US LBM Holdings Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

US LBM Holdings faces intense supplier and buyer dynamics amid consolidation and margin pressure, with moderate threat from substitutes and manageable new-entrant risk due to scale advantages. This snapshot highlights strategic pain points and growth levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

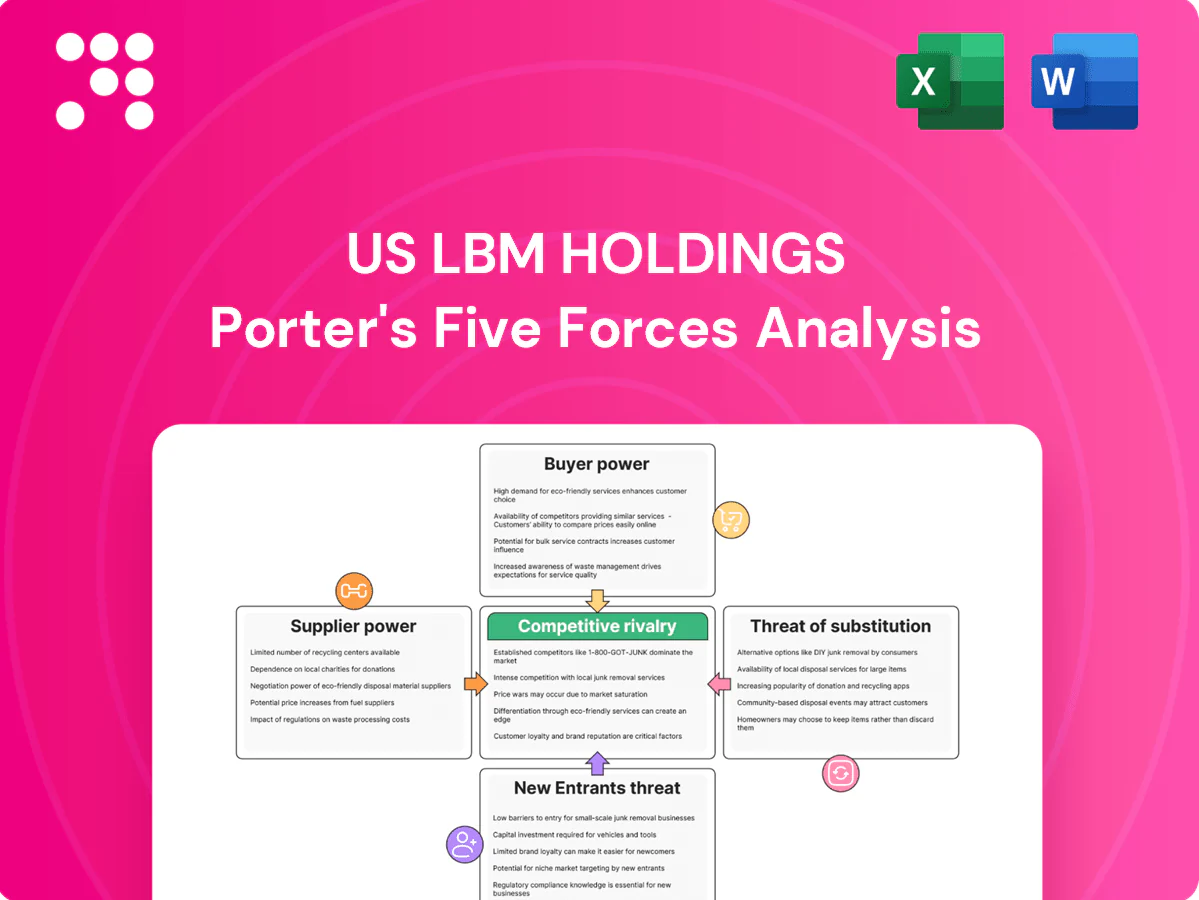

Suppliers Bargaining Power

Consolidated mills and branded OEMs

Engineered wood, roofing and millwork are dominated by large branded manufacturers such as Weyerhaeuser, LP and GAF that use selective distribution; their brand pull and allocation power raise switching costs and create pricing pressure for dealers. Vendor programs and territory protections often restrict alternatives for critical SKUs, increasing dependence on these suppliers. US LBM offsets this by leveraging national relationships and scale to centralize purchasing and negotiate allocation and pricing terms.

Commodity price volatility

Lumber and panel prices remain highly cyclical, swinging with housing activity and policy shifts; 2024 saw renewed single-family starts growth and persistent tariff risk that tightened supply. Rapid price moves can compress distributor margins when changes outpace turnover, and suppliers often tighten allocations in upcycles. Hedging, dynamic pricing, and strict inventory discipline are essential countermeasures.

