Universal Logistics Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

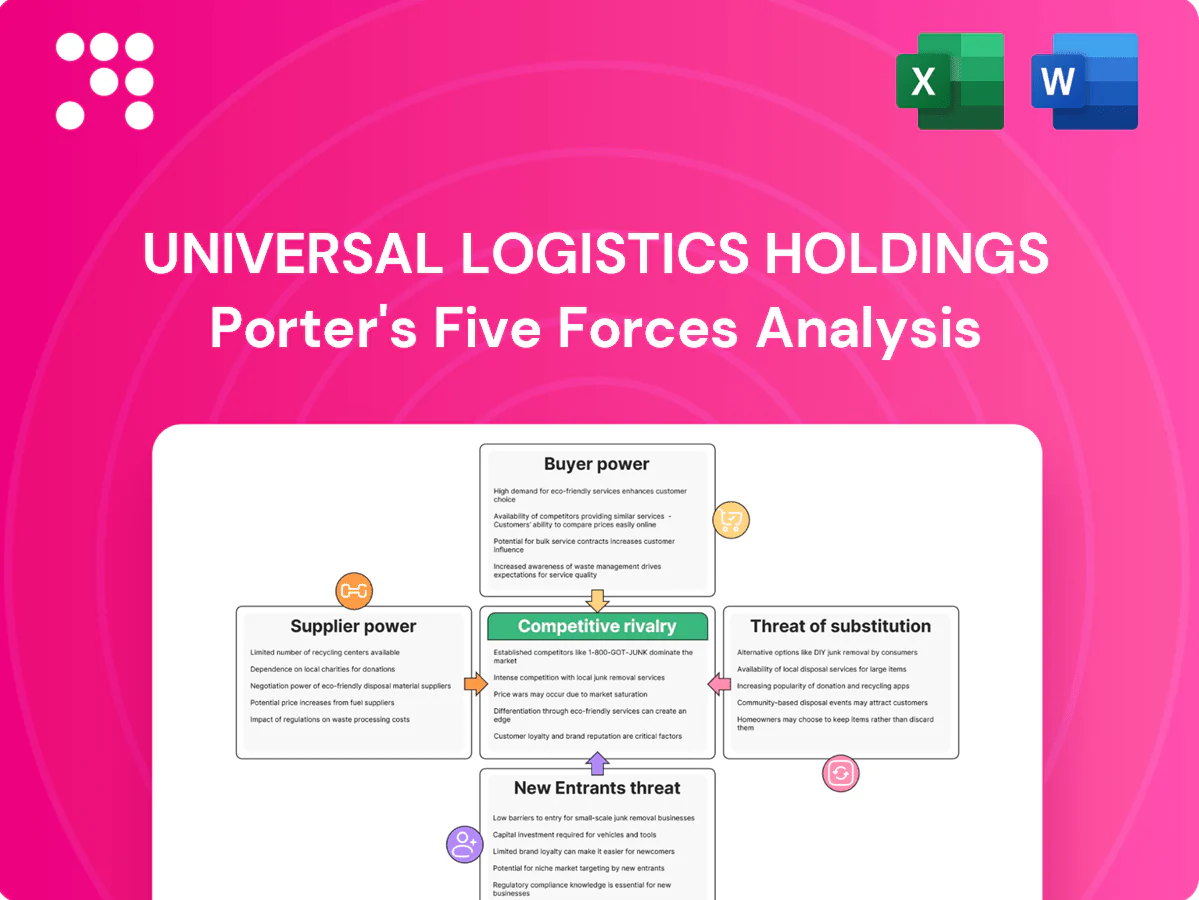

Universal Logistics Holdings faces moderate buyer power, fragmented supplier leverage, and rising competitive pressure from asset-light carriers, with potential threats from new entrants and technological substitutes shaping margins. This snapshot highlights key forces but omits force-by-force ratings, visuals, and strategic implications. Unlock the full Porter's Five Forces Analysis to access consultant-grade insights, data-driven ratings, and tailored recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Fragmented carrier base limits leverage

Universal’s asset-light model taps thousands of small trucking firms, drayage operators, and owner-operators—limiting any single supplier’s influence and aligning with ATA data showing 97% of US carriers operate 20 or fewer trucks. Brokerage networks enable quick switching among carriers, reducing dependency. Tight capacity cycles can temporarily push spot rates higher, while long-standing relationships and volume commitments stabilize contract terms.

