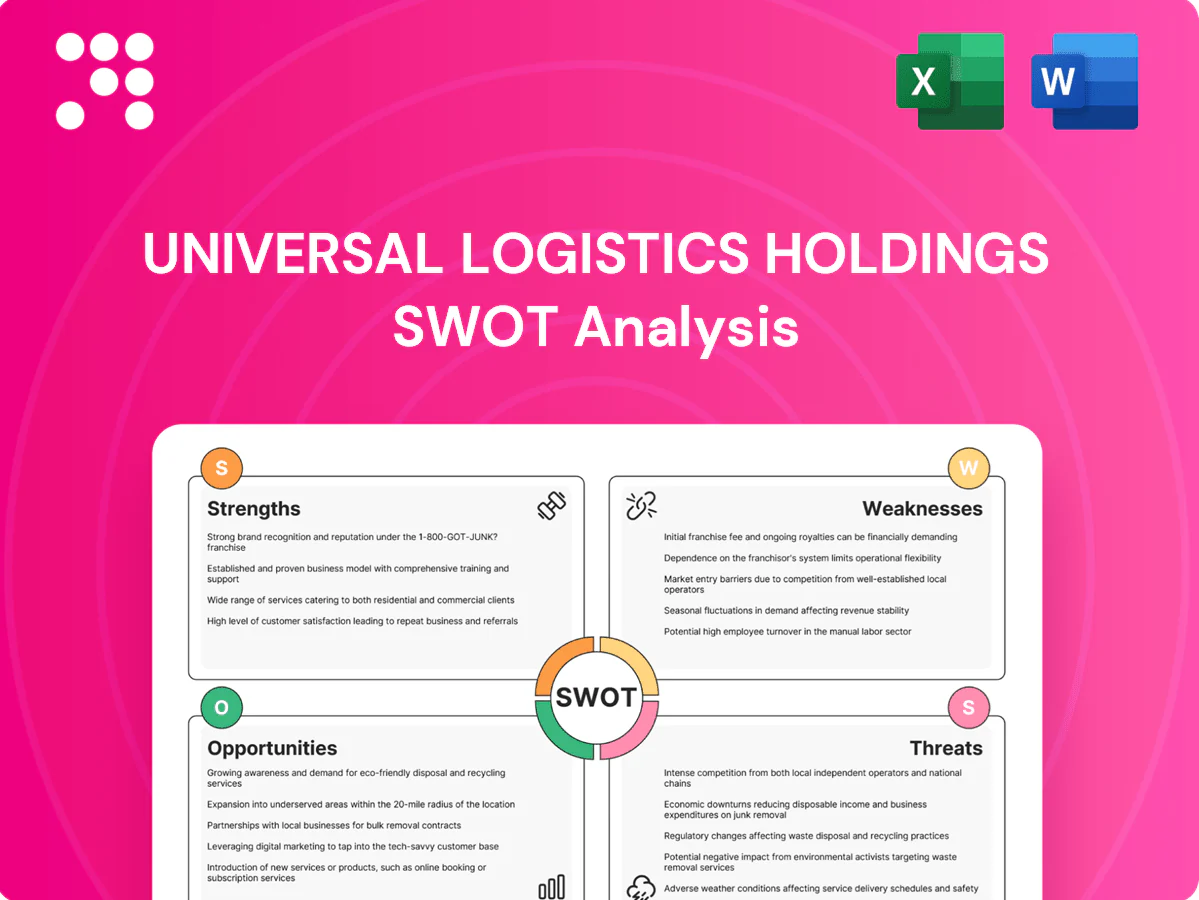

Universal Logistics Holdings SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Universal Logistics Holdings shows operational scale and diversified logistics services but faces margin pressure from fuel costs and driver shortages; growth hinges on tech adoption and strategic partnerships. Want the full picture—purchase the complete SWOT analysis for a research-backed, editable Word and Excel package with tactical recommendations and financial context to inform investment or strategy decisions.

Strengths

Diversified end-to-end service portfolio

Universal Logistics (NASDAQ: ULH) spans truckload, LTL, intermodal, brokerage and dedicated carriage plus warehousing and fulfillment, enabling true one-stop solutions and higher wallet share. This breadth smooths revenue volatility by balancing modes and industries and supports cross-selling that boosts customer stickiness and lifetime value. The integrated offering drives deeper penetration of existing accounts and more resilient revenue streams.

