Vale Porter's Five Forces Analysis

From Overview to Strategy Blueprint

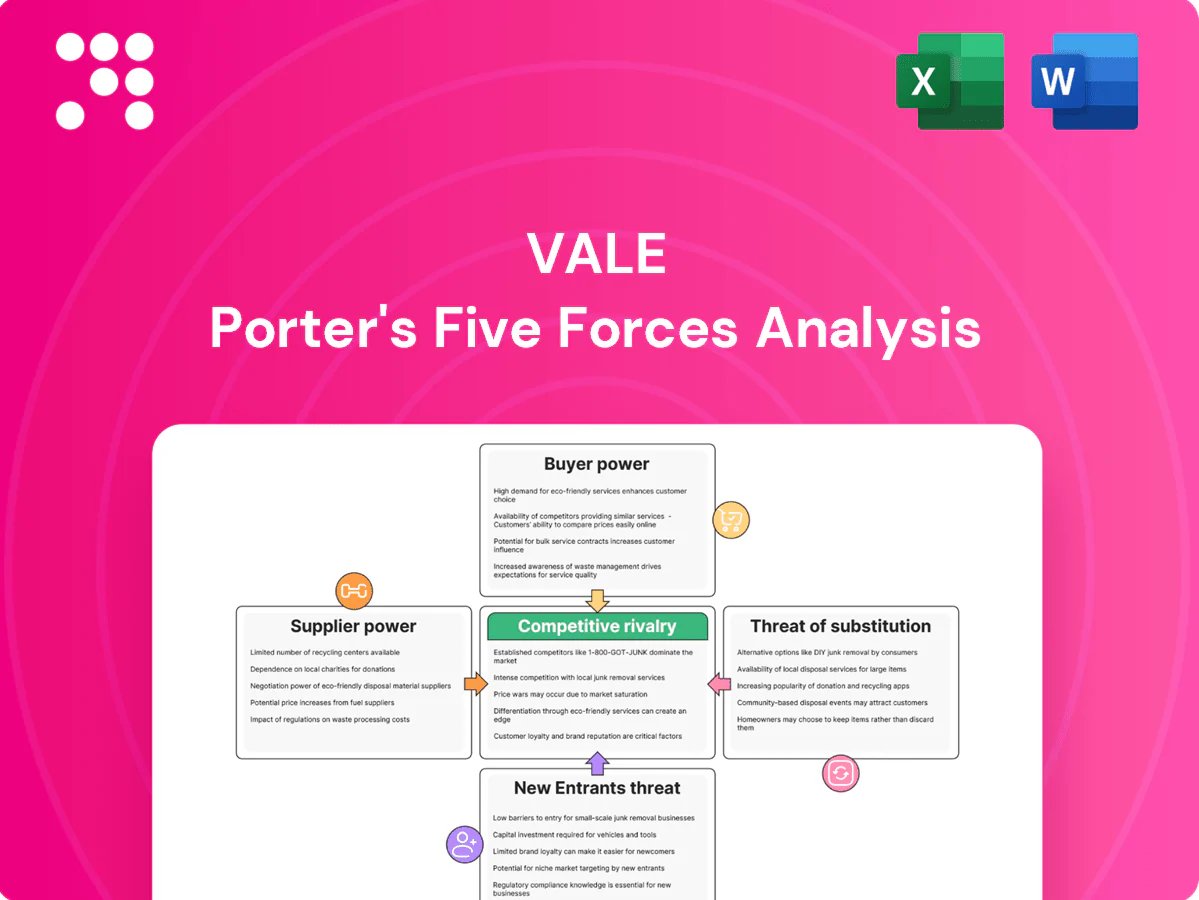

Vale's Porter’s Five Forces assessment highlights intense buyer and rival pressures, supplier leverage in key inputs, moderate threat from new entrants, and substitute risks tied to commodity cycles. This snapshot teases strategic levers and vulnerabilities. Unlock the full analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy.