Railroads and ports exert structural power

Intermodal depends on a concentrated supplier set—seven North American Class I railroads and a handful of major ports—giving those carriers pricing and service leverage. Access constraints, schedule changes and terminal surcharges can materially compress margins and disrupt reliability. Universal offsets risk with multi-rail exposure and lane diversification across key gateways. Despite mitigation, rail/port suppliers retain higher bargaining power than fragmented trucking.

Equipment and fuel suppliers influence costs

Equipment vendors for trailers, chassis and MHE can tighten availability and push up prices during shortage cycles, while fuel providers and card programs largely pass market volatility through to carriers with limited leverage beyond volume discounts; fuel surcharge mechanisms commonly recoup part of diesel cost swings, and proactive procurement and maintenance partnerships help Universal Logistics blunt supply shocks and stabilize operating costs.

Warehouse real estate and labor providers matter

Warehouse real estate and labor providers strongly influence Universal Logistics’ costs; port- and urban-adjacent industrial vacancy dipped under 3% in many US gateway markets in 2024, giving landlords pricing power, while tight markets pushed temporary staffing premiums roughly 20–30% above permanent wages in 2024. 3PL subleases and third-party facilities provide stopgap capacity but can be pricier in peaks; multi-site sourcing, flexible lease terms, automation and cross-training cut exposure to high-cost labor.

- Third-party facilities: rapid capacity, often higher per-square-foot cost

- 3PL subleases: short-term relief, limited supply in 2024

- Temp agencies: ~20–30% premium vs permanent staff in 2024

- Mitigants: multi-site options, flexible terms, automation, cross-training

Technology platforms create switching frictions

Technology platforms (TMS, visibility and telematics) create switching frictions at Universal Logistics by locking integrations and forming data moats; the TMS market reached about $3.1B in 2024, reinforcing vendor leverage. While alternatives exist, migration costs and operational disruption give key providers pricing power. Negotiating modular contracts and open APIs reduces dependency; building internal data layers preserves flexibility and bargaining position.

- lock-in: integrations & data moats

- 2024 TMS market ≈ $3.1B

- modular contracts + APIs

- internal data layer = bargaining power

Fragmented trucking (97% ≤20 trucks) cedes power to 7 Class I rail/ports; vacancy <3%

Trucking fragmentation limits supplier power (97% of US carriers operate ≤20 trucks), while seven Class I railroads and major ports exert higher leverage. Gateway industrial vacancy <3% in 2024 and temp labor premiums ~20–30% boost landlord/labor bargaining power. TMS market ≈$3.1B in 2024 creates moderate tech lock-in mitigants: multi-rail lanes, flexible leases, APIs.

| Supplier | 2024 metric / power |

|---|---|

| Trucking | 97% ≤20 trucks / Low |

| Rail/Ports | 7 Class I / High |

| Real estate/labor | Vacancy <3% / High |

| Tech (TMS) | $3.1B market / Moderate |

What is included in the product

Tailored Porter’s Five Forces analysis for Universal Logistics Holdings examining competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, plus disruptive risks and strategic levers affecting pricing and profitability.

A single-sheet Porter's Five Forces for Universal Logistics Holdings—clarifies competitive pressures, supplier/customer leverage, and regulatory threats so executives can make fast, confident strategic decisions.

Customers Bargaining Power

Diverse but procurement-savvy clientele

Customers across manufacturing, retail and energy centralize logistics via RFPs, driving price pressure as the global 3PL market reached about $1.4 trillion in 2024 (Armstrong & Associates); large shippers routinely benchmark across multiple 3PLs and carriers. Universal’s customized solutions and KPI-driven performance enable premium pricing versus spot rates. Buyers still wield leverage through multi-sourcing and lane-by-lane awards, keeping margins tight.