Logistics and lead-time constraints

Special-order millwork (typically 6–12 weeks), trusses (2–6 weeks) and EWP (4–12 weeks) create supplier leverage in tight 2024 markets; national truckload rate volatility and fuel/freight surcharges—routinely passed through by vendors—raise landed costs and compress margins. Variability in supplier service levels disrupts US LBM’s delivery promises, while back-to-back ordering and vendor-managed inventory materially reduce inventory and fulfillment exposure.

Countervailing scale and multisourcing

US LBM’s 450+ locations aggregate purchasing volume to secure rebates and preferred access, weakening supplier leverage; multisourcing across product categories further dilutes any single vendor’s hold. Private-label and secondary brands provide price alternatives for customers, while EDI and portal-based data sharing in 2024 have improved forecast accuracy and strengthened US LBM’s bargaining position.

- 450+ locations aggregate volume

- Multisourcing reduces single-supplier risk

- Private-label offers lower-cost alternatives

- EDI/portals improve forecasts and negotiation

Specialization and technical support

Supply concentration raises switching costs; US LBM 450+ locations, lead times 2–12 weeks

Engineered wood, roofing and millwork are concentrated with brands Weyerhaeuser, LP and GAF, raising switching costs and pricing pressure. Lumber/panel prices remained cyclical in 2024 and suppliers tightened allocations; millwork/truss/EWP lead times typically 2–12 weeks. US LBM’s 450+ locations, multisourcing, private-labels and EDI strengthen purchasing leverage.

| Metric | Value |

|---|---|

| Locations | 450+ |

| Key suppliers | Weyerhaeuser, LP, GAF |

| Lead times | 2–12 weeks |

| 2024 dynamic | Supplier allocations tightened |

What is included in the product

Porter’s Five Forces analysis for US LBM Holdings uncovers competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and industry rivalry to clarify pricing and profitability drivers. It highlights barriers protecting incumbents, supplier concentration risks, buyer leverage, and emerging disruptions shaping strategic priorities.

A one-sheet Porter's Five Forces view of US LBM Holdings that simplifies competitive pressure into a single, customizable radar—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

Large pro builders wield volume leverage

In 2024 regional and national pro builders wield strong volume leverage, negotiating aggressive pricing and contract terms that compress distributor margins. Bid-based, multi-project awards force distributors into tighter competition and favor suppliers offering rebates and dedicated service levels tied to volume commitments. While per-unit margins are thinner, long-term contract visibility stabilizes cash flow and procurement planning for US LBM.

Fragmented local contractors dilute power

Remodelers and small contractors—over 90% of U.S. construction firms have fewer than 20 employees—are numerous and relationship-driven, diluting collective pricing power. Their smaller baskets blunt price pressure versus national accounts, so service, credit, and delivery reliability often outweigh a few pennies. US LBM operates over 260 local branches that tailor product mixes and credit terms to retain loyalty and protect margins.

Moderate switching costs via services

Takeoffs, design coordination, jobsite staging and credit accounts create meaningful friction to switch, especially for large contractors working with US LBM whose 2024 pro forma revenue approached $10 billion. Mid-project changes risk costly delays and rework for customers. Commodity SKUs remain comparable, enabling price-driven switching on roughly 40% of volumes. Service differentiation preserves margin on mixed baskets.

Credit terms and cash-flow sensitivity

Builders value flexible terms and lien-waiver support; in 2024, with the US federal funds rate around 5.25–5.50%, tighter credit raised requests for extended terms or discounts, increasing buyer bargaining power and pressuring margins. Strong credit management, risk scoring and disciplined collections helped US LBM protect profitability amid greater payment flexibility demands.

- Higher buyer power: more term/discount requests

- Cash sensitivity: elevated by 2024 rate environment

- Defense: credit scoring, collections, lien-waivers

Omnichannel and price transparency

Omnichannel tools—pro desks, e-commerce and digital quoting—have increased price discovery across US LBM’s network, letting commercial buyers benchmark distributors and big-box channels in real time; industry reports in 2024 show digital ordering penetration rising in professional channels. Price transparency compresses gross margins on like-for-like SKUs, while bundling and value-add services preserve total ticket economics and share of wallet.

- Pro desks improve retention

- E-commerce raises benchmarking

- Transparency compresses SKU margins

- Bundles defend ticket value

Pro builders squeeze margins; pro forma revenue near $10B in 2024

Large pro builders exert strong leverage—multi-project bids and volume rebates compress distributor margins despite stable contract visibility; US LBM pro forma revenue approached $10 billion in 2024.

