Urban Outfitters Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

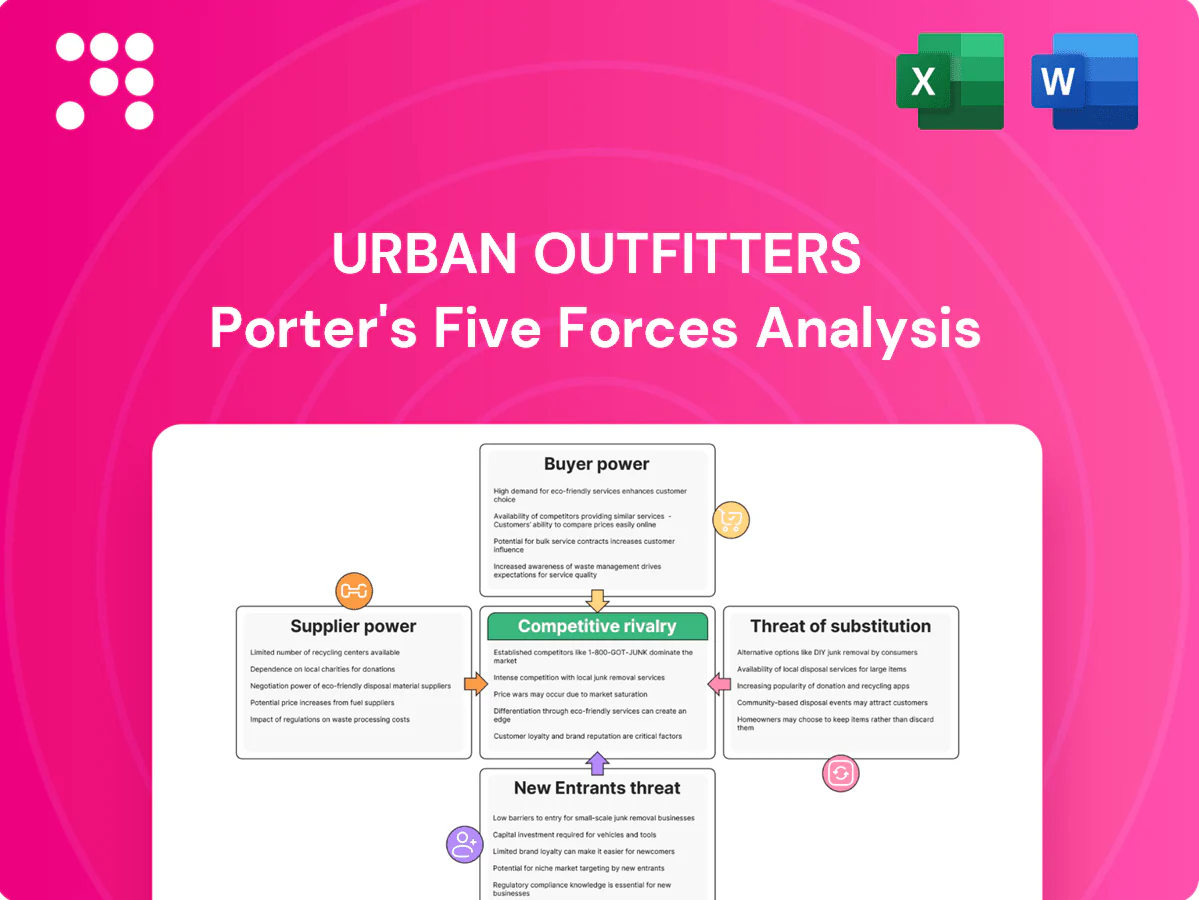

Urban Outfitters faces moderate rivalry and shifting buyer tastes, balanced by brand differentiation and omni-channel reach; supplier power is limited but fast-fashion substitutes and online entrants raise strategic risks. This snapshot highlights key pressures—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Diverse global vendor base

URBN sources apparel and home goods from a diverse network of factories and mills across Asia, Europe and the Americas, limiting any single supplier’s leverage and supporting FY2024 revenue of about $4.8 billion. Vendor switching is feasible for standard categories but remains constrained for specialty fabrics and heavily embellished goods, where expertise and tooling create stickiness. Multiplicity of suppliers strengthens negotiating position on pricing and lead times and hedges disruption risk; however, consolidation among key mills can tighten availability of critical inputs.

