United Utilities Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how regulatory change, climate risks, and infrastructure investment are reshaping United Utilities Group's outlook. Our concise PESTLE highlights political, economic, social, technological, legal and environmental drivers with actionable implications for investors and strategists. Buy the full analysis to access detailed data, scenario-driven risks and ready-to-use strategic recommendations.

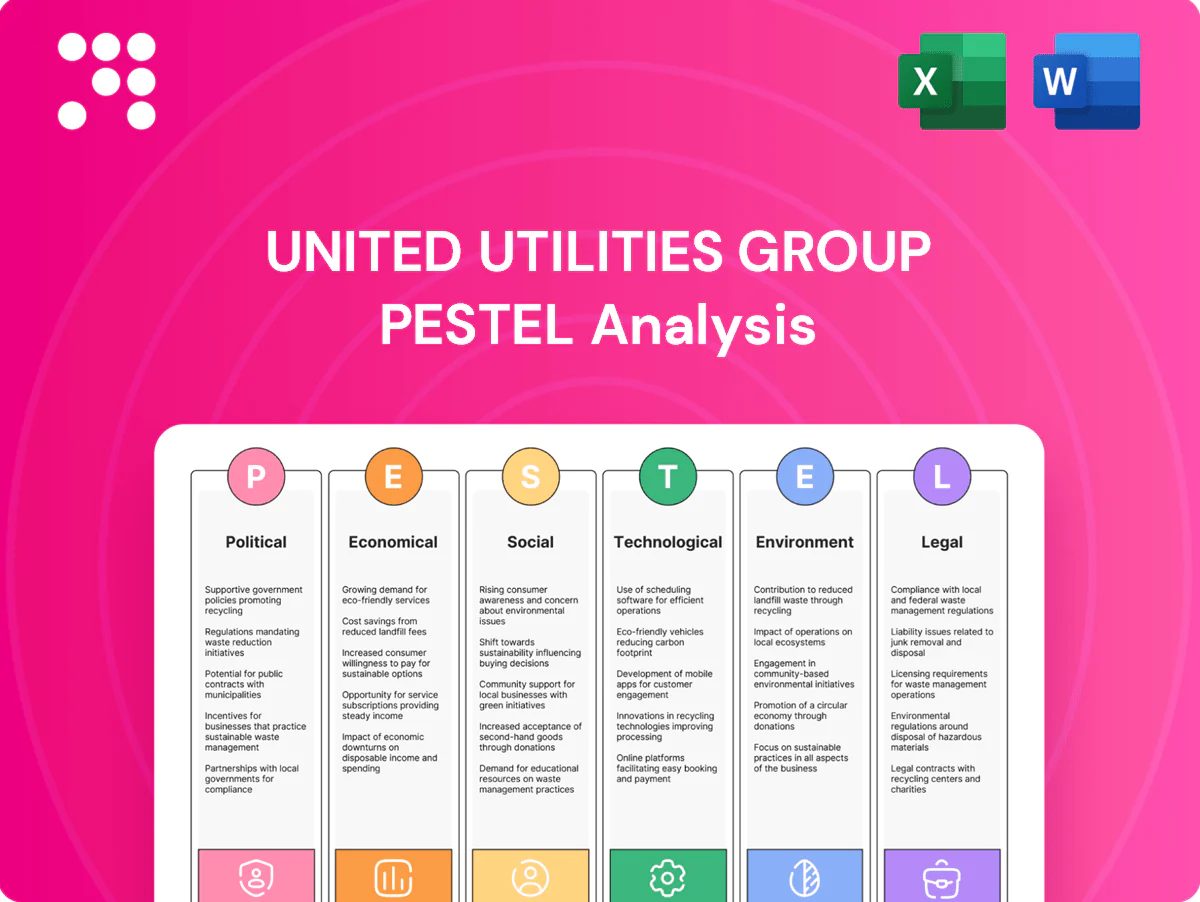

Political factors

Ofwat price control

Ofwat’s five-year PR24 review (covering 2025–30) sets allowed revenues and service outcomes that directly determine United Utilities’ investment profile, customer bills and regulated returns; United Utilities has a regulatory capital value of about £7.6bn (2023/24). Tighter efficiency and performance incentives in determinations can shift value from shareholders to customers, while proactive engagement and outperformance recover incentives and reputational capital.

