US Steel Porter's Five Forces Analysis

Don't Miss the Bigger Picture

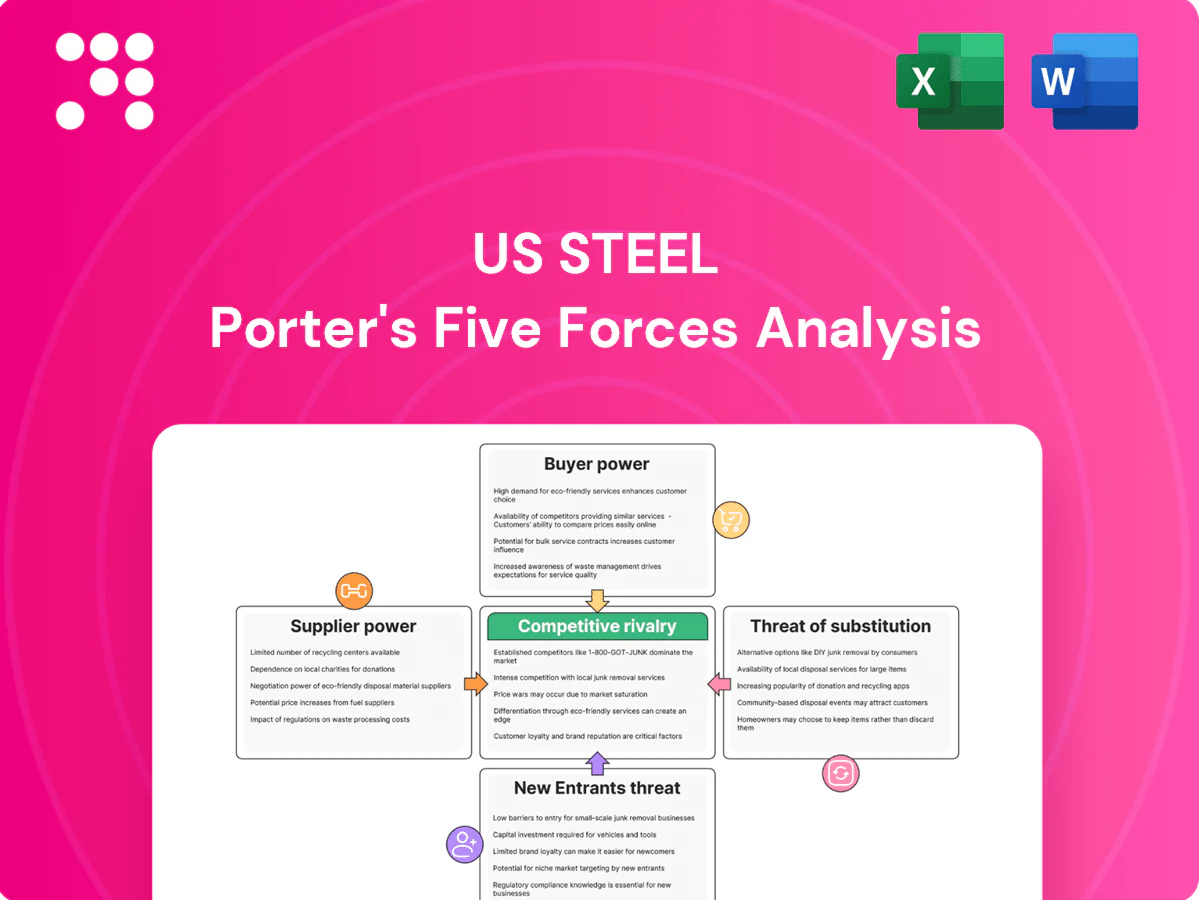

US Steel faces intense competitive pressures—volatile commodity prices, strong buyer negotiation, and concentrated supplier influence shape margins and strategic choices. Rivalry from global mills and cyclic demand heighten risk while substitutes and incremental automation shift cost dynamics. This snapshot highlights key tensions; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Upstream integration dampens input leverage

As of 2024 U.S. Steel operates integrated facilities including iron-ore mining and coke production, which lowers reliance on third-party raw materials. This vertical integration reduces exposure to input price spikes and supply disruptions, improving margin resilience. Not all inputs are captive, so residual supply and price risk persists. Integration also strengthens U.S. Steel's negotiation leverage with external suppliers.