Suppliers Bargaining Power

Concentrated critical equipment

In 2024 OEMs such as Caterpillar and Komatsu remained the dominant providers of large trucks, drills and autonomous systems, constraining Vale’s switching options and pressuring lead times and pricing. Vale’s scale supports framework agreements that lower unit costs and secure priority service, while maintenance, parts and software lock-in raise lifecycle dependence. Global OEM competition allows periodic rebids, providing limited leverage.

Energy and fuel exposure

Diesel, electricity and bunker fuel drive a material share of mining costs—commonly 20–35% of operating cash costs—and remained volatile through 2024. Long-term PPAs and fuel hedges blunt price swings but do not remove structural exposure to fuel-intensive inputs. Grid constraints in some Brazilian and Indonesian regions raise supplier leverage. Decarbonization pushed 2024 renewable PPA demand up ~25%, tightening terms from credible providers.

Logistics and maritime capacity

Deepwater ports, Brazilian rail links and Capesize shipping (which carry roughly 70% of seaborne iron ore) are critical for Vale’s exports, giving port and dredging providers leverage. Vale’s integrated logistics and owned tonnage reduce exposure, but tight third‑party freight markets can spike charter rates and handling costs. Dependence on specialized dredging and terminal services concentrates supplier power despite diversified chartering.

Specialized services and compliance

Specialized tailings management, geotechnical and environmental remediation firms command bargaining power due to scarce expertise; Vale’s post-Brumadinho liabilities (about $7.1 billion provision in 2019) highlight the financial stakes that raise demand for certified contractors under tighter ESG and safety regimes. Permitting or audit delays concentrate schedule leverage with suppliers, while multi-sourcing or insourcing can trim the premium.

- Scarce expertise → higher rates

- ESG/safety rules ↑ demand for certified contractors

- Permitting delays amplify supplier leverage

- Multi-sourcing/insourcing reduces premium

Labor and local stakeholders

Skilled labor, strong unions and community agreements act as quasi-suppliers of operational continuity for Vale; the company reported about 66,000 employees in 2023, concentrating bargaining power in regions with scarce labor. Regional shortages or strikes can lift wage bills and cut output; indigenous and community benefit agreements add legally binding non-price obligations. Long-term training pipelines and constructive engagement can reduce this supplier-like power over time.

- Skilled labor concentration: raises replacement cost and downtime risk

- Union influence: can trigger wage inflation and industrial action

- Community/Indigenous agreements: non-price commitments and social license costs

- Mitigants: training pipelines, local hiring, engagement

Supplier power fuels cost volatility: fuel, OEM constraints, ports, tailings, labor

OEMs (Caterpillar/Komatsu) constrained switching and pricing in 2024; Vale’s scale and framework deals moderate but not eliminate leverage. Fuel (diesel/electricity/bunkers) remained 20–35% of operating cash costs and volatile; renewable PPA demand rose ~25% in 2024. Ports/charters (Capesize ~70% of seaborne ore), specialized tailings (Brumadinho provision $7.1bn) and 66,000 employees concentrate supplier power.

| Supplier | 2024 indicator | Impact |

|---|---|---|

| OEMs | Frameworks; limited competition | Price/lead-time pressure |

| Fuel | 20–35% opex; PPA demand +25% | Cost volatility |

| Shipping/ports | Capesize ~70% | Freight spikes |

| Tailings | $7.1bn provision | Higher certified contractor demand |

| Labor | 66,000 employees | Wage/strike risk |

What is included in the product

Tailored for Vale, this Porter's Five Forces analysis reveals competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces shaping its mining and logistics advantage. Includes strategic implications for pricing, profitability, and defenses to protect market share.

A concise Vale Porter's Five Forces one‑sheet that visualizes competitive pressure via a spider chart, lets teams customize force levels for evolving market data, and drops directly into pitch decks—no macros, no fuss.