Sewage spill scrutiny

National focus on storm overflows—highlighted by analyses showing about 400,000 discharges in England in recent years—raises expectations for faster pollution reduction. Ministers and MPs are pressing regulators to demand stricter penalties and tighter timelines, and public inquiries and select committees are already shaping near‑term spending priorities. This increases pressure on United Utilities for credible delivery plans and transparent, frequent reporting.

Infrastructure policy

Government support for critical infrastructure can unlock larger capital programmes for United Utilities, which serves about 7 million customers in the North West; planning reforms and regional growth agendas directly affect reservoir, pipeline and treatment upgrades. Political backing for nature‑based solutions may unlock grants or partnerships tied to the UKs £5.2bn flood‑defence commitment (2021–27). However, post‑election policy shifts can quickly alter funding certainty.

Public ownership debate

Periodic calls for renationalisation and tighter public control fuel strategic uncertainty for United Utilities, which supplies water to about 7 million customers in the North West and faces the PR24 regime (Ofwat, Dec 2023) that raises environmental and performance standards. Even without ownership change, tougher mandates can compress returns; strong service reliability, environmental delivery and transparent governance disclosures help limit policy risk premiums.

- Customers served: ~7 million

- Regulator: Ofwat PR24 raised performance expectations (Dec 2023)

- Mitigation: reliability, environmental performance, governance disclosures

Devolution dynamics

United Utilities, serving about 7 million customers across the North West, must align catchment strategies with local and regional authorities such as Greater Manchester Combined Authority and Liverpool City Region, which control planning approvals and funding levers. Alignment with Northern priorities—jobs, resilience and environment—increases project acceptance, while shifting political coalitions can speed or stall major schemes. Community benefits and local procurement strengthen political goodwill and reduce approval friction.

- Regional footprint: North West, ~7 million customers

- Key stakeholders: GMCA, Liverpool City Region

- Priority alignment: jobs, resilience, environment

- Political risk: coalition changes can accelerate or delay projects

PR24, storm overflow penalties and RCV ≈ £7.6bn reshape water spending

Ofwat’s PR24 (2025–30) sets allowed revenues and tougher incentives that directly shape United Utilities’ investment, customer bills and returns; RCV ~£7.6bn (2023/24). Public and ministerial pressure on storm overflows (≈400,000 discharges recently) raises penalties and faster delivery expectations. Government flood spend (£5.2bn, 2021–27) and regional planning influence project funding and timelines. Renationalisation talk and shifting coalitions increase policy uncertainty.

| Metric | Value |

|---|---|

| Customers | ~7,000,000 |

| Regulatory capital value | £7.6bn (2023/24) |

| Storm overflows | ≈400,000 discharges |

| PR24 period | 2025–2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect United Utilities Group, with data-driven trends and region-specific regulatory context. Designed to help executives and investors identify actionable risks, opportunities and scenario-driven strategies.

A concise, visually segmented PESTLE summary of United Utilities Group that’s easily dropped into presentations, edited with region- or business-specific notes, and shared across teams to speed risk discussions and strategic alignment during planning sessions.

Economic factors

Inflation linkage

Regulated asset values and allowed revenues for UK water firms, including United Utilities, are commonly indexed to inflation measures such as RPI/CPIH, giving partial protection against cost rises but tending to lift customer bills.

Mismatches between indexation and actual input-cost moves—notably the energy shocks of 2021–22 when European wholesale gas prices roughly doubled—create margin risk.

Effective hedging of energy and proactive procurement have been used to stabilise cash flows and mitigate volatility in recent years.

Interest rate exposure

Capital‑intensive utilities like United Utilities rely on substantial debt financing; with the Bank of England base rate at 5.25% and 10‑year UK gilt yields around 4.6% (July 2025), higher base rates and wider credit spreads raise borrowing costs and squeeze interest cover and FFO/debt ratios. Regulatory allowances can lag market moves, creating margin pressure, while prudent liability management and staggered maturities reduce refinancing volatility.

AMP8 capex cycle

The AMP8 2025–30 cycle drives elevated resilience and environmental capex, with the UK water sector targeting c.£55bn investment and United Utilities committing a multi‑hundred‑million pound programme for upgrades. Large programmes strain supply chains and delivery capacity, raising unit costs and schedule risk. Efficient execution can unlock PR24 incentive rewards and long‑term Opex savings, while poor delivery risks regulatory penalties and reputational damage, potentially costing firms hundreds of millions.

