Vector Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

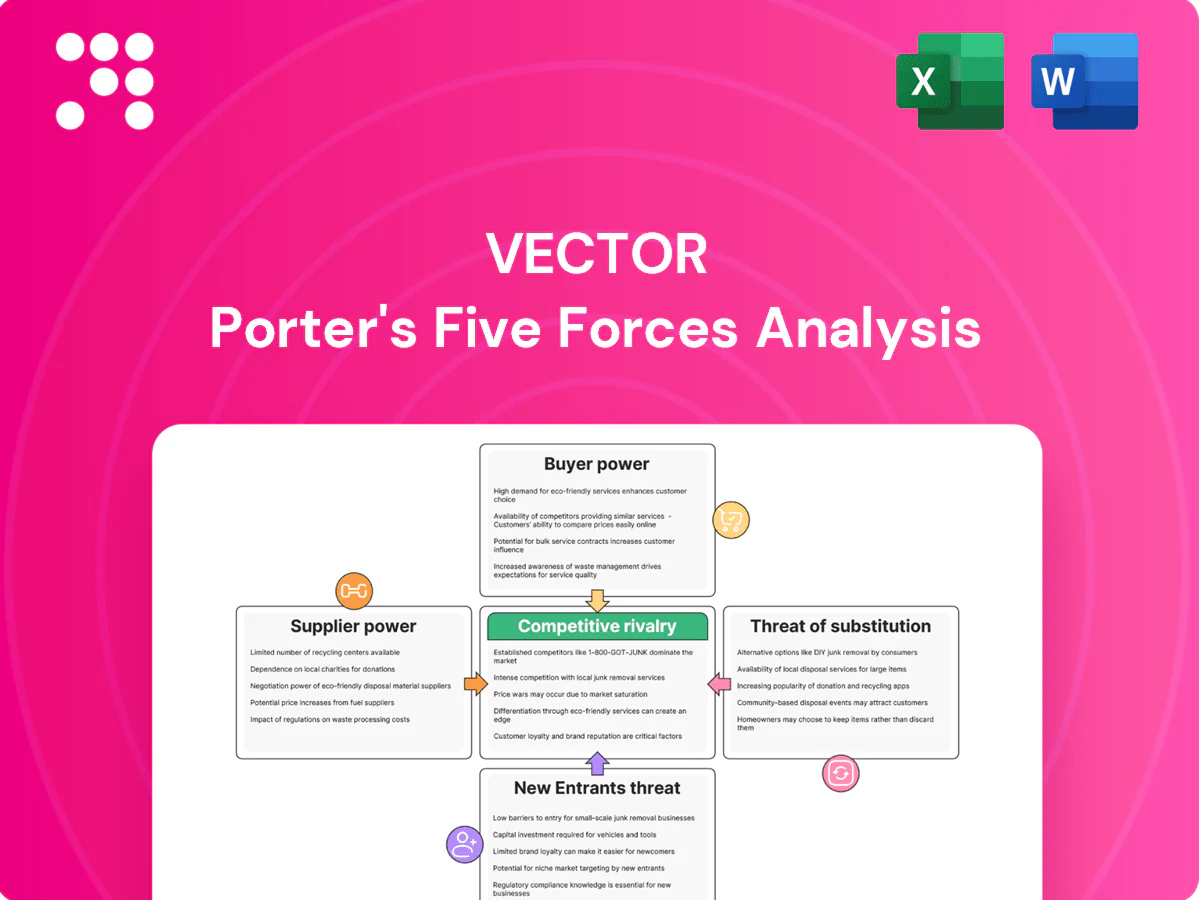

Vector's Porter's Five Forces snapshot outlines competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry to clarify industry pressure points. It highlights where Vector holds advantage and where strategic risks lie. This preview points to actionable themes for strategy and investment. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and tailored recommendations.

Suppliers Bargaining Power

Dominant ad/tech platforms

Google (Alphabet reported $224.5B ad revenue in 2023) and Meta ($116.6B in 2023), plus X (~500M MAUs) and LINE (Japan ~86M MAUs), concentrate reach and data, giving rate-setting power; algorithm changes can raise CPMs or erode campaign ROI with little notice. Vector must maintain multi-platform expertise to mitigate dependency; long-term spend commitments can secure better rates but increase client and platform lock-in risk.

