Upstart Business Model Canvas

Business Model Canvas: Actionable growth blueprint for investors, founders and analysts

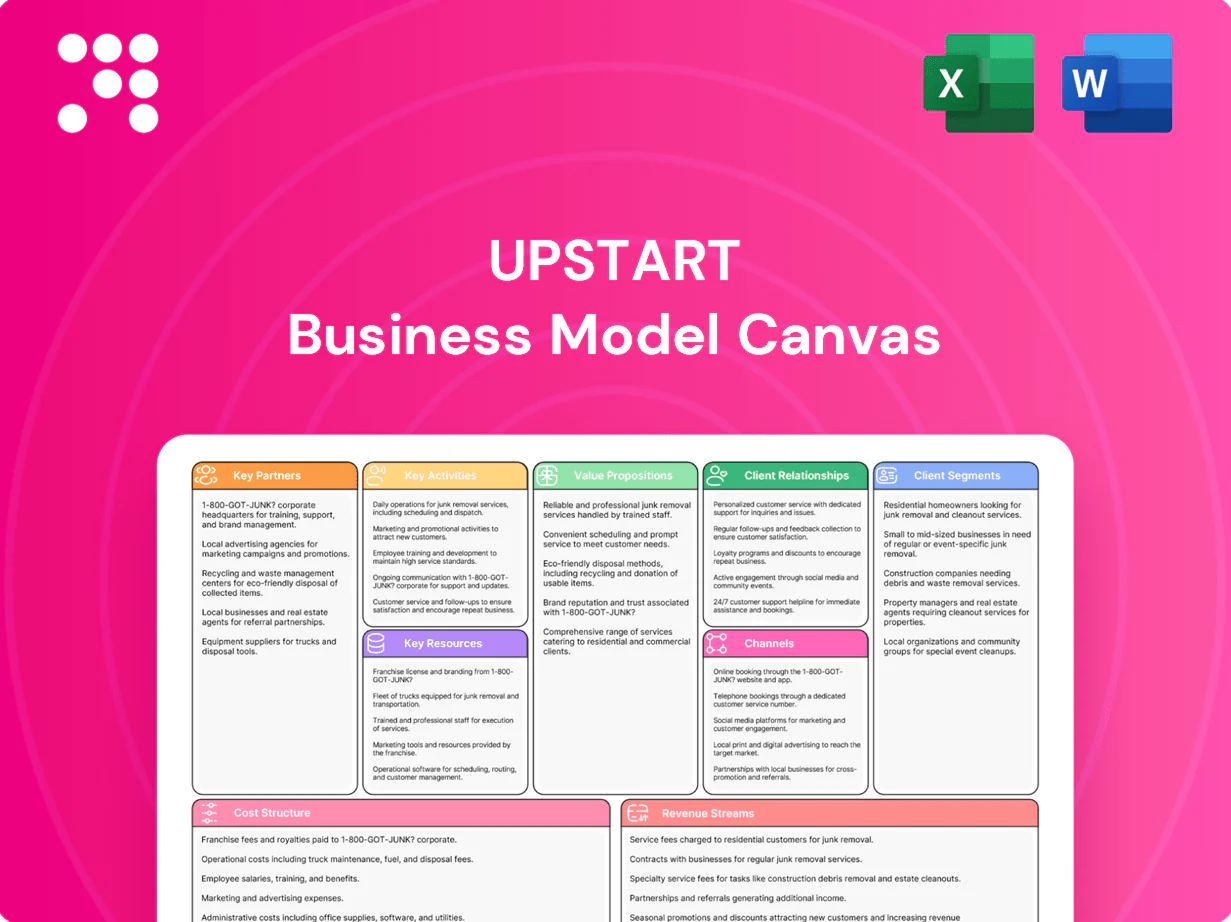

Unlock Upstart’s growth blueprint with our concise Business Model Canvas that maps value propositions, customer segments, revenue streams and competitive advantages. Perfect for investors, founders and analysts, it turns strategy into action. Download the full Word & Excel kit to benchmark, plan and scale confidently.

Partnerships

Banks and Credit Unions

Partner banks and credit unions originate loans using Upstart’s AI underwriting while supplying balance-sheet capacity and regulatory infrastructure, enabling rapid scaling. Co-branded programs align incentives and expand reach through partner distribution channels. Ongoing performance data from these originations feeds continuous model refinement and risk calibration.

