Unilever Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Unilever faces intense competitive rivalry across personal care and FMCG, with scale and strong brands partly insulating margins. Buyer power is significant in retail channel negotiations, though consumer loyalty limits price elasticity. Supplier power is moderate and threats from substitutes and new entrants are manageable but persistent. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Unilever’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse raw materials

Unilever sources agricultural oils, fragrances, chemicals and packaging across global markets—operating in over 190 countries—which dilutes any single supplier’s leverage and spreads risk.

Many inputs are commodity-like, making benchmarking transparent and keeping switching costs moderate.

However, traceability and strict quality requirements in categories like palm oil and fragrances create supplier stickiness.

Scale purchasing leverage

Unilever's massive scale—serving ~2.5 billion consumers daily and generating ~€61bn revenue in 2023—lets procurement extract volume discounts, multi-year contracts and hedging, lowering supplier price pass-through and volatility. Preferred-supplier programs and dual sourcing further curb dependence. Suppliers routinely compete for access to Unilever volumes, intensifying buyer leverage.

Specialty ingredients

Certain actives, enzymes and fragrances are supplied by a handful of specialist houses; in 2024 the top five fragrance firms still control roughly 80% of the global market, creating niche supplier leverage. Reformulation to switch vendors often takes 6–12 months and incurs significant testing and validation costs, raising switching friction. Patented actives and tight technical specs further entrench suppliers, so these pockets amplify supplier influence despite Unilever’s overall scale.

Sustainability constraints

Sustainability constraints — driven by Unilever’s 2024 commitments to 100% reusable/recyclable/compostable packaging by 2025 and net‑zero value chain emissions by 2039 — narrow the approved supplier base for palm oil, plastics and energy inputs.

Certified suppliers command premiums, reduce substitution options, and face higher qualification costs from audits and traceability; ethical sourcing thus strengthens select supplier bargaining power.

- Approved supplier pool tightened (traceability/audits)

- Certified inputs command price premiums

- Higher supplier qualification costs

- Ethical sourcing increases supplier leverage

Geopolitics and logistics

Geopolitics, trade restrictions, weather shocks and freight bottlenecks periodically tighten supply and push up input costs, giving suppliers short-term leverage when capacity is constrained; Unilever cites regional sourcing and larger inventory buffers to reduce exposure.

- Trade restrictions raise lead times

- Weather shocks tighten capacity

- Freight bottlenecks lift supplier power

- Regionalization + inventory buffers mitigate risk

Global consumer scale and buyer leverage vs concentrated fragrance firms and sustainability limits

Unilever’s global scale (≈2.5bn consumers/day; €61bn revenue in 2023) and procurement programs drive strong buyer leverage, but certified/traceable suppliers and specialist fragrance/active houses retain pockets of power. In 2024 the top five fragrance firms control ~80% of the market, and sustainability requirements (100% reusable/recyclable/compostable packaging by 2025; net‑zero by 2039) narrow approved suppliers. Geopolitical, weather and freight shocks create episodic supplier leverage despite dual sourcing and inventory buffers.

| Metric | Value | Effect on Supplier Power |

|---|---|---|

| Consumers reached | ≈2.5bn/day | Increases buyer leverage |

| Revenue (2023) | ≈€61bn | Volume discounts |

| Fragrance top5 (2024) | ≈80% market share | Raises niche supplier power |

| Packaging target | 100% by 2025 | Tightens approved suppliers |

What is included in the product

Comprehensive Porter’s Five Forces analysis of Unilever revealing competitive intensity, buyer and supplier power, substitute threats, and entry barriers, highlighting disruptive risks and strategic levers to protect market share.

A single-sheet Unilever Porter's Five Forces snapshot that distills competitive pressures into actionable insights—ideal for fast strategic decisions and boardroom slides.

Customers Bargaining Power

Retail giants’ clout

Global retailers and wholesalers like Walmart (US$611.3bn revenue FY2024) exert strong leverage to negotiate price, payment terms and shelf space, concentrating bargaining power through consolidation. Trade spend and slotting fees squeeze supplier margins, often shifting promotional costs onto manufacturers. Unilever offsets this pressure with entrenched category leadership and high-demand brands that secure shelf presence and promotional support.

