Valeo Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

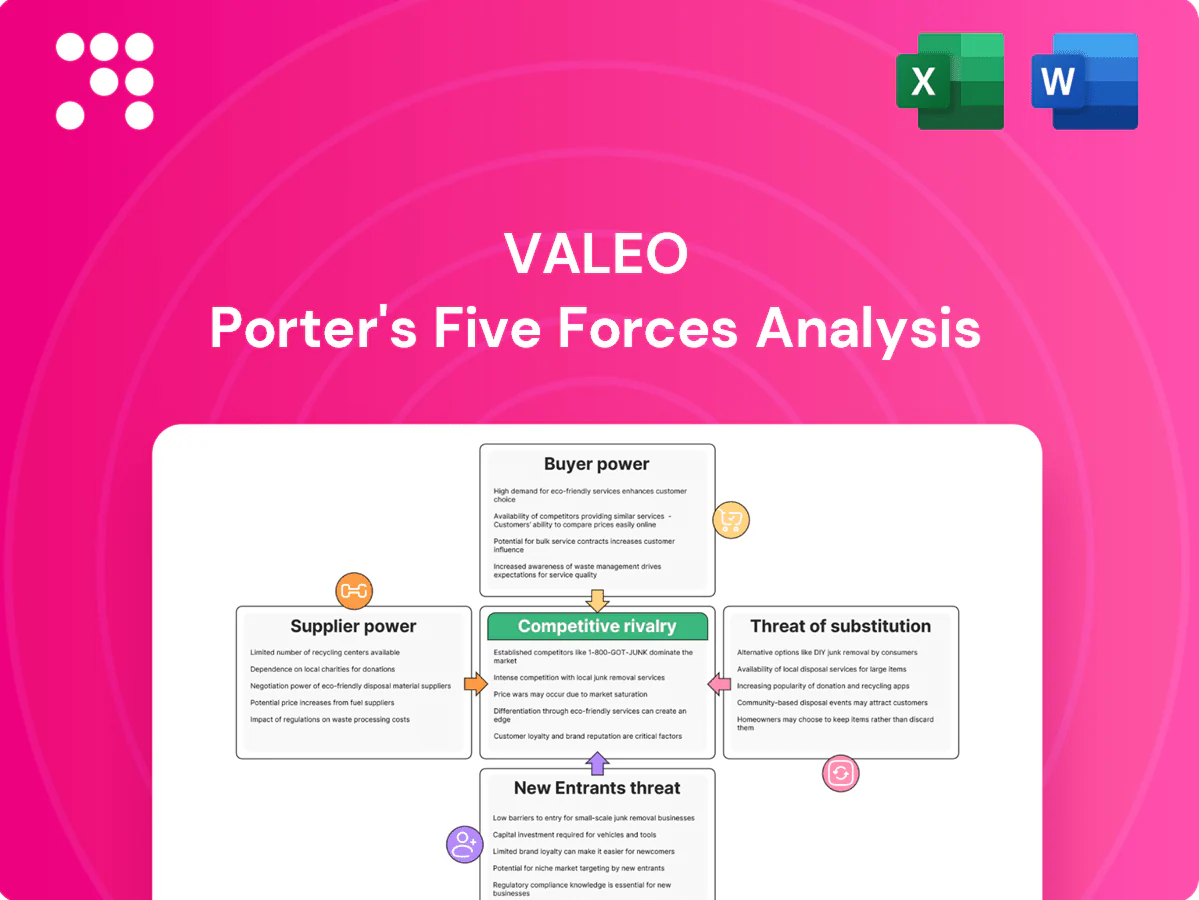

Valeo faces intense competitive pressure from global OEMs and suppliers as rapid EV and ADAS tech shift margins and supply chains. Buyer concentration, supplier bargaining on semiconductors, and substitute mobility solutions raise strategic risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valeo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor and sensor concentration

Chips, imagers and power electronics for Valeo come from a concentrated set of fabs and Tier‑2 specialists — TSMC held about 54% of global foundry revenue in 2023 and top players dominate advanced nodes.

Shortages or node transitions shift leverage to suppliers on price and allocation, as seen in 2020–22 disruptions.