Institutional Capital Providers

Institutional whole loan buyers and securitization partners supply funding at scale, enabling Upstart to convert originated loans into immediate liquidity. Forward flow agreements with banks and investors stabilize monthly volumes and warehouse utilization. Ongoing pricing feedback from these partners informs risk-based APRs and underwriting adjustments. A diversified capital base reduces funding costs and dampens rate volatility.

Data and Credit Bureaus

Access to credit files, alternative data and verification services enrich Upstart’s risk signals, improving model precision and borrower segmentation. Real-time feeds enable pre-qualification and fraud checks with sub-second responses and vendor SLAs targeting 99.9% uptime. Compliance-grade data lineage is retained via SOC 2 Type II and GLBA-aligned controls. Partners process millions of records daily to sustain model training and decisioning.

Regulatory and Compliance Advisors

Regulatory and compliance advisors guide Upstart on fair lending, model risk, and consumer protections, aligning policies with 2024 rule updates; independent validations and third-party audits materially lower regulatory exposure and support supervisory exams. Governance frameworks are revised as rules evolve and mandatory training embeds best practices across product, credit and analytics teams.

- Fair lending oversight — advisory alignment with 2024 guidance

- Independent validations — third-party audits reduce regulatory risk

- Governance updates — continuous rule-driven revisions

- Training — mandatory compliance and model-risk education for teams

Technology and Cloud Providers

Technology and cloud providers (AWS, Azure, GCP ~66% combined market share in 2024) supply cloud compute, MLOps tooling, and security vendors that power Upstart’s AI-first lending platform; APIs enable bank integrations and full KYC/AML workflows. Monitoring and observability deliver near 99.99% availability targets and sub-second API latency SLAs, while auto-scaling supports peak demand during lending cycles.

- Cloud compute: AWS/Azure/GCP (~66% 2024)

- MLOps: model deployment, CI/CD, feature stores

- Security: IAM, encryption, third-party vendors

- APIs: bank integrations, KYC/AML orchestration

- Reliability: monitoring, observability, 99.99% targets

- Scalability: auto-scaling for peak origination

Banks drive origination; investors add liquidity; cloud AI powers risk

Bank partners originate loans and provide balance-sheet/regulatory capacity; co-branded deals expand distribution and supply performance data for model tuning. Institutional buyers and securitizers provide liquidity via whole-loan purchases and forward flows, stabilizing volumes and pricing. Data, verification and cloud providers (AWS/Azure/GCP ~66% 2024) enable AI decisioning, uptime and real-time risk signals.

| Partner | Role | 2024 metric |

|---|---|---|

| Banks/credit unions | Origination, capital | ~60% originations via bank partners |

| Investors/securitizers | Funding/liquidity | Forward flows stabilizing monthly volume |

| Data/Cloud vendors | Signals+infra | AWS/Azure/GCP ~66% market share |

What is included in the product

Comprehensive Upstart Business Model Canvas mapping all 9 BMC blocks with clear value propositions, customer segments, channels and revenue streams. Designed for investors and analysts, it includes competitive advantages, SWOT-linked insights and real-company validation for presentations and strategic decisions.

High-level view of Upstart’s business model with editable cells that quickly surface core pain relievers—automated underwriting, partner distribution, and fee structure—so teams can diagnose value drivers and risks in minutes.

Activities

AI Model Development

Build and retrain credit, pricing, and fraud models using continual ingestion of borrower, bureau, and payment data; perform feature engineering and rigorous bias testing across demographics; run backtesting and challenger experiments to compare production models and quantify lift; govern models with comprehensive documentation, version control, monitoring, and controls to meet regulatory and audit requirements.

Loan Origination and Decisioning

Run pre-qualification, verification, and underwriting flows that automate identity, income, and employment checks to scale decisioning and reduce manual review. Upstart reports its AI historically enables roughly 27% higher approvals and up to 75% lower loss rates versus traditional credit-score-only models, while routing approvals to partner-specific criteria. Continuous tuning optimizes conversion while managing portfolio-level risk.

Risk and Compliance Management

Monitor portfolio performance and vintage curves continuously, execute fair lending analyses and documented underwriting overrides, and maintain model risk and data privacy policies in line with GLBA and SEC filing requirements.

Partner Onboarding and Integration

Customer Acquisition and Servicing

Upstart runs digital marketing and referral programs to scale borrower inflow, offers self-serve portals plus live support for applications and account management, and outsources payments, hardship programs and collections to partner servicers while tracking NPS and funnel KPIs to optimize conversion and credit outcomes.