Remodelers and small contractors dilute collective pricing power; US LBM’s 260+ local branches and service focus limit switching on mixed baskets while ~40% of volumes remain price-sensitive.

Higher 2024 fed funds (5.25–5.50%) increased term/discount requests; credit scoring and collections protected margins.

| Metric | 2024 |

|---|---|

| Pro forma revenue | $~10B |

| Branches | 260+ |

| Price-switchable volume | ~40% |

| Federal funds rate | 5.25–5.50% |

Same Document Delivered

US LBM Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for US LBM Holdings you'll receive immediately after purchase—no placeholders, no mockups. The document is professionally written, fully formatted, and ready for download and use the moment you buy. You're looking at the final deliverable, the same file available for instant access after payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

US LBM Holdings faces intense supplier and buyer dynamics amid consolidation and margin pressure, with moderate threat from substitutes and manageable new-entrant risk due to scale advantages. This snapshot highlights strategic pain points and growth levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Consolidated mills and branded OEMs

Engineered wood, roofing and millwork are dominated by large branded manufacturers such as Weyerhaeuser, LP and GAF that use selective distribution; their brand pull and allocation power raise switching costs and create pricing pressure for dealers. Vendor programs and territory protections often restrict alternatives for critical SKUs, increasing dependence on these suppliers. US LBM offsets this by leveraging national relationships and scale to centralize purchasing and negotiate allocation and pricing terms.

Commodity price volatility

Lumber and panel prices remain highly cyclical, swinging with housing activity and policy shifts; 2024 saw renewed single-family starts growth and persistent tariff risk that tightened supply. Rapid price moves can compress distributor margins when changes outpace turnover, and suppliers often tighten allocations in upcycles. Hedging, dynamic pricing, and strict inventory discipline are essential countermeasures.

Logistics and lead-time constraints

Special-order millwork (typically 6–12 weeks), trusses (2–6 weeks) and EWP (4–12 weeks) create supplier leverage in tight 2024 markets; national truckload rate volatility and fuel/freight surcharges—routinely passed through by vendors—raise landed costs and compress margins. Variability in supplier service levels disrupts US LBM’s delivery promises, while back-to-back ordering and vendor-managed inventory materially reduce inventory and fulfillment exposure.

Countervailing scale and multisourcing

US LBM’s 450+ locations aggregate purchasing volume to secure rebates and preferred access, weakening supplier leverage; multisourcing across product categories further dilutes any single vendor’s hold. Private-label and secondary brands provide price alternatives for customers, while EDI and portal-based data sharing in 2024 have improved forecast accuracy and strengthened US LBM’s bargaining position.

- 450+ locations aggregate volume

- Multisourcing reduces single-supplier risk

- Private-label offers lower-cost alternatives

- EDI/portals improve forecasts and negotiation

Specialization and technical support

Supply concentration raises switching costs; US LBM 450+ locations, lead times 2–12 weeks

Engineered wood, roofing and millwork are concentrated with brands Weyerhaeuser, LP and GAF, raising switching costs and pricing pressure. Lumber/panel prices remained cyclical in 2024 and suppliers tightened allocations; millwork/truss/EWP lead times typically 2–12 weeks. US LBM’s 450+ locations, multisourcing, private-labels and EDI strengthen purchasing leverage.

| Metric | Value |

|---|---|

| Locations | 450+ |

| Key suppliers | Weyerhaeuser, LP, GAF |

| Lead times | 2–12 weeks |

| 2024 dynamic | Supplier allocations tightened |

What is included in the product

Porter’s Five Forces analysis for US LBM Holdings uncovers competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and industry rivalry to clarify pricing and profitability drivers. It highlights barriers protecting incumbents, supplier concentration risks, buyer leverage, and emerging disruptions shaping strategic priorities.

A one-sheet Porter's Five Forces view of US LBM Holdings that simplifies competitive pressure into a single, customizable radar—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

Large pro builders wield volume leverage

In 2024 regional and national pro builders wield strong volume leverage, negotiating aggressive pricing and contract terms that compress distributor margins. Bid-based, multi-project awards force distributors into tighter competition and favor suppliers offering rebates and dedicated service levels tied to volume commitments. While per-unit margins are thinner, long-term contract visibility stabilizes cash flow and procurement planning for US LBM.