Valeo mitigates via dual‑sourcing and redesigns but automotive qualification cycles typically take 12–24 months.

Geopolitics and export controls (notably US restrictions since 2022) add ongoing volatility to supply risk.

Critical materials volatility

Aluminum (~$2,300/t LME 2024), copper (~$9,500/t 2024), rare-earth magnets (China controls ~80–90% processing) and specialty chemicals are critical to Valeo’s electrification and thermal systems, with input volatility directly squeezing margins. Price swings and logistics bottlenecks in 2024 led to margin compression of several percentage points for auto suppliers. Hedging and long-term contracts mitigate but cannot fully offset spikes. Sustainability and traceability rules have narrowed the vetted supplier pool.

High switching and qualification costs

Automotive-grade PPAP and IATF 16949 processes (published 2016) make supplier changes slow and costly, extending qualification timelines and validation runs. Strict failure-rate and reliability specs force Valeo into deep co-development with vendors, creating operational dependency and stronger supplier leverage on critical modules. Multi-year framework agreements (commonly 3–5 years) partially rebalance terms across the contract horizon.

Software and algorithm dependencies

ADAS stacks, AI tools and middleware often depend on third-party platforms and toolchains; licensing, updates and ASIL safety certification give specialized vendors significant leverage. Valeo’s heavy R&D focus (roughly 10–12% of sales historically) reduces supplier power but talent scarcity keeps dependence on key partners, while API/SDK lock-in raises migration costs.

- Third-party ASIL tooling influence

- In-house cuts costs but needs talent

- API/SDK lock-in increases switching costs

Tooling and equipment bottlenecks

Tooling and equipment bottlenecks constrain Valeo: molds, testers and SiC/GaN-capable tools commonly face lead times exceeding 12 months, with some specialized testers at 18+ months. Capacity expansions depend on a few global OEMs such as Applied Materials, KLA and Tokyo Electron, concentrating supply risk. Upfront tooling often paid by Valeo or OEMs ties capacity to specific programs, so delays can ripple across multiple product lines and launch timelines.

- Lead times: >12 months (specialized testers 18+ months)

- Equipment OEMs: Applied Materials, KLA, Tokyo Electron (few suppliers)

- Upfront tooling ties capacity to programs, causing cross-line delay risk

High supplier power: concentrated foundries, volatile raw materials and long lead times

Supplier power is high: semiconductors concentrated (TSMC ~54% foundry rev 2023), raw-material volatility (Al ~$2,300/t, Cu ~$9,500/t in 2024) and China dominant in rare‑earth processing (~80–90%). Qualification cycles (12–24 months) and tooling lead times (>12–18 months) raise switching costs despite dual‑sourcing and long‑term contracts.

| Metric | Value |

|---|---|

| Foundry concentration | TSMC ~54% (2023) |

| Raw prices (2024) | Al $2,300/t; Cu $9,500/t |

| Qualification / tooling | 12–24 months / >12–18 months |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entrant threats and substitutes affecting Valeo, with strategic commentary on pricing, profitability and barriers that protect incumbents in the automotive components market.

A concise, slide-ready Porter's Five Forces for Valeo that highlights supplier/customer power, competitive rivalry and entrant/substitute threats to accelerate strategic decisions; customizable pressure levels and clean visuals make it easy to slot into decks or reports without complex tools.

Customers Bargaining Power

Concentrated global automakers

OEMs buy components in massive volumes and negotiate aggressively; in 2024 the top 5 groups (Toyota, Volkswagen, Stellantis, Hyundai‑Kia, GM) accounted for roughly 45% of global vehicle production, concentrating demand and amplifying price pressure.

Design-in lock and switching frictions

Once Valeo is designed into a platform, switching mid-cycle is costly for OEMs because typical vehicle program lifecycles run 5–7 years, making changes after SOP disruptive and expensive; this reduces buyer power during production but not at initial sourcing. Re-award cycles tied to model redesigns (commonly every 5–7 years) restore OEM leverage. Strong performance KPIs and on-time quality metrics are vital to retain programs and influence re-award decisions.