- Digital marketing & referrals

- Self-serve portals & support

- Partner payments, hardship, collections

- NPS & funnel KPI measurement

Automate decisioning — ~27% approvals, up to 75% loss cuts

Build and retrain credit, pricing, and fraud models with continual data ingestion, feature engineering, bias testing, backtesting and governance; run automated pre-qualification, verification and underwriting flows to scale decisioning; monitor portfolio vintage curves, fair lending and model risk; onboard partners via API/LOS integrations, product design, SLAs and performance dashboards while scaling acquisition and servicing.

| Metric | Value |

|---|---|

| Approval lift vs FICO | ~27% |

| Loss reduction vs FICO | up to 75% |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Upstart Business Model Canvas you'll receive—it's not a mockup or teaser. When you purchase, you'll get this exact, fully editable file in the same format shown. It's ready for presentation, analysis, or modification with all sections included and no surprises.

Business Model Canvas: Actionable growth blueprint for investors, founders and analysts

Unlock Upstart’s growth blueprint with our concise Business Model Canvas that maps value propositions, customer segments, revenue streams and competitive advantages. Perfect for investors, founders and analysts, it turns strategy into action. Download the full Word & Excel kit to benchmark, plan and scale confidently.

Partnerships

Banks and Credit Unions

Partner banks and credit unions originate loans using Upstart’s AI underwriting while supplying balance-sheet capacity and regulatory infrastructure, enabling rapid scaling. Co-branded programs align incentives and expand reach through partner distribution channels. Ongoing performance data from these originations feeds continuous model refinement and risk calibration.

Institutional Capital Providers

Institutional whole loan buyers and securitization partners supply funding at scale, enabling Upstart to convert originated loans into immediate liquidity. Forward flow agreements with banks and investors stabilize monthly volumes and warehouse utilization. Ongoing pricing feedback from these partners informs risk-based APRs and underwriting adjustments. A diversified capital base reduces funding costs and dampens rate volatility.

Data and Credit Bureaus

Access to credit files, alternative data and verification services enrich Upstart’s risk signals, improving model precision and borrower segmentation. Real-time feeds enable pre-qualification and fraud checks with sub-second responses and vendor SLAs targeting 99.9% uptime. Compliance-grade data lineage is retained via SOC 2 Type II and GLBA-aligned controls. Partners process millions of records daily to sustain model training and decisioning.

Regulatory and Compliance Advisors

Regulatory and compliance advisors guide Upstart on fair lending, model risk, and consumer protections, aligning policies with 2024 rule updates; independent validations and third-party audits materially lower regulatory exposure and support supervisory exams. Governance frameworks are revised as rules evolve and mandatory training embeds best practices across product, credit and analytics teams.

- Fair lending oversight — advisory alignment with 2024 guidance

- Independent validations — third-party audits reduce regulatory risk

- Governance updates — continuous rule-driven revisions

- Training — mandatory compliance and model-risk education for teams

Technology and Cloud Providers

Technology and cloud providers (AWS, Azure, GCP ~66% combined market share in 2024) supply cloud compute, MLOps tooling, and security vendors that power Upstart’s AI-first lending platform; APIs enable bank integrations and full KYC/AML workflows. Monitoring and observability deliver near 99.99% availability targets and sub-second API latency SLAs, while auto-scaling supports peak demand during lending cycles.

- Cloud compute: AWS/Azure/GCP (~66% 2024)

- MLOps: model deployment, CI/CD, feature stores

- Security: IAM, encryption, third-party vendors

- APIs: bank integrations, KYC/AML orchestration

- Reliability: monitoring, observability, 99.99% targets

- Scalability: auto-scaling for peak origination

Banks drive origination; investors add liquidity; cloud AI powers risk

Bank partners originate loans and provide balance-sheet/regulatory capacity; co-branded deals expand distribution and supply performance data for model tuning. Institutional buyers and securitizers provide liquidity via whole-loan purchases and forward flows, stabilizing volumes and pricing. Data, verification and cloud providers (AWS/Azure/GCP ~66% 2024) enable AI decisioning, uptime and real-time risk signals.

| Partner | Role | 2024 metric |

|---|---|---|

| Banks/credit unions | Origination, capital | ~60% originations via bank partners |

| Investors/securitizers | Funding/liquidity | Forward flows stabilizing monthly volume |

| Data/Cloud vendors | Signals+infra | AWS/Azure/GCP ~66% market share |

What is included in the product

Comprehensive Upstart Business Model Canvas mapping all 9 BMC blocks with clear value propositions, customer segments, channels and revenue streams. Designed for investors and analysts, it includes competitive advantages, SWOT-linked insights and real-company validation for presentations and strategic decisions.