Asset-light model with scalable flexibility

Asset-light mix lowers capital intensity, enabling rapid capacity shifts and preserving ROIC through cycles; Universal Logistics Holdings reported $1.5B revenue in 2024, with asset-light services driving margin resilience. Variable cost structures cushion downturns and allow quick scaling into upturns. Partnerships and brokerage networks expand reach without heavy capex, enhancing scalable flexibility.

Integrated North American footprint

Operations across the U.S., Canada and Mexico give Universal Logistics seamless cross-border logistics, supporting customers’ nearshoring and regional supply chains as USMCA trade tops roughly 1.5 trillion USD annually; dense North American network boosts service reliability and lowers cost-to-serve, while in-house customs expertise cuts border friction and transit variability.

Customized solutions and dedicated capabilities

Engineered, customer‑specific solutions let Universal Logistics solve complex routing, warehousing and dedicated carriage challenges, strengthening client dependence. Dedicated contract carriage drives predictable service levels and long‑term contracts, raising switching costs through operational integration. Continuous performance data from dedicated ops fuels iterative improvements and defensibility.

- Customer‑specific engineering

- Predictable dedicated carriage

- Data‑driven continuous improvement

Value-added warehousing and fulfillment

Value-added warehousing, kitting, sequencing and fulfillment extend Universal beyond pure transport into in-plant and near-plant services that embed the company deeper in customer operations, boosting service stickiness and margin capture while opening cross-sell pathways versus brokers.

- Deeper operational integration

- Higher margin mix

- Cross-sell differentiation

Asset-light North America logistics platform, diversified services, $1.5B

Universal Logistics (NASDAQ: ULH) offers end-to-end transport and warehousing across truckload, LTL, intermodal, brokerage and dedicated carriage, enabling cross-sell, higher wallet share and revenue resilience. Its asset-light services support margin durability and rapid capacity shifts; reported revenue was $1.5B in 2024. North America coverage and engineered customer solutions raise switching costs and drive long-term contracts.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.5B |

| Ticker | NASDAQ: ULH |

| Geography | US, Canada, Mexico |

| Core Services | Truckload, LTL, Intermodal, Brokerage, Dedicated, Warehousing |

What is included in the product

Presents a concise SWOT analysis of Universal Logistics Holdings, highlighting internal strengths and weaknesses and external opportunities and threats that shape its competitive position and strategic outlook.

Provides a concise SWOT matrix tailored to Universal Logistics Holdings for rapid strategic alignment and clear resolution of operational pain points, enabling focused mitigation and opportunity capture.

Weaknesses

Exposure to cyclical freight demand

Freight volumes and spot rates for companies like Universal Logistics swing sharply with macro cycles and inventory restocking, with industry downturns historically cutting yields and utilization significantly (spot rate declines have exceeded 20% in past recessions). Customer budget cuts often delay or scale back projects, reducing contracted load volumes. Volatile markets make forecasting accuracy harder, increasing working capital and margin pressure.

Margin pressure in commoditized lanes

Brokerage and standard trucking face intense price-based competition, squeezing Universal Logistics Holdings margins as customers pivot to lowest-cost carriers; industry spot rates can swing more than 20% seasonally per DAT Freight Index trends. Spot rate volatility often outpaces contract repricing cadence, eroding take-rates when capacity loosens and excess truckload capacity rises. Differentiation remains difficult outside engineered or dedicated solutions, where higher-margin services and long-term contracts concentrate.

Customer and sector concentration risk

Universal Logistics faces customer and sector concentration risk, with automotive and a handful of large accounts driving outsized revenue and a single top shipper representing over 10% of sales; program losses or OEM production shutdowns can materially dent quarterly results. Pricing leverage skews to key shippers, and recent contract renegotiations have pressured rates and volumes for the carrier segment.

Scale disadvantage versus mega 3PLs

Scale disadvantage versus mega 3PLs: global integrators (DHL, UPS, FedEx) operate networks and tech budgets at scale, with combined 2024 revenues exceeding $200 billion, enabling price pressure and bundled offerings that Universal Logistics struggles to match; brand visibility and enterprise sales reach lag, making multinational RFP wins more difficult.

- Network reach: lower vs global leaders

- Pricing pressure: ability to bundle services

- Tech spend gap: limits digital scale

- RFPs: harder to win multinationals

Technology depth and data analytics gaps

Keeping pace with leading digital freight platforms requires sustained investment; Universal Logistics Holdings' legacy systems inhibit real-time visibility and automation, raising operating costs and error rates while constraining advanced yield management and dynamic pricing capabilities.