Media outlets and publishers

Tier-1 Japanese media and key vertical publishers control scarce earned-media inventory, creating access bottlenecks across national audiences (Japan population ~125 million in 2024). Exclusive editorial calendars and longstanding relationships concentrate influence despite high internet penetration (~93% in 2024). Strong PR craft and clear newsworthiness can offset publisher leverage but cannot fully neutralize it. Seasonal spikes (New Year, Golden Week) sharply increase placement competition and pricing.

Influencers and talent agencies

High-demand creators and talent agencies extract premium fees—the influencer market reached about $24 billion in 2024—while top creators can command six-figure single-post deals and agencies charge 10–30% commissions. Availability constraints and strict brand-safety filters raise transaction complexity and vetting costs. Direct marketplaces cut intermediary layers but cannot eliminate star power premiums. Long-term ambassador contracts (12–36 months) stabilize rates yet reduce flexibility.

Creative/freelance specialists

Top creatives, videographers and niche translators remain scarce, giving suppliers leverage while project timing pressures enable freelancers to charge rush premiums typically 15–50%; 2024 platform sign-ups rose ~12% increasing available talent but not eliminating skill gaps.

- Scarcity: high demand for niche skills

- Rush premium: 15–50%

- Mitigation: preferred rosters, internal training, remote hiring

Data/MarTech and measurement providers

Attribution, social listening and IR tools become highly sticky once embedded, driving renewal dependence and allowing vendors to push price escalators and tiered-features that raise total cost of ownership; global MarTech spend topped $100B in 2024, amplifying supplier leverage. Privacy and API shifts (e.g., recent platform API deprecations) can force costly re-integration, while diversified vendor stacks and stronger first-party data reduce supplier bargaining power.

- Sticky integrations

- Price escalators/TCO

- Privacy/API risk

- First-party data strengthens buyers

Platform giants, top publishers and creators set ad rates; first-party data cuts supplier leverage

Platform giants (Google ad rev $224.5B 2023; Meta ad rev $116.6B 2023) and top Japanese publishers (reach vs Japan pop ~125M in 2024) exert strong rate-setting power; creators and agencies (influencer market ~$24B 2024) extract premiums. Sticky MarTech (global spend >$100B 2024) raises TCO; first-party data and multi-platform expertise reduce supplier leverage.

| Supplier | Power | Metric (2023/2024) |

|---|---|---|

| Platforms | High | Google $224.5B, Meta $116.6B |

| Publishers | High | Japan pop ~125M (2024) |

| Creators | High | Influencer market ~$24B (2024) |

| MarTech | Sticky | Spend >$100B (2024) |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Vector, highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and market entry barriers to inform strategic, investor, or academic use.

Quickly distill competitive pressure into a single, customizable Five Forces dashboard—ideal for fast strategic decisions and investor decks.

Customers Bargaining Power

Enterprise procurement rigor

Enterprise procurement rigor in 2024 sees large Japanese corporates using competitive RFPs and framework agreements to compress fees and narrow scopes, while vendor consolidation further tightens margins. Demonstrable ROI and a strong compliance track record are decisive selection criteria in these procurements. Securing multi-year framework wins offsets pricing pressure by delivering volume stability and predictable revenue streams.

Low switching costs in PR/marketing

Clients commonly rotate PR/marketing agencies by campaign or fiscal year, with WARC/ISBA 2024 reporting global client churn around 12%. Knowledge-transfer frictions exist but are routinely managed via playbooks and documentation, cutting onboarding time significantly. Performance slumps trigger rapid reallocations, keeping bargaining power high. Deep embedding in strategy and analytics, however, raises exit costs and can reduce churn by an estimated 20–30%.

In-house teams as alternatives

By 2024 many companies increasingly benchmark agency pricing against growing in-house PR and digital teams, pushing agencies to justify fees. Agencies must therefore deliver capabilities or speed—content scale, analytics, crisis IR—that in-house units cannot match. Hybrid models shifting execution to clients compress agency margins while strategic advisory and investor relations expertise preserve premium value.

Outcome-based and risk-sharing models

Clients increasingly demand KPI-linked, outcome-based fees to de-risk spend, shifting performance risk to agencies and raising revenue volatility; measurement changes and cookie deprecation in 2024 accelerated this shift. Agencies protect economics through robust measurement frameworks, disciplined test-and-learn and clear scope guardrails to prevent value leakage.

