2024 pre-tax profit

- Hedging volumes +20% YoY (2024)

- Local-currency funding lowers mismatches

- Global FDI ~1.2tn USD (UNCTAD 2024)

EU rules, CMU, sanctions raise crossborder funding and compliance risks; Italy debt strains

UniCredit earnings remain tied to ECB policy (deposit rate 4.00% June 2024) and TLTRO runoff (~€1.0tn) while Eurozone inflation ~2.3% (May 2025) and Italy wage growth (~3.0% 2024) shape margins and credit demand. Credit quality shows gross NPE 2.7% (end‑2024) with 61% coverage; CEE contributes ~40% of 2024 pre‑tax profit, amplifying FX and growth exposure.

| Metric | Value |

|---|---|

| ECB deposit rate | 4.00% (Jun 2024) |

| Eurozone inflation | 2.3% (May 2025) |

| Gross NPE | 2.7% (end‑2024) |

| Coverage | ~61% (end‑2024) |

| CEE pre‑tax profit share | ~40% (2024) |

| TLTRO outstanding | ~€1.0tn (2024–25) |

| Hedging volumes | +20% YoY (2024) |

Preview Before You Purchase

UniCredit PESTLE Analysis

The preview shown here is the exact UniCredit PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This is the real, finished file with complete content and structure, not a placeholder or teaser. After checkout you’ll be able to download this same professionally structured report immediately.