United Utilities Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

United Utilities Group faces moderate supplier power, stable buyer demand, high regulatory barriers, low threat of substitutes, and moderate rivalry driven by regional utilities — this snapshot highlights key pressures shaping profitability and strategic choices. This brief preview only scratches the surface; unlock the full Porter’s Five Forces Analysis for detailed force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialist chemical and energy inputs

United Utilities depends on a limited pool of specialist water-treatment chemicals and remains exposed to volatile wholesale energy markets, with the company reporting energy-driven operating cost pressures in 2024 and energy costs rising roughly 15% year-on-year in 2023–24. Concentration among chemical suppliers elevates switching costs and delivery risk, tightening procurement options and logistics. Long-term contracts and energy hedges have reduced short-term volatility but cannot eliminate market spikes, while progressively stricter regulatory water-quality standards in 2024 narrowed the pool of qualified suppliers further.

Capital projects and contractor dependence

Large AMP-cycle programmes — water sector AMP7 totals ~£51bn for 2020–25 (Ofwat) — rely on major engineering, civils and M&E Tier‑1 contractors, concentrating supplier power. Capacity constraints and recent civils cost pressure elevate leverage despite framework agreements and competitive tenders. Key Tier‑1s remain pivotal for timely delivery, and mission‑critical performance limits scope for aggressive price negotiation.

Technology and asset OEMs

SCADA, telemetry, smart meters, pumps, membranes and analytics often come from proprietary OEMs, creating technical lock-in and high integration and switching costs for United Utilities, which serves about 7 million household customers in North West England; open standards and modular procurement reduce but do not eliminate this dependency. Lifecycle support agreements and stringent cybersecurity and data-compliance requirements further constrain vendor choice and bargaining leverage.

Skilled labor and unionized workforce

Specialist operators, network engineers and process scientists remain scarce in 2024, giving labour suppliers meaningful bargaining power as wage pressure and long training lead-times raise replacement costs; outsourcing for peak workloads still depends on those scarce skills, while strong workforce relations and retention programmes are essential to stabilise costs and service levels.

- Specialist skill shortage: operators, engineers, scientists

- Wage pressure + long training lead-times increase supplier leverage

- Outsourcing for peaks still reliant on scarce skills

- Retention and relations critical to stabilise costs and service

Raw water abstraction and environmental constraints

Raw water access for United Utilities is set by the Environment Agency and environmental stakeholders rather than market suppliers; the company serves about 7 million customers across North West England and operates under tight AMP7 environmental targets (2020–25). Seasonal hydrology and fixed abstraction licences constrain available input volumes, while river health and nutrient limits can force higher treatment and compliance costs, effectively acting as high-power external suppliers.

- Environment Agency control of abstractions

- ~7 million customers — regional supply constraints

- AMP7 environmental targets increase CAPEX/OPEX

Concentrated suppliers, lock-in and +15% energy spike pressure water sector

United Utilities faces concentrated suppliers of chemicals, OEMs and Tier‑1 contractors that limit bargaining power. Energy costs rose ~15% y/y in 2023–24, while AMP7 sector spend is ~£51bn (2020–25) and the company serves ~7 million customers, all increasing supplier leverage. Long contracts, technical lock‑in and 2024 skill shortages moderate negotiation despite hedges and frameworks.

| Metric | Value | Impact |

|---|---|---|

| Energy cost change 2023–24 | +~15% | Higher OPEX |

| Customers | ~7m | Scale dependence |

| AMP7 sector spend | £51bn (2020–25) | Tier‑1 concentration |

What is included in the product

Concise Porter’s Five Forces overview for United Utilities Group, highlighting competitive rivalry, buyer and supplier power, substitute risks, and barriers to entry to assess threats, pricing leverage, and strategic resilience.

Clear one-sheet Porter's Five Forces for United Utilities Group—instantly highlights regulatory, supplier and competitive pressure to relieve strategic uncertainty and accelerate boardroom decisions. Customizable pressure levels and spider-chart visuals make it easy to update for regulatory shifts or M&A scenarios.

Customers Bargaining Power

Household customers are captive

Domestic users in United Utilities' North West region are captive, with the company serving around 7 million customers, so households cannot switch water or wastewater provider and have limited direct price bargaining power.

Affordability pressures and service expectations create reputational risk—Ofwat data showed average household water bills around £440 in 2024—heightening scrutiny and complaint volumes.