Contracted volumes vs spot optionality

Contracted volumes give Universal Logistics visibility and baseline revenue, yet shippers keep spot channels to arbitrage during soft capacity periods. Take-or-pay clauses and service-level credits align incentives but remain negotiable and erode margins under strong buyer leverage. Universal raises stickiness by bundling brokerage, dedicated fleets and warehousing, while customers press for rate indexing and fuel-surcharge transparency to strengthen their bargaining power.

Switching costs vary by integration depth

Basic brokerage lanes are routinely rebid on 30–90 day cycles, elevating buyer power and price sensitivity. Dedicated, warehousing and value-added services typically use multi-year contracts (average 3–5 years), integrating systems and workflows and raising switching costs. Co-designed solutions and on-site operations embed Universal deeper, and more integrated offerings cut practical customer leverage, with dedicated-account retention commonly above 85%.

Service quality and resilience expectations

- OTIF benchmark: 95% (2024)

- Visibility + recovery plans = performance contracts

- Reliability reduces price-only bargaining

Industry cycles reshape leverage

Industry cycles reshape buyer leverage: freight downturns create excess capacity that amplifies customer power and compresses margins; DAT Freight Index shows spot truckload rates down about 30% from 2022 peaks by 2024. In tight markets service assurance reduces bargaining; Universal can use dynamic pricing and broad capacity access while its multimodal, multi‑region portfolio smooths buyer leverage swings.

- Downturns: excess capacity → higher buyer power

- Tight markets: service assurance tempers leverage

- Actions: dynamic pricing, capacity access

- Portfolio: multimodal/regional diversity reduces cycle exposure

3PL $1.4T market, OTIF 95%: RFPs pressure rates, spot down ~30%, 85%+ retention

Large shippers centralize via RFPs creating price pressure despite Universal’s KPI-driven premium; global 3PL market ~$1.4T (2024) and OTIF demand ~95% raise performance stakes. Spot rates fell ~30% from 2022 peaks (DAT, 2024), boosting buyer leverage; multi-year contracts (avg 3–5 yrs) and 85%+ dedicated-account retention limit switching.

| Metric | 2024 |

|---|---|

| 3PL market | $1.4T |

| OTIF | 95% |

| Spot decline (truckload) | -30% |

| Dedicated retention | 85%+ |

Full Version Awaits

Universal Logistics Holdings Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Universal Logistics Holdings is the exact, fully formatted document you see in the preview—no placeholders or mockups. Upon purchase you’ll receive this same file instantly, ready for download and immediate use. The report provides a complete assessment of competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and strategic implications for stakeholders.

Don't Miss the Bigger Picture

Universal Logistics Holdings faces moderate buyer power, fragmented supplier leverage, and rising competitive pressure from asset-light carriers, with potential threats from new entrants and technological substitutes shaping margins. This snapshot highlights key forces but omits force-by-force ratings, visuals, and strategic implications. Unlock the full Porter's Five Forces Analysis to access consultant-grade insights, data-driven ratings, and tailored recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Fragmented carrier base limits leverage

Universal’s asset-light model taps thousands of small trucking firms, drayage operators, and owner-operators—limiting any single supplier’s influence and aligning with ATA data showing 97% of US carriers operate 20 or fewer trucks. Brokerage networks enable quick switching among carriers, reducing dependency. Tight capacity cycles can temporarily push spot rates higher, while long-standing relationships and volume commitments stabilize contract terms.

Railroads and ports exert structural power

Intermodal depends on a concentrated supplier set—seven North American Class I railroads and a handful of major ports—giving those carriers pricing and service leverage. Access constraints, schedule changes and terminal surcharges can materially compress margins and disrupt reliability. Universal offsets risk with multi-rail exposure and lane diversification across key gateways. Despite mitigation, rail/port suppliers retain higher bargaining power than fragmented trucking.

Equipment and fuel suppliers influence costs

Equipment vendors for trailers, chassis and MHE can tighten availability and push up prices during shortage cycles, while fuel providers and card programs largely pass market volatility through to carriers with limited leverage beyond volume discounts; fuel surcharge mechanisms commonly recoup part of diesel cost swings, and proactive procurement and maintenance partnerships help Universal Logistics blunt supply shocks and stabilize operating costs.