- Legacy IT limits real-time visibility

- Higher operating costs and error rates

- Reduced dynamic pricing and yield management

- Need for sustained capex and tech hiring

Logistics operator: spot volatility > 20%, top shipper > 10%, scale gap

Universal Logistics faces high spot-rate volatility (>20%) and demand cyclicality that depress margins and utilization. Customer concentration is material with the largest shipper >10% of revenue, amplifying downside from account losses or OEM slowdowns. Scale and tech gaps versus global integrators (combined 2024 revenues >200 billion) limit pricing power and RFP wins.

| Metric | Value |

|---|---|

| Spot-rate volatility | >20% |

| Top shipper concentration | >10% of revenue |

| Global integrators combined revenue (2024) | >200 billion |

Same Document Delivered

Universal Logistics Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Universal Logistics Holdings' strengths, weaknesses, opportunities, and threats. Buy now to unlock the complete, editable version.

Elevate Your Analysis with the Complete SWOT Report

Universal Logistics Holdings shows operational scale and diversified logistics services but faces margin pressure from fuel costs and driver shortages; growth hinges on tech adoption and strategic partnerships. Want the full picture—purchase the complete SWOT analysis for a research-backed, editable Word and Excel package with tactical recommendations and financial context to inform investment or strategy decisions.

Strengths

Diversified end-to-end service portfolio

Universal Logistics (NASDAQ: ULH) spans truckload, LTL, intermodal, brokerage and dedicated carriage plus warehousing and fulfillment, enabling true one-stop solutions and higher wallet share. This breadth smooths revenue volatility by balancing modes and industries and supports cross-selling that boosts customer stickiness and lifetime value. The integrated offering drives deeper penetration of existing accounts and more resilient revenue streams.

Asset-light model with scalable flexibility

Asset-light mix lowers capital intensity, enabling rapid capacity shifts and preserving ROIC through cycles; Universal Logistics Holdings reported $1.5B revenue in 2024, with asset-light services driving margin resilience. Variable cost structures cushion downturns and allow quick scaling into upturns. Partnerships and brokerage networks expand reach without heavy capex, enhancing scalable flexibility.

Integrated North American footprint

Operations across the U.S., Canada and Mexico give Universal Logistics seamless cross-border logistics, supporting customers’ nearshoring and regional supply chains as USMCA trade tops roughly 1.5 trillion USD annually; dense North American network boosts service reliability and lowers cost-to-serve, while in-house customs expertise cuts border friction and transit variability.

Customized solutions and dedicated capabilities

Engineered, customer‑specific solutions let Universal Logistics solve complex routing, warehousing and dedicated carriage challenges, strengthening client dependence. Dedicated contract carriage drives predictable service levels and long‑term contracts, raising switching costs through operational integration. Continuous performance data from dedicated ops fuels iterative improvements and defensibility.

- Customer‑specific engineering

- Predictable dedicated carriage

- Data‑driven continuous improvement

Value-added warehousing and fulfillment

Value-added warehousing, kitting, sequencing and fulfillment extend Universal beyond pure transport into in-plant and near-plant services that embed the company deeper in customer operations, boosting service stickiness and margin capture while opening cross-sell pathways versus brokers.

- Deeper operational integration

- Higher margin mix

- Cross-sell differentiation

Asset-light North America logistics platform, diversified services, $1.5B

Universal Logistics (NASDAQ: ULH) offers end-to-end transport and warehousing across truckload, LTL, intermodal, brokerage and dedicated carriage, enabling cross-sell, higher wallet share and revenue resilience. Its asset-light services support margin durability and rapid capacity shifts; reported revenue was $1.5B in 2024. North America coverage and engineered customer solutions raise switching costs and drive long-term contracts.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.5B |

| Ticker | NASDAQ: ULH |

| Geography | US, Canada, Mexico |

| Core Services | Truckload, LTL, Intermodal, Brokerage, Dedicated, Warehousing |

What is included in the product

Presents a concise SWOT analysis of Universal Logistics Holdings, highlighting internal strengths and weaknesses and external opportunities and threats that shape its competitive position and strategic outlook.

Provides a concise SWOT matrix tailored to Universal Logistics Holdings for rapid strategic alignment and clear resolution of operational pain points, enabling focused mitigation and opportunity capture.

Weaknesses

Exposure to cyclical freight demand

Freight volumes and spot rates for companies like Universal Logistics swing sharply with macro cycles and inventory restocking, with industry downturns historically cutting yields and utilization significantly (spot rate declines have exceeded 20% in past recessions). Customer budget cuts often delay or scale back projects, reducing contracted load volumes. Volatile markets make forecasting accuracy harder, increasing working capital and margin pressure.