Energy and labor costs

Treatment and pumping are energy‑intensive, leaving United Utilities exposed to wholesale power swings; UK wholesale baseload averaged about £55/MWh in 2024, pressuring margins. Tight UK labour markets (unemployment ~4.0% in 2024) and need for specialist engineers drive wage inflation. Onsite generation and long‑term power contracts, plus a target of net‑zero operational emissions by 2030, reduce volatility, while workforce planning and automation curb cost pressure.

- Energy exposure: high (treatment, pumping)

- Wholesale price (2024): ~£55/MWh

- Labour tightness (2024): unemployment ~4.0%

- Mitigants: onsite generation, long‑term contracts, net‑zero 2030

- Cost control: workforce planning, automation

Customer affordability

Household income stress reduces bill headroom and raises bad‑debt risk, forcing United Utilities to expand affordability programs and social tariffs to sustain collections and regulatory compliance. Regulators factor affordability into price settlements, while clear communication of service value supports customer acceptance of necessary investment and resilience measures.

- Household stress increases bad‑debt exposure

- Affordability schemes sustain payment rates

- Regulators embed affordability in price reviews

- Value communication aids investment acceptance

PR24, storm overflow penalties and RCV ≈ £7.6bn reshape water spending

United Utilities faces inflation‑linked allowed revenues that partially offset cost rises, but RPI/CPIH lag and energy shocks (2021–22) created margin risk. Higher rates (Bank Rate 5.25%, 10y gilt ~4.6% Jul 2025) and AMP8 capex (UK water c.£55bn 2025–30) raise financing and delivery costs. Wholesale power ~£55/MWh (2024) and unemployment ~4.0% squeeze margins; mitigants include onsite generation, long‑term contracts and net‑zero 2030 targets.

| Metric | Value |

|---|---|

| Bank Rate (Jul 2025) | 5.25% |

| 10y UK gilt (Jul 2025) | ~4.6% |

| Wholesale power (2024) | ~£55/MWh |

| Unemployment (2024) | ~4.0% |

| UK water capex (AMP8 2025–30) | c.£55bn |

Full Version Awaits

United Utilities Group PESTLE Analysis

The preview shown here is the exact United Utilities Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It includes comprehensive Political, Economic, Social, Technological, Legal and Environmental evaluations with charts and citations. No placeholders or edits are needed; what you see is the final downloadable file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how regulatory change, climate risks, and infrastructure investment are reshaping United Utilities Group's outlook. Our concise PESTLE highlights political, economic, social, technological, legal and environmental drivers with actionable implications for investors and strategists. Buy the full analysis to access detailed data, scenario-driven risks and ready-to-use strategic recommendations.

Political factors

Ofwat price control

Ofwat’s five-year PR24 review (covering 2025–30) sets allowed revenues and service outcomes that directly determine United Utilities’ investment profile, customer bills and regulated returns; United Utilities has a regulatory capital value of about £7.6bn (2023/24). Tighter efficiency and performance incentives in determinations can shift value from shareholders to customers, while proactive engagement and outperformance recover incentives and reputational capital.

Sewage spill scrutiny

National focus on storm overflows—highlighted by analyses showing about 400,000 discharges in England in recent years—raises expectations for faster pollution reduction. Ministers and MPs are pressing regulators to demand stricter penalties and tighter timelines, and public inquiries and select committees are already shaping near‑term spending priorities. This increases pressure on United Utilities for credible delivery plans and transparent, frequent reporting.

Infrastructure policy

Government support for critical infrastructure can unlock larger capital programmes for United Utilities, which serves about 7 million customers in the North West; planning reforms and regional growth agendas directly affect reservoir, pipeline and treatment upgrades. Political backing for nature‑based solutions may unlock grants or partnerships tied to the UKs £5.2bn flood‑defence commitment (2021–27). However, post‑election policy shifts can quickly alter funding certainty.

Public ownership debate

Periodic calls for renationalisation and tighter public control fuel strategic uncertainty for United Utilities, which supplies water to about 7 million customers in the North West and faces the PR24 regime (Ofwat, Dec 2023) that raises environmental and performance standards. Even without ownership change, tougher mandates can compress returns; strong service reliability, environmental delivery and transparent governance disclosures help limit policy risk premiums.