Total cost and warranty accountability

OEMs push mid-single-digit annual cost-downs and demand productivity givebacks while shifting warranty risk and chargebacks for quality spills, which can reach multi-million-euro impacts on program profitability; Valeo must therefore balance margin protection with zero-defect expectations. Collaborative VA/VE initiatives that exchange measured value for preferred-supplier status are critical to retaining awards and limiting warranty exposure.

Regulatory and tech roadmap influence

Buyers push specifications tied to safety, emissions and electrification (eg EU 2035 passenger car CO2 phase-out), forcing suppliers like Valeo to absorb compliance costs on tight OEM timelines; early engineering involvement secures higher content but raises customization and margin pressure. Standardization initiatives and modular platforms risk commoditizing modules over time, reducing bargaining power.

- Buyers dictate ADAS/thermal/e‑powertrain specs

- Compliance costs shift to suppliers under tight deadlines

- Early involvement = more content, more customization

- Standardization can commoditize modules

Aftermarket and new mobility mix

Aftermarket buyers are fragmented, which moderates customer power across many Valeo product lines; in 2024 Valeo reported €18.7bn sales with aftermarket contributing roughly a quarter, diluting single-buyer influence. Fleet and mobility operators push TCO and uptime demands, driving service SLAs and recurring revenue models. Software updates, feature unlocks and data-access terms now serve as new negotiation levers and potential revenue streams.

- Aftermarket fragmentation lowers single-buyer leverage

- Fleets demand SLAs, uptime and TCO focus

- Software features & data access create bargaining chips

OEM buying concentrated: top-5 ~45%, lifecycle 5–7 yrs

OEMs concentrate buying (top 5 ~45% of production) and push mid-single-digit annual cost‑downs; program lifecycles 5–7 years limit mid-cycle switching but re-awards restore leverage. Valeo 2024 sales €18.7bn, aftermarket ~25% softens single-buyer power. Compliance, warranty and software/data terms intensify negotiations.

| Metric | Value |

|---|---|

| Top-5 OEM share | ~45% |

| Valeo sales (2024) | €18.7bn |

| Aftermarket share | ~25% |

| Cost-downs | Mid-single-digit % |

| Program lifecycle | 5–7 yrs |

What You See Is What You Get

Valeo Porter's Five Forces Analysis

This preview shows the exact Valeo Porter's Five Forces analysis you'll receive after purchase—no surprises, no placeholders. It assesses supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes, and offers evidence-based strategic implications. The file is fully formatted and ready for immediate download and use the moment you buy.

Go Beyond the Preview—Access the Full Strategic Report

Valeo faces intense competitive pressure from global OEMs and suppliers as rapid EV and ADAS tech shift margins and supply chains. Buyer concentration, supplier bargaining on semiconductors, and substitute mobility solutions raise strategic risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valeo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor and sensor concentration

Chips, imagers and power electronics for Valeo come from a concentrated set of fabs and Tier‑2 specialists — TSMC held about 54% of global foundry revenue in 2023 and top players dominate advanced nodes.

Shortages or node transitions shift leverage to suppliers on price and allocation, as seen in 2020–22 disruptions.

Valeo mitigates via dual‑sourcing and redesigns but automotive qualification cycles typically take 12–24 months.

Geopolitics and export controls (notably US restrictions since 2022) add ongoing volatility to supply risk.

Critical materials volatility

Aluminum (~$2,300/t LME 2024), copper (~$9,500/t 2024), rare-earth magnets (China controls ~80–90% processing) and specialty chemicals are critical to Valeo’s electrification and thermal systems, with input volatility directly squeezing margins. Price swings and logistics bottlenecks in 2024 led to margin compression of several percentage points for auto suppliers. Hedging and long-term contracts mitigate but cannot fully offset spikes. Sustainability and traceability rules have narrowed the vetted supplier pool.

High switching and qualification costs

Automotive-grade PPAP and IATF 16949 processes (published 2016) make supplier changes slow and costly, extending qualification timelines and validation runs. Strict failure-rate and reliability specs force Valeo into deep co-development with vendors, creating operational dependency and stronger supplier leverage on critical modules. Multi-year framework agreements (commonly 3–5 years) partially rebalance terms across the contract horizon.