Private label and design control

Significant in-house design across Urban Outfitters, Anthropologie and Free People—with private-label assortments accounting for about 60% of merchandise—reduces dependency on branded suppliers and limits supplier leverage. Owning specs and IP allows multi-vendor bidding and quicker reorders, compressing supplier pricing power on core styles. High-touch artisanal or small-batch craftsmanship, however, can remain supplier-led and command premiums.

Exclusive collabs and niche artisans

Exclusive collabs and niche artisan partnerships boost differentiation for URBN brands (Urban Outfitters, Anthropologie, Free People) but increase supplier power because uniqueness raises switching costs when brand equity relies on a partner’s aesthetic; URBN reported roughly $4.85 billion in net sales in fiscal 2024, so constrained partner lead times and minimums can materially affect inventory and margins, forcing a balance between exclusivity and optionality.

Logistics, freight, and compliance

Ocean freight, port congestion and geopolitical shifts have periodically shifted bargaining power to logistics intermediaries, with container spot rates down roughly 70% from 2021 peaks by 2024 but volatility remaining; compliance on labor, ESG and chemical standards has narrowed the approved vendor pool, strengthening compliant suppliers; currency swings and cotton/dye spikes are often passed through to retailers, while long‑term contracts and diversified routing mitigate exposure.

- Container rates: -70% vs 2021 (2024)

- Compliance: smaller approved vendor pool

- Pass-through: raw-material/currency risk

- Mitigation: long-term contracts, diversified routing

Nuuly inventory dynamics

Nuuly rental depends on durable, replenishable inventory and occasional branded partners, giving suppliers that meet rental-grade specs incremental leverage. Wear-and-tear and refurbishment requirements constrain direct substitutes and raise switching costs. Bulk purchase commitments for rental fleets can lock pricing and lead times. URBN’s owned brands supply a meaningful share, tempering supplier power.

- Supplier leverage: rental-grade specs

- Switching constraints: refurbishment

- Contractual lock: bulk fleet buys

- Counterbalance: URBN-owned brand supply

Diverse sourcing and 60% private-label curb supplier power vs $4.85B sales

URBN’s diverse global sourcing limits single-supplier leverage and supports FY2024 net sales of $4.85 billion. Private-label assortments (~60% of merchandise) reduce branded-supplier power, while logistics volatility, tightened compliant vendor pools and Nuuly rental specs increase supplier leverage on select inputs.

| Metric | 2024 |

|---|---|

| Net sales | $4.85B |

| Private-label share | ~60% |

| Container rates vs 2021 | -70% |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Urban Outfitters, assessing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers affecting its pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Urban Outfitters—clarifying competitive, supplier, buyer, entrant and substitute pressures for quick strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Low switching costs, high choice

Low switching costs let consumers move quickly to Zara, H&M, Abercrombie, Revolve or local boutiques; online marketplaces heighten side-by-side comparison and price discovery. URBN reported roughly $4.6B in net sales in FY2024, underscoring scale but also exposure to churn. Buyers now demand continuous value and novelty, empowering returns and markdown pressure. URBN must refresh assortments and store/online experiences constantly to retain customers.

Price transparency and promos

E-commerce and social media make pricing highly visible, pressuring margins; Urban Outfitters reported roughly $4.6B in FY2024 net sales with large digital engagement. Frequent promotions train buyers to wait for markdowns, lowering full‑price sell‑through. Dynamic pricing and segmented offers can manage elasticity, but aggressive discounting risks brand dilution and margin erosion.

Omnichannel expectations

Customers demand fast shipping, easy returns, BOPIS and consistent inventory across channels; e-commerce return rates hovered around 18% in 2024, raising service SLA stakes and churn risk. Missed SLAs drive defections while strong UX and loyalty reduce perceived switching gains. Urban Outfitters’ investments in fulfillment and data integration (omnichannel inventory, real-time SKU sync) blunt buyer leverage and protect margins.

