Valid SA Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

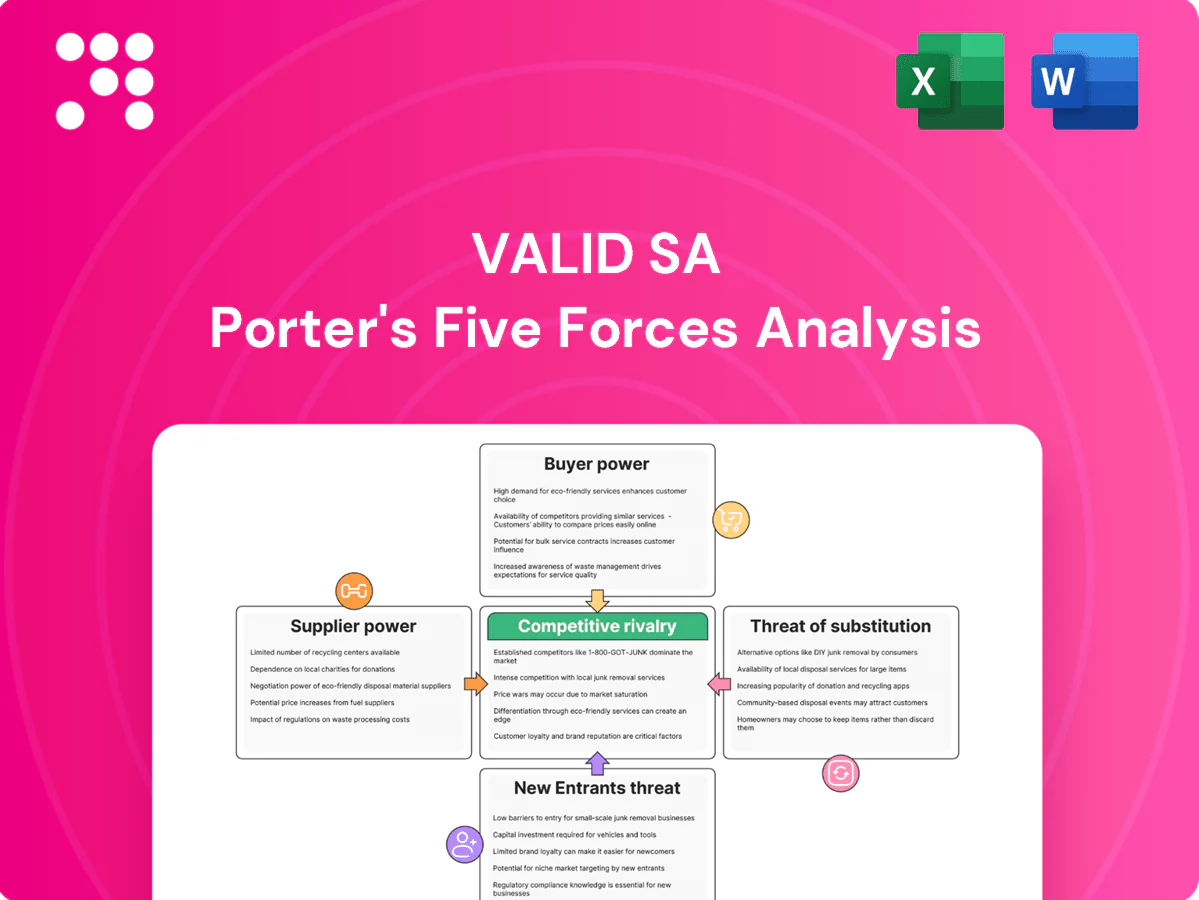

This brief snapshot outlines the competitive pressures facing Valid SA—supplier leverage, buyer bargaining, new entrants, substitutes, and competitive rivalry. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable implications tailored to Valid SA. Purchase the complete report for a consultant-grade, data-driven strategic roadmap you can use in presentations or investment decisions.

Suppliers Bargaining Power

Specialized components

Valid relies on secure chips, secure elements and specialty substrates sourced from few qualified global suppliers, giving suppliers strong leverage; qualification cycles typically run 6–18 months and 2024 foundry constraints pushed lead times to roughly 20–40 weeks, raising pricing risk; dual-sourcing mitigates exposure but equivalency must pass full certifications, adding time and cost.

Security materials

Overt and covert security features for civil IDs and bank cards are niche and IP-protected, letting specialized suppliers extract premium pricing; vendors with proprietary holograms, inks and laminates often dominate tender evaluations. Switching suppliers forces redesigns and document re-certification, delaying rollouts and raising costs. Supply assurances are tightly tied to compliance and chain-of-custody standards such as ISO 14298.