High-level view of Upstart’s business model with editable cells that quickly surface core pain relievers—automated underwriting, partner distribution, and fee structure—so teams can diagnose value drivers and risks in minutes.

Activities

AI Model Development

Build and retrain credit, pricing, and fraud models using continual ingestion of borrower, bureau, and payment data; perform feature engineering and rigorous bias testing across demographics; run backtesting and challenger experiments to compare production models and quantify lift; govern models with comprehensive documentation, version control, monitoring, and controls to meet regulatory and audit requirements.

Loan Origination and Decisioning

Run pre-qualification, verification, and underwriting flows that automate identity, income, and employment checks to scale decisioning and reduce manual review. Upstart reports its AI historically enables roughly 27% higher approvals and up to 75% lower loss rates versus traditional credit-score-only models, while routing approvals to partner-specific criteria. Continuous tuning optimizes conversion while managing portfolio-level risk.

Risk and Compliance Management

Monitor portfolio performance and vintage curves continuously, execute fair lending analyses and documented underwriting overrides, and maintain model risk and data privacy policies in line with GLBA and SEC filing requirements.

Partner Onboarding and Integration

Customer Acquisition and Servicing

Upstart runs digital marketing and referral programs to scale borrower inflow, offers self-serve portals plus live support for applications and account management, and outsources payments, hardship programs and collections to partner servicers while tracking NPS and funnel KPIs to optimize conversion and credit outcomes.

- Digital marketing & referrals

- Self-serve portals & support

- Partner payments, hardship, collections

- NPS & funnel KPI measurement

Automate decisioning — ~27% approvals, up to 75% loss cuts

Build and retrain credit, pricing, and fraud models with continual data ingestion, feature engineering, bias testing, backtesting and governance; run automated pre-qualification, verification and underwriting flows to scale decisioning; monitor portfolio vintage curves, fair lending and model risk; onboard partners via API/LOS integrations, product design, SLAs and performance dashboards while scaling acquisition and servicing.

| Metric | Value |

|---|---|

| Approval lift vs FICO | ~27% |

| Loss reduction vs FICO | up to 75% |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Upstart Business Model Canvas you'll receive—it's not a mockup or teaser. When you purchase, you'll get this exact, fully editable file in the same format shown. It's ready for presentation, analysis, or modification with all sections included and no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: Actionable growth blueprint for investors, founders and analysts

Unlock Upstart’s growth blueprint with our concise Business Model Canvas that maps value propositions, customer segments, revenue streams and competitive advantages. Perfect for investors, founders and analysts, it turns strategy into action. Download the full Word & Excel kit to benchmark, plan and scale confidently.

Partnerships

Banks and Credit Unions

Partner banks and credit unions originate loans using Upstart’s AI underwriting while supplying balance-sheet capacity and regulatory infrastructure, enabling rapid scaling. Co-branded programs align incentives and expand reach through partner distribution channels. Ongoing performance data from these originations feeds continuous model refinement and risk calibration.

Institutional Capital Providers

Institutional whole loan buyers and securitization partners supply funding at scale, enabling Upstart to convert originated loans into immediate liquidity. Forward flow agreements with banks and investors stabilize monthly volumes and warehouse utilization. Ongoing pricing feedback from these partners informs risk-based APRs and underwriting adjustments. A diversified capital base reduces funding costs and dampens rate volatility.

Data and Credit Bureaus

Access to credit files, alternative data and verification services enrich Upstart’s risk signals, improving model precision and borrower segmentation. Real-time feeds enable pre-qualification and fraud checks with sub-second responses and vendor SLAs targeting 99.9% uptime. Compliance-grade data lineage is retained via SOC 2 Type II and GLBA-aligned controls. Partners process millions of records daily to sustain model training and decisioning.

Regulatory and Compliance Advisors

Regulatory and compliance advisors guide Upstart on fair lending, model risk, and consumer protections, aligning policies with 2024 rule updates; independent validations and third-party audits materially lower regulatory exposure and support supervisory exams. Governance frameworks are revised as rules evolve and mandatory training embeds best practices across product, credit and analytics teams.

