Valneva Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

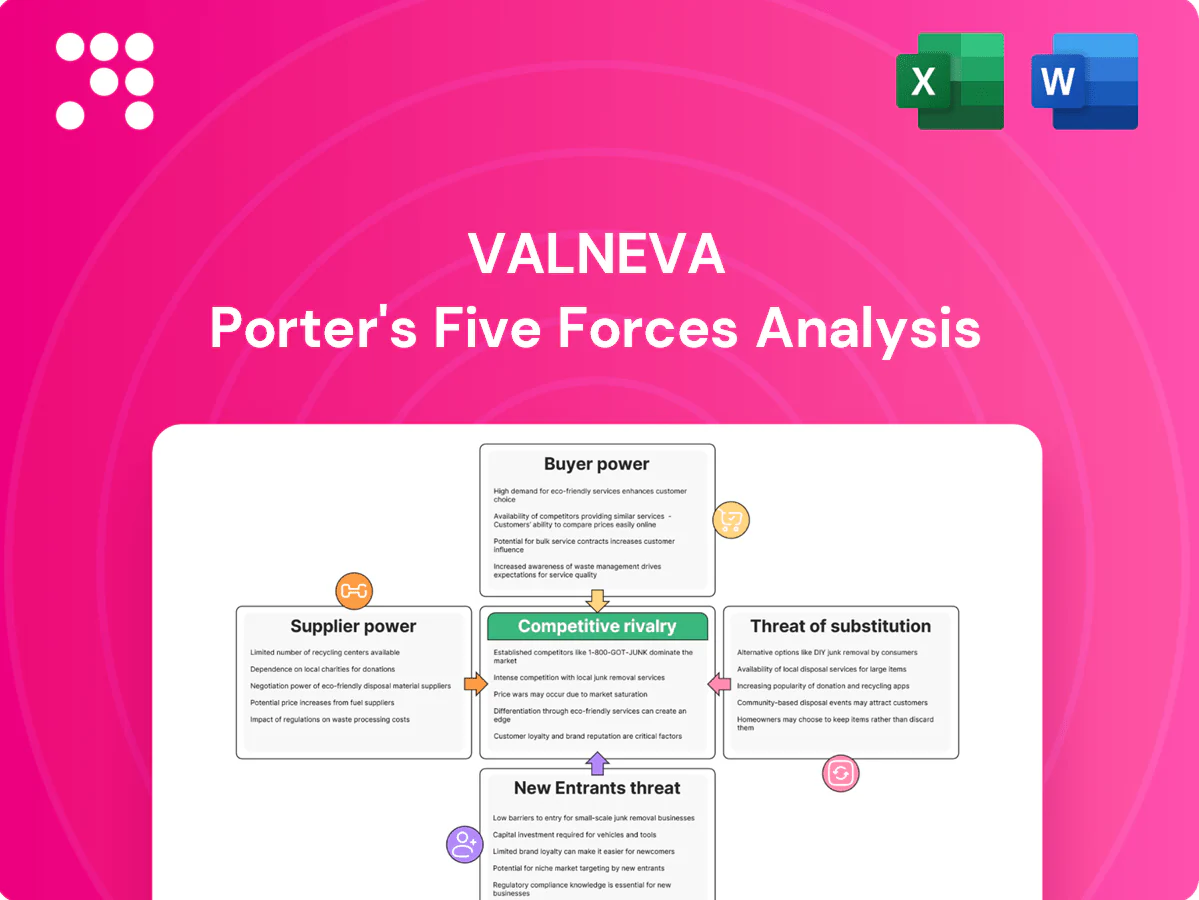

Valneva operates in a capital‑intensive, regulation‑heavy vaccine market where high entry barriers and proprietary assets limit new entrants, yet supplier concentration and pricing pressures from large buyers create tension. Competitive rivalry and substitute technologies warrant close monitoring. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Valneva’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized biologics and adjuvant inputs

By 2024 Valneva depends on niche inputs—cell substrates, adjuvants and single‑use bioprocess components—from a small pool of qualified vendors, making supplier concentration and qualification requirements a key source of high switching costs; any supplier disruption risks batch release delays and regulatory timeline slippage, and while long‑term supply agreements reduce volatility they do not eliminate exposure.