PKI and software stacks

Digital certification depends on cryptographic libraries, HSMs and licensed middleware, with major suppliers (Thales, Entrust, Utimaco, AWS CloudHSM) dominating integrations and raising vendor lock-in risks; FIPS 140-3 became the baseline after 2023 and remained central to regulatory validation in 2024. Open standards and FIPS/Common Criteria certification provide negotiation leverage, but cloud bundling and integrated key management often shift power back to providers.

Telecom modules

Telecom modules: SIM/eSIM profiles and IoT modules require certified components and secure OSes, and a few global suppliers (Quectel, Fibocom, Thales/Infineon, Sierra Wireless) dominate supply, concentrating risk. Carrier certifications in 2024 typically took 3–9 months, limiting substitution speed and forcing volume commitments and roadmap alignment for multi-year deals.

- Concentration: top vendors dominate supply

- Certification: 3–9 months (2024)

- Contracts: volume commitments common

- Roadmap: alignment required for carrier approval

Skilled talent

- Talent scarcity: 3.4M shortfall (ISC2, 2023)

- Hiring difficulty: 68% employers (2024)

- Cost pressure: ~20–30% higher hiring/retention costs

- Mitigation: nearshoring/training lower but not remove risk

Suppliers retain pricing power: 20-40 week lead times, 3-9 month certs, talent gap hikes costs

Suppliers hold strong leverage due to concentrated secure-chip, HSM and niche security-material markets; 2024 lead times 20–40 weeks and FIPS 140-3 baseline increase switching costs. Certifications take 3–9 months, forcing volume commitments and roadmap alignment. Talent shortfall (ISC2 3.4M) and 68% hiring difficulty in 2024 raise labour costs ~20–30%, preserving supplier power.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Lead times | 20–40 weeks | Higher prices, delays |

| Certifications | 3–9 months | Slow substitution |

| Talent | 3.4M shortfall / 68% hiring difficulty | +20–30% costs |

What is included in the product

Concise Porter's Five Forces for Valid SA uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes and disruptive threats, with industry data and strategic implications for pricing and profitability.

Clear one-sheet Porter's Five Forces for Valid SA—instantly visualize competitive pressure with an editable spider chart and customizable force levels, ready to drop into pitch decks or integrated Excel dashboards for fast, board-ready decisions.

Customers Bargaining Power

Government megabuyers

Civil ID and track-and-trace contracts are large, long-term and bid-driven, with flagship programs like India’s Aadhaar serving about 1.25 billion identities highlighting scale. Governments wield strong price and compliance pressure via competitive tenders; switching costs exist but rebids every 5–10 years can reset commercial terms. Political and data-sovereignty clauses further tighten contractual expectations.

Banks and issuers

Financial institutions buy millions of payment cards and authentication services annually and routinely multi-source via aggressive RFPs, increasing price sensitivity among suppliers. Differentiation through metal cards, tokenization, or eco-materials reduces pure price play and supports premium pricing. Card networks mandate PCI DSS and EMV compliance and banks typically demand high SLAs (commonly 99.99% availability).

Telecom operators

Telecom operators buy SIM/eSIM and device-activation services at scale, driving tough negotiations on volume, roadmaps and total cost of ownership; major carriers pressure suppliers for multi-year SLAs. eSIM shifts value toward software provisioning and platforms, with GSMA reporting over 1 billion eSIM-capable devices by 2024, while high churn rates force suppliers to offer end-to-end lifecycle platforms to retain customers.

Switching and standards

Standards-based products reduce buyer lock-in across segments, but certification, stored personalization data and integration create practical switching frictions; in 2024 about 58% of enterprises report dual-vendor or pilot-lot strategies to preserve optionality. Buyers use pilot lots and dual sourcing to leverage better terms, while long contracts commonly embed penalty and performance clauses that raise exit costs. Suppliers face pressure to certify and integrate or risk commoditization.

- Standards lower lock-in

- Certification, data, integration increase frictions

- 58% use dual vendors/pilots (2024)

- Long contracts include penalties

Demand cyclicality

Demand cyclicality: card reissuance cycles (typically 3–5 years), periodic national ID program waves and telco upgrade windows drive order volatility; buyers time procurements to market conditions and pushed discounts of roughly 5–15% in downturns in 2024, while predictable run-rates secured 3–10% better supplier terms; customization can trade 5–20% margin for increased customer stickiness.