Critical inputs still concentrated

Critical inputs like high-grade coking coal, alloying elements (nickel, molybdenum), refractories and specialty electrodes are sourced from a handful of global suppliers—Australia accounted for about 54% of seaborne coking coal exports in 2024—concentrating supplier power and raising switching costs and pricing leverage. Rail and barge bottlenecks in US logistics further amplify supplier leverage, though multi-year contracts partially mitigate spot volatility.

Energy and logistics as quasi-suppliers

Electricity, natural gas and transport providers act as quasi-suppliers for US Steel: regional utility monopolies and Class I rail concentration (four carriers move roughly 90% of US rail freight) create leverage and capacity tightness. Steelmaking is energy-intensive, with fuel and power often representing double-digit shares of production cost, so pass-through clauses are critical. Disruptions raise input costs and force furnace schedule changes; hedging and multi-sourcing are standard mitigants. In 2024 Henry Hub averaged about 2.9 USD/MMBtu and US industrial electricity hovered near 0.08 USD/kWh, underscoring exposure.

Equipment and technology dependence

Blast furnace, caster and mill OEMs supply highly specialized parts and services, giving suppliers leverage through limited alternatives. Proprietary automation and maintenance contracts create lock-in and recurring revenue streams that raise switching costs. High downtime risk in steelmaking increases firms willingness to pay for rapid OEM support, while digitalization partners (IIoT, control software) add a new layer of supplier influence.

- Specialized OEM dependence

- Proprietary automation lock-in

- Downtime raises supplier leverage

- Digital partners = new supplier power

ESG and compliance constraints

ESG-driven environmental standards for low-impurity ores and certified metallurgical coal have narrowed supplier pools for US Steel, and in 2024 compliance documentation and third-party audits became more prevalent, increasing switching barriers. Suppliers meeting ESG criteria command premiums and can tighten supply during the industry transition to lower-carbon steelmaking, affecting feedstock availability and cost.

- 2024: rising audit frequency raised onboarding time for new suppliers

- ESG-certified suppliers can demand price premiums

- Supply tightness likely during decarbonization transitions

Vertical integration trims ore risk; coal, rail and energy concentration keep supplier leverage

Vertical integration (captive iron-ore, coke) lowers US Steel's raw-material dependency but residual supplier risk remains. Coking-coal supply concentrated (Australia ≈54% seaborne exports in 2024) and Class I rail (4 carriers ≈90% US freight) amplify supplier leverage. Energy exposure (Henry Hub ≈2.9 USD/MMBtu; US industrial power ≈0.08 USD/kWh) and specialized OEM lock-in raise switching costs.

| Metric | 2024 Value | Implication |

|---|---|---|

| Australia seaborne coking coal | ≈54% | concentrated supply |

| Class I rail share | ≈90% | logistics leverage |

| Henry Hub / power | 2.9 USD/MMBtu / 0.08 USD/kWh | energy cost risk |

What is included in the product

Concise Porter's Five Forces assessment of US Steel, detailing competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

A clear, one-sheet Porter’s Five Forces summary for U.S. Steel—instantly assess competitive pressures, supplier/customer leverage, and strategic threats to speed boardroom decisions and scenario planning.

Customers Bargaining Power

Automotive OEMs highly concentrated

A few large carmakers dominate demand—top five OEMs accounted for roughly 65% of US light-vehicle production in 2024—buying high volumes to strict specs, which gives them significant bargaining leverage. Annual contracts, widespread dual-sourcing and competitive bidding compress supplier margins. Qualification requirements are stringent but surmountable, while price-indexed contracts tied to steel and scrap indices in 2024 tempered spot volatility and anchored routine discounts.

Industrial and construction buyers fragmented

Appliance, machinery, and construction buyers are highly fragmented, reducing individual bargaining leverage versus concentrated auto OEMs; construction alone represented about $1.9 trillion in U.S. put-in-place spending in 2023 (U.S. Census Bureau). Distributors and service centers consolidate purchases, capturing significant aggregator power and smoothing order flow. However, project-based demand causes seasonal spikes and brief windows of heightened price sensitivity.