GMP manufacturing equipment and consumables

GMP equipment and consumables for Valneva are highly concentrated in 2024, with top three suppliers (Sartorius/Cytiva/Thermo Fisher) commanding about 65–75% of bioreactor, resin and sterile consumable supply; supplier leverage is amplified by typical lead times of 12–24 weeks and extensive validation burdens. Standardized single‑use systems cut risk but validated process lock‑in persists, and dual‑sourcing remains feasible yet typically adds $1–3M in qualification costs and ~10–20% ongoing supply overhead.

CDMO and fill‑finish capacity constraints

External aseptic fill‑finish and specialty capacity is frequently tight, with industry utilization exceeding 85% in peak cycles (2024 data) and localized shortages during demand surges. Qualified CDMOs can command price premiums of 15–30% in peak periods, pressuring margins. Deviations or scheduling conflicts can delay launches and add significant cost, so strategic capacity reservations and selective in‑house capabilities are essential to balance this supplier power.

Cold‑chain logistics and specialty distributors

Temperature‑controlled distribution for Valneva is mission‑critical and concentrated among a few specialist providers; the global pharmaceutical cold‑chain market was about 24 billion USD in 2023, keeping bargaining power elevated. Service‑level failures can cause spoilage and recalls—WHO estimates up to 50% vaccine wastage in some contexts—amplifying supplier influence. Compliance and serialization requirements increase switching costs, while multi‑provider networks and redundancy materially reduce single‑supplier dependency.

- Concentration: few specialists dominate high‑value pharma lanes

- Risk: spoilage/recall exposure (WHO up to 50% vaccine wastage)

- Complexity: serialization/compliance raise switching costs

- Mitigation: multi‑provider networks and redundancy lower dependency

IP, assays, and reference standards

Access to proprietary assays, reference materials, and licensed technologies often resides with a few specialized licensors, giving them leverage via royalty terms and restrictive usage rights; published industry royalty ranges for assays and bioassays commonly fall between 3% and 8% of product net sales. Validation of alternative methods is lengthy, typically 6–18 months, increasing switching costs for Valneva. Negotiating broader field‑of‑use and step‑in rights can materially rebalance supplier power and protect time-to-market.

- Concentration: few licensors control key IP

- Royalty pressure: typical assay royalties 3–8%

- Switching cost: validation 6–18 months

- Mitigation: secure field-of-use + step-in rights

2024 supplier bottlenecks: bioprocess, CDMO, cold-chain and IP risks raise costs and delays

By 2024 Valneva faces high supplier power: core bioprocess suppliers (Sartorius/Cytiva/Thermo Fisher) supply ~65–75% of equipment with 12–24 week lead times and dual‑sourcing adding $1–3M plus 10–20% overhead. CDMO fill‑finish tightness (industry utilization >85%) lets providers charge 15–30% premiums; cold‑chain ties to a $24B market (2023) with WHO vaccine wastage up to 50%. Assay/IP licensors levy 3–8% royalties and 6–18 month validation timelines, making supplier risk material to cost and timelines.

| Category | Metric (2023/24) | Impact |

|---|---|---|

| Bioprocess suppliers | 65–75% share; 12–24 wk lead | High switching cost |

| CDMO capacity | >85% util.; 15–30% premium | Launch delay/cost |

| Cold‑chain | $24B market; wastage ≤50% | Supply risk |

| Assay/IP | 3–8% royalties; 6–18 mo val. | Royalty + timeline risk |

What is included in the product

Tailored Porter's Five Forces analysis of Valneva uncovering competitive intensity, buyer and supplier bargaining power, threats from new entrants and substitutes, and industry disruptors impacting pricing and profitability; includes strategic implications for protecting market share and growth opportunities.

A concise one-sheet Porter's Five Forces for Valneva that clarifies competitive, supplier, buyer and regulatory pressures—ideal for rapid strategic decisions and boardroom briefings.

Customers Bargaining Power

Government and supranational tenders

Government agencies, WHO, UNICEF and regional consortia (UNICEF procures over 2.5 billion vaccine doses annually in 2024) buy via large tenders, concentrating volume and using global price benchmarks to exert strong buyer power. Limited supplier options for some indications moderate pricing pressure, while proven performance and supply reliability are decisive for winning and retaining awards.