- Card cycles: 3–5 years

- Buyer discounts: 5–15% (2024)

- Run-rate premium: 3–10%

- Customization margin trade: 5–20%

Regulation, PCI/EMV SLAs and eSIM scale squeeze margins, raise switching frictions

Governments exert strong price and compliance pressure on large, bid-driven ID contracts with rebids every 5–10 years. Banks multi-source cards/authentication, demanding PCI/EMV compliance and 99.99% SLAs, raising price sensitivity. Telcos drive volume-negotiation and eSIM/software value (over 1 billion eSIM-capable devices by 2024); standards cut lock-in but certification/data create switching frictions.

| Metric | 2024 |

|---|---|

| Dual-vendor/pilot use | 58% |

| Buyer discounts (downturn) | 5–15% |

| Card reissue cycle | 3–5 yrs |

| eSIM-capable devices | >1B |

Same Document Delivered

Valid SA Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Valid SA you’ll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file for your strategic and investment decisions.

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot outlines the competitive pressures facing Valid SA—supplier leverage, buyer bargaining, new entrants, substitutes, and competitive rivalry. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable implications tailored to Valid SA. Purchase the complete report for a consultant-grade, data-driven strategic roadmap you can use in presentations or investment decisions.

Suppliers Bargaining Power

Specialized components

Valid relies on secure chips, secure elements and specialty substrates sourced from few qualified global suppliers, giving suppliers strong leverage; qualification cycles typically run 6–18 months and 2024 foundry constraints pushed lead times to roughly 20–40 weeks, raising pricing risk; dual-sourcing mitigates exposure but equivalency must pass full certifications, adding time and cost.

Security materials

Overt and covert security features for civil IDs and bank cards are niche and IP-protected, letting specialized suppliers extract premium pricing; vendors with proprietary holograms, inks and laminates often dominate tender evaluations. Switching suppliers forces redesigns and document re-certification, delaying rollouts and raising costs. Supply assurances are tightly tied to compliance and chain-of-custody standards such as ISO 14298.

PKI and software stacks

Digital certification depends on cryptographic libraries, HSMs and licensed middleware, with major suppliers (Thales, Entrust, Utimaco, AWS CloudHSM) dominating integrations and raising vendor lock-in risks; FIPS 140-3 became the baseline after 2023 and remained central to regulatory validation in 2024. Open standards and FIPS/Common Criteria certification provide negotiation leverage, but cloud bundling and integrated key management often shift power back to providers.

Telecom modules

Telecom modules: SIM/eSIM profiles and IoT modules require certified components and secure OSes, and a few global suppliers (Quectel, Fibocom, Thales/Infineon, Sierra Wireless) dominate supply, concentrating risk. Carrier certifications in 2024 typically took 3–9 months, limiting substitution speed and forcing volume commitments and roadmap alignment for multi-year deals.

- Concentration: top vendors dominate supply

- Certification: 3–9 months (2024)

- Contracts: volume commitments common

- Roadmap: alignment required for carrier approval

Skilled talent

- Talent scarcity: 3.4M shortfall (ISC2, 2023)

- Hiring difficulty: 68% employers (2024)

- Cost pressure: ~20–30% higher hiring/retention costs

- Mitigation: nearshoring/training lower but not remove risk

Suppliers retain pricing power: 20-40 week lead times, 3-9 month certs, talent gap hikes costs

Suppliers hold strong leverage due to concentrated secure-chip, HSM and niche security-material markets; 2024 lead times 20–40 weeks and FIPS 140-3 baseline increase switching costs. Certifications take 3–9 months, forcing volume commitments and roadmap alignment. Talent shortfall (ISC2 3.4M) and 68% hiring difficulty in 2024 raise labour costs ~20–30%, preserving supplier power.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Lead times | 20–40 weeks | Higher prices, delays |

| Certifications | 3–9 months | Slow substitution |

| Talent | 3.4M shortfall / 68% hiring difficulty | +20–30% costs |

What is included in the product

Concise Porter's Five Forces for Valid SA uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes and disruptive threats, with industry data and strategic implications for pricing and profitability.

Clear one-sheet Porter's Five Forces for Valid SA—instantly visualize competitive pressure with an editable spider chart and customizable force levels, ready to drop into pitch decks or integrated Excel dashboards for fast, board-ready decisions.

Customers Bargaining Power

Government megabuyers

Civil ID and track-and-trace contracts are large, long-term and bid-driven, with flagship programs like India’s Aadhaar serving about 1.25 billion identities highlighting scale. Governments wield strong price and compliance pressure via competitive tenders; switching costs exist but rebids every 5–10 years can reset commercial terms. Political and data-sovereignty clauses further tighten contractual expectations.