- Customers served: ~7 million

- Regulator: Ofwat PR24 raised performance expectations (Dec 2023)

- Mitigation: reliability, environmental performance, governance disclosures

Devolution dynamics

United Utilities, serving about 7 million customers across the North West, must align catchment strategies with local and regional authorities such as Greater Manchester Combined Authority and Liverpool City Region, which control planning approvals and funding levers. Alignment with Northern priorities—jobs, resilience and environment—increases project acceptance, while shifting political coalitions can speed or stall major schemes. Community benefits and local procurement strengthen political goodwill and reduce approval friction.

- Regional footprint: North West, ~7 million customers

- Key stakeholders: GMCA, Liverpool City Region

- Priority alignment: jobs, resilience, environment

- Political risk: coalition changes can accelerate or delay projects

PR24, storm overflow penalties and RCV ≈ £7.6bn reshape water spending

Ofwat’s PR24 (2025–30) sets allowed revenues and tougher incentives that directly shape United Utilities’ investment, customer bills and returns; RCV ~£7.6bn (2023/24). Public and ministerial pressure on storm overflows (≈400,000 discharges recently) raises penalties and faster delivery expectations. Government flood spend (£5.2bn, 2021–27) and regional planning influence project funding and timelines. Renationalisation talk and shifting coalitions increase policy uncertainty.

| Metric | Value |

|---|---|

| Customers | ~7,000,000 |

| Regulatory capital value | £7.6bn (2023/24) |

| Storm overflows | ≈400,000 discharges |

| PR24 period | 2025–2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect United Utilities Group, with data-driven trends and region-specific regulatory context. Designed to help executives and investors identify actionable risks, opportunities and scenario-driven strategies.

A concise, visually segmented PESTLE summary of United Utilities Group that’s easily dropped into presentations, edited with region- or business-specific notes, and shared across teams to speed risk discussions and strategic alignment during planning sessions.

Economic factors

Inflation linkage

Regulated asset values and allowed revenues for UK water firms, including United Utilities, are commonly indexed to inflation measures such as RPI/CPIH, giving partial protection against cost rises but tending to lift customer bills.

Mismatches between indexation and actual input-cost moves—notably the energy shocks of 2021–22 when European wholesale gas prices roughly doubled—create margin risk.

Effective hedging of energy and proactive procurement have been used to stabilise cash flows and mitigate volatility in recent years.

Interest rate exposure

Capital‑intensive utilities like United Utilities rely on substantial debt financing; with the Bank of England base rate at 5.25% and 10‑year UK gilt yields around 4.6% (July 2025), higher base rates and wider credit spreads raise borrowing costs and squeeze interest cover and FFO/debt ratios. Regulatory allowances can lag market moves, creating margin pressure, while prudent liability management and staggered maturities reduce refinancing volatility.

AMP8 capex cycle

The AMP8 2025–30 cycle drives elevated resilience and environmental capex, with the UK water sector targeting c.£55bn investment and United Utilities committing a multi‑hundred‑million pound programme for upgrades. Large programmes strain supply chains and delivery capacity, raising unit costs and schedule risk. Efficient execution can unlock PR24 incentive rewards and long‑term Opex savings, while poor delivery risks regulatory penalties and reputational damage, potentially costing firms hundreds of millions.

Energy and labor costs

Treatment and pumping are energy‑intensive, leaving United Utilities exposed to wholesale power swings; UK wholesale baseload averaged about £55/MWh in 2024, pressuring margins. Tight UK labour markets (unemployment ~4.0% in 2024) and need for specialist engineers drive wage inflation. Onsite generation and long‑term power contracts, plus a target of net‑zero operational emissions by 2030, reduce volatility, while workforce planning and automation curb cost pressure.

- Energy exposure: high (treatment, pumping)

- Wholesale price (2024): ~£55/MWh

- Labour tightness (2024): unemployment ~4.0%

- Mitigants: onsite generation, long‑term contracts, net‑zero 2030

- Cost control: workforce planning, automation

Customer affordability

Household income stress reduces bill headroom and raises bad‑debt risk, forcing United Utilities to expand affordability programs and social tariffs to sustain collections and regulatory compliance. Regulators factor affordability into price settlements, while clear communication of service value supports customer acceptance of necessary investment and resilience measures.