Margin pressure in commoditized lanes

Brokerage and standard trucking face intense price-based competition, squeezing Universal Logistics Holdings margins as customers pivot to lowest-cost carriers; industry spot rates can swing more than 20% seasonally per DAT Freight Index trends. Spot rate volatility often outpaces contract repricing cadence, eroding take-rates when capacity loosens and excess truckload capacity rises. Differentiation remains difficult outside engineered or dedicated solutions, where higher-margin services and long-term contracts concentrate.

Customer and sector concentration risk

Universal Logistics faces customer and sector concentration risk, with automotive and a handful of large accounts driving outsized revenue and a single top shipper representing over 10% of sales; program losses or OEM production shutdowns can materially dent quarterly results. Pricing leverage skews to key shippers, and recent contract renegotiations have pressured rates and volumes for the carrier segment.

Scale disadvantage versus mega 3PLs

Scale disadvantage versus mega 3PLs: global integrators (DHL, UPS, FedEx) operate networks and tech budgets at scale, with combined 2024 revenues exceeding $200 billion, enabling price pressure and bundled offerings that Universal Logistics struggles to match; brand visibility and enterprise sales reach lag, making multinational RFP wins more difficult.

- Network reach: lower vs global leaders

- Pricing pressure: ability to bundle services

- Tech spend gap: limits digital scale

- RFPs: harder to win multinationals

Technology depth and data analytics gaps

Keeping pace with leading digital freight platforms requires sustained investment; Universal Logistics Holdings' legacy systems inhibit real-time visibility and automation, raising operating costs and error rates while constraining advanced yield management and dynamic pricing capabilities.

- Legacy IT limits real-time visibility

- Higher operating costs and error rates

- Reduced dynamic pricing and yield management

- Need for sustained capex and tech hiring

Logistics operator: spot volatility > 20%, top shipper > 10%, scale gap

Universal Logistics faces high spot-rate volatility (>20%) and demand cyclicality that depress margins and utilization. Customer concentration is material with the largest shipper >10% of revenue, amplifying downside from account losses or OEM slowdowns. Scale and tech gaps versus global integrators (combined 2024 revenues >200 billion) limit pricing power and RFP wins.

| Metric | Value |

|---|---|

| Spot-rate volatility | >20% |

| Top shipper concentration | >10% of revenue |

| Global integrators combined revenue (2024) | >200 billion |

Same Document Delivered

Universal Logistics Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Universal Logistics Holdings' strengths, weaknesses, opportunities, and threats. Buy now to unlock the complete, editable version.

Description

Elevate Your Analysis with the Complete SWOT Report

Universal Logistics Holdings shows operational scale and diversified logistics services but faces margin pressure from fuel costs and driver shortages; growth hinges on tech adoption and strategic partnerships. Want the full picture—purchase the complete SWOT analysis for a research-backed, editable Word and Excel package with tactical recommendations and financial context to inform investment or strategy decisions.

Strengths

Diversified end-to-end service portfolio

Universal Logistics (NASDAQ: ULH) spans truckload, LTL, intermodal, brokerage and dedicated carriage plus warehousing and fulfillment, enabling true one-stop solutions and higher wallet share. This breadth smooths revenue volatility by balancing modes and industries and supports cross-selling that boosts customer stickiness and lifetime value. The integrated offering drives deeper penetration of existing accounts and more resilient revenue streams.

Asset-light model with scalable flexibility

Asset-light mix lowers capital intensity, enabling rapid capacity shifts and preserving ROIC through cycles; Universal Logistics Holdings reported $1.5B revenue in 2024, with asset-light services driving margin resilience. Variable cost structures cushion downturns and allow quick scaling into upturns. Partnerships and brokerage networks expand reach without heavy capex, enhancing scalable flexibility.

Integrated North American footprint

Operations across the U.S., Canada and Mexico give Universal Logistics seamless cross-border logistics, supporting customers’ nearshoring and regional supply chains as USMCA trade tops roughly 1.5 trillion USD annually; dense North American network boosts service reliability and lowers cost-to-serve, while in-house customs expertise cuts border friction and transit variability.

Customized solutions and dedicated capabilities

Engineered, customer‑specific solutions let Universal Logistics solve complex routing, warehousing and dedicated carriage challenges, strengthening client dependence. Dedicated contract carriage drives predictable service levels and long‑term contracts, raising switching costs through operational integration. Continuous performance data from dedicated ops fuels iterative improvements and defensibility.