Software and algorithm dependencies

ADAS stacks, AI tools and middleware often depend on third-party platforms and toolchains; licensing, updates and ASIL safety certification give specialized vendors significant leverage. Valeo’s heavy R&D focus (roughly 10–12% of sales historically) reduces supplier power but talent scarcity keeps dependence on key partners, while API/SDK lock-in raises migration costs.

- Third-party ASIL tooling influence

- In-house cuts costs but needs talent

- API/SDK lock-in increases switching costs

Tooling and equipment bottlenecks

Tooling and equipment bottlenecks constrain Valeo: molds, testers and SiC/GaN-capable tools commonly face lead times exceeding 12 months, with some specialized testers at 18+ months. Capacity expansions depend on a few global OEMs such as Applied Materials, KLA and Tokyo Electron, concentrating supply risk. Upfront tooling often paid by Valeo or OEMs ties capacity to specific programs, so delays can ripple across multiple product lines and launch timelines.

- Lead times: >12 months (specialized testers 18+ months)

- Equipment OEMs: Applied Materials, KLA, Tokyo Electron (few suppliers)

- Upfront tooling ties capacity to programs, causing cross-line delay risk

High supplier power: concentrated foundries, volatile raw materials and long lead times

Supplier power is high: semiconductors concentrated (TSMC ~54% foundry rev 2023), raw-material volatility (Al ~$2,300/t, Cu ~$9,500/t in 2024) and China dominant in rare‑earth processing (~80–90%). Qualification cycles (12–24 months) and tooling lead times (>12–18 months) raise switching costs despite dual‑sourcing and long‑term contracts.

| Metric | Value |

|---|---|

| Foundry concentration | TSMC ~54% (2023) |

| Raw prices (2024) | Al $2,300/t; Cu $9,500/t |

| Qualification / tooling | 12–24 months / >12–18 months |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entrant threats and substitutes affecting Valeo, with strategic commentary on pricing, profitability and barriers that protect incumbents in the automotive components market.

A concise, slide-ready Porter's Five Forces for Valeo that highlights supplier/customer power, competitive rivalry and entrant/substitute threats to accelerate strategic decisions; customizable pressure levels and clean visuals make it easy to slot into decks or reports without complex tools.

Customers Bargaining Power

Concentrated global automakers

OEMs buy components in massive volumes and negotiate aggressively; in 2024 the top 5 groups (Toyota, Volkswagen, Stellantis, Hyundai‑Kia, GM) accounted for roughly 45% of global vehicle production, concentrating demand and amplifying price pressure.

Design-in lock and switching frictions

Once Valeo is designed into a platform, switching mid-cycle is costly for OEMs because typical vehicle program lifecycles run 5–7 years, making changes after SOP disruptive and expensive; this reduces buyer power during production but not at initial sourcing. Re-award cycles tied to model redesigns (commonly every 5–7 years) restore OEM leverage. Strong performance KPIs and on-time quality metrics are vital to retain programs and influence re-award decisions.

Total cost and warranty accountability

OEMs push mid-single-digit annual cost-downs and demand productivity givebacks while shifting warranty risk and chargebacks for quality spills, which can reach multi-million-euro impacts on program profitability; Valeo must therefore balance margin protection with zero-defect expectations. Collaborative VA/VE initiatives that exchange measured value for preferred-supplier status are critical to retaining awards and limiting warranty exposure.

Regulatory and tech roadmap influence

Buyers push specifications tied to safety, emissions and electrification (eg EU 2035 passenger car CO2 phase-out), forcing suppliers like Valeo to absorb compliance costs on tight OEM timelines; early engineering involvement secures higher content but raises customization and margin pressure. Standardization initiatives and modular platforms risk commoditizing modules over time, reducing bargaining power.

- Buyers dictate ADAS/thermal/e‑powertrain specs

- Compliance costs shift to suppliers under tight deadlines

- Early involvement = more content, more customization

- Standardization can commoditize modules

Aftermarket and new mobility mix

Aftermarket buyers are fragmented, which moderates customer power across many Valeo product lines; in 2024 Valeo reported €18.7bn sales with aftermarket contributing roughly a quarter, diluting single-buyer influence. Fleet and mobility operators push TCO and uptime demands, driving service SLAs and recurring revenue models. Software updates, feature unlocks and data-access terms now serve as new negotiation levers and potential revenue streams.