Fragmented local contractors dilute power

Remodelers and small contractors—over 90% of U.S. construction firms have fewer than 20 employees—are numerous and relationship-driven, diluting collective pricing power. Their smaller baskets blunt price pressure versus national accounts, so service, credit, and delivery reliability often outweigh a few pennies. US LBM operates over 260 local branches that tailor product mixes and credit terms to retain loyalty and protect margins.

Moderate switching costs via services

Takeoffs, design coordination, jobsite staging and credit accounts create meaningful friction to switch, especially for large contractors working with US LBM whose 2024 pro forma revenue approached $10 billion. Mid-project changes risk costly delays and rework for customers. Commodity SKUs remain comparable, enabling price-driven switching on roughly 40% of volumes. Service differentiation preserves margin on mixed baskets.

Credit terms and cash-flow sensitivity

Builders value flexible terms and lien-waiver support; in 2024, with the US federal funds rate around 5.25–5.50%, tighter credit raised requests for extended terms or discounts, increasing buyer bargaining power and pressuring margins. Strong credit management, risk scoring and disciplined collections helped US LBM protect profitability amid greater payment flexibility demands.

- Higher buyer power: more term/discount requests

- Cash sensitivity: elevated by 2024 rate environment

- Defense: credit scoring, collections, lien-waivers

Omnichannel and price transparency

Omnichannel tools—pro desks, e-commerce and digital quoting—have increased price discovery across US LBM’s network, letting commercial buyers benchmark distributors and big-box channels in real time; industry reports in 2024 show digital ordering penetration rising in professional channels. Price transparency compresses gross margins on like-for-like SKUs, while bundling and value-add services preserve total ticket economics and share of wallet.

- Pro desks improve retention

- E-commerce raises benchmarking

- Transparency compresses SKU margins

- Bundles defend ticket value

Pro builders squeeze margins; pro forma revenue near $10B in 2024

Large pro builders exert strong leverage—multi-project bids and volume rebates compress distributor margins despite stable contract visibility; US LBM pro forma revenue approached $10 billion in 2024.

Remodelers and small contractors dilute collective pricing power; US LBM’s 260+ local branches and service focus limit switching on mixed baskets while ~40% of volumes remain price-sensitive.

Higher 2024 fed funds (5.25–5.50%) increased term/discount requests; credit scoring and collections protected margins.

| Metric | 2024 |

|---|---|

| Pro forma revenue | $~10B |

| Branches | 260+ |

| Price-switchable volume | ~40% |

| Federal funds rate | 5.25–5.50% |

Same Document Delivered

US LBM Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for US LBM Holdings you'll receive immediately after purchase—no placeholders, no mockups. The document is professionally written, fully formatted, and ready for download and use the moment you buy. You're looking at the final deliverable, the same file available for instant access after payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

US LBM Holdings faces intense supplier and buyer dynamics amid consolidation and margin pressure, with moderate threat from substitutes and manageable new-entrant risk due to scale advantages. This snapshot highlights strategic pain points and growth levers. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Consolidated mills and branded OEMs

Engineered wood, roofing and millwork are dominated by large branded manufacturers such as Weyerhaeuser, LP and GAF that use selective distribution; their brand pull and allocation power raise switching costs and create pricing pressure for dealers. Vendor programs and territory protections often restrict alternatives for critical SKUs, increasing dependence on these suppliers. US LBM offsets this by leveraging national relationships and scale to centralize purchasing and negotiate allocation and pricing terms.

Commodity price volatility

Lumber and panel prices remain highly cyclical, swinging with housing activity and policy shifts; 2024 saw renewed single-family starts growth and persistent tariff risk that tightened supply. Rapid price moves can compress distributor margins when changes outpace turnover, and suppliers often tighten allocations in upcycles. Hedging, dynamic pricing, and strict inventory discipline are essential countermeasures.

Logistics and lead-time constraints

Special-order millwork (typically 6–12 weeks), trusses (2–6 weeks) and EWP (4–12 weeks) create supplier leverage in tight 2024 markets; national truckload rate volatility and fuel/freight surcharges—routinely passed through by vendors—raise landed costs and compress margins. Variability in supplier service levels disrupts US LBM’s delivery promises, while back-to-back ordering and vendor-managed inventory materially reduce inventory and fulfillment exposure.

Countervailing scale and multisourcing

US LBM’s 450+ locations aggregate purchasing volume to secure rebates and preferred access, weakening supplier leverage; multisourcing across product categories further dilutes any single vendor’s hold. Private-label and secondary brands provide price alternatives for customers, while EDI and portal-based data sharing in 2024 have improved forecast accuracy and strengthened US LBM’s bargaining position.