Customers Bargaining Power

Concentrated steelmakers

Global steel producers, with China accounting for roughly half of global crude steel output, buy millions of tonnes and can negotiate commercial terms at scale. Index-linked contracts (IODEX/PLS benchmarks) reduce direct price haggling but leave room for quality, logistics and lead-time negotiations. Buyers can switch among major miners for mainstream fines, while premiums for high-grade, low-impurity ore give Vale leverage for lower-emission steel routes.

Nickel and battery chain dynamics

Stainless producers and battery-precursor makers are more sophisticated buyers, with batteries rising to roughly 20% of nickel demand in 2024 while stainless still accounts for ~70%. Rapid EV growth (≈16 million light‑vehicle BEV/PHEV sales in 2024) boosts offtake contracting but also drives aggressive price benchmarking. Rising LFP adoption (≈40–50% of cell production in 2024) weakens nickel reliance and buyer leverage. Long‑term, traceable low‑carbon nickel can earn premiums of ~15–25%, offsetting some buyer power.

Specification and value-in-use

Customers price-in silica, alumina and moisture, which directly reduces realized prices; the 62% Fe seaborne benchmark remains a market reference while Vale’s Carajás ore and pellets average about 65–67% Fe in 2024. Higher Fe/pellet quality raises blast furnace yield and lowers CO2 intensity, limiting buyer power versus low‑grade feed; in oversupplied markets discounts can still widen regardless of quality.

Geographic and logistics optionality

In 2024 Australian shipments retained clear freight advantages into North Asia, pressuring Brazil-origin ores despite Vale’s dedicated rail-to-port logistics which partly offsets but cannot erase distance economics. Buyers routinely reoptimize blends and use strategic stockpiles and flexible contracts to manage total landed cost and exploit short-term dislocations, increasing their bargaining power.

- Australia freight advantage into North Asia (2024)

- Vale logistics mitigates but not nullifies distance

- Blend reoptimization lowers landed cost

- Stockpiles and flexible contracts boost buyer leverage

Backward integration and alliances

Some steelmakers and battery players pursue upstream stakes or long-term offtakes to secure supply and reduce reliance on volatile spot markets; by 2024 major OEMs and battery groups had committed multi-billion USD upstream investments and multi-year offtake contracts, helped by global EV sales of ~14.2 million in 2024 boosting demand. These partners can press for co-investment and price incentives, but the high capital intensity and execution risk limit broad full integration, tempering overall buyer power.

- Upstream stakes: multi-billion USD commitments (2023–24)

- Offtakes: multi-year contracts cover material for major EV projects (2024)

- Leverage: co-investment and price incentives increased

- Limit: capital/execution constraints keep buyer power moderate

China steel demand and battery growth reshape iron ore leverage: high-grade vs freight

Major steel buyers (China ~50% of crude steel) and large OEMs negotiate at scale, using index-linked contracts and blend optimization to press prices. Battery demand (≈16M BEV/PHEV sales; nickel battery share ~20% in 2024; LFP ~40–50%) creates targeted offtakes but also shifts leverage. Vale’s 65–67% Fe ore (vs 62% benchmark) and strong logistics limit buyer power, though Australian freight edge into North Asia amplifies buyer options.

| Metric | 2024 |

|---|---|

| China share of crude steel | ~50% |

| BEV/PHEV sales | ≈16M |

| Nickel battery demand | ~20% |

| Vale Fe grade | 65–67% |

| LFP share | 40–50% |

What You See Is What You Get

Vale Porter's Five Forces Analysis

This preview shows the exact Vale Porter's Five Forces analysis you'll receive upon purchase—fully formatted and ready to use. It evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes tailored to Vale’s mining and logistics operations. No placeholders or samples: the file available after payment is identical to this preview. Instant download for immediate strategic or investment use.

From Overview to Strategy Blueprint

Vale's Porter’s Five Forces assessment highlights intense buyer and rival pressures, supplier leverage in key inputs, moderate threat from new entrants, and substitute risks tied to commodity cycles. This snapshot teases strategic levers and vulnerabilities. Unlock the full analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy.