Payers and HTA-driven pricing

Reimbursement hinges on cost‑effectiveness and budget‑impact models, with HTA bodies shaping list and net prices; for example NICE uses ≈£20,000–30,000 per QALY as its reference range. HTA outcomes create payer leverage in negotiations, while robust real‑world evidence strengthens value claims and defenders of higher net prices; clear unmet‑need positioning helps preserve premium pricing for novel vaccines.

Travel clinics and private providers

Travel clinics and private providers benchmark Valneva vaccines on efficacy, safety profile, dosing schedule convenience, and cold-chain handling when choosing brands. In categories with few substitutes buyer power is moderate, though discounts and service terms materially influence formulary placement and purchasing rhythm. Ongoing medical education programs and proven supply reliability consistently sway clinic decisions toward preferred suppliers.

Strategic partners and co-development deals

Large pharma strategic partners bring capital and market access but exert strong bargaining power, often driving milestone, profit‑share and territorial clauses that reflect their leverage in co‑development deals.

Performance clauses and governance structures determine Valneva’s value capture, with balanced risk‑sharing and clear incentive alignment improving outcomes.

End-user sensitivity to price and dosing

In 2024 patients and travelers remain highly sensitive to out‑of‑pocket cost and dosing burden; shorter schedules and favorable safety profiles can materially offset price pressure and raise uptake. Clear communication on disease risk increases willingness to pay, while vaccine stock‑outs or complex cold‑chain logistics shift bargaining power back to buyers.

- Sensitivity: high out‑of‑pocket concern

- Dosing: shorter schedules reduce price pressure

- Communication: risk messaging raises willingness to pay

- Supply: stock‑outs/complex logistics favor buyers

Buyers concentrate power: large tenders (>2.5bn doses), HTA cost pressure

Buyers concentrated: WHO/UNICEF/regional consortia (UNICEF procures >2.5bn doses in 2024) use large tenders and global benchmarks, driving strong buyer power. HTA/payers (NICE ≈£20k–30k/QALY) enforce cost‑effectiveness and net price pressure. Strategic partners exert high deal leverage via milestones and profit‑share. Patient sensitivity to OOP costs and dosing schedules materially affects uptake.

| Metric | 2024 Value |

|---|---|

| UNICEF annual doses | >2.5bn |

| NICE reference | ≈£20k–30k/QALY |

| Patient OOP sensitivity | High |

Same Document Delivered

Valneva Porter's Five Forces Analysis

This Valneva Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive immediately after purchase, with no placeholders or mockups. It contains the complete competitive assessment ready for download and use. Purchase grants instant access to this identical file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Valneva operates in a capital‑intensive, regulation‑heavy vaccine market where high entry barriers and proprietary assets limit new entrants, yet supplier concentration and pricing pressures from large buyers create tension. Competitive rivalry and substitute technologies warrant close monitoring. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Valneva’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized biologics and adjuvant inputs

By 2024 Valneva depends on niche inputs—cell substrates, adjuvants and single‑use bioprocess components—from a small pool of qualified vendors, making supplier concentration and qualification requirements a key source of high switching costs; any supplier disruption risks batch release delays and regulatory timeline slippage, and while long‑term supply agreements reduce volatility they do not eliminate exposure.

GMP manufacturing equipment and consumables

GMP equipment and consumables for Valneva are highly concentrated in 2024, with top three suppliers (Sartorius/Cytiva/Thermo Fisher) commanding about 65–75% of bioreactor, resin and sterile consumable supply; supplier leverage is amplified by typical lead times of 12–24 weeks and extensive validation burdens. Standardized single‑use systems cut risk but validated process lock‑in persists, and dual‑sourcing remains feasible yet typically adds $1–3M in qualification costs and ~10–20% ongoing supply overhead.

CDMO and fill‑finish capacity constraints

External aseptic fill‑finish and specialty capacity is frequently tight, with industry utilization exceeding 85% in peak cycles (2024 data) and localized shortages during demand surges. Qualified CDMOs can command price premiums of 15–30% in peak periods, pressuring margins. Deviations or scheduling conflicts can delay launches and add significant cost, so strategic capacity reservations and selective in‑house capabilities are essential to balance this supplier power.

Cold‑chain logistics and specialty distributors

Temperature‑controlled distribution for Valneva is mission‑critical and concentrated among a few specialist providers; the global pharmaceutical cold‑chain market was about 24 billion USD in 2023, keeping bargaining power elevated. Service‑level failures can cause spoilage and recalls—WHO estimates up to 50% vaccine wastage in some contexts—amplifying supplier influence. Compliance and serialization requirements increase switching costs, while multi‑provider networks and redundancy materially reduce single‑supplier dependency.

