Universal Technical Institute Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

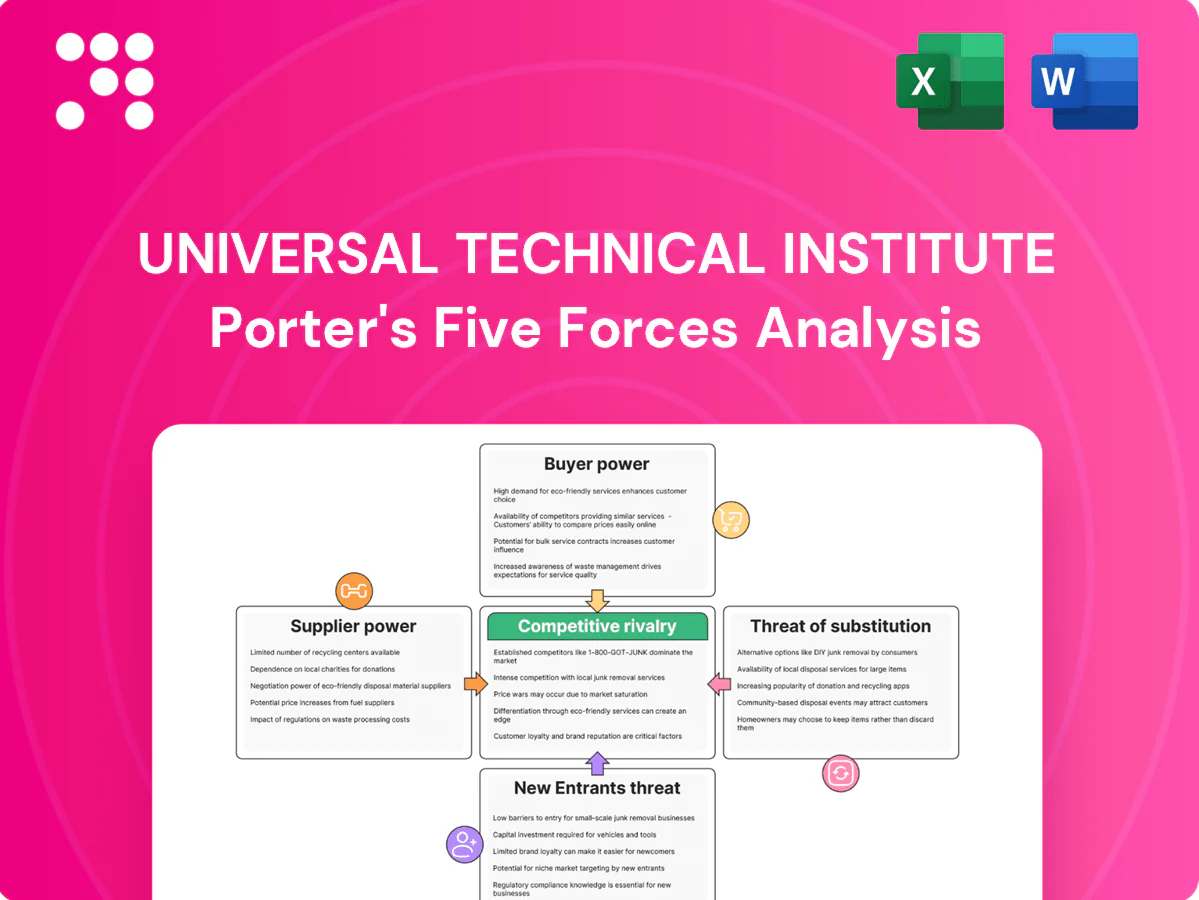

Universal Technical Institute faces moderate buyer power, concentrated supplier relationships for training equipment, limited substitute threats but rising online alternatives, and barriers to new entrants tempered by accreditation requirements. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Universal Technical Institute’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on OEM partners

UTI depends on OEM partners such as Ford, GM, Toyota, Honda, BMW and Harley-Davidson for curriculum alignment, branded programs and placement pipelines; these partners can dictate program content, co-branding and revenue-sharing terms. Losing or switching a marquee OEM raises student demand risk and increases marketing and recruitment costs. Diversifying across multiple OEMs reduces but does not eliminate their bargaining power as of 2024.