Segment tastes and trend velocity

Gen Z and millennial cohorts shift trends rapidly, raising defection risk for Urban Outfitters; FY2024 net sales were about $4.05 billion, amplifying revenue exposure to misses. Social virality (about 70% of Gen Z discover brands via social platforms in 2024) can swing demand abruptly. Fit, inclusivity and sustainability (66% of Gen Z prefer sustainable options) drive purchases. Improved demand sensing can cut markdowns/ write-offs by up to 30%, lowering buyer power.

- Trend velocity: high—70% social discovery

- Preferences: 66% sustainability, strong inclusivity/fit demand

- Mitigation: demand sensing → up to 30% fewer markdowns

Nuuly subscription churn risk

Nuuly rental subscribers can pause or cancel easily, giving renters tangible price and assortment leverage; Urban Outfitters cites 2024 initiatives—exclusive capsules and flexible plans—that aim to reduce churn and assortment pressure while cross-brand benefits seek to increase switching costs.

- pause/cancel ease: raises bargaining power

- exclusive capsules & flexible plans: reduce churn

- high satisfaction: lowers renter leverage

- cross-brand perks: lock-in value

Demand sensing and omnichannel exclusives fight high returns and Gen Z price power

Low switching costs and visible pricing (online marketplaces, social) give buyers strong leverage; frequent promotions train customers to wait for markdowns. Fast trend shifts among Gen Z/millennials and high e‑commerce return rates (~18% in 2024) amplify churn risk versus URBN’s ~$4.6B FY2024 net sales. Omnichannel fulfillment, exclusive Nuuly capsules and demand sensing (can cut markdowns ~30%) reduce customer power.

| Metric | 2024 |

|---|---|

| URBN net sales | $4.6B |

| E‑commerce return rate | ~18% |

| Gen Z social discovery | ~70% |

| Gen Z sustainability preference | ~66% |

| Markdown reduction (demand sensing) | up to 30% |

Preview the Actual Deliverable

Urban Outfitters Porter's Five Forces Analysis

This preview shows the exact Urban Outfitters Porter's Five Forces Analysis you'll receive upon purchase—no surprises, no placeholders. It is the full, professionally formatted document ready for download and immediate use. Completing your purchase grants instant access to this identical file.

Go Beyond the Preview—Access the Full Strategic Report

Urban Outfitters faces moderate rivalry and shifting buyer tastes, balanced by brand differentiation and omni-channel reach; supplier power is limited but fast-fashion substitutes and online entrants raise strategic risks. This snapshot highlights key pressures—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Diverse global vendor base

URBN sources apparel and home goods from a diverse network of factories and mills across Asia, Europe and the Americas, limiting any single supplier’s leverage and supporting FY2024 revenue of about $4.8 billion. Vendor switching is feasible for standard categories but remains constrained for specialty fabrics and heavily embellished goods, where expertise and tooling create stickiness. Multiplicity of suppliers strengthens negotiating position on pricing and lead times and hedges disruption risk; however, consolidation among key mills can tighten availability of critical inputs.

Private label and design control

Significant in-house design across Urban Outfitters, Anthropologie and Free People—with private-label assortments accounting for about 60% of merchandise—reduces dependency on branded suppliers and limits supplier leverage. Owning specs and IP allows multi-vendor bidding and quicker reorders, compressing supplier pricing power on core styles. High-touch artisanal or small-batch craftsmanship, however, can remain supplier-led and command premiums.

Exclusive collabs and niche artisans

Exclusive collabs and niche artisan partnerships boost differentiation for URBN brands (Urban Outfitters, Anthropologie, Free People) but increase supplier power because uniqueness raises switching costs when brand equity relies on a partner’s aesthetic; URBN reported roughly $4.85 billion in net sales in fiscal 2024, so constrained partner lead times and minimums can materially affect inventory and margins, forcing a balance between exclusivity and optionality.