Suppliers Bargaining Power

Concentrated critical equipment

In 2024 OEMs such as Caterpillar and Komatsu remained the dominant providers of large trucks, drills and autonomous systems, constraining Vale’s switching options and pressuring lead times and pricing. Vale’s scale supports framework agreements that lower unit costs and secure priority service, while maintenance, parts and software lock-in raise lifecycle dependence. Global OEM competition allows periodic rebids, providing limited leverage.

Energy and fuel exposure

Diesel, electricity and bunker fuel drive a material share of mining costs—commonly 20–35% of operating cash costs—and remained volatile through 2024. Long-term PPAs and fuel hedges blunt price swings but do not remove structural exposure to fuel-intensive inputs. Grid constraints in some Brazilian and Indonesian regions raise supplier leverage. Decarbonization pushed 2024 renewable PPA demand up ~25%, tightening terms from credible providers.

Logistics and maritime capacity

Deepwater ports, Brazilian rail links and Capesize shipping (which carry roughly 70% of seaborne iron ore) are critical for Vale’s exports, giving port and dredging providers leverage. Vale’s integrated logistics and owned tonnage reduce exposure, but tight third‑party freight markets can spike charter rates and handling costs. Dependence on specialized dredging and terminal services concentrates supplier power despite diversified chartering.

Specialized services and compliance

Specialized tailings management, geotechnical and environmental remediation firms command bargaining power due to scarce expertise; Vale’s post-Brumadinho liabilities (about $7.1 billion provision in 2019) highlight the financial stakes that raise demand for certified contractors under tighter ESG and safety regimes. Permitting or audit delays concentrate schedule leverage with suppliers, while multi-sourcing or insourcing can trim the premium.

- Scarce expertise → higher rates

- ESG/safety rules ↑ demand for certified contractors

- Permitting delays amplify supplier leverage

- Multi-sourcing/insourcing reduces premium

Labor and local stakeholders

Skilled labor, strong unions and community agreements act as quasi-suppliers of operational continuity for Vale; the company reported about 66,000 employees in 2023, concentrating bargaining power in regions with scarce labor. Regional shortages or strikes can lift wage bills and cut output; indigenous and community benefit agreements add legally binding non-price obligations. Long-term training pipelines and constructive engagement can reduce this supplier-like power over time.

- Skilled labor concentration: raises replacement cost and downtime risk

- Union influence: can trigger wage inflation and industrial action

- Community/Indigenous agreements: non-price commitments and social license costs

- Mitigants: training pipelines, local hiring, engagement

Supplier power fuels cost volatility: fuel, OEM constraints, ports, tailings, labor

OEMs (Caterpillar/Komatsu) constrained switching and pricing in 2024; Vale’s scale and framework deals moderate but not eliminate leverage. Fuel (diesel/electricity/bunkers) remained 20–35% of operating cash costs and volatile; renewable PPA demand rose ~25% in 2024. Ports/charters (Capesize ~70% of seaborne ore), specialized tailings (Brumadinho provision $7.1bn) and 66,000 employees concentrate supplier power.

| Supplier | 2024 indicator | Impact |

|---|---|---|

| OEMs | Frameworks; limited competition | Price/lead-time pressure |

| Fuel | 20–35% opex; PPA demand +25% | Cost volatility |

| Shipping/ports | Capesize ~70% | Freight spikes |

| Tailings | $7.1bn provision | Higher certified contractor demand |

| Labor | 66,000 employees | Wage/strike risk |

What is included in the product

Tailored for Vale, this Porter's Five Forces analysis reveals competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces shaping its mining and logistics advantage. Includes strategic implications for pricing, profitability, and defenses to protect market share.

A concise Vale Porter's Five Forces one‑sheet that visualizes competitive pressure via a spider chart, lets teams customize force levels for evolving market data, and drops directly into pitch decks—no macros, no fuss.

