Vantiva Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

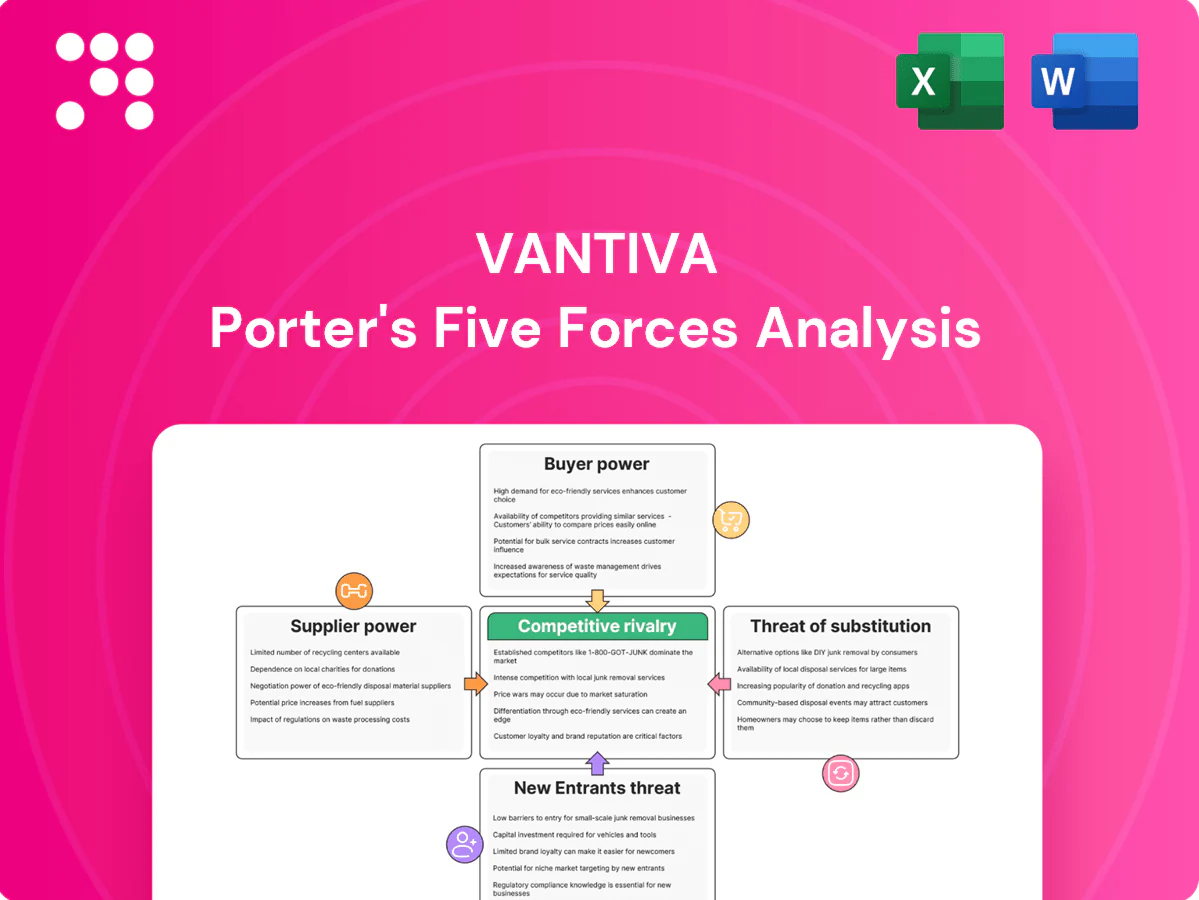

Vantiva faces moderate supplier leverage, intense buyer price sensitivity, and rising substitute threats from streaming and smart TVs, while regulatory and tech shifts shape entry barriers. Competitive rivalry is high amid consolidation and margin pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vantiva’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor concentration

Core set-top box chipsets are concentrated among a few suppliers—notably Broadcom, Amlogic and MediaTek—giving vendors pricing and allocation leverage. Design-in cycles typically lock Vantiva to platforms for 3–5 years, raising switching costs and roadmap dependency. In tight markets lead times can exceed 20 weeks, increasing launch delays. Any allocation squeeze directly compresses margins and revenue timing.