- Customer‑specific engineering

- Predictable dedicated carriage

- Data‑driven continuous improvement

Value-added warehousing and fulfillment

Value-added warehousing, kitting, sequencing and fulfillment extend Universal beyond pure transport into in-plant and near-plant services that embed the company deeper in customer operations, boosting service stickiness and margin capture while opening cross-sell pathways versus brokers.

- Deeper operational integration

- Higher margin mix

- Cross-sell differentiation

Asset-light North America logistics platform, diversified services, $1.5B

Universal Logistics (NASDAQ: ULH) offers end-to-end transport and warehousing across truckload, LTL, intermodal, brokerage and dedicated carriage, enabling cross-sell, higher wallet share and revenue resilience. Its asset-light services support margin durability and rapid capacity shifts; reported revenue was $1.5B in 2024. North America coverage and engineered customer solutions raise switching costs and drive long-term contracts.

| Metric | Value |

|---|---|

| 2024 Revenue | $1.5B |

| Ticker | NASDAQ: ULH |

| Geography | US, Canada, Mexico |

| Core Services | Truckload, LTL, Intermodal, Brokerage, Dedicated, Warehousing |

What is included in the product

Presents a concise SWOT analysis of Universal Logistics Holdings, highlighting internal strengths and weaknesses and external opportunities and threats that shape its competitive position and strategic outlook.

Provides a concise SWOT matrix tailored to Universal Logistics Holdings for rapid strategic alignment and clear resolution of operational pain points, enabling focused mitigation and opportunity capture.

Weaknesses

Exposure to cyclical freight demand

Freight volumes and spot rates for companies like Universal Logistics swing sharply with macro cycles and inventory restocking, with industry downturns historically cutting yields and utilization significantly (spot rate declines have exceeded 20% in past recessions). Customer budget cuts often delay or scale back projects, reducing contracted load volumes. Volatile markets make forecasting accuracy harder, increasing working capital and margin pressure.

Margin pressure in commoditized lanes

Brokerage and standard trucking face intense price-based competition, squeezing Universal Logistics Holdings margins as customers pivot to lowest-cost carriers; industry spot rates can swing more than 20% seasonally per DAT Freight Index trends. Spot rate volatility often outpaces contract repricing cadence, eroding take-rates when capacity loosens and excess truckload capacity rises. Differentiation remains difficult outside engineered or dedicated solutions, where higher-margin services and long-term contracts concentrate.

Customer and sector concentration risk

Universal Logistics faces customer and sector concentration risk, with automotive and a handful of large accounts driving outsized revenue and a single top shipper representing over 10% of sales; program losses or OEM production shutdowns can materially dent quarterly results. Pricing leverage skews to key shippers, and recent contract renegotiations have pressured rates and volumes for the carrier segment.

Scale disadvantage versus mega 3PLs

Scale disadvantage versus mega 3PLs: global integrators (DHL, UPS, FedEx) operate networks and tech budgets at scale, with combined 2024 revenues exceeding $200 billion, enabling price pressure and bundled offerings that Universal Logistics struggles to match; brand visibility and enterprise sales reach lag, making multinational RFP wins more difficult.

- Network reach: lower vs global leaders

- Pricing pressure: ability to bundle services

- Tech spend gap: limits digital scale

- RFPs: harder to win multinationals

Technology depth and data analytics gaps

Keeping pace with leading digital freight platforms requires sustained investment; Universal Logistics Holdings' legacy systems inhibit real-time visibility and automation, raising operating costs and error rates while constraining advanced yield management and dynamic pricing capabilities.

- Legacy IT limits real-time visibility

- Higher operating costs and error rates

- Reduced dynamic pricing and yield management

- Need for sustained capex and tech hiring

Logistics operator: spot volatility > 20%, top shipper > 10%, scale gap

Universal Logistics faces high spot-rate volatility (>20%) and demand cyclicality that depress margins and utilization. Customer concentration is material with the largest shipper >10% of revenue, amplifying downside from account losses or OEM slowdowns. Scale and tech gaps versus global integrators (combined 2024 revenues >200 billion) limit pricing power and RFP wins.

| Metric | Value |

|---|---|

| Spot-rate volatility | >20% |

| Top shipper concentration | >10% of revenue |

| Global integrators combined revenue (2024) | >200 billion |

Same Document Delivered

Universal Logistics Holdings SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering Universal Logistics Holdings' strengths, weaknesses, opportunities, and threats. Buy now to unlock the complete, editable version.