Customers Bargaining Power

Concentrated steelmakers

Global steel producers, with China accounting for roughly half of global crude steel output, buy millions of tonnes and can negotiate commercial terms at scale. Index-linked contracts (IODEX/PLS benchmarks) reduce direct price haggling but leave room for quality, logistics and lead-time negotiations. Buyers can switch among major miners for mainstream fines, while premiums for high-grade, low-impurity ore give Vale leverage for lower-emission steel routes.

Nickel and battery chain dynamics

Stainless producers and battery-precursor makers are more sophisticated buyers, with batteries rising to roughly 20% of nickel demand in 2024 while stainless still accounts for ~70%. Rapid EV growth (≈16 million light‑vehicle BEV/PHEV sales in 2024) boosts offtake contracting but also drives aggressive price benchmarking. Rising LFP adoption (≈40–50% of cell production in 2024) weakens nickel reliance and buyer leverage. Long‑term, traceable low‑carbon nickel can earn premiums of ~15–25%, offsetting some buyer power.

Specification and value-in-use

Customers price-in silica, alumina and moisture, which directly reduces realized prices; the 62% Fe seaborne benchmark remains a market reference while Vale’s Carajás ore and pellets average about 65–67% Fe in 2024. Higher Fe/pellet quality raises blast furnace yield and lowers CO2 intensity, limiting buyer power versus low‑grade feed; in oversupplied markets discounts can still widen regardless of quality.

Geographic and logistics optionality

In 2024 Australian shipments retained clear freight advantages into North Asia, pressuring Brazil-origin ores despite Vale’s dedicated rail-to-port logistics which partly offsets but cannot erase distance economics. Buyers routinely reoptimize blends and use strategic stockpiles and flexible contracts to manage total landed cost and exploit short-term dislocations, increasing their bargaining power.

- Australia freight advantage into North Asia (2024)

- Vale logistics mitigates but not nullifies distance

- Blend reoptimization lowers landed cost

- Stockpiles and flexible contracts boost buyer leverage

Backward integration and alliances

Some steelmakers and battery players pursue upstream stakes or long-term offtakes to secure supply and reduce reliance on volatile spot markets; by 2024 major OEMs and battery groups had committed multi-billion USD upstream investments and multi-year offtake contracts, helped by global EV sales of ~14.2 million in 2024 boosting demand. These partners can press for co-investment and price incentives, but the high capital intensity and execution risk limit broad full integration, tempering overall buyer power.

- Upstream stakes: multi-billion USD commitments (2023–24)

- Offtakes: multi-year contracts cover material for major EV projects (2024)

- Leverage: co-investment and price incentives increased

- Limit: capital/execution constraints keep buyer power moderate

China steel demand and battery growth reshape iron ore leverage: high-grade vs freight

Major steel buyers (China ~50% of crude steel) and large OEMs negotiate at scale, using index-linked contracts and blend optimization to press prices. Battery demand (≈16M BEV/PHEV sales; nickel battery share ~20% in 2024; LFP ~40–50%) creates targeted offtakes but also shifts leverage. Vale’s 65–67% Fe ore (vs 62% benchmark) and strong logistics limit buyer power, though Australian freight edge into North Asia amplifies buyer options.

| Metric | 2024 |

|---|---|

| China share of crude steel | ~50% |

| BEV/PHEV sales | ≈16M |

| Nickel battery demand | ~20% |

| Vale Fe grade | 65–67% |

| LFP share | 40–50% |

What You See Is What You Get

Vale Porter's Five Forces Analysis

This preview shows the exact Vale Porter's Five Forces analysis you'll receive upon purchase—fully formatted and ready to use. It evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes tailored to Vale’s mining and logistics operations. No placeholders or samples: the file available after payment is identical to this preview. Instant download for immediate strategic or investment use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Vale's Porter’s Five Forces assessment highlights intense buyer and rival pressures, supplier leverage in key inputs, moderate threat from new entrants, and substitute risks tied to commodity cycles. This snapshot teases strategic levers and vulnerabilities. Unlock the full analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy.