Private label pressure

Store-brand penetration in Europe is roughly 40% of grocery sales, and private labels increasingly offer cheaper substitutes in home and personal care, compressing Unilever's premium gaps. This heightens price sensitivity among consumers and erodes margins as trading-down rises, especially during recessionary cycles when private-label sales spike. Unilever's defense depends on sustained brand equity and accelerated innovation to protect share and pricing. Recent retailer assortments show growing shelf space for private labels, intensifying competitive pressure.

Consumer switching ease

Low switching costs and abundant options empower consumers; global FMCG e-commerce penetration reached about 14% in 2023, increasing price and product comparison. Promotions, reviews and social proof (roughly 89% of shoppers consult reviews) accelerate churn between brands. Loyalty programs and differentiated benefits are used to reduce churn and raise retention.

Omnichannel dynamics

Omnichannel dynamics boost customer bargaining power as marketplaces and quick-commerce shorten lead times and widen choice; platforms like Amazon reported 2023 net sales of 513.98 billion USD, increasing buyer options and price transparency. Digital-native shoppers demand personalization and perceived value, pressuring margins and promotions. Unilever’s D2C and analytics investments improve consumer insight and partly counter retailer leverage, while shifts in channel mix alter negotiation leverage across categories.

- Marketplaces widen choice, compress lead times

- Digital buyers expect personalization/value

- D2C + analytics = more consumer insight

- Channel mix shifts reshape retailer bargaining

Regulatory and ESG expectations

Buyers increasingly demand sustainable packaging, clean labels and ethical sourcing, and non-compliance can trigger retailer delistings or penalties that weaken suppliers' negotiating positions. Meeting these standards raises costs but secures shelf space and consumer trust; Unilever has pledged 100% recyclable/reusable/compostable packaging and to halve virgin plastic use by 2025, strengthening its bargaining leverage with buyers.

- Buyers: demand sustainable packaging, clean labels, ethical sourcing

- Risk: retailer delistings/penalties reduce supplier leverage

- Cost: compliance raises COGS but protects shelf presence

- Fact: Unilever target—100% recyclable/reusable/compostable packaging; halve virgin plastic by 2025

Retail power, 14% FMCG e-comm, 89% review influence

Global retailers (Walmart revenue US$611.3bn FY2024) and e‑marketplaces (Amazon sales US$513.98bn 2023) exert strong pricing and shelf leverage, while 14% FMCG e‑commerce penetration and 89% review consults raise consumer bargaining power. Private labels (~40% EU grocery) compress premiums; sustainability mandates (Unilever 2025 packaging targets) shift costs but protect access.