Social tariffs, targeted hardship schemes and active customer engagement (priority registers and payment plans) mitigate bill impacts and temper political and regulatory pressure.

Business retail market dynamics

Since the non-household market opened in 2017, non-household customers can switch among 20+ retailers by 2024 while United Utilities remains the sole wholesale provider to its c.7 million regional customers. Retail competition shifts billing and some service pressure downstream to retailers, reducing UU's direct customer-facing exposure. Large industrial users exert bargaining power through retailer-negotiated service levels and bespoke contracts. Ofwat's PR24 wholesale charging rules (set for 2025–30) constrain UU's overall pricing freedom.

Regulatory surrogate for customers

Ofwat and the Consumer Council for Water act as regulatory surrogates, amplifying customer interests and shaping expectations under PR24 outcome regimes. Outcome Delivery Incentives tie a portion of allowed revenue to service performance, increasing financial exposure for United Utilities. Poor customer satisfaction can trigger ODIs, penalties and heightened regulatory scrutiny, creating indirect buyer power despite captive end users.

Elasticity of demand is low

Elasticity of demand for United Utilities is low because water is essential and short-run consumption is hard to cut, reducing customers' bargaining power; United Utilities serves about 7 million household customers and the Ofwat 2023–24 average household bill was £448, anchoring willingness to pay. Metering and efficiency programs can moderate usage, while drought measures and public campaigns shift behavior at the margin.

- Essential service → low price elasticity

- ~7 million customers (United Utilities)

- Ofwat 2023–24 avg bill £448

- Metering/efficiency reduce usage

- Drought measures change marginal behavior

Service quality and environmental expectations

Rising expectations on leakage, pollution events and river health have elevated perceived value of United Utilities services; the company serves about 7 million customers in the North West, magnifying public scrutiny. Customer advocacy and media attention—heightened after high-profile 2023–24 incidents—push faster investment and operational change. Failures can trigger political intervention and regulatory penalties, strengthening customer influence over capital allocation.

- 7 million customers

- Heightened 2023–24 scrutiny

- Customer/media pressure → faster investment

North West water: 7m homes, avg bill £448, PR24 shifts customer power

Households served c.7 million in the North West, captive to United Utilities so direct price bargaining is limited; Ofwat 2023–24 average household bill was £448. Non-household retail competition (20+ retailers by 2024) shifts billing pressure away from UU while UU remains sole wholesale provider. PR24 (2025–30) links revenue to outcomes, increasing indirect customer power via regulators.