Warehouse real estate and labor providers matter

Warehouse real estate and labor providers strongly influence Universal Logistics’ costs; port- and urban-adjacent industrial vacancy dipped under 3% in many US gateway markets in 2024, giving landlords pricing power, while tight markets pushed temporary staffing premiums roughly 20–30% above permanent wages in 2024. 3PL subleases and third-party facilities provide stopgap capacity but can be pricier in peaks; multi-site sourcing, flexible lease terms, automation and cross-training cut exposure to high-cost labor.

- Third-party facilities: rapid capacity, often higher per-square-foot cost

- 3PL subleases: short-term relief, limited supply in 2024

- Temp agencies: ~20–30% premium vs permanent staff in 2024

- Mitigants: multi-site options, flexible terms, automation, cross-training

Technology platforms create switching frictions

Technology platforms (TMS, visibility and telematics) create switching frictions at Universal Logistics by locking integrations and forming data moats; the TMS market reached about $3.1B in 2024, reinforcing vendor leverage. While alternatives exist, migration costs and operational disruption give key providers pricing power. Negotiating modular contracts and open APIs reduces dependency; building internal data layers preserves flexibility and bargaining position.

- lock-in: integrations & data moats

- 2024 TMS market ≈ $3.1B

- modular contracts + APIs

- internal data layer = bargaining power

Fragmented trucking (97% ≤20 trucks) cedes power to 7 Class I rail/ports; vacancy <3%

Trucking fragmentation limits supplier power (97% of US carriers operate ≤20 trucks), while seven Class I railroads and major ports exert higher leverage. Gateway industrial vacancy <3% in 2024 and temp labor premiums ~20–30% boost landlord/labor bargaining power. TMS market ≈$3.1B in 2024 creates moderate tech lock-in mitigants: multi-rail lanes, flexible leases, APIs.

| Supplier | 2024 metric / power |

|---|---|

| Trucking | 97% ≤20 trucks / Low |

| Rail/Ports | 7 Class I / High |

| Real estate/labor | Vacancy <3% / High |

| Tech (TMS) | $3.1B market / Moderate |

What is included in the product

Tailored Porter’s Five Forces analysis for Universal Logistics Holdings examining competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, plus disruptive risks and strategic levers affecting pricing and profitability.

A single-sheet Porter's Five Forces for Universal Logistics Holdings—clarifies competitive pressures, supplier/customer leverage, and regulatory threats so executives can make fast, confident strategic decisions.

Customers Bargaining Power

Diverse but procurement-savvy clientele

Customers across manufacturing, retail and energy centralize logistics via RFPs, driving price pressure as the global 3PL market reached about $1.4 trillion in 2024 (Armstrong & Associates); large shippers routinely benchmark across multiple 3PLs and carriers. Universal’s customized solutions and KPI-driven performance enable premium pricing versus spot rates. Buyers still wield leverage through multi-sourcing and lane-by-lane awards, keeping margins tight.

Contracted volumes vs spot optionality

Contracted volumes give Universal Logistics visibility and baseline revenue, yet shippers keep spot channels to arbitrage during soft capacity periods. Take-or-pay clauses and service-level credits align incentives but remain negotiable and erode margins under strong buyer leverage. Universal raises stickiness by bundling brokerage, dedicated fleets and warehousing, while customers press for rate indexing and fuel-surcharge transparency to strengthen their bargaining power.

Switching costs vary by integration depth

Basic brokerage lanes are routinely rebid on 30–90 day cycles, elevating buyer power and price sensitivity. Dedicated, warehousing and value-added services typically use multi-year contracts (average 3–5 years), integrating systems and workflows and raising switching costs. Co-designed solutions and on-site operations embed Universal deeper, and more integrated offerings cut practical customer leverage, with dedicated-account retention commonly above 85%.

Service quality and resilience expectations

- OTIF benchmark: 95% (2024)

- Visibility + recovery plans = performance contracts

- Reliability reduces price-only bargaining

Industry cycles reshape leverage

Industry cycles reshape buyer leverage: freight downturns create excess capacity that amplifies customer power and compresses margins; DAT Freight Index shows spot truckload rates down about 30% from 2022 peaks by 2024. In tight markets service assurance reduces bargaining; Universal can use dynamic pricing and broad capacity access while its multimodal, multi‑region portfolio smooths buyer leverage swings.