| Metric | Value |

|---|---|

| Walmart rev | US$611.3bn FY2024 |

| Amazon sales | US$513.98bn 2023 |

| FMCG e‑comm | 14% 2023 |

| EU private label | ~40% |

What You See Is What You Get

Unilever Porter's Five Forces Analysis

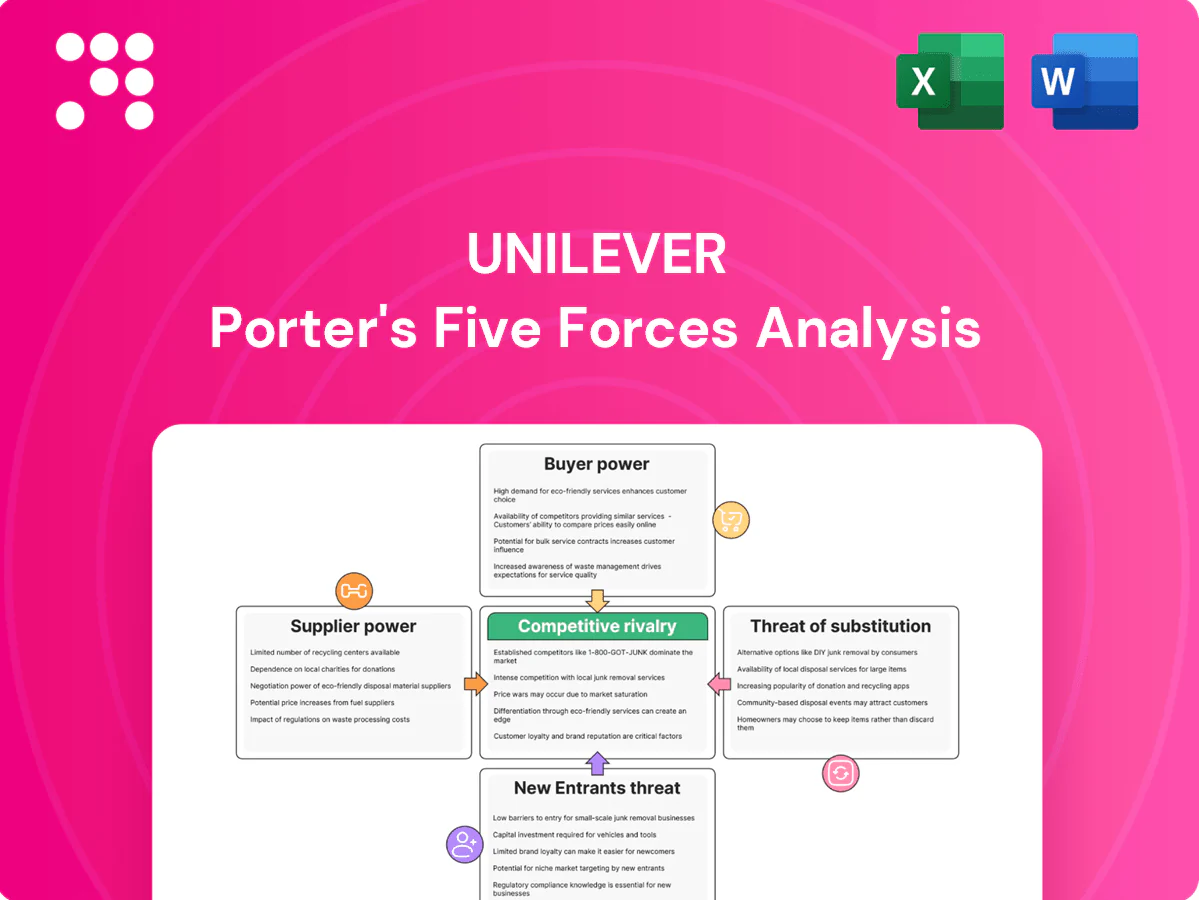

This preview shows the exact Unilever Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. It provides a concise assessment of competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes tailored to Unilever's consumer goods context. The file is fully formatted and ready for immediate download and use.

Go Beyond the Preview—Access the Full Strategic Report

Unilever faces intense competitive rivalry across personal care and FMCG, with scale and strong brands partly insulating margins. Buyer power is significant in retail channel negotiations, though consumer loyalty limits price elasticity. Supplier power is moderate and threats from substitutes and new entrants are manageable but persistent. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Unilever’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse raw materials

Unilever sources agricultural oils, fragrances, chemicals and packaging across global markets—operating in over 190 countries—which dilutes any single supplier’s leverage and spreads risk.

Many inputs are commodity-like, making benchmarking transparent and keeping switching costs moderate.

However, traceability and strict quality requirements in categories like palm oil and fragrances create supplier stickiness.

Scale purchasing leverage

Unilever's massive scale—serving ~2.5 billion consumers daily and generating ~€61bn revenue in 2023—lets procurement extract volume discounts, multi-year contracts and hedging, lowering supplier price pass-through and volatility. Preferred-supplier programs and dual sourcing further curb dependence. Suppliers routinely compete for access to Unilever volumes, intensifying buyer leverage.

Specialty ingredients

Certain actives, enzymes and fragrances are supplied by a handful of specialist houses; in 2024 the top five fragrance firms still control roughly 80% of the global market, creating niche supplier leverage. Reformulation to switch vendors often takes 6–12 months and incurs significant testing and validation costs, raising switching friction. Patented actives and tight technical specs further entrench suppliers, so these pockets amplify supplier influence despite Unilever’s overall scale.

Sustainability constraints

Sustainability constraints — driven by Unilever’s 2024 commitments to 100% reusable/recyclable/compostable packaging by 2025 and net‑zero value chain emissions by 2039 — narrow the approved supplier base for palm oil, plastics and energy inputs.

Certified suppliers command premiums, reduce substitution options, and face higher qualification costs from audits and traceability; ethical sourcing thus strengthens select supplier bargaining power.