Specialized equipment vendors

Labs require proprietary diagnostic tools, engines, simulators, and fixtures supplied by a small set of OEM vendors, giving suppliers strong leverage; lead times commonly run 8–12 weeks and maintenance contracts 1–5 years. Vendor concentration and high switching costs raise pricing and service control, though bulk purchasing and multi-campus standardization can secure 5–15% discounts and reduced unit costs.

Accreditation and testing inputs

Accrediting bodies such as NATEF and ASE drive curriculum standards and assessment materials, with reaccreditation cycles typically every 5 years (NATEF as of 2024); their specifications effectively shape program design. Compliance costs and periodic standard changes act as supplier power, forcing curricular updates and capital investment. Non-compliance can revoke Title IV eligibility administered by the US Dept of Education and erode employer trust. Early alignment with accreditors reduces risk of disruptive rework.

Skilled instructor labor

Experienced technician-instructors are scarce and command premium wages; BLS 2023 median pay for automotive technicians was about 48,880, and instructor premiums often run 20–35% higher, raising labor cost. Competition from OEMs and repair shops increases hiring and retention costs, capping cohort sizes and limiting program expansion. Grow-your-own pipelines and adjunct models partially alleviate pressure but require upfront investment.

- High instructor pay

- Industry hiring competition

- Cohort size caps

- Grow-your-own, adjunct relief

Facilities and digital platforms

Facilities and digital platforms are critical inputs: large shop spaces, leased campuses and LMS/simulation software represent concentrated supplier power; long-term campus leases (typically 5–15 years) and multi-year software integrations raise switching costs. Landlords and vendors pushed price increases in 2024—software license inflation near 8% and commercial rent growth around 4–6%—squeezing margins. Portfolio optimization and tougher vendor negotiations (consolidation of suppliers, RFPs) are primary levers to rebalance terms.

- Concentrated inputs: leased campuses, shop space, LMS

- Switching barriers: 5–15 year leases, integration costs

- 2024 pressure: ~8% software price inflation, ~4–6% rent growth

- Mitigants: portfolio optimization, vendor consolidation, renegotiation

Tech training hit by OEM/vendor leverage, instructor shortage and rising rent/software costs

UTI is highly dependent on OEM partners for curriculum, branding and placements, giving OEMs strong leverage. Proprietary lab vendors and long lead times (8–12 weeks) raise supplier power and switching costs. Accrediting bodies and scarce instructor labor (BLS 2023 median tech pay $48,880; instructor premiums +20–35%) further constrain flexibility. Leases/software inflation (rent +4–6%, software ~8% in 2024) squeeze margins.

| Input | Supplier power | 2024 metric |

|---|---|---|

| OEM partners | High | 6+ marquee OEMs; co-branding control |

| Diagnostic vendors | High | Lead times 8–12 weeks |

| Instructors | High | Tech median $48,880 (2023); instructor +20–35% |

| Leases/software | Med-High | Rent +4–6%, software +~8% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Universal Technical Institute that uncovers competitive rivalry, supplier and buyer power, threat of substitutes and entry risks, identifies disruptive trends and strategic levers to protect market share.

A concise one-sheet Porter's Five Forces for Universal Technical Institute—instantly maps competitive pressures to relieve analysis overload and is ready to drop into decks or tweak with your own data.

Customers Bargaining Power

Price-sensitive students

Price-sensitive students compare UTI tuition, time-to-completion and job outcomes across alternatives, leaning heavily on transparent placement rates and published median earnings when assessing value-for-money. Access to federal Title IV aid increases enrollment options but heightens scrutiny of return on investment. Scholarships and flexible schedules measurably reduce churn by improving affordability and retention.

Employer partners as co-buyers

Employer partners act as co-buyers at Universal Technical Institute, with the company disclosing more than 3,000 employer partnerships as of 2024, allowing employers to influence program content, sponsorships, and hiring commitments. They request customized cohorts, outcome guarantees, or tuition-assistance terms, leveraging strong placement pipelines to affect seat allocation and curriculum cadence. Deeper partnerships that include guaranteed hires or funded cohorts convert this leverage into enrollment stickiness.