- Fair lending oversight — advisory alignment with 2024 guidance

- Independent validations — third-party audits reduce regulatory risk

- Governance updates — continuous rule-driven revisions

- Training — mandatory compliance and model-risk education for teams

Technology and Cloud Providers

Technology and cloud providers (AWS, Azure, GCP ~66% combined market share in 2024) supply cloud compute, MLOps tooling, and security vendors that power Upstart’s AI-first lending platform; APIs enable bank integrations and full KYC/AML workflows. Monitoring and observability deliver near 99.99% availability targets and sub-second API latency SLAs, while auto-scaling supports peak demand during lending cycles.

- Cloud compute: AWS/Azure/GCP (~66% 2024)

- MLOps: model deployment, CI/CD, feature stores

- Security: IAM, encryption, third-party vendors

- APIs: bank integrations, KYC/AML orchestration

- Reliability: monitoring, observability, 99.99% targets

- Scalability: auto-scaling for peak origination

Banks drive origination; investors add liquidity; cloud AI powers risk

Bank partners originate loans and provide balance-sheet/regulatory capacity; co-branded deals expand distribution and supply performance data for model tuning. Institutional buyers and securitizers provide liquidity via whole-loan purchases and forward flows, stabilizing volumes and pricing. Data, verification and cloud providers (AWS/Azure/GCP ~66% 2024) enable AI decisioning, uptime and real-time risk signals.

| Partner | Role | 2024 metric |

|---|---|---|

| Banks/credit unions | Origination, capital | ~60% originations via bank partners |

| Investors/securitizers | Funding/liquidity | Forward flows stabilizing monthly volume |

| Data/Cloud vendors | Signals+infra | AWS/Azure/GCP ~66% market share |

What is included in the product

Comprehensive Upstart Business Model Canvas mapping all 9 BMC blocks with clear value propositions, customer segments, channels and revenue streams. Designed for investors and analysts, it includes competitive advantages, SWOT-linked insights and real-company validation for presentations and strategic decisions.

High-level view of Upstart’s business model with editable cells that quickly surface core pain relievers—automated underwriting, partner distribution, and fee structure—so teams can diagnose value drivers and risks in minutes.

Activities

AI Model Development

Build and retrain credit, pricing, and fraud models using continual ingestion of borrower, bureau, and payment data; perform feature engineering and rigorous bias testing across demographics; run backtesting and challenger experiments to compare production models and quantify lift; govern models with comprehensive documentation, version control, monitoring, and controls to meet regulatory and audit requirements.

Loan Origination and Decisioning

Run pre-qualification, verification, and underwriting flows that automate identity, income, and employment checks to scale decisioning and reduce manual review. Upstart reports its AI historically enables roughly 27% higher approvals and up to 75% lower loss rates versus traditional credit-score-only models, while routing approvals to partner-specific criteria. Continuous tuning optimizes conversion while managing portfolio-level risk.

Risk and Compliance Management

Monitor portfolio performance and vintage curves continuously, execute fair lending analyses and documented underwriting overrides, and maintain model risk and data privacy policies in line with GLBA and SEC filing requirements.

Partner Onboarding and Integration

Customer Acquisition and Servicing

Upstart runs digital marketing and referral programs to scale borrower inflow, offers self-serve portals plus live support for applications and account management, and outsources payments, hardship programs and collections to partner servicers while tracking NPS and funnel KPIs to optimize conversion and credit outcomes.

- Digital marketing & referrals

- Self-serve portals & support

- Partner payments, hardship, collections

- NPS & funnel KPI measurement

Automate decisioning — ~27% approvals, up to 75% loss cuts

Build and retrain credit, pricing, and fraud models with continual data ingestion, feature engineering, bias testing, backtesting and governance; run automated pre-qualification, verification and underwriting flows to scale decisioning; monitor portfolio vintage curves, fair lending and model risk; onboard partners via API/LOS integrations, product design, SLAs and performance dashboards while scaling acquisition and servicing.

| Metric | Value |

|---|---|

| Approval lift vs FICO | ~27% |

| Loss reduction vs FICO | up to 75% |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Upstart Business Model Canvas you'll receive—it's not a mockup or teaser. When you purchase, you'll get this exact, fully editable file in the same format shown. It's ready for presentation, analysis, or modification with all sections included and no surprises.