- Approved supplier pool tightened (traceability/audits)

- Certified inputs command price premiums

- Higher supplier qualification costs

- Ethical sourcing increases supplier leverage

Geopolitics and logistics

Geopolitics, trade restrictions, weather shocks and freight bottlenecks periodically tighten supply and push up input costs, giving suppliers short-term leverage when capacity is constrained; Unilever cites regional sourcing and larger inventory buffers to reduce exposure.

- Trade restrictions raise lead times

- Weather shocks tighten capacity

- Freight bottlenecks lift supplier power

- Regionalization + inventory buffers mitigate risk

Global consumer scale and buyer leverage vs concentrated fragrance firms and sustainability limits

Unilever’s global scale (≈2.5bn consumers/day; €61bn revenue in 2023) and procurement programs drive strong buyer leverage, but certified/traceable suppliers and specialist fragrance/active houses retain pockets of power. In 2024 the top five fragrance firms control ~80% of the market, and sustainability requirements (100% reusable/recyclable/compostable packaging by 2025; net‑zero by 2039) narrow approved suppliers. Geopolitical, weather and freight shocks create episodic supplier leverage despite dual sourcing and inventory buffers.

| Metric | Value | Effect on Supplier Power |

|---|---|---|

| Consumers reached | ≈2.5bn/day | Increases buyer leverage |

| Revenue (2023) | ≈€61bn | Volume discounts |

| Fragrance top5 (2024) | ≈80% market share | Raises niche supplier power |

| Packaging target | 100% by 2025 | Tightens approved suppliers |

What is included in the product

Comprehensive Porter’s Five Forces analysis of Unilever revealing competitive intensity, buyer and supplier power, substitute threats, and entry barriers, highlighting disruptive risks and strategic levers to protect market share.

A single-sheet Unilever Porter's Five Forces snapshot that distills competitive pressures into actionable insights—ideal for fast strategic decisions and boardroom slides.

Customers Bargaining Power

Retail giants’ clout

Global retailers and wholesalers like Walmart (US$611.3bn revenue FY2024) exert strong leverage to negotiate price, payment terms and shelf space, concentrating bargaining power through consolidation. Trade spend and slotting fees squeeze supplier margins, often shifting promotional costs onto manufacturers. Unilever offsets this pressure with entrenched category leadership and high-demand brands that secure shelf presence and promotional support.

Private label pressure

Store-brand penetration in Europe is roughly 40% of grocery sales, and private labels increasingly offer cheaper substitutes in home and personal care, compressing Unilever's premium gaps. This heightens price sensitivity among consumers and erodes margins as trading-down rises, especially during recessionary cycles when private-label sales spike. Unilever's defense depends on sustained brand equity and accelerated innovation to protect share and pricing. Recent retailer assortments show growing shelf space for private labels, intensifying competitive pressure.

Consumer switching ease

Low switching costs and abundant options empower consumers; global FMCG e-commerce penetration reached about 14% in 2023, increasing price and product comparison. Promotions, reviews and social proof (roughly 89% of shoppers consult reviews) accelerate churn between brands. Loyalty programs and differentiated benefits are used to reduce churn and raise retention.

Omnichannel dynamics

Omnichannel dynamics boost customer bargaining power as marketplaces and quick-commerce shorten lead times and widen choice; platforms like Amazon reported 2023 net sales of 513.98 billion USD, increasing buyer options and price transparency. Digital-native shoppers demand personalization and perceived value, pressuring margins and promotions. Unilever’s D2C and analytics investments improve consumer insight and partly counter retailer leverage, while shifts in channel mix alter negotiation leverage across categories.

- Marketplaces widen choice, compress lead times

- Digital buyers expect personalization/value

- D2C + analytics = more consumer insight

- Channel mix shifts reshape retailer bargaining

Regulatory and ESG expectations

Buyers increasingly demand sustainable packaging, clean labels and ethical sourcing, and non-compliance can trigger retailer delistings or penalties that weaken suppliers' negotiating positions. Meeting these standards raises costs but secures shelf space and consumer trust; Unilever has pledged 100% recyclable/reusable/compostable packaging and to halve virgin plastic use by 2025, strengthening its bargaining leverage with buyers.