Community college alternatives

Lower-cost community college programs, often under $10,000 per year, give buyers credible alternatives to UTI’s career-focused programs costing roughly $48,000 per diploma, enabling students to negotiate or switch in overlapping geographies. UTI must justify its premium with faster completion, strong brand recognition and direct OEM alignment (Ford, GM, Toyota). Published outcome data and employer endorsements—UTI reports roughly 70–75% placement—help counter pure price pressure.

Information transparency

Online reviews (98% of consumers consult reviews per BrightLocal 2024), UTIs reported alumni base of about 300,000, and public outcome disclosures raise buyer sophistication and amplify switching and negotiation power; any gap between marketed and realized graduate earnings quickly erodes pricing power while proactive outcome reporting sustains trust.

- Online reviews: 98% consult reviews (BrightLocal 2024)

- Alumni network: ~300,000 graduates

- Transparency: increases switching/negotiation power

- Outcome gaps: rapid pricing erosion

- Proactive reporting: sustains trust

Geographic and modality choice

Multiple campuses (17 in 2024) lower travel barriers for Universal Technical Institute students, but commuting or relocation costs still affect enrollment decisions; hybrid/online theory modules, up ~30% in 2023–24, broaden buyer options and comparison shopping. Flexible start dates and blended delivery cut buyer leverage by improving fit; strong local employer demand in regions with low technician supply pushes pricing and placement dynamics.

- Campuses: 17 (2024)

- Hybrid theory growth: +30% (2023–24)

- Flexible starts reduce churn

- Regional employer demand tightens pricing

Buyer power moderate: $48k, 70–75% placement, >3,000

Students and employer-buyers exert moderate bargaining power, comparing UTI tuition (~$48,000/diploma), placement (70–75%) and alternatives (community college < $10,000). Employer partners (>3,000 in 2024) influence curriculum and funded cohorts, increasing leverage. Transparency (98% consult reviews; alumni ~300,000) raises switching risk, while 17 campuses and +30% hybrid growth partly reduce buyer pressure.

| Metric | 2024 |

|---|---|

| Tuition | $48,000 |

| Placement | 70–75% |

| Employer partners | >3,000 |

| Alumni | ~300,000 |

| Campuses | 17 |

Full Version Awaits

Universal Technical Institute Porter's Five Forces Analysis

This preview shows the exact Universal Technical Institute Porter’s Five Forces analysis you'll receive after purchase—no placeholders, no mockups. It contains the full competitive assessment including supplier and buyer power, rivalry, and threat analyses plus strategic implications. The file is fully formatted and ready for immediate download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Universal Technical Institute faces moderate buyer power, concentrated supplier relationships for training equipment, limited substitute threats but rising online alternatives, and barriers to new entrants tempered by accreditation requirements. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Universal Technical Institute’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on OEM partners

UTI depends on OEM partners such as Ford, GM, Toyota, Honda, BMW and Harley-Davidson for curriculum alignment, branded programs and placement pipelines; these partners can dictate program content, co-branding and revenue-sharing terms. Losing or switching a marquee OEM raises student demand risk and increases marketing and recruitment costs. Diversifying across multiple OEMs reduces but does not eliminate their bargaining power as of 2024.

Specialized equipment vendors

Labs require proprietary diagnostic tools, engines, simulators, and fixtures supplied by a small set of OEM vendors, giving suppliers strong leverage; lead times commonly run 8–12 weeks and maintenance contracts 1–5 years. Vendor concentration and high switching costs raise pricing and service control, though bulk purchasing and multi-campus standardization can secure 5–15% discounts and reduced unit costs.

Accreditation and testing inputs

Accrediting bodies such as NATEF and ASE drive curriculum standards and assessment materials, with reaccreditation cycles typically every 5 years (NATEF as of 2024); their specifications effectively shape program design. Compliance costs and periodic standard changes act as supplier power, forcing curricular updates and capital investment. Non-compliance can revoke Title IV eligibility administered by the US Dept of Education and erode employer trust. Early alignment with accreditors reduces risk of disruptive rework.

Skilled instructor labor

Experienced technician-instructors are scarce and command premium wages; BLS 2023 median pay for automotive technicians was about 48,880, and instructor premiums often run 20–35% higher, raising labor cost. Competition from OEMs and repair shops increases hiring and retention costs, capping cohort sizes and limiting program expansion. Grow-your-own pipelines and adjunct models partially alleviate pressure but require upfront investment.