- Household stress increases bad‑debt exposure

- Affordability schemes sustain payment rates

- Regulators embed affordability in price reviews

- Value communication aids investment acceptance

PR24, storm overflow penalties and RCV ≈ £7.6bn reshape water spending

United Utilities faces inflation‑linked allowed revenues that partially offset cost rises, but RPI/CPIH lag and energy shocks (2021–22) created margin risk. Higher rates (Bank Rate 5.25%, 10y gilt ~4.6% Jul 2025) and AMP8 capex (UK water c.£55bn 2025–30) raise financing and delivery costs. Wholesale power ~£55/MWh (2024) and unemployment ~4.0% squeeze margins; mitigants include onsite generation, long‑term contracts and net‑zero 2030 targets.

| Metric | Value |

|---|---|

| Bank Rate (Jul 2025) | 5.25% |

| 10y UK gilt (Jul 2025) | ~4.6% |

| Wholesale power (2024) | ~£55/MWh |

| Unemployment (2024) | ~4.0% |

| UK water capex (AMP8 2025–30) | c.£55bn |

Full Version Awaits

United Utilities Group PESTLE Analysis

The preview shown here is the exact United Utilities Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It includes comprehensive Political, Economic, Social, Technological, Legal and Environmental evaluations with charts and citations. No placeholders or edits are needed; what you see is the final downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how regulatory change, climate risks, and infrastructure investment are reshaping United Utilities Group's outlook. Our concise PESTLE highlights political, economic, social, technological, legal and environmental drivers with actionable implications for investors and strategists. Buy the full analysis to access detailed data, scenario-driven risks and ready-to-use strategic recommendations.

Political factors

Ofwat price control

Ofwat’s five-year PR24 review (covering 2025–30) sets allowed revenues and service outcomes that directly determine United Utilities’ investment profile, customer bills and regulated returns; United Utilities has a regulatory capital value of about £7.6bn (2023/24). Tighter efficiency and performance incentives in determinations can shift value from shareholders to customers, while proactive engagement and outperformance recover incentives and reputational capital.

Sewage spill scrutiny

National focus on storm overflows—highlighted by analyses showing about 400,000 discharges in England in recent years—raises expectations for faster pollution reduction. Ministers and MPs are pressing regulators to demand stricter penalties and tighter timelines, and public inquiries and select committees are already shaping near‑term spending priorities. This increases pressure on United Utilities for credible delivery plans and transparent, frequent reporting.

Infrastructure policy

Government support for critical infrastructure can unlock larger capital programmes for United Utilities, which serves about 7 million customers in the North West; planning reforms and regional growth agendas directly affect reservoir, pipeline and treatment upgrades. Political backing for nature‑based solutions may unlock grants or partnerships tied to the UKs £5.2bn flood‑defence commitment (2021–27). However, post‑election policy shifts can quickly alter funding certainty.

Public ownership debate

Periodic calls for renationalisation and tighter public control fuel strategic uncertainty for United Utilities, which supplies water to about 7 million customers in the North West and faces the PR24 regime (Ofwat, Dec 2023) that raises environmental and performance standards. Even without ownership change, tougher mandates can compress returns; strong service reliability, environmental delivery and transparent governance disclosures help limit policy risk premiums.

- Customers served: ~7 million

- Regulator: Ofwat PR24 raised performance expectations (Dec 2023)

- Mitigation: reliability, environmental performance, governance disclosures

Devolution dynamics

United Utilities, serving about 7 million customers across the North West, must align catchment strategies with local and regional authorities such as Greater Manchester Combined Authority and Liverpool City Region, which control planning approvals and funding levers. Alignment with Northern priorities—jobs, resilience and environment—increases project acceptance, while shifting political coalitions can speed or stall major schemes. Community benefits and local procurement strengthen political goodwill and reduce approval friction.

- Regional footprint: North West, ~7 million customers

- Key stakeholders: GMCA, Liverpool City Region

- Priority alignment: jobs, resilience, environment

- Political risk: coalition changes can accelerate or delay projects

PR24, storm overflow penalties and RCV ≈ £7.6bn reshape water spending

Ofwat’s PR24 (2025–30) sets allowed revenues and tougher incentives that directly shape United Utilities’ investment, customer bills and returns; RCV ~£7.6bn (2023/24). Public and ministerial pressure on storm overflows (≈400,000 discharges recently) raises penalties and faster delivery expectations. Government flood spend (£5.2bn, 2021–27) and regional planning influence project funding and timelines. Renationalisation talk and shifting coalitions increase policy uncertainty.

| Metric | Value |

|---|---|

| Customers | ~7,000,000 |

| Regulatory capital value | £7.6bn (2023/24) |

| Storm overflows | ≈400,000 discharges |

| PR24 period | 2025–2030 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect United Utilities Group, with data-driven trends and region-specific regulatory context. Designed to help executives and investors identify actionable risks, opportunities and scenario-driven strategies.