Switching costs moderate with qualification

As of 2024, switching costs for advanced high-strength steels and tubulars remain moderate because testing and mill approvals create stickiness for specific grades. Buyers, however, commonly pre-qualify multiple mills to preserve leverage and pricing flexibility. Substitution to EAF competitors is feasible on commodity grades, increasing buyer bargaining power. Robust technical service and application support can meaningfully reduce churn.

Price transparency and indices

Benchmarks like the CRU US HRC index (averaging about $700/short ton in 2024) raise buyer information and negotiation strength, with buyers increasingly questioning alloy and freight surcharges. Procurement teams time purchases to spot-price dips, and indexation has narrowed spot-to-contract spreads, compressing premium capture in oversupplied markets.

- CRU/HRC: higher transparency

- Surcharges: greater scrutiny

- Timing: purchases skew to dips

- Indexation: premiums compressed

Cyclical demand amplifies power swings

Cyclical demand makes buyers swing from weak to strong leverage: in downturns buyers delay orders and extract price and payment concessions, while in tight markets 2024 capacity constraints and allocations flipped leverage to suppliers. Import availability—imports were about 25% of U.S. apparent steel consumption in 2024—and the 25% Section 232 tariff shape viable alternatives. Service centers holding roughly 60 days of inventory in 2024 can tighten or loosen near-term pricing power.

- Downturns: deferred orders, concession pressure

- Tight markets: allocations shift power to suppliers

- Imports ~25% (2024); 25% tariff affects alternatives

- Service centers ≈60 days inventory — impacts short-term pricing

Top-5 OEMs dominate pricing; imports and cyclicality shift buyer leverage

Large OEMs (top five ≈65% of US light-vehicle production in 2024) exert strong bargaining power via volume, specs and dual-sourcing; appliance/construction buyers are fragmented and weaker. Indexation (CRU HRC ≈$700/st in 2024) and procurement timing compress premiums; switching costs for AHSS moderate but multi-qualification preserves buyer leverage. Cyclicality and imports (~25% of consumption, 2024) shift power seasonally.

| Metric | 2024 |

|---|---|

| Top-5 OEM share | ≈65% |

| CRU US HRC | $700/short ton |

| Imports | ≈25% |

| Service center days | ≈60 |

Same Document Delivered

US Steel Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for U.S. Steel you’ll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document ready for instant download and use upon payment. What you see is the deliverable.

Don't Miss the Bigger Picture

US Steel faces intense competitive pressures—volatile commodity prices, strong buyer negotiation, and concentrated supplier influence shape margins and strategic choices. Rivalry from global mills and cyclic demand heighten risk while substitutes and incremental automation shift cost dynamics. This snapshot highlights key tensions; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Upstream integration dampens input leverage

As of 2024 U.S. Steel operates integrated facilities including iron-ore mining and coke production, which lowers reliance on third-party raw materials. This vertical integration reduces exposure to input price spikes and supply disruptions, improving margin resilience. Not all inputs are captive, so residual supply and price risk persists. Integration also strengthens U.S. Steel's negotiation leverage with external suppliers.

Critical inputs still concentrated

Critical inputs like high-grade coking coal, alloying elements (nickel, molybdenum), refractories and specialty electrodes are sourced from a handful of global suppliers—Australia accounted for about 54% of seaborne coking coal exports in 2024—concentrating supplier power and raising switching costs and pricing leverage. Rail and barge bottlenecks in US logistics further amplify supplier leverage, though multi-year contracts partially mitigate spot volatility.

Energy and logistics as quasi-suppliers

Electricity, natural gas and transport providers act as quasi-suppliers for US Steel: regional utility monopolies and Class I rail concentration (four carriers move roughly 90% of US rail freight) create leverage and capacity tightness. Steelmaking is energy-intensive, with fuel and power often representing double-digit shares of production cost, so pass-through clauses are critical. Disruptions raise input costs and force furnace schedule changes; hedging and multi-sourcing are standard mitigants. In 2024 Henry Hub averaged about 2.9 USD/MMBtu and US industrial electricity hovered near 0.08 USD/kWh, underscoring exposure.