- High instructor pay

- Industry hiring competition

- Cohort size caps

- Grow-your-own, adjunct relief

Facilities and digital platforms

Facilities and digital platforms are critical inputs: large shop spaces, leased campuses and LMS/simulation software represent concentrated supplier power; long-term campus leases (typically 5–15 years) and multi-year software integrations raise switching costs. Landlords and vendors pushed price increases in 2024—software license inflation near 8% and commercial rent growth around 4–6%—squeezing margins. Portfolio optimization and tougher vendor negotiations (consolidation of suppliers, RFPs) are primary levers to rebalance terms.

- Concentrated inputs: leased campuses, shop space, LMS

- Switching barriers: 5–15 year leases, integration costs

- 2024 pressure: ~8% software price inflation, ~4–6% rent growth

- Mitigants: portfolio optimization, vendor consolidation, renegotiation

Tech training hit by OEM/vendor leverage, instructor shortage and rising rent/software costs

UTI is highly dependent on OEM partners for curriculum, branding and placements, giving OEMs strong leverage. Proprietary lab vendors and long lead times (8–12 weeks) raise supplier power and switching costs. Accrediting bodies and scarce instructor labor (BLS 2023 median tech pay $48,880; instructor premiums +20–35%) further constrain flexibility. Leases/software inflation (rent +4–6%, software ~8% in 2024) squeeze margins.

| Input | Supplier power | 2024 metric |

|---|---|---|

| OEM partners | High | 6+ marquee OEMs; co-branding control |

| Diagnostic vendors | High | Lead times 8–12 weeks |

| Instructors | High | Tech median $48,880 (2023); instructor +20–35% |

| Leases/software | Med-High | Rent +4–6%, software +~8% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Universal Technical Institute that uncovers competitive rivalry, supplier and buyer power, threat of substitutes and entry risks, identifies disruptive trends and strategic levers to protect market share.

A concise one-sheet Porter's Five Forces for Universal Technical Institute—instantly maps competitive pressures to relieve analysis overload and is ready to drop into decks or tweak with your own data.

Customers Bargaining Power

Price-sensitive students

Price-sensitive students compare UTI tuition, time-to-completion and job outcomes across alternatives, leaning heavily on transparent placement rates and published median earnings when assessing value-for-money. Access to federal Title IV aid increases enrollment options but heightens scrutiny of return on investment. Scholarships and flexible schedules measurably reduce churn by improving affordability and retention.

Employer partners as co-buyers

Employer partners act as co-buyers at Universal Technical Institute, with the company disclosing more than 3,000 employer partnerships as of 2024, allowing employers to influence program content, sponsorships, and hiring commitments. They request customized cohorts, outcome guarantees, or tuition-assistance terms, leveraging strong placement pipelines to affect seat allocation and curriculum cadence. Deeper partnerships that include guaranteed hires or funded cohorts convert this leverage into enrollment stickiness.

Community college alternatives

Lower-cost community college programs, often under $10,000 per year, give buyers credible alternatives to UTI’s career-focused programs costing roughly $48,000 per diploma, enabling students to negotiate or switch in overlapping geographies. UTI must justify its premium with faster completion, strong brand recognition and direct OEM alignment (Ford, GM, Toyota). Published outcome data and employer endorsements—UTI reports roughly 70–75% placement—help counter pure price pressure.

Information transparency

Online reviews (98% of consumers consult reviews per BrightLocal 2024), UTIs reported alumni base of about 300,000, and public outcome disclosures raise buyer sophistication and amplify switching and negotiation power; any gap between marketed and realized graduate earnings quickly erodes pricing power while proactive outcome reporting sustains trust.

- Online reviews: 98% consult reviews (BrightLocal 2024)

- Alumni network: ~300,000 graduates

- Transparency: increases switching/negotiation power

- Outcome gaps: rapid pricing erosion

- Proactive reporting: sustains trust

Geographic and modality choice

Multiple campuses (17 in 2024) lower travel barriers for Universal Technical Institute students, but commuting or relocation costs still affect enrollment decisions; hybrid/online theory modules, up ~30% in 2023–24, broaden buyer options and comparison shopping. Flexible start dates and blended delivery cut buyer leverage by improving fit; strong local employer demand in regions with low technician supply pushes pricing and placement dynamics.