- Buyers: demand sustainable packaging, clean labels, ethical sourcing

- Risk: retailer delistings/penalties reduce supplier leverage

- Cost: compliance raises COGS but protects shelf presence

- Fact: Unilever target—100% recyclable/reusable/compostable packaging; halve virgin plastic by 2025

Retail power, 14% FMCG e-comm, 89% review influence

Global retailers (Walmart revenue US$611.3bn FY2024) and e‑marketplaces (Amazon sales US$513.98bn 2023) exert strong pricing and shelf leverage, while 14% FMCG e‑commerce penetration and 89% review consults raise consumer bargaining power. Private labels (~40% EU grocery) compress premiums; sustainability mandates (Unilever 2025 packaging targets) shift costs but protect access.

| Metric | Value |

|---|---|

| Walmart rev | US$611.3bn FY2024 |

| Amazon sales | US$513.98bn 2023 |

| FMCG e‑comm | 14% 2023 |

| EU private label | ~40% |

What You See Is What You Get

Unilever Porter's Five Forces Analysis

This preview shows the exact Unilever Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. It provides a concise assessment of competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes tailored to Unilever's consumer goods context. The file is fully formatted and ready for immediate download and use.

Description

Go Beyond the Preview—Access the Full Strategic Report

Unilever faces intense competitive rivalry across personal care and FMCG, with scale and strong brands partly insulating margins. Buyer power is significant in retail channel negotiations, though consumer loyalty limits price elasticity. Supplier power is moderate and threats from substitutes and new entrants are manageable but persistent. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Unilever’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse raw materials

Unilever sources agricultural oils, fragrances, chemicals and packaging across global markets—operating in over 190 countries—which dilutes any single supplier’s leverage and spreads risk.

Many inputs are commodity-like, making benchmarking transparent and keeping switching costs moderate.

However, traceability and strict quality requirements in categories like palm oil and fragrances create supplier stickiness.

Scale purchasing leverage

Unilever's massive scale—serving ~2.5 billion consumers daily and generating ~€61bn revenue in 2023—lets procurement extract volume discounts, multi-year contracts and hedging, lowering supplier price pass-through and volatility. Preferred-supplier programs and dual sourcing further curb dependence. Suppliers routinely compete for access to Unilever volumes, intensifying buyer leverage.

Specialty ingredients

Certain actives, enzymes and fragrances are supplied by a handful of specialist houses; in 2024 the top five fragrance firms still control roughly 80% of the global market, creating niche supplier leverage. Reformulation to switch vendors often takes 6–12 months and incurs significant testing and validation costs, raising switching friction. Patented actives and tight technical specs further entrench suppliers, so these pockets amplify supplier influence despite Unilever’s overall scale.

Sustainability constraints

Sustainability constraints — driven by Unilever’s 2024 commitments to 100% reusable/recyclable/compostable packaging by 2025 and net‑zero value chain emissions by 2039 — narrow the approved supplier base for palm oil, plastics and energy inputs.

Certified suppliers command premiums, reduce substitution options, and face higher qualification costs from audits and traceability; ethical sourcing thus strengthens select supplier bargaining power.

- Approved supplier pool tightened (traceability/audits)

- Certified inputs command price premiums

- Higher supplier qualification costs

- Ethical sourcing increases supplier leverage

Geopolitics and logistics

Geopolitics, trade restrictions, weather shocks and freight bottlenecks periodically tighten supply and push up input costs, giving suppliers short-term leverage when capacity is constrained; Unilever cites regional sourcing and larger inventory buffers to reduce exposure.

- Trade restrictions raise lead times

- Weather shocks tighten capacity

- Freight bottlenecks lift supplier power

- Regionalization + inventory buffers mitigate risk

Global consumer scale and buyer leverage vs concentrated fragrance firms and sustainability limits

Unilever’s global scale (≈2.5bn consumers/day; €61bn revenue in 2023) and procurement programs drive strong buyer leverage, but certified/traceable suppliers and specialist fragrance/active houses retain pockets of power. In 2024 the top five fragrance firms control ~80% of the market, and sustainability requirements (100% reusable/recyclable/compostable packaging by 2025; net‑zero by 2039) narrow approved suppliers. Geopolitical, weather and freight shocks create episodic supplier leverage despite dual sourcing and inventory buffers.

| Metric | Value | Effect on Supplier Power |

|---|---|---|

| Consumers reached | ≈2.5bn/day | Increases buyer leverage |

| Revenue (2023) | ≈€61bn | Volume discounts |

| Fragrance top5 (2024) | ≈80% market share | Raises niche supplier power |

| Packaging target | 100% by 2025 | Tightens approved suppliers |

What is included in the product

Comprehensive Porter’s Five Forces analysis of Unilever revealing competitive intensity, buyer and supplier power, substitute threats, and entry barriers, highlighting disruptive risks and strategic levers to protect market share.