Logistics, freight, and compliance

Ocean freight, port congestion and geopolitical shifts have periodically shifted bargaining power to logistics intermediaries, with container spot rates down roughly 70% from 2021 peaks by 2024 but volatility remaining; compliance on labor, ESG and chemical standards has narrowed the approved vendor pool, strengthening compliant suppliers; currency swings and cotton/dye spikes are often passed through to retailers, while long‑term contracts and diversified routing mitigate exposure.

- Container rates: -70% vs 2021 (2024)

- Compliance: smaller approved vendor pool

- Pass-through: raw-material/currency risk

- Mitigation: long-term contracts, diversified routing

Nuuly inventory dynamics

Nuuly rental depends on durable, replenishable inventory and occasional branded partners, giving suppliers that meet rental-grade specs incremental leverage. Wear-and-tear and refurbishment requirements constrain direct substitutes and raise switching costs. Bulk purchase commitments for rental fleets can lock pricing and lead times. URBN’s owned brands supply a meaningful share, tempering supplier power.

- Supplier leverage: rental-grade specs

- Switching constraints: refurbishment

- Contractual lock: bulk fleet buys

- Counterbalance: URBN-owned brand supply

Diverse sourcing and 60% private-label curb supplier power vs $4.85B sales

URBN’s diverse global sourcing limits single-supplier leverage and supports FY2024 net sales of $4.85 billion. Private-label assortments (~60% of merchandise) reduce branded-supplier power, while logistics volatility, tightened compliant vendor pools and Nuuly rental specs increase supplier leverage on select inputs.

| Metric | 2024 |

|---|---|

| Net sales | $4.85B |

| Private-label share | ~60% |

| Container rates vs 2021 | -70% |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Urban Outfitters, assessing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers affecting its pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Urban Outfitters—clarifying competitive, supplier, buyer, entrant and substitute pressures for quick strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Low switching costs, high choice

Low switching costs let consumers move quickly to Zara, H&M, Abercrombie, Revolve or local boutiques; online marketplaces heighten side-by-side comparison and price discovery. URBN reported roughly $4.6B in net sales in FY2024, underscoring scale but also exposure to churn. Buyers now demand continuous value and novelty, empowering returns and markdown pressure. URBN must refresh assortments and store/online experiences constantly to retain customers.

Price transparency and promos

E-commerce and social media make pricing highly visible, pressuring margins; Urban Outfitters reported roughly $4.6B in FY2024 net sales with large digital engagement. Frequent promotions train buyers to wait for markdowns, lowering full‑price sell‑through. Dynamic pricing and segmented offers can manage elasticity, but aggressive discounting risks brand dilution and margin erosion.

Omnichannel expectations

Customers demand fast shipping, easy returns, BOPIS and consistent inventory across channels; e-commerce return rates hovered around 18% in 2024, raising service SLA stakes and churn risk. Missed SLAs drive defections while strong UX and loyalty reduce perceived switching gains. Urban Outfitters’ investments in fulfillment and data integration (omnichannel inventory, real-time SKU sync) blunt buyer leverage and protect margins.

Segment tastes and trend velocity

Gen Z and millennial cohorts shift trends rapidly, raising defection risk for Urban Outfitters; FY2024 net sales were about $4.05 billion, amplifying revenue exposure to misses. Social virality (about 70% of Gen Z discover brands via social platforms in 2024) can swing demand abruptly. Fit, inclusivity and sustainability (66% of Gen Z prefer sustainable options) drive purchases. Improved demand sensing can cut markdowns/ write-offs by up to 30%, lowering buyer power.

- Trend velocity: high—70% social discovery

- Preferences: 66% sustainability, strong inclusivity/fit demand

- Mitigation: demand sensing → up to 30% fewer markdowns

Nuuly subscription churn risk

Nuuly rental subscribers can pause or cancel easily, giving renters tangible price and assortment leverage; Urban Outfitters cites 2024 initiatives—exclusive capsules and flexible plans—that aim to reduce churn and assortment pressure while cross-brand benefits seek to increase switching costs.