| Metric | Value |

|---|---|

| Household customers | c.7 million |

| Avg bill (Ofwat 2023–24) | £448 |

| Retailers (non-household, 2024) | 20+ |

| PR24 period | 2025–30 |

Preview Before You Purchase

United Utilities Group Porter's Five Forces Analysis

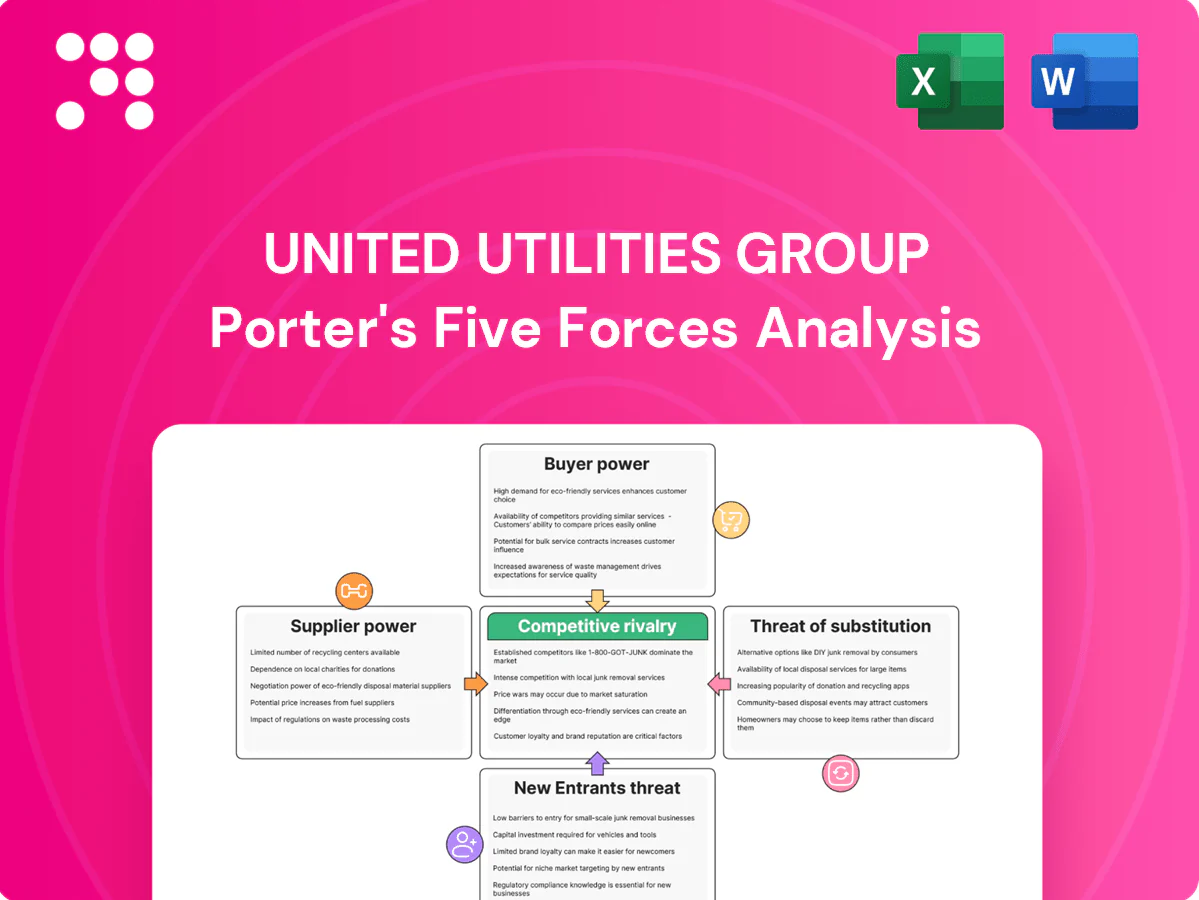

This United Utilities Group Porter's Five Forces Analysis examines supplier and buyer power, barriers to entry, substitute threats and industry rivalry in the UK regulated water sector, highlighting strong regulation, low substitution risk, modest supplier leverage and moderate rivalry. The preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders, ready to use.

From Overview to Strategy Blueprint

United Utilities Group faces moderate supplier power, stable buyer demand, high regulatory barriers, low threat of substitutes, and moderate rivalry driven by regional utilities — this snapshot highlights key pressures shaping profitability and strategic choices. This brief preview only scratches the surface; unlock the full Porter’s Five Forces Analysis for detailed force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialist chemical and energy inputs

United Utilities depends on a limited pool of specialist water-treatment chemicals and remains exposed to volatile wholesale energy markets, with the company reporting energy-driven operating cost pressures in 2024 and energy costs rising roughly 15% year-on-year in 2023–24. Concentration among chemical suppliers elevates switching costs and delivery risk, tightening procurement options and logistics. Long-term contracts and energy hedges have reduced short-term volatility but cannot eliminate market spikes, while progressively stricter regulatory water-quality standards in 2024 narrowed the pool of qualified suppliers further.

Capital projects and contractor dependence

Large AMP-cycle programmes — water sector AMP7 totals ~£51bn for 2020–25 (Ofwat) — rely on major engineering, civils and M&E Tier‑1 contractors, concentrating supplier power. Capacity constraints and recent civils cost pressure elevate leverage despite framework agreements and competitive tenders. Key Tier‑1s remain pivotal for timely delivery, and mission‑critical performance limits scope for aggressive price negotiation.

Technology and asset OEMs

SCADA, telemetry, smart meters, pumps, membranes and analytics often come from proprietary OEMs, creating technical lock-in and high integration and switching costs for United Utilities, which serves about 7 million household customers in North West England; open standards and modular procurement reduce but do not eliminate this dependency. Lifecycle support agreements and stringent cybersecurity and data-compliance requirements further constrain vendor choice and bargaining leverage.

Skilled labor and unionized workforce

Specialist operators, network engineers and process scientists remain scarce in 2024, giving labour suppliers meaningful bargaining power as wage pressure and long training lead-times raise replacement costs; outsourcing for peak workloads still depends on those scarce skills, while strong workforce relations and retention programmes are essential to stabilise costs and service levels.