- Aftermarket fragmentation lowers single-buyer leverage

- Fleets demand SLAs, uptime and TCO focus

- Software features & data access create bargaining chips

OEM buying concentrated: top-5 ~45%, lifecycle 5–7 yrs

OEMs concentrate buying (top 5 ~45% of production) and push mid-single-digit annual cost‑downs; program lifecycles 5–7 years limit mid-cycle switching but re-awards restore leverage. Valeo 2024 sales €18.7bn, aftermarket ~25% softens single-buyer power. Compliance, warranty and software/data terms intensify negotiations.

| Metric | Value |

|---|---|

| Top-5 OEM share | ~45% |

| Valeo sales (2024) | €18.7bn |

| Aftermarket share | ~25% |

| Cost-downs | Mid-single-digit % |

| Program lifecycle | 5–7 yrs |

What You See Is What You Get

Valeo Porter's Five Forces Analysis

This preview shows the exact Valeo Porter's Five Forces analysis you'll receive after purchase—no surprises, no placeholders. It assesses supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes, and offers evidence-based strategic implications. The file is fully formatted and ready for immediate download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Valeo faces intense competitive pressure from global OEMs and suppliers as rapid EV and ADAS tech shift margins and supply chains. Buyer concentration, supplier bargaining on semiconductors, and substitute mobility solutions raise strategic risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Valeo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor and sensor concentration

Chips, imagers and power electronics for Valeo come from a concentrated set of fabs and Tier‑2 specialists — TSMC held about 54% of global foundry revenue in 2023 and top players dominate advanced nodes.

Shortages or node transitions shift leverage to suppliers on price and allocation, as seen in 2020–22 disruptions.

Valeo mitigates via dual‑sourcing and redesigns but automotive qualification cycles typically take 12–24 months.

Geopolitics and export controls (notably US restrictions since 2022) add ongoing volatility to supply risk.

Critical materials volatility

Aluminum (~$2,300/t LME 2024), copper (~$9,500/t 2024), rare-earth magnets (China controls ~80–90% processing) and specialty chemicals are critical to Valeo’s electrification and thermal systems, with input volatility directly squeezing margins. Price swings and logistics bottlenecks in 2024 led to margin compression of several percentage points for auto suppliers. Hedging and long-term contracts mitigate but cannot fully offset spikes. Sustainability and traceability rules have narrowed the vetted supplier pool.

High switching and qualification costs

Automotive-grade PPAP and IATF 16949 processes (published 2016) make supplier changes slow and costly, extending qualification timelines and validation runs. Strict failure-rate and reliability specs force Valeo into deep co-development with vendors, creating operational dependency and stronger supplier leverage on critical modules. Multi-year framework agreements (commonly 3–5 years) partially rebalance terms across the contract horizon.

Software and algorithm dependencies

ADAS stacks, AI tools and middleware often depend on third-party platforms and toolchains; licensing, updates and ASIL safety certification give specialized vendors significant leverage. Valeo’s heavy R&D focus (roughly 10–12% of sales historically) reduces supplier power but talent scarcity keeps dependence on key partners, while API/SDK lock-in raises migration costs.

- Third-party ASIL tooling influence

- In-house cuts costs but needs talent

- API/SDK lock-in increases switching costs

Tooling and equipment bottlenecks

Tooling and equipment bottlenecks constrain Valeo: molds, testers and SiC/GaN-capable tools commonly face lead times exceeding 12 months, with some specialized testers at 18+ months. Capacity expansions depend on a few global OEMs such as Applied Materials, KLA and Tokyo Electron, concentrating supply risk. Upfront tooling often paid by Valeo or OEMs ties capacity to specific programs, so delays can ripple across multiple product lines and launch timelines.