- pause/cancel ease: raises bargaining power

- exclusive capsules & flexible plans: reduce churn

- high satisfaction: lowers renter leverage

- cross-brand perks: lock-in value

Demand sensing and omnichannel exclusives fight high returns and Gen Z price power

Low switching costs and visible pricing (online marketplaces, social) give buyers strong leverage; frequent promotions train customers to wait for markdowns. Fast trend shifts among Gen Z/millennials and high e‑commerce return rates (~18% in 2024) amplify churn risk versus URBN’s ~$4.6B FY2024 net sales. Omnichannel fulfillment, exclusive Nuuly capsules and demand sensing (can cut markdowns ~30%) reduce customer power.

| Metric | 2024 |

|---|---|

| URBN net sales | $4.6B |

| E‑commerce return rate | ~18% |

| Gen Z social discovery | ~70% |

| Gen Z sustainability preference | ~66% |

| Markdown reduction (demand sensing) | up to 30% |

Preview the Actual Deliverable

Urban Outfitters Porter's Five Forces Analysis

This preview shows the exact Urban Outfitters Porter's Five Forces Analysis you'll receive upon purchase—no surprises, no placeholders. It is the full, professionally formatted document ready for download and immediate use. Completing your purchase grants instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Urban Outfitters faces moderate rivalry and shifting buyer tastes, balanced by brand differentiation and omni-channel reach; supplier power is limited but fast-fashion substitutes and online entrants raise strategic risks. This snapshot highlights key pressures—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Diverse global vendor base

URBN sources apparel and home goods from a diverse network of factories and mills across Asia, Europe and the Americas, limiting any single supplier’s leverage and supporting FY2024 revenue of about $4.8 billion. Vendor switching is feasible for standard categories but remains constrained for specialty fabrics and heavily embellished goods, where expertise and tooling create stickiness. Multiplicity of suppliers strengthens negotiating position on pricing and lead times and hedges disruption risk; however, consolidation among key mills can tighten availability of critical inputs.

Private label and design control

Significant in-house design across Urban Outfitters, Anthropologie and Free People—with private-label assortments accounting for about 60% of merchandise—reduces dependency on branded suppliers and limits supplier leverage. Owning specs and IP allows multi-vendor bidding and quicker reorders, compressing supplier pricing power on core styles. High-touch artisanal or small-batch craftsmanship, however, can remain supplier-led and command premiums.

Exclusive collabs and niche artisans

Exclusive collabs and niche artisan partnerships boost differentiation for URBN brands (Urban Outfitters, Anthropologie, Free People) but increase supplier power because uniqueness raises switching costs when brand equity relies on a partner’s aesthetic; URBN reported roughly $4.85 billion in net sales in fiscal 2024, so constrained partner lead times and minimums can materially affect inventory and margins, forcing a balance between exclusivity and optionality.

Logistics, freight, and compliance

Ocean freight, port congestion and geopolitical shifts have periodically shifted bargaining power to logistics intermediaries, with container spot rates down roughly 70% from 2021 peaks by 2024 but volatility remaining; compliance on labor, ESG and chemical standards has narrowed the approved vendor pool, strengthening compliant suppliers; currency swings and cotton/dye spikes are often passed through to retailers, while long‑term contracts and diversified routing mitigate exposure.

- Container rates: -70% vs 2021 (2024)

- Compliance: smaller approved vendor pool

- Pass-through: raw-material/currency risk

- Mitigation: long-term contracts, diversified routing

Nuuly inventory dynamics

Nuuly rental depends on durable, replenishable inventory and occasional branded partners, giving suppliers that meet rental-grade specs incremental leverage. Wear-and-tear and refurbishment requirements constrain direct substitutes and raise switching costs. Bulk purchase commitments for rental fleets can lock pricing and lead times. URBN’s owned brands supply a meaningful share, tempering supplier power.