Suppliers Bargaining Power

Concentrated critical equipment

In 2024 OEMs such as Caterpillar and Komatsu remained the dominant providers of large trucks, drills and autonomous systems, constraining Vale’s switching options and pressuring lead times and pricing. Vale’s scale supports framework agreements that lower unit costs and secure priority service, while maintenance, parts and software lock-in raise lifecycle dependence. Global OEM competition allows periodic rebids, providing limited leverage.

Energy and fuel exposure

Diesel, electricity and bunker fuel drive a material share of mining costs—commonly 20–35% of operating cash costs—and remained volatile through 2024. Long-term PPAs and fuel hedges blunt price swings but do not remove structural exposure to fuel-intensive inputs. Grid constraints in some Brazilian and Indonesian regions raise supplier leverage. Decarbonization pushed 2024 renewable PPA demand up ~25%, tightening terms from credible providers.

Logistics and maritime capacity

Deepwater ports, Brazilian rail links and Capesize shipping (which carry roughly 70% of seaborne iron ore) are critical for Vale’s exports, giving port and dredging providers leverage. Vale’s integrated logistics and owned tonnage reduce exposure, but tight third‑party freight markets can spike charter rates and handling costs. Dependence on specialized dredging and terminal services concentrates supplier power despite diversified chartering.

Specialized services and compliance

Specialized tailings management, geotechnical and environmental remediation firms command bargaining power due to scarce expertise; Vale’s post-Brumadinho liabilities (about $7.1 billion provision in 2019) highlight the financial stakes that raise demand for certified contractors under tighter ESG and safety regimes. Permitting or audit delays concentrate schedule leverage with suppliers, while multi-sourcing or insourcing can trim the premium.

- Scarce expertise → higher rates

- ESG/safety rules ↑ demand for certified contractors

- Permitting delays amplify supplier leverage

- Multi-sourcing/insourcing reduces premium

Labor and local stakeholders

Skilled labor, strong unions and community agreements act as quasi-suppliers of operational continuity for Vale; the company reported about 66,000 employees in 2023, concentrating bargaining power in regions with scarce labor. Regional shortages or strikes can lift wage bills and cut output; indigenous and community benefit agreements add legally binding non-price obligations. Long-term training pipelines and constructive engagement can reduce this supplier-like power over time.

- Skilled labor concentration: raises replacement cost and downtime risk

- Union influence: can trigger wage inflation and industrial action

- Community/Indigenous agreements: non-price commitments and social license costs

- Mitigants: training pipelines, local hiring, engagement

Supplier power fuels cost volatility: fuel, OEM constraints, ports, tailings, labor

OEMs (Caterpillar/Komatsu) constrained switching and pricing in 2024; Vale’s scale and framework deals moderate but not eliminate leverage. Fuel (diesel/electricity/bunkers) remained 20–35% of operating cash costs and volatile; renewable PPA demand rose ~25% in 2024. Ports/charters (Capesize ~70% of seaborne ore), specialized tailings (Brumadinho provision $7.1bn) and 66,000 employees concentrate supplier power.

| Supplier | 2024 indicator | Impact |

|---|---|---|

| OEMs | Frameworks; limited competition | Price/lead-time pressure |

| Fuel | 20–35% opex; PPA demand +25% | Cost volatility |

| Shipping/ports | Capesize ~70% | Freight spikes |

| Tailings | $7.1bn provision | Higher certified contractor demand |

| Labor | 66,000 employees | Wage/strike risk |

What is included in the product

Tailored for Vale, this Porter's Five Forces analysis reveals competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces shaping its mining and logistics advantage. Includes strategic implications for pricing, profitability, and defenses to protect market share.