- 450+ locations aggregate volume

- Multisourcing reduces single-supplier risk

- Private-label offers lower-cost alternatives

- EDI/portals improve forecasts and negotiation

Specialization and technical support

Supply concentration raises switching costs; US LBM 450+ locations, lead times 2–12 weeks

Engineered wood, roofing and millwork are concentrated with brands Weyerhaeuser, LP and GAF, raising switching costs and pricing pressure. Lumber/panel prices remained cyclical in 2024 and suppliers tightened allocations; millwork/truss/EWP lead times typically 2–12 weeks. US LBM’s 450+ locations, multisourcing, private-labels and EDI strengthen purchasing leverage.

| Metric | Value |

|---|---|

| Locations | 450+ |

| Key suppliers | Weyerhaeuser, LP, GAF |

| Lead times | 2–12 weeks |

| 2024 dynamic | Supplier allocations tightened |

What is included in the product

Porter’s Five Forces analysis for US LBM Holdings uncovers competitive intensity, supplier and buyer bargaining power, threat of new entrants and substitutes, and industry rivalry to clarify pricing and profitability drivers. It highlights barriers protecting incumbents, supplier concentration risks, buyer leverage, and emerging disruptions shaping strategic priorities.

A one-sheet Porter's Five Forces view of US LBM Holdings that simplifies competitive pressure into a single, customizable radar—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

Large pro builders wield volume leverage

In 2024 regional and national pro builders wield strong volume leverage, negotiating aggressive pricing and contract terms that compress distributor margins. Bid-based, multi-project awards force distributors into tighter competition and favor suppliers offering rebates and dedicated service levels tied to volume commitments. While per-unit margins are thinner, long-term contract visibility stabilizes cash flow and procurement planning for US LBM.

Fragmented local contractors dilute power

Remodelers and small contractors—over 90% of U.S. construction firms have fewer than 20 employees—are numerous and relationship-driven, diluting collective pricing power. Their smaller baskets blunt price pressure versus national accounts, so service, credit, and delivery reliability often outweigh a few pennies. US LBM operates over 260 local branches that tailor product mixes and credit terms to retain loyalty and protect margins.

Moderate switching costs via services

Takeoffs, design coordination, jobsite staging and credit accounts create meaningful friction to switch, especially for large contractors working with US LBM whose 2024 pro forma revenue approached $10 billion. Mid-project changes risk costly delays and rework for customers. Commodity SKUs remain comparable, enabling price-driven switching on roughly 40% of volumes. Service differentiation preserves margin on mixed baskets.

Credit terms and cash-flow sensitivity

Builders value flexible terms and lien-waiver support; in 2024, with the US federal funds rate around 5.25–5.50%, tighter credit raised requests for extended terms or discounts, increasing buyer bargaining power and pressuring margins. Strong credit management, risk scoring and disciplined collections helped US LBM protect profitability amid greater payment flexibility demands.

- Higher buyer power: more term/discount requests

- Cash sensitivity: elevated by 2024 rate environment

- Defense: credit scoring, collections, lien-waivers

Omnichannel and price transparency

Omnichannel tools—pro desks, e-commerce and digital quoting—have increased price discovery across US LBM’s network, letting commercial buyers benchmark distributors and big-box channels in real time; industry reports in 2024 show digital ordering penetration rising in professional channels. Price transparency compresses gross margins on like-for-like SKUs, while bundling and value-add services preserve total ticket economics and share of wallet.

- Pro desks improve retention

- E-commerce raises benchmarking

- Transparency compresses SKU margins

- Bundles defend ticket value

Pro builders squeeze margins; pro forma revenue near $10B in 2024

Large pro builders exert strong leverage—multi-project bids and volume rebates compress distributor margins despite stable contract visibility; US LBM pro forma revenue approached $10 billion in 2024.

Remodelers and small contractors dilute collective pricing power; US LBM’s 260+ local branches and service focus limit switching on mixed baskets while ~40% of volumes remain price-sensitive.

Higher 2024 fed funds (5.25–5.50%) increased term/discount requests; credit scoring and collections protected margins.

| Metric | 2024 |

|---|---|

| Pro forma revenue | $~10B |

| Branches | 260+ |

| Price-switchable volume | ~40% |

| Federal funds rate | 5.25–5.50% |

Same Document Delivered

US LBM Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for US LBM Holdings you'll receive immediately after purchase—no placeholders, no mockups. The document is professionally written, fully formatted, and ready for download and use the moment you buy. You're looking at the final deliverable, the same file available for instant access after payment.