- Supplier leverage: rental-grade specs

- Switching constraints: refurbishment

- Contractual lock: bulk fleet buys

- Counterbalance: URBN-owned brand supply

Diverse sourcing and 60% private-label curb supplier power vs $4.85B sales

URBN’s diverse global sourcing limits single-supplier leverage and supports FY2024 net sales of $4.85 billion. Private-label assortments (~60% of merchandise) reduce branded-supplier power, while logistics volatility, tightened compliant vendor pools and Nuuly rental specs increase supplier leverage on select inputs.

| Metric | 2024 |

|---|---|

| Net sales | $4.85B |

| Private-label share | ~60% |

| Container rates vs 2021 | -70% |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Urban Outfitters, assessing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers affecting its pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Urban Outfitters—clarifying competitive, supplier, buyer, entrant and substitute pressures for quick strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Low switching costs, high choice

Low switching costs let consumers move quickly to Zara, H&M, Abercrombie, Revolve or local boutiques; online marketplaces heighten side-by-side comparison and price discovery. URBN reported roughly $4.6B in net sales in FY2024, underscoring scale but also exposure to churn. Buyers now demand continuous value and novelty, empowering returns and markdown pressure. URBN must refresh assortments and store/online experiences constantly to retain customers.

Price transparency and promos

E-commerce and social media make pricing highly visible, pressuring margins; Urban Outfitters reported roughly $4.6B in FY2024 net sales with large digital engagement. Frequent promotions train buyers to wait for markdowns, lowering full‑price sell‑through. Dynamic pricing and segmented offers can manage elasticity, but aggressive discounting risks brand dilution and margin erosion.

Omnichannel expectations

Customers demand fast shipping, easy returns, BOPIS and consistent inventory across channels; e-commerce return rates hovered around 18% in 2024, raising service SLA stakes and churn risk. Missed SLAs drive defections while strong UX and loyalty reduce perceived switching gains. Urban Outfitters’ investments in fulfillment and data integration (omnichannel inventory, real-time SKU sync) blunt buyer leverage and protect margins.

Segment tastes and trend velocity

Gen Z and millennial cohorts shift trends rapidly, raising defection risk for Urban Outfitters; FY2024 net sales were about $4.05 billion, amplifying revenue exposure to misses. Social virality (about 70% of Gen Z discover brands via social platforms in 2024) can swing demand abruptly. Fit, inclusivity and sustainability (66% of Gen Z prefer sustainable options) drive purchases. Improved demand sensing can cut markdowns/ write-offs by up to 30%, lowering buyer power.

- Trend velocity: high—70% social discovery

- Preferences: 66% sustainability, strong inclusivity/fit demand

- Mitigation: demand sensing → up to 30% fewer markdowns

Nuuly subscription churn risk

Nuuly rental subscribers can pause or cancel easily, giving renters tangible price and assortment leverage; Urban Outfitters cites 2024 initiatives—exclusive capsules and flexible plans—that aim to reduce churn and assortment pressure while cross-brand benefits seek to increase switching costs.

- pause/cancel ease: raises bargaining power

- exclusive capsules & flexible plans: reduce churn

- high satisfaction: lowers renter leverage

- cross-brand perks: lock-in value

Demand sensing and omnichannel exclusives fight high returns and Gen Z price power

Low switching costs and visible pricing (online marketplaces, social) give buyers strong leverage; frequent promotions train customers to wait for markdowns. Fast trend shifts among Gen Z/millennials and high e‑commerce return rates (~18% in 2024) amplify churn risk versus URBN’s ~$4.6B FY2024 net sales. Omnichannel fulfillment, exclusive Nuuly capsules and demand sensing (can cut markdowns ~30%) reduce customer power.

| Metric | 2024 |

|---|---|

| URBN net sales | $4.6B |

| E‑commerce return rate | ~18% |

| Gen Z social discovery | ~70% |

| Gen Z sustainability preference | ~66% |

| Markdown reduction (demand sensing) | up to 30% |

Preview the Actual Deliverable

Urban Outfitters Porter's Five Forces Analysis

This preview shows the exact Urban Outfitters Porter's Five Forces Analysis you'll receive upon purchase—no surprises, no placeholders. It is the full, professionally formatted document ready for download and immediate use. Completing your purchase grants instant access to this identical file.