Banks and issuers

Financial institutions buy millions of payment cards and authentication services annually and routinely multi-source via aggressive RFPs, increasing price sensitivity among suppliers. Differentiation through metal cards, tokenization, or eco-materials reduces pure price play and supports premium pricing. Card networks mandate PCI DSS and EMV compliance and banks typically demand high SLAs (commonly 99.99% availability).

Telecom operators

Telecom operators buy SIM/eSIM and device-activation services at scale, driving tough negotiations on volume, roadmaps and total cost of ownership; major carriers pressure suppliers for multi-year SLAs. eSIM shifts value toward software provisioning and platforms, with GSMA reporting over 1 billion eSIM-capable devices by 2024, while high churn rates force suppliers to offer end-to-end lifecycle platforms to retain customers.

Switching and standards

Standards-based products reduce buyer lock-in across segments, but certification, stored personalization data and integration create practical switching frictions; in 2024 about 58% of enterprises report dual-vendor or pilot-lot strategies to preserve optionality. Buyers use pilot lots and dual sourcing to leverage better terms, while long contracts commonly embed penalty and performance clauses that raise exit costs. Suppliers face pressure to certify and integrate or risk commoditization.

- Standards lower lock-in

- Certification, data, integration increase frictions

- 58% use dual vendors/pilots (2024)

- Long contracts include penalties

Demand cyclicality

Demand cyclicality: card reissuance cycles (typically 3–5 years), periodic national ID program waves and telco upgrade windows drive order volatility; buyers time procurements to market conditions and pushed discounts of roughly 5–15% in downturns in 2024, while predictable run-rates secured 3–10% better supplier terms; customization can trade 5–20% margin for increased customer stickiness.

- Card cycles: 3–5 years

- Buyer discounts: 5–15% (2024)

- Run-rate premium: 3–10%

- Customization margin trade: 5–20%

Regulation, PCI/EMV SLAs and eSIM scale squeeze margins, raise switching frictions

Governments exert strong price and compliance pressure on large, bid-driven ID contracts with rebids every 5–10 years. Banks multi-source cards/authentication, demanding PCI/EMV compliance and 99.99% SLAs, raising price sensitivity. Telcos drive volume-negotiation and eSIM/software value (over 1 billion eSIM-capable devices by 2024); standards cut lock-in but certification/data create switching frictions.

| Metric | 2024 |

|---|---|

| Dual-vendor/pilot use | 58% |

| Buyer discounts (downturn) | 5–15% |

| Card reissue cycle | 3–5 yrs |

| eSIM-capable devices | >1B |

Same Document Delivered

Valid SA Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Valid SA you’ll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file for your strategic and investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot outlines the competitive pressures facing Valid SA—supplier leverage, buyer bargaining, new entrants, substitutes, and competitive rivalry. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable implications tailored to Valid SA. Purchase the complete report for a consultant-grade, data-driven strategic roadmap you can use in presentations or investment decisions.

Suppliers Bargaining Power

Specialized components

Valid relies on secure chips, secure elements and specialty substrates sourced from few qualified global suppliers, giving suppliers strong leverage; qualification cycles typically run 6–18 months and 2024 foundry constraints pushed lead times to roughly 20–40 weeks, raising pricing risk; dual-sourcing mitigates exposure but equivalency must pass full certifications, adding time and cost.

Security materials

Overt and covert security features for civil IDs and bank cards are niche and IP-protected, letting specialized suppliers extract premium pricing; vendors with proprietary holograms, inks and laminates often dominate tender evaluations. Switching suppliers forces redesigns and document re-certification, delaying rollouts and raising costs. Supply assurances are tightly tied to compliance and chain-of-custody standards such as ISO 14298.

PKI and software stacks

Digital certification depends on cryptographic libraries, HSMs and licensed middleware, with major suppliers (Thales, Entrust, Utimaco, AWS CloudHSM) dominating integrations and raising vendor lock-in risks; FIPS 140-3 became the baseline after 2023 and remained central to regulatory validation in 2024. Open standards and FIPS/Common Criteria certification provide negotiation leverage, but cloud bundling and integrated key management often shift power back to providers.

Telecom modules

Telecom modules: SIM/eSIM profiles and IoT modules require certified components and secure OSes, and a few global suppliers (Quectel, Fibocom, Thales/Infineon, Sierra Wireless) dominate supply, concentrating risk. Carrier certifications in 2024 typically took 3–9 months, limiting substitution speed and forcing volume commitments and roadmap alignment for multi-year deals.