Software/IP licensors

Software and IP licensors for DRM, middleware, codecs and OS control critical pieces of Vantiva products, constraining design choices and integrations. Certification and compliance regimes (operator/STB/streaming) narrow alternatives and raise switching costs. Royalty structures, commonly in the 1–5% range of unit price, squeeze unit economics, while renewal terms can force roadmap shifts and delay time-to-market.

Contract manufacturing/EMS

Vantiva relies on Asian ODM/EMS partners that provide scale—Asia accounts for roughly 70% of global electronics manufacturing—yet these partners can exert leverage by prioritizing capacity during peak demand. Tooling and NRE create path dependence as sunk capital ties Vantiva to specific suppliers. Quality and yield shortfalls translate into rework and warranty costs borne by Vantiva, and consolidation among EMS players (top vendors controlling ~50% of EMS revenue) narrows bargaining room.

Specialized components

Tuners, Wi-Fi modules and secure elements for Vantiva have few qualified sources, giving suppliers notable leverage; multi-year security certifications in 2024 keep substitution slow and costly. Component shortages can force redesigns or expensive spot buys, letting suppliers shape BOMs and delivery schedules and increase lead-time risk.

- Few qualified sources: tuners, Wi-Fi, secure elements

- 2024: multi-year certifications slow swaps

- Shortages force redesigns or spot buys

- Suppliers influence BOM and delivery timing

Logistics and media inputs

For DVD services, polycarbonate, packaging and freight markets materially affect unit cost; polycarbonate and packaging input inflation contributed to a mid-single-digit cost rise in 2024, while freight rate volatility (around ±30% in 2024) shifted bargaining power to carriers. Fuel price swings and container rate spikes amplified carrier leverage, and tight studio release windows concentrate logistics power; supplier delays can breach SLAs and trigger penalty clauses.

- polycarbonate & packaging: mid-single-digit cost pressure (2024)

- freight volatility: ~±30% (2024)

- time-sensitive releases: increased logistics leverage

- supplier delays: SLA breaches → penalties

Supplier concentration, long lead times and royalties squeeze margins; cost volatility raises risk

Supplier concentration (Broadcom, Amlogic, MediaTek) and 3–5yr design-ins give suppliers pricing/allocation leverage; lead times >20 weeks raise launch risk. Royalties (1–5% of unit price), EMS consolidation (~50% top vendors) and Asia manufacturing share (~70%) compress margins; polycarbonate up mid-single-digit and freight ±30% in 2024 add cost volatility.

| Category | Impact | 2024 data |

|---|---|---|

| Core chipsets | High leverage | 3 suppliers |

| Lead times | Delays/risk | >20 weeks |

| Royalties | Margin pressure | 1–5% unit price |

| EMS/Asia | Switching cost | EMS top ~50% / Asia ~70% |

| Materials & freight | Cost volatility | Polycarbonate mid-single-digit; freight ±30% |

What is included in the product

Uncovers key drivers of competition, customer and supplier influence, substitutes, and entry risks specific to Vantiva, assessing how these forces shape pricing, margins, and strategic positioning. Fully editable Word format for easy integration into investor materials, strategy decks, or academic projects.

One-sheet Porter's Five Forces for Vantiva that visualizes competitive pressure with a spider chart, lets you customize scores/labels, swap in current data, and export clean slides—no macros or coding required—so teams can quickly diagnose strategic risks and build board-ready recommendations.

Customers Bargaining Power

Operator concentration

Pay-TV and broadband operators are few, large and price-sensitive: the top 5 global operators served over 500 million subs in 2024, concentrating buying power and driving aggressive RFPs. RFP-driven procurement compresses margins, often yielding supplier discounts in the 10–25% range and favoring lowest-cost bids. High-volume contracts (frequently >$100m) amplify switching threats, while bespoke operator customization can shift 5–15% extra engineering/BOM costs onto Vantiva.

Studio dependence (DVD)

Major studios in 2024 retained strong negotiating leverage on DVD replication terms, dictating pricing, delivery windows and return policies that compress vendor margins. Volume variability tied to blockbuster cycles makes pricing episodic, with physical order spikes around tentpole releases and sharp troughs off-cycle. The ongoing shift to digital in 2024 has reduced buyer commitment to physical media, while stringent SLAs and chargebacks shift operational and financial risk onto the replication vendor.