Equipment and technology dependence

Blast furnace, caster and mill OEMs supply highly specialized parts and services, giving suppliers leverage through limited alternatives. Proprietary automation and maintenance contracts create lock-in and recurring revenue streams that raise switching costs. High downtime risk in steelmaking increases firms willingness to pay for rapid OEM support, while digitalization partners (IIoT, control software) add a new layer of supplier influence.

- Specialized OEM dependence

- Proprietary automation lock-in

- Downtime raises supplier leverage

- Digital partners = new supplier power

ESG and compliance constraints

ESG-driven environmental standards for low-impurity ores and certified metallurgical coal have narrowed supplier pools for US Steel, and in 2024 compliance documentation and third-party audits became more prevalent, increasing switching barriers. Suppliers meeting ESG criteria command premiums and can tighten supply during the industry transition to lower-carbon steelmaking, affecting feedstock availability and cost.

- 2024: rising audit frequency raised onboarding time for new suppliers

- ESG-certified suppliers can demand price premiums

- Supply tightness likely during decarbonization transitions

Vertical integration trims ore risk; coal, rail and energy concentration keep supplier leverage

Vertical integration (captive iron-ore, coke) lowers US Steel's raw-material dependency but residual supplier risk remains. Coking-coal supply concentrated (Australia ≈54% seaborne exports in 2024) and Class I rail (4 carriers ≈90% US freight) amplify supplier leverage. Energy exposure (Henry Hub ≈2.9 USD/MMBtu; US industrial power ≈0.08 USD/kWh) and specialized OEM lock-in raise switching costs.

| Metric | 2024 Value | Implication |

|---|---|---|

| Australia seaborne coking coal | ≈54% | concentrated supply |

| Class I rail share | ≈90% | logistics leverage |

| Henry Hub / power | 2.9 USD/MMBtu / 0.08 USD/kWh | energy cost risk |

What is included in the product

Concise Porter's Five Forces assessment of US Steel, detailing competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

A clear, one-sheet Porter’s Five Forces summary for U.S. Steel—instantly assess competitive pressures, supplier/customer leverage, and strategic threats to speed boardroom decisions and scenario planning.

Customers Bargaining Power

Automotive OEMs highly concentrated

A few large carmakers dominate demand—top five OEMs accounted for roughly 65% of US light-vehicle production in 2024—buying high volumes to strict specs, which gives them significant bargaining leverage. Annual contracts, widespread dual-sourcing and competitive bidding compress supplier margins. Qualification requirements are stringent but surmountable, while price-indexed contracts tied to steel and scrap indices in 2024 tempered spot volatility and anchored routine discounts.

Industrial and construction buyers fragmented

Appliance, machinery, and construction buyers are highly fragmented, reducing individual bargaining leverage versus concentrated auto OEMs; construction alone represented about $1.9 trillion in U.S. put-in-place spending in 2023 (U.S. Census Bureau). Distributors and service centers consolidate purchases, capturing significant aggregator power and smoothing order flow. However, project-based demand causes seasonal spikes and brief windows of heightened price sensitivity.

Switching costs moderate with qualification

As of 2024, switching costs for advanced high-strength steels and tubulars remain moderate because testing and mill approvals create stickiness for specific grades. Buyers, however, commonly pre-qualify multiple mills to preserve leverage and pricing flexibility. Substitution to EAF competitors is feasible on commodity grades, increasing buyer bargaining power. Robust technical service and application support can meaningfully reduce churn.

Price transparency and indices

Benchmarks like the CRU US HRC index (averaging about $700/short ton in 2024) raise buyer information and negotiation strength, with buyers increasingly questioning alloy and freight surcharges. Procurement teams time purchases to spot-price dips, and indexation has narrowed spot-to-contract spreads, compressing premium capture in oversupplied markets.

- CRU/HRC: higher transparency

- Surcharges: greater scrutiny

- Timing: purchases skew to dips

- Indexation: premiums compressed

Cyclical demand amplifies power swings

Cyclical demand makes buyers swing from weak to strong leverage: in downturns buyers delay orders and extract price and payment concessions, while in tight markets 2024 capacity constraints and allocations flipped leverage to suppliers. Import availability—imports were about 25% of U.S. apparent steel consumption in 2024—and the 25% Section 232 tariff shape viable alternatives. Service centers holding roughly 60 days of inventory in 2024 can tighten or loosen near-term pricing power.