- Concentration: few specialists dominate high‑value pharma lanes

- Risk: spoilage/recall exposure (WHO up to 50% vaccine wastage)

- Complexity: serialization/compliance raise switching costs

- Mitigation: multi‑provider networks and redundancy lower dependency

IP, assays, and reference standards

Access to proprietary assays, reference materials, and licensed technologies often resides with a few specialized licensors, giving them leverage via royalty terms and restrictive usage rights; published industry royalty ranges for assays and bioassays commonly fall between 3% and 8% of product net sales. Validation of alternative methods is lengthy, typically 6–18 months, increasing switching costs for Valneva. Negotiating broader field‑of‑use and step‑in rights can materially rebalance supplier power and protect time-to-market.

- Concentration: few licensors control key IP

- Royalty pressure: typical assay royalties 3–8%

- Switching cost: validation 6–18 months

- Mitigation: secure field-of-use + step-in rights

2024 supplier bottlenecks: bioprocess, CDMO, cold-chain and IP risks raise costs and delays

By 2024 Valneva faces high supplier power: core bioprocess suppliers (Sartorius/Cytiva/Thermo Fisher) supply ~65–75% of equipment with 12–24 week lead times and dual‑sourcing adding $1–3M plus 10–20% overhead. CDMO fill‑finish tightness (industry utilization >85%) lets providers charge 15–30% premiums; cold‑chain ties to a $24B market (2023) with WHO vaccine wastage up to 50%. Assay/IP licensors levy 3–8% royalties and 6–18 month validation timelines, making supplier risk material to cost and timelines.

| Category | Metric (2023/24) | Impact |

|---|---|---|

| Bioprocess suppliers | 65–75% share; 12–24 wk lead | High switching cost |

| CDMO capacity | >85% util.; 15–30% premium | Launch delay/cost |

| Cold‑chain | $24B market; wastage ≤50% | Supply risk |

| Assay/IP | 3–8% royalties; 6–18 mo val. | Royalty + timeline risk |

What is included in the product

Tailored Porter's Five Forces analysis of Valneva uncovering competitive intensity, buyer and supplier bargaining power, threats from new entrants and substitutes, and industry disruptors impacting pricing and profitability; includes strategic implications for protecting market share and growth opportunities.

A concise one-sheet Porter's Five Forces for Valneva that clarifies competitive, supplier, buyer and regulatory pressures—ideal for rapid strategic decisions and boardroom briefings.

Customers Bargaining Power

Government and supranational tenders

Government agencies, WHO, UNICEF and regional consortia (UNICEF procures over 2.5 billion vaccine doses annually in 2024) buy via large tenders, concentrating volume and using global price benchmarks to exert strong buyer power. Limited supplier options for some indications moderate pricing pressure, while proven performance and supply reliability are decisive for winning and retaining awards.

Payers and HTA-driven pricing

Reimbursement hinges on cost‑effectiveness and budget‑impact models, with HTA bodies shaping list and net prices; for example NICE uses ≈£20,000–30,000 per QALY as its reference range. HTA outcomes create payer leverage in negotiations, while robust real‑world evidence strengthens value claims and defenders of higher net prices; clear unmet‑need positioning helps preserve premium pricing for novel vaccines.

Travel clinics and private providers

Travel clinics and private providers benchmark Valneva vaccines on efficacy, safety profile, dosing schedule convenience, and cold-chain handling when choosing brands. In categories with few substitutes buyer power is moderate, though discounts and service terms materially influence formulary placement and purchasing rhythm. Ongoing medical education programs and proven supply reliability consistently sway clinic decisions toward preferred suppliers.

Strategic partners and co-development deals

Large pharma strategic partners bring capital and market access but exert strong bargaining power, often driving milestone, profit‑share and territorial clauses that reflect their leverage in co‑development deals.

Performance clauses and governance structures determine Valneva’s value capture, with balanced risk‑sharing and clear incentive alignment improving outcomes.

End-user sensitivity to price and dosing

In 2024 patients and travelers remain highly sensitive to out‑of‑pocket cost and dosing burden; shorter schedules and favorable safety profiles can materially offset price pressure and raise uptake. Clear communication on disease risk increases willingness to pay, while vaccine stock‑outs or complex cold‑chain logistics shift bargaining power back to buyers.