A concise Vale Porter's Five Forces one‑sheet that visualizes competitive pressure via a spider chart, lets teams customize force levels for evolving market data, and drops directly into pitch decks—no macros, no fuss.

Customers Bargaining Power

Concentrated steelmakers

Global steel producers, with China accounting for roughly half of global crude steel output, buy millions of tonnes and can negotiate commercial terms at scale. Index-linked contracts (IODEX/PLS benchmarks) reduce direct price haggling but leave room for quality, logistics and lead-time negotiations. Buyers can switch among major miners for mainstream fines, while premiums for high-grade, low-impurity ore give Vale leverage for lower-emission steel routes.

Nickel and battery chain dynamics

Stainless producers and battery-precursor makers are more sophisticated buyers, with batteries rising to roughly 20% of nickel demand in 2024 while stainless still accounts for ~70%. Rapid EV growth (≈16 million light‑vehicle BEV/PHEV sales in 2024) boosts offtake contracting but also drives aggressive price benchmarking. Rising LFP adoption (≈40–50% of cell production in 2024) weakens nickel reliance and buyer leverage. Long‑term, traceable low‑carbon nickel can earn premiums of ~15–25%, offsetting some buyer power.

Specification and value-in-use

Customers price-in silica, alumina and moisture, which directly reduces realized prices; the 62% Fe seaborne benchmark remains a market reference while Vale’s Carajás ore and pellets average about 65–67% Fe in 2024. Higher Fe/pellet quality raises blast furnace yield and lowers CO2 intensity, limiting buyer power versus low‑grade feed; in oversupplied markets discounts can still widen regardless of quality.

Geographic and logistics optionality

In 2024 Australian shipments retained clear freight advantages into North Asia, pressuring Brazil-origin ores despite Vale’s dedicated rail-to-port logistics which partly offsets but cannot erase distance economics. Buyers routinely reoptimize blends and use strategic stockpiles and flexible contracts to manage total landed cost and exploit short-term dislocations, increasing their bargaining power.

- Australia freight advantage into North Asia (2024)

- Vale logistics mitigates but not nullifies distance

- Blend reoptimization lowers landed cost

- Stockpiles and flexible contracts boost buyer leverage

Backward integration and alliances

Some steelmakers and battery players pursue upstream stakes or long-term offtakes to secure supply and reduce reliance on volatile spot markets; by 2024 major OEMs and battery groups had committed multi-billion USD upstream investments and multi-year offtake contracts, helped by global EV sales of ~14.2 million in 2024 boosting demand. These partners can press for co-investment and price incentives, but the high capital intensity and execution risk limit broad full integration, tempering overall buyer power.

- Upstream stakes: multi-billion USD commitments (2023–24)

- Offtakes: multi-year contracts cover material for major EV projects (2024)

- Leverage: co-investment and price incentives increased

- Limit: capital/execution constraints keep buyer power moderate

China steel demand and battery growth reshape iron ore leverage: high-grade vs freight

Major steel buyers (China ~50% of crude steel) and large OEMs negotiate at scale, using index-linked contracts and blend optimization to press prices. Battery demand (≈16M BEV/PHEV sales; nickel battery share ~20% in 2024; LFP ~40–50%) creates targeted offtakes but also shifts leverage. Vale’s 65–67% Fe ore (vs 62% benchmark) and strong logistics limit buyer power, though Australian freight edge into North Asia amplifies buyer options.

| Metric | 2024 |

|---|---|

| China share of crude steel | ~50% |

| BEV/PHEV sales | ≈16M |

| Nickel battery demand | ~20% |

| Vale Fe grade | 65–67% |

| LFP share | 40–50% |

What You See Is What You Get

Vale Porter's Five Forces Analysis

This preview shows the exact Vale Porter's Five Forces analysis you'll receive upon purchase—fully formatted and ready to use. It evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes tailored to Vale’s mining and logistics operations. No placeholders or samples: the file available after payment is identical to this preview. Instant download for immediate strategic or investment use.