Specification control

Customers dictate hardware, software and security specs, forcing Vantiva to meet regional compliance gates that in 2024 produced winner-take-all awards per region. Feature creep without commensurate price lift has compressed margins. Long acceptance cycles in 2024 have delayed revenue recognition and extended cash conversion periods. This specification control concentrates bargaining power with buyers.

Multi-sourcing norms

Operators routinely benchmark vendors and split awards across 2–3 suppliers to retain negotiating leverage; incumbency improves win probability but is no longer secure. Continuous benchmarking forces vendors into ongoing cost-reduction cycles, and buyers can rapidly reallocate volumes after performance lapses, increasing churn risk for Vantiva.

- Benchmarking: split awards 2–3 vendors

- Incumbency: valuable but fragile

- Cost pressure: continuous downward pricing

- Reallocation risk: rapid volume shifts on lapses

Total cost focus

Buyers push Vantiva to optimize total cost of ownership across hardware, support and field ops, using remote diagnostics and low DOA expectations as pricing leverage; Vantiva, listed on Euronext Paris (VIVA), faces penalties that shift lifecycle costs back to the supplier.

- Buyers focus TCO

- Remote diagnostics = pricing leverage

- Low DOA rates demanded

- Returns penalties raise supplier lifecycle costs

- Service bundling required to defend ASPs

Top-5 buyers (>500m) force 10–25% supplier discounts, shorten incumbency

Buyers concentrated (top 5 operators >500m subs in 2024) exert strong price pressure, driving RFPs that yield supplier discounts of 10–25% and favor lowest-cost bids. Large contracts (>€100m) and spec control (5–15% extra customization costs) amplify switching risk; benchmarking and split awards (2–3 vendors) force continuous cost cuts and shorten incumbency advantages.

| Metric | 2024 |

|---|---|

| Top-5 operator subs | >500m |

| Typical supplier discounts | 10–25% |

| Large contract size | >€100m |

| Customization cost uplift | 5–15% |

| Supplier split | 2–3 vendors |

Preview the Actual Deliverable

Vantiva Porter's Five Forces Analysis

This preview shows the exact Vantiva Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is the full, professionally formatted deliverable and will be available for immediate download upon payment. It’s ready to use in reports or presentations.

Go Beyond the Preview—Access the Full Strategic Report

Vantiva faces moderate supplier leverage, intense buyer price sensitivity, and rising substitute threats from streaming and smart TVs, while regulatory and tech shifts shape entry barriers. Competitive rivalry is high amid consolidation and margin pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vantiva’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor concentration

Core set-top box chipsets are concentrated among a few suppliers—notably Broadcom, Amlogic and MediaTek—giving vendors pricing and allocation leverage. Design-in cycles typically lock Vantiva to platforms for 3–5 years, raising switching costs and roadmap dependency. In tight markets lead times can exceed 20 weeks, increasing launch delays. Any allocation squeeze directly compresses margins and revenue timing.

Software/IP licensors

Software and IP licensors for DRM, middleware, codecs and OS control critical pieces of Vantiva products, constraining design choices and integrations. Certification and compliance regimes (operator/STB/streaming) narrow alternatives and raise switching costs. Royalty structures, commonly in the 1–5% range of unit price, squeeze unit economics, while renewal terms can force roadmap shifts and delay time-to-market.

Contract manufacturing/EMS

Vantiva relies on Asian ODM/EMS partners that provide scale—Asia accounts for roughly 70% of global electronics manufacturing—yet these partners can exert leverage by prioritizing capacity during peak demand. Tooling and NRE create path dependence as sunk capital ties Vantiva to specific suppliers. Quality and yield shortfalls translate into rework and warranty costs borne by Vantiva, and consolidation among EMS players (top vendors controlling ~50% of EMS revenue) narrows bargaining room.

Specialized components

Tuners, Wi-Fi modules and secure elements for Vantiva have few qualified sources, giving suppliers notable leverage; multi-year security certifications in 2024 keep substitution slow and costly. Component shortages can force redesigns or expensive spot buys, letting suppliers shape BOMs and delivery schedules and increase lead-time risk.