- Sensitivity: high out‑of‑pocket concern

- Dosing: shorter schedules reduce price pressure

- Communication: risk messaging raises willingness to pay

- Supply: stock‑outs/complex logistics favor buyers

Buyers concentrate power: large tenders (>2.5bn doses), HTA cost pressure

Buyers concentrated: WHO/UNICEF/regional consortia (UNICEF procures >2.5bn doses in 2024) use large tenders and global benchmarks, driving strong buyer power. HTA/payers (NICE ≈£20k–30k/QALY) enforce cost‑effectiveness and net price pressure. Strategic partners exert high deal leverage via milestones and profit‑share. Patient sensitivity to OOP costs and dosing schedules materially affects uptake.

| Metric | 2024 Value |

|---|---|

| UNICEF annual doses | >2.5bn |

| NICE reference | ≈£20k–30k/QALY |

| Patient OOP sensitivity | High |

Same Document Delivered

Valneva Porter's Five Forces Analysis

This Valneva Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive immediately after purchase, with no placeholders or mockups. It contains the complete competitive assessment ready for download and use. Purchase grants instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Valneva operates in a capital‑intensive, regulation‑heavy vaccine market where high entry barriers and proprietary assets limit new entrants, yet supplier concentration and pricing pressures from large buyers create tension. Competitive rivalry and substitute technologies warrant close monitoring. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Valneva’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized biologics and adjuvant inputs

By 2024 Valneva depends on niche inputs—cell substrates, adjuvants and single‑use bioprocess components—from a small pool of qualified vendors, making supplier concentration and qualification requirements a key source of high switching costs; any supplier disruption risks batch release delays and regulatory timeline slippage, and while long‑term supply agreements reduce volatility they do not eliminate exposure.

GMP manufacturing equipment and consumables

GMP equipment and consumables for Valneva are highly concentrated in 2024, with top three suppliers (Sartorius/Cytiva/Thermo Fisher) commanding about 65–75% of bioreactor, resin and sterile consumable supply; supplier leverage is amplified by typical lead times of 12–24 weeks and extensive validation burdens. Standardized single‑use systems cut risk but validated process lock‑in persists, and dual‑sourcing remains feasible yet typically adds $1–3M in qualification costs and ~10–20% ongoing supply overhead.

CDMO and fill‑finish capacity constraints

External aseptic fill‑finish and specialty capacity is frequently tight, with industry utilization exceeding 85% in peak cycles (2024 data) and localized shortages during demand surges. Qualified CDMOs can command price premiums of 15–30% in peak periods, pressuring margins. Deviations or scheduling conflicts can delay launches and add significant cost, so strategic capacity reservations and selective in‑house capabilities are essential to balance this supplier power.

Cold‑chain logistics and specialty distributors

Temperature‑controlled distribution for Valneva is mission‑critical and concentrated among a few specialist providers; the global pharmaceutical cold‑chain market was about 24 billion USD in 2023, keeping bargaining power elevated. Service‑level failures can cause spoilage and recalls—WHO estimates up to 50% vaccine wastage in some contexts—amplifying supplier influence. Compliance and serialization requirements increase switching costs, while multi‑provider networks and redundancy materially reduce single‑supplier dependency.

- Concentration: few specialists dominate high‑value pharma lanes

- Risk: spoilage/recall exposure (WHO up to 50% vaccine wastage)

- Complexity: serialization/compliance raise switching costs

- Mitigation: multi‑provider networks and redundancy lower dependency

IP, assays, and reference standards

Access to proprietary assays, reference materials, and licensed technologies often resides with a few specialized licensors, giving them leverage via royalty terms and restrictive usage rights; published industry royalty ranges for assays and bioassays commonly fall between 3% and 8% of product net sales. Validation of alternative methods is lengthy, typically 6–18 months, increasing switching costs for Valneva. Negotiating broader field‑of‑use and step‑in rights can materially rebalance supplier power and protect time-to-market.