- Specialist skill shortage: operators, engineers, scientists

- Wage pressure + long training lead-times increase supplier leverage

- Outsourcing for peaks still reliant on scarce skills

- Retention and relations critical to stabilise costs and service

Raw water abstraction and environmental constraints

Raw water access for United Utilities is set by the Environment Agency and environmental stakeholders rather than market suppliers; the company serves about 7 million customers across North West England and operates under tight AMP7 environmental targets (2020–25). Seasonal hydrology and fixed abstraction licences constrain available input volumes, while river health and nutrient limits can force higher treatment and compliance costs, effectively acting as high-power external suppliers.

- Environment Agency control of abstractions

- ~7 million customers — regional supply constraints

- AMP7 environmental targets increase CAPEX/OPEX

Concentrated suppliers, lock-in and +15% energy spike pressure water sector

United Utilities faces concentrated suppliers of chemicals, OEMs and Tier‑1 contractors that limit bargaining power. Energy costs rose ~15% y/y in 2023–24, while AMP7 sector spend is ~£51bn (2020–25) and the company serves ~7 million customers, all increasing supplier leverage. Long contracts, technical lock‑in and 2024 skill shortages moderate negotiation despite hedges and frameworks.

| Metric | Value | Impact |

|---|---|---|

| Energy cost change 2023–24 | +~15% | Higher OPEX |

| Customers | ~7m | Scale dependence |

| AMP7 sector spend | £51bn (2020–25) | Tier‑1 concentration |

What is included in the product

Concise Porter’s Five Forces overview for United Utilities Group, highlighting competitive rivalry, buyer and supplier power, substitute risks, and barriers to entry to assess threats, pricing leverage, and strategic resilience.

Clear one-sheet Porter's Five Forces for United Utilities Group—instantly highlights regulatory, supplier and competitive pressure to relieve strategic uncertainty and accelerate boardroom decisions. Customizable pressure levels and spider-chart visuals make it easy to update for regulatory shifts or M&A scenarios.

Customers Bargaining Power

Household customers are captive

Domestic users in United Utilities' North West region are captive, with the company serving around 7 million customers, so households cannot switch water or wastewater provider and have limited direct price bargaining power.

Affordability pressures and service expectations create reputational risk—Ofwat data showed average household water bills around £440 in 2024—heightening scrutiny and complaint volumes.

Social tariffs, targeted hardship schemes and active customer engagement (priority registers and payment plans) mitigate bill impacts and temper political and regulatory pressure.

Business retail market dynamics

Since the non-household market opened in 2017, non-household customers can switch among 20+ retailers by 2024 while United Utilities remains the sole wholesale provider to its c.7 million regional customers. Retail competition shifts billing and some service pressure downstream to retailers, reducing UU's direct customer-facing exposure. Large industrial users exert bargaining power through retailer-negotiated service levels and bespoke contracts. Ofwat's PR24 wholesale charging rules (set for 2025–30) constrain UU's overall pricing freedom.

Regulatory surrogate for customers

Ofwat and the Consumer Council for Water act as regulatory surrogates, amplifying customer interests and shaping expectations under PR24 outcome regimes. Outcome Delivery Incentives tie a portion of allowed revenue to service performance, increasing financial exposure for United Utilities. Poor customer satisfaction can trigger ODIs, penalties and heightened regulatory scrutiny, creating indirect buyer power despite captive end users.

Elasticity of demand is low

Elasticity of demand for United Utilities is low because water is essential and short-run consumption is hard to cut, reducing customers' bargaining power; United Utilities serves about 7 million household customers and the Ofwat 2023–24 average household bill was £448, anchoring willingness to pay. Metering and efficiency programs can moderate usage, while drought measures and public campaigns shift behavior at the margin.

- Essential service → low price elasticity

- ~7 million customers (United Utilities)

- Ofwat 2023–24 avg bill £448

- Metering/efficiency reduce usage

- Drought measures change marginal behavior

Service quality and environmental expectations

Rising expectations on leakage, pollution events and river health have elevated perceived value of United Utilities services; the company serves about 7 million customers in the North West, magnifying public scrutiny. Customer advocacy and media attention—heightened after high-profile 2023–24 incidents—push faster investment and operational change. Failures can trigger political intervention and regulatory penalties, strengthening customer influence over capital allocation.