- Few qualified sources: tuners, Wi-Fi, secure elements

- 2024: multi-year certifications slow swaps

- Shortages force redesigns or spot buys

- Suppliers influence BOM and delivery timing

Logistics and media inputs

For DVD services, polycarbonate, packaging and freight markets materially affect unit cost; polycarbonate and packaging input inflation contributed to a mid-single-digit cost rise in 2024, while freight rate volatility (around ±30% in 2024) shifted bargaining power to carriers. Fuel price swings and container rate spikes amplified carrier leverage, and tight studio release windows concentrate logistics power; supplier delays can breach SLAs and trigger penalty clauses.

- polycarbonate & packaging: mid-single-digit cost pressure (2024)

- freight volatility: ~±30% (2024)

- time-sensitive releases: increased logistics leverage

- supplier delays: SLA breaches → penalties

Supplier concentration, long lead times and royalties squeeze margins; cost volatility raises risk

Supplier concentration (Broadcom, Amlogic, MediaTek) and 3–5yr design-ins give suppliers pricing/allocation leverage; lead times >20 weeks raise launch risk. Royalties (1–5% of unit price), EMS consolidation (~50% top vendors) and Asia manufacturing share (~70%) compress margins; polycarbonate up mid-single-digit and freight ±30% in 2024 add cost volatility.

| Category | Impact | 2024 data |

|---|---|---|

| Core chipsets | High leverage | 3 suppliers |

| Lead times | Delays/risk | >20 weeks |

| Royalties | Margin pressure | 1–5% unit price |

| EMS/Asia | Switching cost | EMS top ~50% / Asia ~70% |

| Materials & freight | Cost volatility | Polycarbonate mid-single-digit; freight ±30% |

What is included in the product

Uncovers key drivers of competition, customer and supplier influence, substitutes, and entry risks specific to Vantiva, assessing how these forces shape pricing, margins, and strategic positioning. Fully editable Word format for easy integration into investor materials, strategy decks, or academic projects.

One-sheet Porter's Five Forces for Vantiva that visualizes competitive pressure with a spider chart, lets you customize scores/labels, swap in current data, and export clean slides—no macros or coding required—so teams can quickly diagnose strategic risks and build board-ready recommendations.

Customers Bargaining Power

Operator concentration

Pay-TV and broadband operators are few, large and price-sensitive: the top 5 global operators served over 500 million subs in 2024, concentrating buying power and driving aggressive RFPs. RFP-driven procurement compresses margins, often yielding supplier discounts in the 10–25% range and favoring lowest-cost bids. High-volume contracts (frequently >$100m) amplify switching threats, while bespoke operator customization can shift 5–15% extra engineering/BOM costs onto Vantiva.

Studio dependence (DVD)

Major studios in 2024 retained strong negotiating leverage on DVD replication terms, dictating pricing, delivery windows and return policies that compress vendor margins. Volume variability tied to blockbuster cycles makes pricing episodic, with physical order spikes around tentpole releases and sharp troughs off-cycle. The ongoing shift to digital in 2024 has reduced buyer commitment to physical media, while stringent SLAs and chargebacks shift operational and financial risk onto the replication vendor.

Specification control

Customers dictate hardware, software and security specs, forcing Vantiva to meet regional compliance gates that in 2024 produced winner-take-all awards per region. Feature creep without commensurate price lift has compressed margins. Long acceptance cycles in 2024 have delayed revenue recognition and extended cash conversion periods. This specification control concentrates bargaining power with buyers.

Multi-sourcing norms

Operators routinely benchmark vendors and split awards across 2–3 suppliers to retain negotiating leverage; incumbency improves win probability but is no longer secure. Continuous benchmarking forces vendors into ongoing cost-reduction cycles, and buyers can rapidly reallocate volumes after performance lapses, increasing churn risk for Vantiva.

- Benchmarking: split awards 2–3 vendors

- Incumbency: valuable but fragile

- Cost pressure: continuous downward pricing

- Reallocation risk: rapid volume shifts on lapses

Total cost focus

Buyers push Vantiva to optimize total cost of ownership across hardware, support and field ops, using remote diagnostics and low DOA expectations as pricing leverage; Vantiva, listed on Euronext Paris (VIVA), faces penalties that shift lifecycle costs back to the supplier.