- Concentration: few licensors control key IP

- Royalty pressure: typical assay royalties 3–8%

- Switching cost: validation 6–18 months

- Mitigation: secure field-of-use + step-in rights

2024 supplier bottlenecks: bioprocess, CDMO, cold-chain and IP risks raise costs and delays

By 2024 Valneva faces high supplier power: core bioprocess suppliers (Sartorius/Cytiva/Thermo Fisher) supply ~65–75% of equipment with 12–24 week lead times and dual‑sourcing adding $1–3M plus 10–20% overhead. CDMO fill‑finish tightness (industry utilization >85%) lets providers charge 15–30% premiums; cold‑chain ties to a $24B market (2023) with WHO vaccine wastage up to 50%. Assay/IP licensors levy 3–8% royalties and 6–18 month validation timelines, making supplier risk material to cost and timelines.

| Category | Metric (2023/24) | Impact |

|---|---|---|

| Bioprocess suppliers | 65–75% share; 12–24 wk lead | High switching cost |

| CDMO capacity | >85% util.; 15–30% premium | Launch delay/cost |

| Cold‑chain | $24B market; wastage ≤50% | Supply risk |

| Assay/IP | 3–8% royalties; 6–18 mo val. | Royalty + timeline risk |

What is included in the product

Tailored Porter's Five Forces analysis of Valneva uncovering competitive intensity, buyer and supplier bargaining power, threats from new entrants and substitutes, and industry disruptors impacting pricing and profitability; includes strategic implications for protecting market share and growth opportunities.

A concise one-sheet Porter's Five Forces for Valneva that clarifies competitive, supplier, buyer and regulatory pressures—ideal for rapid strategic decisions and boardroom briefings.

Customers Bargaining Power

Government and supranational tenders

Government agencies, WHO, UNICEF and regional consortia (UNICEF procures over 2.5 billion vaccine doses annually in 2024) buy via large tenders, concentrating volume and using global price benchmarks to exert strong buyer power. Limited supplier options for some indications moderate pricing pressure, while proven performance and supply reliability are decisive for winning and retaining awards.

Payers and HTA-driven pricing

Reimbursement hinges on cost‑effectiveness and budget‑impact models, with HTA bodies shaping list and net prices; for example NICE uses ≈£20,000–30,000 per QALY as its reference range. HTA outcomes create payer leverage in negotiations, while robust real‑world evidence strengthens value claims and defenders of higher net prices; clear unmet‑need positioning helps preserve premium pricing for novel vaccines.

Travel clinics and private providers

Travel clinics and private providers benchmark Valneva vaccines on efficacy, safety profile, dosing schedule convenience, and cold-chain handling when choosing brands. In categories with few substitutes buyer power is moderate, though discounts and service terms materially influence formulary placement and purchasing rhythm. Ongoing medical education programs and proven supply reliability consistently sway clinic decisions toward preferred suppliers.

Strategic partners and co-development deals

Large pharma strategic partners bring capital and market access but exert strong bargaining power, often driving milestone, profit‑share and territorial clauses that reflect their leverage in co‑development deals.

Performance clauses and governance structures determine Valneva’s value capture, with balanced risk‑sharing and clear incentive alignment improving outcomes.

End-user sensitivity to price and dosing

In 2024 patients and travelers remain highly sensitive to out‑of‑pocket cost and dosing burden; shorter schedules and favorable safety profiles can materially offset price pressure and raise uptake. Clear communication on disease risk increases willingness to pay, while vaccine stock‑outs or complex cold‑chain logistics shift bargaining power back to buyers.

- Sensitivity: high out‑of‑pocket concern

- Dosing: shorter schedules reduce price pressure

- Communication: risk messaging raises willingness to pay

- Supply: stock‑outs/complex logistics favor buyers

Buyers concentrate power: large tenders (>2.5bn doses), HTA cost pressure

Buyers concentrated: WHO/UNICEF/regional consortia (UNICEF procures >2.5bn doses in 2024) use large tenders and global benchmarks, driving strong buyer power. HTA/payers (NICE ≈£20k–30k/QALY) enforce cost‑effectiveness and net price pressure. Strategic partners exert high deal leverage via milestones and profit‑share. Patient sensitivity to OOP costs and dosing schedules materially affects uptake.

| Metric | 2024 Value |

|---|---|

| UNICEF annual doses | >2.5bn |

| NICE reference | ≈£20k–30k/QALY |

| Patient OOP sensitivity | High |

Same Document Delivered

Valneva Porter's Five Forces Analysis

This Valneva Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive immediately after purchase, with no placeholders or mockups. It contains the complete competitive assessment ready for download and use. Purchase grants instant access to this identical file.