- Campuses: 17 (2024)

- Hybrid theory growth: +30% (2023–24)

- Flexible starts reduce churn

- Regional employer demand tightens pricing

Buyer power moderate: $48k, 70–75% placement, >3,000

Students and employer-buyers exert moderate bargaining power, comparing UTI tuition (~$48,000/diploma), placement (70–75%) and alternatives (community college < $10,000). Employer partners (>3,000 in 2024) influence curriculum and funded cohorts, increasing leverage. Transparency (98% consult reviews; alumni ~300,000) raises switching risk, while 17 campuses and +30% hybrid growth partly reduce buyer pressure.

| Metric | 2024 |

|---|---|

| Tuition | $48,000 |

| Placement | 70–75% |

| Employer partners | >3,000 |

| Alumni | ~300,000 |

| Campuses | 17 |

Full Version Awaits

Universal Technical Institute Porter's Five Forces Analysis

This preview shows the exact Universal Technical Institute Porter’s Five Forces analysis you'll receive after purchase—no placeholders, no mockups. It contains the full competitive assessment including supplier and buyer power, rivalry, and threat analyses plus strategic implications. The file is fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Universal Technical Institute faces moderate buyer power, concentrated supplier relationships for training equipment, limited substitute threats but rising online alternatives, and barriers to new entrants tempered by accreditation requirements. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Universal Technical Institute’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on OEM partners

UTI depends on OEM partners such as Ford, GM, Toyota, Honda, BMW and Harley-Davidson for curriculum alignment, branded programs and placement pipelines; these partners can dictate program content, co-branding and revenue-sharing terms. Losing or switching a marquee OEM raises student demand risk and increases marketing and recruitment costs. Diversifying across multiple OEMs reduces but does not eliminate their bargaining power as of 2024.

Specialized equipment vendors

Labs require proprietary diagnostic tools, engines, simulators, and fixtures supplied by a small set of OEM vendors, giving suppliers strong leverage; lead times commonly run 8–12 weeks and maintenance contracts 1–5 years. Vendor concentration and high switching costs raise pricing and service control, though bulk purchasing and multi-campus standardization can secure 5–15% discounts and reduced unit costs.

Accreditation and testing inputs

Accrediting bodies such as NATEF and ASE drive curriculum standards and assessment materials, with reaccreditation cycles typically every 5 years (NATEF as of 2024); their specifications effectively shape program design. Compliance costs and periodic standard changes act as supplier power, forcing curricular updates and capital investment. Non-compliance can revoke Title IV eligibility administered by the US Dept of Education and erode employer trust. Early alignment with accreditors reduces risk of disruptive rework.

Skilled instructor labor

Experienced technician-instructors are scarce and command premium wages; BLS 2023 median pay for automotive technicians was about 48,880, and instructor premiums often run 20–35% higher, raising labor cost. Competition from OEMs and repair shops increases hiring and retention costs, capping cohort sizes and limiting program expansion. Grow-your-own pipelines and adjunct models partially alleviate pressure but require upfront investment.

- High instructor pay

- Industry hiring competition

- Cohort size caps

- Grow-your-own, adjunct relief

Facilities and digital platforms

Facilities and digital platforms are critical inputs: large shop spaces, leased campuses and LMS/simulation software represent concentrated supplier power; long-term campus leases (typically 5–15 years) and multi-year software integrations raise switching costs. Landlords and vendors pushed price increases in 2024—software license inflation near 8% and commercial rent growth around 4–6%—squeezing margins. Portfolio optimization and tougher vendor negotiations (consolidation of suppliers, RFPs) are primary levers to rebalance terms.