A concise, visually segmented PESTLE summary of United Utilities Group that’s easily dropped into presentations, edited with region- or business-specific notes, and shared across teams to speed risk discussions and strategic alignment during planning sessions.

Economic factors

Inflation linkage

Regulated asset values and allowed revenues for UK water firms, including United Utilities, are commonly indexed to inflation measures such as RPI/CPIH, giving partial protection against cost rises but tending to lift customer bills.

Mismatches between indexation and actual input-cost moves—notably the energy shocks of 2021–22 when European wholesale gas prices roughly doubled—create margin risk.

Effective hedging of energy and proactive procurement have been used to stabilise cash flows and mitigate volatility in recent years.

Interest rate exposure

Capital‑intensive utilities like United Utilities rely on substantial debt financing; with the Bank of England base rate at 5.25% and 10‑year UK gilt yields around 4.6% (July 2025), higher base rates and wider credit spreads raise borrowing costs and squeeze interest cover and FFO/debt ratios. Regulatory allowances can lag market moves, creating margin pressure, while prudent liability management and staggered maturities reduce refinancing volatility.

AMP8 capex cycle

The AMP8 2025–30 cycle drives elevated resilience and environmental capex, with the UK water sector targeting c.£55bn investment and United Utilities committing a multi‑hundred‑million pound programme for upgrades. Large programmes strain supply chains and delivery capacity, raising unit costs and schedule risk. Efficient execution can unlock PR24 incentive rewards and long‑term Opex savings, while poor delivery risks regulatory penalties and reputational damage, potentially costing firms hundreds of millions.

Energy and labor costs

Treatment and pumping are energy‑intensive, leaving United Utilities exposed to wholesale power swings; UK wholesale baseload averaged about £55/MWh in 2024, pressuring margins. Tight UK labour markets (unemployment ~4.0% in 2024) and need for specialist engineers drive wage inflation. Onsite generation and long‑term power contracts, plus a target of net‑zero operational emissions by 2030, reduce volatility, while workforce planning and automation curb cost pressure.

- Energy exposure: high (treatment, pumping)

- Wholesale price (2024): ~£55/MWh

- Labour tightness (2024): unemployment ~4.0%

- Mitigants: onsite generation, long‑term contracts, net‑zero 2030

- Cost control: workforce planning, automation

Customer affordability

Household income stress reduces bill headroom and raises bad‑debt risk, forcing United Utilities to expand affordability programs and social tariffs to sustain collections and regulatory compliance. Regulators factor affordability into price settlements, while clear communication of service value supports customer acceptance of necessary investment and resilience measures.

- Household stress increases bad‑debt exposure

- Affordability schemes sustain payment rates

- Regulators embed affordability in price reviews

- Value communication aids investment acceptance

PR24, storm overflow penalties and RCV ≈ £7.6bn reshape water spending

United Utilities faces inflation‑linked allowed revenues that partially offset cost rises, but RPI/CPIH lag and energy shocks (2021–22) created margin risk. Higher rates (Bank Rate 5.25%, 10y gilt ~4.6% Jul 2025) and AMP8 capex (UK water c.£55bn 2025–30) raise financing and delivery costs. Wholesale power ~£55/MWh (2024) and unemployment ~4.0% squeeze margins; mitigants include onsite generation, long‑term contracts and net‑zero 2030 targets.

| Metric | Value |

|---|---|

| Bank Rate (Jul 2025) | 5.25% |

| 10y UK gilt (Jul 2025) | ~4.6% |

| Wholesale power (2024) | ~£55/MWh |

| Unemployment (2024) | ~4.0% |

| UK water capex (AMP8 2025–30) | c.£55bn |

Full Version Awaits

United Utilities Group PESTLE Analysis

The preview shown here is the exact United Utilities Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It includes comprehensive Political, Economic, Social, Technological, Legal and Environmental evaluations with charts and citations. No placeholders or edits are needed; what you see is the final downloadable file.