- Lead times: >12 months (specialized testers 18+ months)

- Equipment OEMs: Applied Materials, KLA, Tokyo Electron (few suppliers)

- Upfront tooling ties capacity to programs, causing cross-line delay risk

High supplier power: concentrated foundries, volatile raw materials and long lead times

Supplier power is high: semiconductors concentrated (TSMC ~54% foundry rev 2023), raw-material volatility (Al ~$2,300/t, Cu ~$9,500/t in 2024) and China dominant in rare‑earth processing (~80–90%). Qualification cycles (12–24 months) and tooling lead times (>12–18 months) raise switching costs despite dual‑sourcing and long‑term contracts.

| Metric | Value |

|---|---|

| Foundry concentration | TSMC ~54% (2023) |

| Raw prices (2024) | Al $2,300/t; Cu $9,500/t |

| Qualification / tooling | 12–24 months / >12–18 months |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entrant threats and substitutes affecting Valeo, with strategic commentary on pricing, profitability and barriers that protect incumbents in the automotive components market.

A concise, slide-ready Porter's Five Forces for Valeo that highlights supplier/customer power, competitive rivalry and entrant/substitute threats to accelerate strategic decisions; customizable pressure levels and clean visuals make it easy to slot into decks or reports without complex tools.

Customers Bargaining Power

Concentrated global automakers

OEMs buy components in massive volumes and negotiate aggressively; in 2024 the top 5 groups (Toyota, Volkswagen, Stellantis, Hyundai‑Kia, GM) accounted for roughly 45% of global vehicle production, concentrating demand and amplifying price pressure.

Design-in lock and switching frictions

Once Valeo is designed into a platform, switching mid-cycle is costly for OEMs because typical vehicle program lifecycles run 5–7 years, making changes after SOP disruptive and expensive; this reduces buyer power during production but not at initial sourcing. Re-award cycles tied to model redesigns (commonly every 5–7 years) restore OEM leverage. Strong performance KPIs and on-time quality metrics are vital to retain programs and influence re-award decisions.

Total cost and warranty accountability

OEMs push mid-single-digit annual cost-downs and demand productivity givebacks while shifting warranty risk and chargebacks for quality spills, which can reach multi-million-euro impacts on program profitability; Valeo must therefore balance margin protection with zero-defect expectations. Collaborative VA/VE initiatives that exchange measured value for preferred-supplier status are critical to retaining awards and limiting warranty exposure.

Regulatory and tech roadmap influence

Buyers push specifications tied to safety, emissions and electrification (eg EU 2035 passenger car CO2 phase-out), forcing suppliers like Valeo to absorb compliance costs on tight OEM timelines; early engineering involvement secures higher content but raises customization and margin pressure. Standardization initiatives and modular platforms risk commoditizing modules over time, reducing bargaining power.

- Buyers dictate ADAS/thermal/e‑powertrain specs

- Compliance costs shift to suppliers under tight deadlines

- Early involvement = more content, more customization

- Standardization can commoditize modules

Aftermarket and new mobility mix

Aftermarket buyers are fragmented, which moderates customer power across many Valeo product lines; in 2024 Valeo reported €18.7bn sales with aftermarket contributing roughly a quarter, diluting single-buyer influence. Fleet and mobility operators push TCO and uptime demands, driving service SLAs and recurring revenue models. Software updates, feature unlocks and data-access terms now serve as new negotiation levers and potential revenue streams.

- Aftermarket fragmentation lowers single-buyer leverage

- Fleets demand SLAs, uptime and TCO focus

- Software features & data access create bargaining chips

OEM buying concentrated: top-5 ~45%, lifecycle 5–7 yrs

OEMs concentrate buying (top 5 ~45% of production) and push mid-single-digit annual cost‑downs; program lifecycles 5–7 years limit mid-cycle switching but re-awards restore leverage. Valeo 2024 sales €18.7bn, aftermarket ~25% softens single-buyer power. Compliance, warranty and software/data terms intensify negotiations.

| Metric | Value |

|---|---|

| Top-5 OEM share | ~45% |

| Valeo sales (2024) | €18.7bn |

| Aftermarket share | ~25% |

| Cost-downs | Mid-single-digit % |

| Program lifecycle | 5–7 yrs |

What You See Is What You Get

Valeo Porter's Five Forces Analysis

This preview shows the exact Valeo Porter's Five Forces analysis you'll receive after purchase—no surprises, no placeholders. It assesses supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes, and offers evidence-based strategic implications. The file is fully formatted and ready for immediate download and use the moment you buy.