- 7 million customers

- Heightened 2023–24 scrutiny

- Customer/media pressure → faster investment

North West water: 7m homes, avg bill £448, PR24 shifts customer power

Households served c.7 million in the North West, captive to United Utilities so direct price bargaining is limited; Ofwat 2023–24 average household bill was £448. Non-household retail competition (20+ retailers by 2024) shifts billing pressure away from UU while UU remains sole wholesale provider. PR24 (2025–30) links revenue to outcomes, increasing indirect customer power via regulators.

| Metric | Value |

|---|---|

| Household customers | c.7 million |

| Avg bill (Ofwat 2023–24) | £448 |

| Retailers (non-household, 2024) | 20+ |

| PR24 period | 2025–30 |

Preview Before You Purchase

United Utilities Group Porter's Five Forces Analysis

This United Utilities Group Porter's Five Forces Analysis examines supplier and buyer power, barriers to entry, substitute threats and industry rivalry in the UK regulated water sector, highlighting strong regulation, low substitution risk, modest supplier leverage and moderate rivalry. The preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders, ready to use.

Description

From Overview to Strategy Blueprint

United Utilities Group faces moderate supplier power, stable buyer demand, high regulatory barriers, low threat of substitutes, and moderate rivalry driven by regional utilities — this snapshot highlights key pressures shaping profitability and strategic choices. This brief preview only scratches the surface; unlock the full Porter’s Five Forces Analysis for detailed force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialist chemical and energy inputs

United Utilities depends on a limited pool of specialist water-treatment chemicals and remains exposed to volatile wholesale energy markets, with the company reporting energy-driven operating cost pressures in 2024 and energy costs rising roughly 15% year-on-year in 2023–24. Concentration among chemical suppliers elevates switching costs and delivery risk, tightening procurement options and logistics. Long-term contracts and energy hedges have reduced short-term volatility but cannot eliminate market spikes, while progressively stricter regulatory water-quality standards in 2024 narrowed the pool of qualified suppliers further.

Capital projects and contractor dependence

Large AMP-cycle programmes — water sector AMP7 totals ~£51bn for 2020–25 (Ofwat) — rely on major engineering, civils and M&E Tier‑1 contractors, concentrating supplier power. Capacity constraints and recent civils cost pressure elevate leverage despite framework agreements and competitive tenders. Key Tier‑1s remain pivotal for timely delivery, and mission‑critical performance limits scope for aggressive price negotiation.

Technology and asset OEMs

SCADA, telemetry, smart meters, pumps, membranes and analytics often come from proprietary OEMs, creating technical lock-in and high integration and switching costs for United Utilities, which serves about 7 million household customers in North West England; open standards and modular procurement reduce but do not eliminate this dependency. Lifecycle support agreements and stringent cybersecurity and data-compliance requirements further constrain vendor choice and bargaining leverage.

Skilled labor and unionized workforce

Specialist operators, network engineers and process scientists remain scarce in 2024, giving labour suppliers meaningful bargaining power as wage pressure and long training lead-times raise replacement costs; outsourcing for peak workloads still depends on those scarce skills, while strong workforce relations and retention programmes are essential to stabilise costs and service levels.

- Specialist skill shortage: operators, engineers, scientists

- Wage pressure + long training lead-times increase supplier leverage

- Outsourcing for peaks still reliant on scarce skills

- Retention and relations critical to stabilise costs and service

Raw water abstraction and environmental constraints

Raw water access for United Utilities is set by the Environment Agency and environmental stakeholders rather than market suppliers; the company serves about 7 million customers across North West England and operates under tight AMP7 environmental targets (2020–25). Seasonal hydrology and fixed abstraction licences constrain available input volumes, while river health and nutrient limits can force higher treatment and compliance costs, effectively acting as high-power external suppliers.