- Downturns: excess capacity → higher buyer power

- Tight markets: service assurance tempers leverage

- Actions: dynamic pricing, capacity access

- Portfolio: multimodal/regional diversity reduces cycle exposure

3PL $1.4T market, OTIF 95%: RFPs pressure rates, spot down ~30%, 85%+ retention

Large shippers centralize via RFPs creating price pressure despite Universal’s KPI-driven premium; global 3PL market ~$1.4T (2024) and OTIF demand ~95% raise performance stakes. Spot rates fell ~30% from 2022 peaks (DAT, 2024), boosting buyer leverage; multi-year contracts (avg 3–5 yrs) and 85%+ dedicated-account retention limit switching.

| Metric | 2024 |

|---|---|

| 3PL market | $1.4T |

| OTIF | 95% |

| Spot decline (truckload) | -30% |

| Dedicated retention | 85%+ |

Full Version Awaits

Universal Logistics Holdings Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Universal Logistics Holdings is the exact, fully formatted document you see in the preview—no placeholders or mockups. Upon purchase you’ll receive this same file instantly, ready for download and immediate use. The report provides a complete assessment of competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and strategic implications for stakeholders.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Universal Logistics Holdings faces moderate buyer power, fragmented supplier leverage, and rising competitive pressure from asset-light carriers, with potential threats from new entrants and technological substitutes shaping margins. This snapshot highlights key forces but omits force-by-force ratings, visuals, and strategic implications. Unlock the full Porter's Five Forces Analysis to access consultant-grade insights, data-driven ratings, and tailored recommendations for investment or strategy decisions.

Suppliers Bargaining Power

Fragmented carrier base limits leverage

Universal’s asset-light model taps thousands of small trucking firms, drayage operators, and owner-operators—limiting any single supplier’s influence and aligning with ATA data showing 97% of US carriers operate 20 or fewer trucks. Brokerage networks enable quick switching among carriers, reducing dependency. Tight capacity cycles can temporarily push spot rates higher, while long-standing relationships and volume commitments stabilize contract terms.

Railroads and ports exert structural power

Intermodal depends on a concentrated supplier set—seven North American Class I railroads and a handful of major ports—giving those carriers pricing and service leverage. Access constraints, schedule changes and terminal surcharges can materially compress margins and disrupt reliability. Universal offsets risk with multi-rail exposure and lane diversification across key gateways. Despite mitigation, rail/port suppliers retain higher bargaining power than fragmented trucking.

Equipment and fuel suppliers influence costs

Equipment vendors for trailers, chassis and MHE can tighten availability and push up prices during shortage cycles, while fuel providers and card programs largely pass market volatility through to carriers with limited leverage beyond volume discounts; fuel surcharge mechanisms commonly recoup part of diesel cost swings, and proactive procurement and maintenance partnerships help Universal Logistics blunt supply shocks and stabilize operating costs.

Warehouse real estate and labor providers matter

Warehouse real estate and labor providers strongly influence Universal Logistics’ costs; port- and urban-adjacent industrial vacancy dipped under 3% in many US gateway markets in 2024, giving landlords pricing power, while tight markets pushed temporary staffing premiums roughly 20–30% above permanent wages in 2024. 3PL subleases and third-party facilities provide stopgap capacity but can be pricier in peaks; multi-site sourcing, flexible lease terms, automation and cross-training cut exposure to high-cost labor.

- Third-party facilities: rapid capacity, often higher per-square-foot cost

- 3PL subleases: short-term relief, limited supply in 2024

- Temp agencies: ~20–30% premium vs permanent staff in 2024

- Mitigants: multi-site options, flexible terms, automation, cross-training

Technology platforms create switching frictions

Technology platforms (TMS, visibility and telematics) create switching frictions at Universal Logistics by locking integrations and forming data moats; the TMS market reached about $3.1B in 2024, reinforcing vendor leverage. While alternatives exist, migration costs and operational disruption give key providers pricing power. Negotiating modular contracts and open APIs reduces dependency; building internal data layers preserves flexibility and bargaining position.