- Concentrated inputs: leased campuses, shop space, LMS

- Switching barriers: 5–15 year leases, integration costs

- 2024 pressure: ~8% software price inflation, ~4–6% rent growth

- Mitigants: portfolio optimization, vendor consolidation, renegotiation

Tech training hit by OEM/vendor leverage, instructor shortage and rising rent/software costs

UTI is highly dependent on OEM partners for curriculum, branding and placements, giving OEMs strong leverage. Proprietary lab vendors and long lead times (8–12 weeks) raise supplier power and switching costs. Accrediting bodies and scarce instructor labor (BLS 2023 median tech pay $48,880; instructor premiums +20–35%) further constrain flexibility. Leases/software inflation (rent +4–6%, software ~8% in 2024) squeeze margins.

| Input | Supplier power | 2024 metric |

|---|---|---|

| OEM partners | High | 6+ marquee OEMs; co-branding control |

| Diagnostic vendors | High | Lead times 8–12 weeks |

| Instructors | High | Tech median $48,880 (2023); instructor +20–35% |

| Leases/software | Med-High | Rent +4–6%, software +~8% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Universal Technical Institute that uncovers competitive rivalry, supplier and buyer power, threat of substitutes and entry risks, identifies disruptive trends and strategic levers to protect market share.

A concise one-sheet Porter's Five Forces for Universal Technical Institute—instantly maps competitive pressures to relieve analysis overload and is ready to drop into decks or tweak with your own data.

Customers Bargaining Power

Price-sensitive students

Price-sensitive students compare UTI tuition, time-to-completion and job outcomes across alternatives, leaning heavily on transparent placement rates and published median earnings when assessing value-for-money. Access to federal Title IV aid increases enrollment options but heightens scrutiny of return on investment. Scholarships and flexible schedules measurably reduce churn by improving affordability and retention.

Employer partners as co-buyers

Employer partners act as co-buyers at Universal Technical Institute, with the company disclosing more than 3,000 employer partnerships as of 2024, allowing employers to influence program content, sponsorships, and hiring commitments. They request customized cohorts, outcome guarantees, or tuition-assistance terms, leveraging strong placement pipelines to affect seat allocation and curriculum cadence. Deeper partnerships that include guaranteed hires or funded cohorts convert this leverage into enrollment stickiness.

Community college alternatives

Lower-cost community college programs, often under $10,000 per year, give buyers credible alternatives to UTI’s career-focused programs costing roughly $48,000 per diploma, enabling students to negotiate or switch in overlapping geographies. UTI must justify its premium with faster completion, strong brand recognition and direct OEM alignment (Ford, GM, Toyota). Published outcome data and employer endorsements—UTI reports roughly 70–75% placement—help counter pure price pressure.

Information transparency

Online reviews (98% of consumers consult reviews per BrightLocal 2024), UTIs reported alumni base of about 300,000, and public outcome disclosures raise buyer sophistication and amplify switching and negotiation power; any gap between marketed and realized graduate earnings quickly erodes pricing power while proactive outcome reporting sustains trust.

- Online reviews: 98% consult reviews (BrightLocal 2024)

- Alumni network: ~300,000 graduates

- Transparency: increases switching/negotiation power

- Outcome gaps: rapid pricing erosion

- Proactive reporting: sustains trust

Geographic and modality choice

Multiple campuses (17 in 2024) lower travel barriers for Universal Technical Institute students, but commuting or relocation costs still affect enrollment decisions; hybrid/online theory modules, up ~30% in 2023–24, broaden buyer options and comparison shopping. Flexible start dates and blended delivery cut buyer leverage by improving fit; strong local employer demand in regions with low technician supply pushes pricing and placement dynamics.

- Campuses: 17 (2024)

- Hybrid theory growth: +30% (2023–24)

- Flexible starts reduce churn

- Regional employer demand tightens pricing

Buyer power moderate: $48k, 70–75% placement, >3,000

Students and employer-buyers exert moderate bargaining power, comparing UTI tuition (~$48,000/diploma), placement (70–75%) and alternatives (community college < $10,000). Employer partners (>3,000 in 2024) influence curriculum and funded cohorts, increasing leverage. Transparency (98% consult reviews; alumni ~300,000) raises switching risk, while 17 campuses and +30% hybrid growth partly reduce buyer pressure.

| Metric | 2024 |

|---|---|

| Tuition | $48,000 |

| Placement | 70–75% |

| Employer partners | >3,000 |

| Alumni | ~300,000 |

| Campuses | 17 |

Full Version Awaits

Universal Technical Institute Porter's Five Forces Analysis

This preview shows the exact Universal Technical Institute Porter’s Five Forces analysis you'll receive after purchase—no placeholders, no mockups. It contains the full competitive assessment including supplier and buyer power, rivalry, and threat analyses plus strategic implications. The file is fully formatted and ready for immediate download and use.