- Downturns: deferred orders, concession pressure

- Tight markets: allocations shift power to suppliers

- Imports ~25% (2024); 25% tariff affects alternatives

- Service centers ≈60 days inventory — impacts short-term pricing

Top-5 OEMs dominate pricing; imports and cyclicality shift buyer leverage

Large OEMs (top five ≈65% of US light-vehicle production in 2024) exert strong bargaining power via volume, specs and dual-sourcing; appliance/construction buyers are fragmented and weaker. Indexation (CRU HRC ≈$700/st in 2024) and procurement timing compress premiums; switching costs for AHSS moderate but multi-qualification preserves buyer leverage. Cyclicality and imports (~25% of consumption, 2024) shift power seasonally.

| Metric | 2024 |

|---|---|

| Top-5 OEM share | ≈65% |

| CRU US HRC | $700/short ton |

| Imports | ≈25% |

| Service center days | ≈60 |

Same Document Delivered

US Steel Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for U.S. Steel you’ll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document ready for instant download and use upon payment. What you see is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

US Steel faces intense competitive pressures—volatile commodity prices, strong buyer negotiation, and concentrated supplier influence shape margins and strategic choices. Rivalry from global mills and cyclic demand heighten risk while substitutes and incremental automation shift cost dynamics. This snapshot highlights key tensions; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or corporate decisions.

Suppliers Bargaining Power

Upstream integration dampens input leverage

As of 2024 U.S. Steel operates integrated facilities including iron-ore mining and coke production, which lowers reliance on third-party raw materials. This vertical integration reduces exposure to input price spikes and supply disruptions, improving margin resilience. Not all inputs are captive, so residual supply and price risk persists. Integration also strengthens U.S. Steel's negotiation leverage with external suppliers.

Critical inputs still concentrated

Critical inputs like high-grade coking coal, alloying elements (nickel, molybdenum), refractories and specialty electrodes are sourced from a handful of global suppliers—Australia accounted for about 54% of seaborne coking coal exports in 2024—concentrating supplier power and raising switching costs and pricing leverage. Rail and barge bottlenecks in US logistics further amplify supplier leverage, though multi-year contracts partially mitigate spot volatility.

Energy and logistics as quasi-suppliers

Electricity, natural gas and transport providers act as quasi-suppliers for US Steel: regional utility monopolies and Class I rail concentration (four carriers move roughly 90% of US rail freight) create leverage and capacity tightness. Steelmaking is energy-intensive, with fuel and power often representing double-digit shares of production cost, so pass-through clauses are critical. Disruptions raise input costs and force furnace schedule changes; hedging and multi-sourcing are standard mitigants. In 2024 Henry Hub averaged about 2.9 USD/MMBtu and US industrial electricity hovered near 0.08 USD/kWh, underscoring exposure.

Equipment and technology dependence

Blast furnace, caster and mill OEMs supply highly specialized parts and services, giving suppliers leverage through limited alternatives. Proprietary automation and maintenance contracts create lock-in and recurring revenue streams that raise switching costs. High downtime risk in steelmaking increases firms willingness to pay for rapid OEM support, while digitalization partners (IIoT, control software) add a new layer of supplier influence.

- Specialized OEM dependence

- Proprietary automation lock-in

- Downtime raises supplier leverage

- Digital partners = new supplier power

ESG and compliance constraints

ESG-driven environmental standards for low-impurity ores and certified metallurgical coal have narrowed supplier pools for US Steel, and in 2024 compliance documentation and third-party audits became more prevalent, increasing switching barriers. Suppliers meeting ESG criteria command premiums and can tighten supply during the industry transition to lower-carbon steelmaking, affecting feedstock availability and cost.