- lock-in: integrations & data moats

- 2024 TMS market ≈ $3.1B

- modular contracts + APIs

- internal data layer = bargaining power

Fragmented trucking (97% ≤20 trucks) cedes power to 7 Class I rail/ports; vacancy <3%

Trucking fragmentation limits supplier power (97% of US carriers operate ≤20 trucks), while seven Class I railroads and major ports exert higher leverage. Gateway industrial vacancy <3% in 2024 and temp labor premiums ~20–30% boost landlord/labor bargaining power. TMS market ≈$3.1B in 2024 creates moderate tech lock-in mitigants: multi-rail lanes, flexible leases, APIs.

| Supplier | 2024 metric / power |

|---|---|

| Trucking | 97% ≤20 trucks / Low |

| Rail/Ports | 7 Class I / High |

| Real estate/labor | Vacancy <3% / High |

| Tech (TMS) | $3.1B market / Moderate |

What is included in the product

Tailored Porter’s Five Forces analysis for Universal Logistics Holdings examining competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, plus disruptive risks and strategic levers affecting pricing and profitability.

A single-sheet Porter's Five Forces for Universal Logistics Holdings—clarifies competitive pressures, supplier/customer leverage, and regulatory threats so executives can make fast, confident strategic decisions.

Customers Bargaining Power

Diverse but procurement-savvy clientele

Customers across manufacturing, retail and energy centralize logistics via RFPs, driving price pressure as the global 3PL market reached about $1.4 trillion in 2024 (Armstrong & Associates); large shippers routinely benchmark across multiple 3PLs and carriers. Universal’s customized solutions and KPI-driven performance enable premium pricing versus spot rates. Buyers still wield leverage through multi-sourcing and lane-by-lane awards, keeping margins tight.

Contracted volumes vs spot optionality

Contracted volumes give Universal Logistics visibility and baseline revenue, yet shippers keep spot channels to arbitrage during soft capacity periods. Take-or-pay clauses and service-level credits align incentives but remain negotiable and erode margins under strong buyer leverage. Universal raises stickiness by bundling brokerage, dedicated fleets and warehousing, while customers press for rate indexing and fuel-surcharge transparency to strengthen their bargaining power.

Switching costs vary by integration depth

Basic brokerage lanes are routinely rebid on 30–90 day cycles, elevating buyer power and price sensitivity. Dedicated, warehousing and value-added services typically use multi-year contracts (average 3–5 years), integrating systems and workflows and raising switching costs. Co-designed solutions and on-site operations embed Universal deeper, and more integrated offerings cut practical customer leverage, with dedicated-account retention commonly above 85%.

Service quality and resilience expectations

- OTIF benchmark: 95% (2024)

- Visibility + recovery plans = performance contracts

- Reliability reduces price-only bargaining

Industry cycles reshape leverage

Industry cycles reshape buyer leverage: freight downturns create excess capacity that amplifies customer power and compresses margins; DAT Freight Index shows spot truckload rates down about 30% from 2022 peaks by 2024. In tight markets service assurance reduces bargaining; Universal can use dynamic pricing and broad capacity access while its multimodal, multi‑region portfolio smooths buyer leverage swings.

- Downturns: excess capacity → higher buyer power

- Tight markets: service assurance tempers leverage

- Actions: dynamic pricing, capacity access

- Portfolio: multimodal/regional diversity reduces cycle exposure

3PL $1.4T market, OTIF 95%: RFPs pressure rates, spot down ~30%, 85%+ retention

Large shippers centralize via RFPs creating price pressure despite Universal’s KPI-driven premium; global 3PL market ~$1.4T (2024) and OTIF demand ~95% raise performance stakes. Spot rates fell ~30% from 2022 peaks (DAT, 2024), boosting buyer leverage; multi-year contracts (avg 3–5 yrs) and 85%+ dedicated-account retention limit switching.

| Metric | 2024 |

|---|---|

| 3PL market | $1.4T |

| OTIF | 95% |

| Spot decline (truckload) | -30% |

| Dedicated retention | 85%+ |

Full Version Awaits

Universal Logistics Holdings Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Universal Logistics Holdings is the exact, fully formatted document you see in the preview—no placeholders or mockups. Upon purchase you’ll receive this same file instantly, ready for download and immediate use. The report provides a complete assessment of competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and strategic implications for stakeholders.