- Environment Agency control of abstractions

- ~7 million customers — regional supply constraints

- AMP7 environmental targets increase CAPEX/OPEX

Concentrated suppliers, lock-in and +15% energy spike pressure water sector

United Utilities faces concentrated suppliers of chemicals, OEMs and Tier‑1 contractors that limit bargaining power. Energy costs rose ~15% y/y in 2023–24, while AMP7 sector spend is ~£51bn (2020–25) and the company serves ~7 million customers, all increasing supplier leverage. Long contracts, technical lock‑in and 2024 skill shortages moderate negotiation despite hedges and frameworks.

| Metric | Value | Impact |

|---|---|---|

| Energy cost change 2023–24 | +~15% | Higher OPEX |

| Customers | ~7m | Scale dependence |

| AMP7 sector spend | £51bn (2020–25) | Tier‑1 concentration |

What is included in the product

Concise Porter’s Five Forces overview for United Utilities Group, highlighting competitive rivalry, buyer and supplier power, substitute risks, and barriers to entry to assess threats, pricing leverage, and strategic resilience.

Clear one-sheet Porter's Five Forces for United Utilities Group—instantly highlights regulatory, supplier and competitive pressure to relieve strategic uncertainty and accelerate boardroom decisions. Customizable pressure levels and spider-chart visuals make it easy to update for regulatory shifts or M&A scenarios.

Customers Bargaining Power

Household customers are captive

Domestic users in United Utilities' North West region are captive, with the company serving around 7 million customers, so households cannot switch water or wastewater provider and have limited direct price bargaining power.

Affordability pressures and service expectations create reputational risk—Ofwat data showed average household water bills around £440 in 2024—heightening scrutiny and complaint volumes.

Social tariffs, targeted hardship schemes and active customer engagement (priority registers and payment plans) mitigate bill impacts and temper political and regulatory pressure.

Business retail market dynamics

Since the non-household market opened in 2017, non-household customers can switch among 20+ retailers by 2024 while United Utilities remains the sole wholesale provider to its c.7 million regional customers. Retail competition shifts billing and some service pressure downstream to retailers, reducing UU's direct customer-facing exposure. Large industrial users exert bargaining power through retailer-negotiated service levels and bespoke contracts. Ofwat's PR24 wholesale charging rules (set for 2025–30) constrain UU's overall pricing freedom.

Regulatory surrogate for customers

Ofwat and the Consumer Council for Water act as regulatory surrogates, amplifying customer interests and shaping expectations under PR24 outcome regimes. Outcome Delivery Incentives tie a portion of allowed revenue to service performance, increasing financial exposure for United Utilities. Poor customer satisfaction can trigger ODIs, penalties and heightened regulatory scrutiny, creating indirect buyer power despite captive end users.

Elasticity of demand is low

Elasticity of demand for United Utilities is low because water is essential and short-run consumption is hard to cut, reducing customers' bargaining power; United Utilities serves about 7 million household customers and the Ofwat 2023–24 average household bill was £448, anchoring willingness to pay. Metering and efficiency programs can moderate usage, while drought measures and public campaigns shift behavior at the margin.

- Essential service → low price elasticity

- ~7 million customers (United Utilities)

- Ofwat 2023–24 avg bill £448

- Metering/efficiency reduce usage

- Drought measures change marginal behavior

Service quality and environmental expectations

Rising expectations on leakage, pollution events and river health have elevated perceived value of United Utilities services; the company serves about 7 million customers in the North West, magnifying public scrutiny. Customer advocacy and media attention—heightened after high-profile 2023–24 incidents—push faster investment and operational change. Failures can trigger political intervention and regulatory penalties, strengthening customer influence over capital allocation.

- 7 million customers

- Heightened 2023–24 scrutiny

- Customer/media pressure → faster investment

North West water: 7m homes, avg bill £448, PR24 shifts customer power

Households served c.7 million in the North West, captive to United Utilities so direct price bargaining is limited; Ofwat 2023–24 average household bill was £448. Non-household retail competition (20+ retailers by 2024) shifts billing pressure away from UU while UU remains sole wholesale provider. PR24 (2025–30) links revenue to outcomes, increasing indirect customer power via regulators.

| Metric | Value |

|---|---|

| Household customers | c.7 million |

| Avg bill (Ofwat 2023–24) | £448 |

| Retailers (non-household, 2024) | 20+ |

| PR24 period | 2025–30 |

Preview Before You Purchase

United Utilities Group Porter's Five Forces Analysis

This United Utilities Group Porter's Five Forces Analysis examines supplier and buyer power, barriers to entry, substitute threats and industry rivalry in the UK regulated water sector, highlighting strong regulation, low substitution risk, modest supplier leverage and moderate rivalry. The preview is the exact, fully formatted document you'll receive immediately after purchase—no placeholders, ready to use.