- 2024: rising audit frequency raised onboarding time for new suppliers

- ESG-certified suppliers can demand price premiums

- Supply tightness likely during decarbonization transitions

Vertical integration trims ore risk; coal, rail and energy concentration keep supplier leverage

Vertical integration (captive iron-ore, coke) lowers US Steel's raw-material dependency but residual supplier risk remains. Coking-coal supply concentrated (Australia ≈54% seaborne exports in 2024) and Class I rail (4 carriers ≈90% US freight) amplify supplier leverage. Energy exposure (Henry Hub ≈2.9 USD/MMBtu; US industrial power ≈0.08 USD/kWh) and specialized OEM lock-in raise switching costs.

| Metric | 2024 Value | Implication |

|---|---|---|

| Australia seaborne coking coal | ≈54% | concentrated supply |

| Class I rail share | ≈90% | logistics leverage |

| Henry Hub / power | 2.9 USD/MMBtu / 0.08 USD/kWh | energy cost risk |

What is included in the product

Concise Porter's Five Forces assessment of US Steel, detailing competitive rivalry, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

A clear, one-sheet Porter’s Five Forces summary for U.S. Steel—instantly assess competitive pressures, supplier/customer leverage, and strategic threats to speed boardroom decisions and scenario planning.

Customers Bargaining Power

Automotive OEMs highly concentrated

A few large carmakers dominate demand—top five OEMs accounted for roughly 65% of US light-vehicle production in 2024—buying high volumes to strict specs, which gives them significant bargaining leverage. Annual contracts, widespread dual-sourcing and competitive bidding compress supplier margins. Qualification requirements are stringent but surmountable, while price-indexed contracts tied to steel and scrap indices in 2024 tempered spot volatility and anchored routine discounts.

Industrial and construction buyers fragmented

Appliance, machinery, and construction buyers are highly fragmented, reducing individual bargaining leverage versus concentrated auto OEMs; construction alone represented about $1.9 trillion in U.S. put-in-place spending in 2023 (U.S. Census Bureau). Distributors and service centers consolidate purchases, capturing significant aggregator power and smoothing order flow. However, project-based demand causes seasonal spikes and brief windows of heightened price sensitivity.

Switching costs moderate with qualification

As of 2024, switching costs for advanced high-strength steels and tubulars remain moderate because testing and mill approvals create stickiness for specific grades. Buyers, however, commonly pre-qualify multiple mills to preserve leverage and pricing flexibility. Substitution to EAF competitors is feasible on commodity grades, increasing buyer bargaining power. Robust technical service and application support can meaningfully reduce churn.

Price transparency and indices

Benchmarks like the CRU US HRC index (averaging about $700/short ton in 2024) raise buyer information and negotiation strength, with buyers increasingly questioning alloy and freight surcharges. Procurement teams time purchases to spot-price dips, and indexation has narrowed spot-to-contract spreads, compressing premium capture in oversupplied markets.

- CRU/HRC: higher transparency

- Surcharges: greater scrutiny

- Timing: purchases skew to dips

- Indexation: premiums compressed

Cyclical demand amplifies power swings

Cyclical demand makes buyers swing from weak to strong leverage: in downturns buyers delay orders and extract price and payment concessions, while in tight markets 2024 capacity constraints and allocations flipped leverage to suppliers. Import availability—imports were about 25% of U.S. apparent steel consumption in 2024—and the 25% Section 232 tariff shape viable alternatives. Service centers holding roughly 60 days of inventory in 2024 can tighten or loosen near-term pricing power.

- Downturns: deferred orders, concession pressure

- Tight markets: allocations shift power to suppliers

- Imports ~25% (2024); 25% tariff affects alternatives

- Service centers ≈60 days inventory — impacts short-term pricing

Top-5 OEMs dominate pricing; imports and cyclicality shift buyer leverage

Large OEMs (top five ≈65% of US light-vehicle production in 2024) exert strong bargaining power via volume, specs and dual-sourcing; appliance/construction buyers are fragmented and weaker. Indexation (CRU HRC ≈$700/st in 2024) and procurement timing compress premiums; switching costs for AHSS moderate but multi-qualification preserves buyer leverage. Cyclicality and imports (~25% of consumption, 2024) shift power seasonally.

| Metric | 2024 |

|---|---|

| Top-5 OEM share | ≈65% |

| CRU US HRC | $700/short ton |

| Imports | ≈25% |

| Service center days | ≈60 |

Same Document Delivered

US Steel Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for U.S. Steel you’ll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document ready for instant download and use upon payment. What you see is the deliverable.