- Buyers focus TCO

- Remote diagnostics = pricing leverage

- Low DOA rates demanded

- Returns penalties raise supplier lifecycle costs

- Service bundling required to defend ASPs

Top-5 buyers (>500m) force 10–25% supplier discounts, shorten incumbency

Buyers concentrated (top 5 operators >500m subs in 2024) exert strong price pressure, driving RFPs that yield supplier discounts of 10–25% and favor lowest-cost bids. Large contracts (>€100m) and spec control (5–15% extra customization costs) amplify switching risk; benchmarking and split awards (2–3 vendors) force continuous cost cuts and shorten incumbency advantages.

| Metric | 2024 |

|---|---|

| Top-5 operator subs | >500m |

| Typical supplier discounts | 10–25% |

| Large contract size | >€100m |

| Customization cost uplift | 5–15% |

| Supplier split | 2–3 vendors |

Preview the Actual Deliverable

Vantiva Porter's Five Forces Analysis

This preview shows the exact Vantiva Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is the full, professionally formatted deliverable and will be available for immediate download upon payment. It’s ready to use in reports or presentations.

Description

Go Beyond the Preview—Access the Full Strategic Report

Vantiva faces moderate supplier leverage, intense buyer price sensitivity, and rising substitute threats from streaming and smart TVs, while regulatory and tech shifts shape entry barriers. Competitive rivalry is high amid consolidation and margin pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vantiva’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Semiconductor concentration

Core set-top box chipsets are concentrated among a few suppliers—notably Broadcom, Amlogic and MediaTek—giving vendors pricing and allocation leverage. Design-in cycles typically lock Vantiva to platforms for 3–5 years, raising switching costs and roadmap dependency. In tight markets lead times can exceed 20 weeks, increasing launch delays. Any allocation squeeze directly compresses margins and revenue timing.

Software/IP licensors

Software and IP licensors for DRM, middleware, codecs and OS control critical pieces of Vantiva products, constraining design choices and integrations. Certification and compliance regimes (operator/STB/streaming) narrow alternatives and raise switching costs. Royalty structures, commonly in the 1–5% range of unit price, squeeze unit economics, while renewal terms can force roadmap shifts and delay time-to-market.

Contract manufacturing/EMS

Vantiva relies on Asian ODM/EMS partners that provide scale—Asia accounts for roughly 70% of global electronics manufacturing—yet these partners can exert leverage by prioritizing capacity during peak demand. Tooling and NRE create path dependence as sunk capital ties Vantiva to specific suppliers. Quality and yield shortfalls translate into rework and warranty costs borne by Vantiva, and consolidation among EMS players (top vendors controlling ~50% of EMS revenue) narrows bargaining room.

Specialized components

Tuners, Wi-Fi modules and secure elements for Vantiva have few qualified sources, giving suppliers notable leverage; multi-year security certifications in 2024 keep substitution slow and costly. Component shortages can force redesigns or expensive spot buys, letting suppliers shape BOMs and delivery schedules and increase lead-time risk.

- Few qualified sources: tuners, Wi-Fi, secure elements

- 2024: multi-year certifications slow swaps

- Shortages force redesigns or spot buys

- Suppliers influence BOM and delivery timing

Logistics and media inputs

For DVD services, polycarbonate, packaging and freight markets materially affect unit cost; polycarbonate and packaging input inflation contributed to a mid-single-digit cost rise in 2024, while freight rate volatility (around ±30% in 2024) shifted bargaining power to carriers. Fuel price swings and container rate spikes amplified carrier leverage, and tight studio release windows concentrate logistics power; supplier delays can breach SLAs and trigger penalty clauses.