- Concentration: top vendors dominate supply

- Certification: 3–9 months (2024)

- Contracts: volume commitments common

- Roadmap: alignment required for carrier approval

Skilled talent

- Talent scarcity: 3.4M shortfall (ISC2, 2023)

- Hiring difficulty: 68% employers (2024)

- Cost pressure: ~20–30% higher hiring/retention costs

- Mitigation: nearshoring/training lower but not remove risk

Suppliers retain pricing power: 20-40 week lead times, 3-9 month certs, talent gap hikes costs

Suppliers hold strong leverage due to concentrated secure-chip, HSM and niche security-material markets; 2024 lead times 20–40 weeks and FIPS 140-3 baseline increase switching costs. Certifications take 3–9 months, forcing volume commitments and roadmap alignment. Talent shortfall (ISC2 3.4M) and 68% hiring difficulty in 2024 raise labour costs ~20–30%, preserving supplier power.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Lead times | 20–40 weeks | Higher prices, delays |

| Certifications | 3–9 months | Slow substitution |

| Talent | 3.4M shortfall / 68% hiring difficulty | +20–30% costs |

What is included in the product

Concise Porter's Five Forces for Valid SA uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitutes and disruptive threats, with industry data and strategic implications for pricing and profitability.

Clear one-sheet Porter's Five Forces for Valid SA—instantly visualize competitive pressure with an editable spider chart and customizable force levels, ready to drop into pitch decks or integrated Excel dashboards for fast, board-ready decisions.

Customers Bargaining Power

Government megabuyers

Civil ID and track-and-trace contracts are large, long-term and bid-driven, with flagship programs like India’s Aadhaar serving about 1.25 billion identities highlighting scale. Governments wield strong price and compliance pressure via competitive tenders; switching costs exist but rebids every 5–10 years can reset commercial terms. Political and data-sovereignty clauses further tighten contractual expectations.

Banks and issuers

Financial institutions buy millions of payment cards and authentication services annually and routinely multi-source via aggressive RFPs, increasing price sensitivity among suppliers. Differentiation through metal cards, tokenization, or eco-materials reduces pure price play and supports premium pricing. Card networks mandate PCI DSS and EMV compliance and banks typically demand high SLAs (commonly 99.99% availability).

Telecom operators

Telecom operators buy SIM/eSIM and device-activation services at scale, driving tough negotiations on volume, roadmaps and total cost of ownership; major carriers pressure suppliers for multi-year SLAs. eSIM shifts value toward software provisioning and platforms, with GSMA reporting over 1 billion eSIM-capable devices by 2024, while high churn rates force suppliers to offer end-to-end lifecycle platforms to retain customers.

Switching and standards

Standards-based products reduce buyer lock-in across segments, but certification, stored personalization data and integration create practical switching frictions; in 2024 about 58% of enterprises report dual-vendor or pilot-lot strategies to preserve optionality. Buyers use pilot lots and dual sourcing to leverage better terms, while long contracts commonly embed penalty and performance clauses that raise exit costs. Suppliers face pressure to certify and integrate or risk commoditization.

- Standards lower lock-in

- Certification, data, integration increase frictions

- 58% use dual vendors/pilots (2024)

- Long contracts include penalties

Demand cyclicality

Demand cyclicality: card reissuance cycles (typically 3–5 years), periodic national ID program waves and telco upgrade windows drive order volatility; buyers time procurements to market conditions and pushed discounts of roughly 5–15% in downturns in 2024, while predictable run-rates secured 3–10% better supplier terms; customization can trade 5–20% margin for increased customer stickiness.

- Card cycles: 3–5 years

- Buyer discounts: 5–15% (2024)

- Run-rate premium: 3–10%

- Customization margin trade: 5–20%

Regulation, PCI/EMV SLAs and eSIM scale squeeze margins, raise switching frictions

Governments exert strong price and compliance pressure on large, bid-driven ID contracts with rebids every 5–10 years. Banks multi-source cards/authentication, demanding PCI/EMV compliance and 99.99% SLAs, raising price sensitivity. Telcos drive volume-negotiation and eSIM/software value (over 1 billion eSIM-capable devices by 2024); standards cut lock-in but certification/data create switching frictions.

| Metric | 2024 |

|---|---|

| Dual-vendor/pilot use | 58% |

| Buyer discounts (downturn) | 5–15% |

| Card reissue cycle | 3–5 yrs |

| eSIM-capable devices | >1B |

Same Document Delivered

Valid SA Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Valid SA you’ll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical file for your strategic and investment decisions.