A single-sheet Unilever Porter's Five Forces snapshot that distills competitive pressures into actionable insights—ideal for fast strategic decisions and boardroom slides.

Customers Bargaining Power

Retail giants’ clout

Global retailers and wholesalers like Walmart (US$611.3bn revenue FY2024) exert strong leverage to negotiate price, payment terms and shelf space, concentrating bargaining power through consolidation. Trade spend and slotting fees squeeze supplier margins, often shifting promotional costs onto manufacturers. Unilever offsets this pressure with entrenched category leadership and high-demand brands that secure shelf presence and promotional support.

Private label pressure

Store-brand penetration in Europe is roughly 40% of grocery sales, and private labels increasingly offer cheaper substitutes in home and personal care, compressing Unilever's premium gaps. This heightens price sensitivity among consumers and erodes margins as trading-down rises, especially during recessionary cycles when private-label sales spike. Unilever's defense depends on sustained brand equity and accelerated innovation to protect share and pricing. Recent retailer assortments show growing shelf space for private labels, intensifying competitive pressure.

Consumer switching ease

Low switching costs and abundant options empower consumers; global FMCG e-commerce penetration reached about 14% in 2023, increasing price and product comparison. Promotions, reviews and social proof (roughly 89% of shoppers consult reviews) accelerate churn between brands. Loyalty programs and differentiated benefits are used to reduce churn and raise retention.

Omnichannel dynamics

Omnichannel dynamics boost customer bargaining power as marketplaces and quick-commerce shorten lead times and widen choice; platforms like Amazon reported 2023 net sales of 513.98 billion USD, increasing buyer options and price transparency. Digital-native shoppers demand personalization and perceived value, pressuring margins and promotions. Unilever’s D2C and analytics investments improve consumer insight and partly counter retailer leverage, while shifts in channel mix alter negotiation leverage across categories.

- Marketplaces widen choice, compress lead times

- Digital buyers expect personalization/value

- D2C + analytics = more consumer insight

- Channel mix shifts reshape retailer bargaining

Regulatory and ESG expectations

Buyers increasingly demand sustainable packaging, clean labels and ethical sourcing, and non-compliance can trigger retailer delistings or penalties that weaken suppliers' negotiating positions. Meeting these standards raises costs but secures shelf space and consumer trust; Unilever has pledged 100% recyclable/reusable/compostable packaging and to halve virgin plastic use by 2025, strengthening its bargaining leverage with buyers.

- Buyers: demand sustainable packaging, clean labels, ethical sourcing

- Risk: retailer delistings/penalties reduce supplier leverage

- Cost: compliance raises COGS but protects shelf presence

- Fact: Unilever target—100% recyclable/reusable/compostable packaging; halve virgin plastic by 2025

Retail power, 14% FMCG e-comm, 89% review influence

Global retailers (Walmart revenue US$611.3bn FY2024) and e‑marketplaces (Amazon sales US$513.98bn 2023) exert strong pricing and shelf leverage, while 14% FMCG e‑commerce penetration and 89% review consults raise consumer bargaining power. Private labels (~40% EU grocery) compress premiums; sustainability mandates (Unilever 2025 packaging targets) shift costs but protect access.

| Metric | Value |

|---|---|

| Walmart rev | US$611.3bn FY2024 |

| Amazon sales | US$513.98bn 2023 |

| FMCG e‑comm | 14% 2023 |

| EU private label | ~40% |

What You See Is What You Get

Unilever Porter's Five Forces Analysis

This preview shows the exact Unilever Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. It provides a concise assessment of competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes tailored to Unilever's consumer goods context. The file is fully formatted and ready for immediate download and use.