- polycarbonate & packaging: mid-single-digit cost pressure (2024)

- freight volatility: ~±30% (2024)

- time-sensitive releases: increased logistics leverage

- supplier delays: SLA breaches → penalties

Supplier concentration, long lead times and royalties squeeze margins; cost volatility raises risk

Supplier concentration (Broadcom, Amlogic, MediaTek) and 3–5yr design-ins give suppliers pricing/allocation leverage; lead times >20 weeks raise launch risk. Royalties (1–5% of unit price), EMS consolidation (~50% top vendors) and Asia manufacturing share (~70%) compress margins; polycarbonate up mid-single-digit and freight ±30% in 2024 add cost volatility.

| Category | Impact | 2024 data |

|---|---|---|

| Core chipsets | High leverage | 3 suppliers |

| Lead times | Delays/risk | >20 weeks |

| Royalties | Margin pressure | 1–5% unit price |

| EMS/Asia | Switching cost | EMS top ~50% / Asia ~70% |

| Materials & freight | Cost volatility | Polycarbonate mid-single-digit; freight ±30% |

What is included in the product

Uncovers key drivers of competition, customer and supplier influence, substitutes, and entry risks specific to Vantiva, assessing how these forces shape pricing, margins, and strategic positioning. Fully editable Word format for easy integration into investor materials, strategy decks, or academic projects.

One-sheet Porter's Five Forces for Vantiva that visualizes competitive pressure with a spider chart, lets you customize scores/labels, swap in current data, and export clean slides—no macros or coding required—so teams can quickly diagnose strategic risks and build board-ready recommendations.

Customers Bargaining Power

Operator concentration

Pay-TV and broadband operators are few, large and price-sensitive: the top 5 global operators served over 500 million subs in 2024, concentrating buying power and driving aggressive RFPs. RFP-driven procurement compresses margins, often yielding supplier discounts in the 10–25% range and favoring lowest-cost bids. High-volume contracts (frequently >$100m) amplify switching threats, while bespoke operator customization can shift 5–15% extra engineering/BOM costs onto Vantiva.

Studio dependence (DVD)

Major studios in 2024 retained strong negotiating leverage on DVD replication terms, dictating pricing, delivery windows and return policies that compress vendor margins. Volume variability tied to blockbuster cycles makes pricing episodic, with physical order spikes around tentpole releases and sharp troughs off-cycle. The ongoing shift to digital in 2024 has reduced buyer commitment to physical media, while stringent SLAs and chargebacks shift operational and financial risk onto the replication vendor.

Specification control

Customers dictate hardware, software and security specs, forcing Vantiva to meet regional compliance gates that in 2024 produced winner-take-all awards per region. Feature creep without commensurate price lift has compressed margins. Long acceptance cycles in 2024 have delayed revenue recognition and extended cash conversion periods. This specification control concentrates bargaining power with buyers.

Multi-sourcing norms

Operators routinely benchmark vendors and split awards across 2–3 suppliers to retain negotiating leverage; incumbency improves win probability but is no longer secure. Continuous benchmarking forces vendors into ongoing cost-reduction cycles, and buyers can rapidly reallocate volumes after performance lapses, increasing churn risk for Vantiva.

- Benchmarking: split awards 2–3 vendors

- Incumbency: valuable but fragile

- Cost pressure: continuous downward pricing

- Reallocation risk: rapid volume shifts on lapses

Total cost focus

Buyers push Vantiva to optimize total cost of ownership across hardware, support and field ops, using remote diagnostics and low DOA expectations as pricing leverage; Vantiva, listed on Euronext Paris (VIVA), faces penalties that shift lifecycle costs back to the supplier.

- Buyers focus TCO

- Remote diagnostics = pricing leverage

- Low DOA rates demanded

- Returns penalties raise supplier lifecycle costs

- Service bundling required to defend ASPs

Top-5 buyers (>500m) force 10–25% supplier discounts, shorten incumbency

Buyers concentrated (top 5 operators >500m subs in 2024) exert strong price pressure, driving RFPs that yield supplier discounts of 10–25% and favor lowest-cost bids. Large contracts (>€100m) and spec control (5–15% extra customization costs) amplify switching risk; benchmarking and split awards (2–3 vendors) force continuous cost cuts and shorten incumbency advantages.

| Metric | 2024 |

|---|---|

| Top-5 operator subs | >500m |

| Typical supplier discounts | 10–25% |

| Large contract size | >€100m |

| Customization cost uplift | 5–15% |

| Supplier split | 2–3 vendors |

Preview the Actual Deliverable

Vantiva Porter's Five Forces Analysis

This preview shows the exact Vantiva Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is the full, professionally formatted deliverable and will be available for immediate download upon payment. It’s ready to use in reports or presentations.