- Clients: KPI-linked fees shift risk to agencies

- Impact: higher revenue volatility

- Mitigation: strong measurement & test-and-learn

- Control: clear scope guardrails to prevent leakage

Startups and VC portfolio dynamics

Startups are price sensitive with constrained budgets yet can scale quickly, keeping buyer power high early but diminishing as customers grow; Vector’s VC arm builds pipeline and stickiness by embedding offerings in portfolio companies, reducing churn. Equity-for-services aligns incentives and boosts lifetime value while introducing concentration and valuation risk. Documented portfolio wins increase cross-sell credibility and negotiating leverage.

- VC-driven pipeline: boosts retention

- Equity-for-services: aligns incentives, raises risk

- Startups: high price sensitivity, rapid scale potential

- Case studies: improve cross-sell and reduce buyer leverage

Client leverage: 12% churn; embedding lowers 20–30%

Clients exhibit high bargaining power: global client churn ~12% in 2024 (WARC/ISBA), with KPI-linked, outcome-based fees increasing revenue volatility. Multi-year framework wins and deep strategic embedding reduce churn by 20–30% and stabilize margins. Agencies must prove ROI, compliance and unique capabilities to resist fee compression.

| Metric | 2024 | Impact |

|---|---|---|

| Client churn | 12% | High buyer leverage |

| Embedding effect | 20–30% churn ↓ | Revenue stability |

Preview Before You Purchase

Vector Porter's Five Forces Analysis

This preview shows the exact Vector Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this same file.

Go Beyond the Preview—Access the Full Strategic Report

Vector's Porter's Five Forces snapshot outlines competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry to clarify industry pressure points. It highlights where Vector holds advantage and where strategic risks lie. This preview points to actionable themes for strategy and investment. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and tailored recommendations.

Suppliers Bargaining Power

Dominant ad/tech platforms

Google (Alphabet reported $224.5B ad revenue in 2023) and Meta ($116.6B in 2023), plus X (~500M MAUs) and LINE (Japan ~86M MAUs), concentrate reach and data, giving rate-setting power; algorithm changes can raise CPMs or erode campaign ROI with little notice. Vector must maintain multi-platform expertise to mitigate dependency; long-term spend commitments can secure better rates but increase client and platform lock-in risk.

Media outlets and publishers

Tier-1 Japanese media and key vertical publishers control scarce earned-media inventory, creating access bottlenecks across national audiences (Japan population ~125 million in 2024). Exclusive editorial calendars and longstanding relationships concentrate influence despite high internet penetration (~93% in 2024). Strong PR craft and clear newsworthiness can offset publisher leverage but cannot fully neutralize it. Seasonal spikes (New Year, Golden Week) sharply increase placement competition and pricing.

Influencers and talent agencies

High-demand creators and talent agencies extract premium fees—the influencer market reached about $24 billion in 2024—while top creators can command six-figure single-post deals and agencies charge 10–30% commissions. Availability constraints and strict brand-safety filters raise transaction complexity and vetting costs. Direct marketplaces cut intermediary layers but cannot eliminate star power premiums. Long-term ambassador contracts (12–36 months) stabilize rates yet reduce flexibility.

Creative/freelance specialists

Top creatives, videographers and niche translators remain scarce, giving suppliers leverage while project timing pressures enable freelancers to charge rush premiums typically 15–50%; 2024 platform sign-ups rose ~12% increasing available talent but not eliminating skill gaps.

- Scarcity: high demand for niche skills

- Rush premium: 15–50%

- Mitigation: preferred rosters, internal training, remote hiring

Data/MarTech and measurement providers

Attribution, social listening and IR tools become highly sticky once embedded, driving renewal dependence and allowing vendors to push price escalators and tiered-features that raise total cost of ownership; global MarTech spend topped $100B in 2024, amplifying supplier leverage. Privacy and API shifts (e.g., recent platform API deprecations) can force costly re-integration, while diversified vendor stacks and stronger first-party data reduce supplier bargaining power.

- Sticky integrations

- Price escalators/TCO

- Privacy/API risk

- First-party data strengthens buyers

Platform giants, top publishers and creators set ad rates; first-party data cuts supplier leverage

Platform giants (Google ad rev $224.5B 2023; Meta ad rev $116.6B 2023) and top Japanese publishers (reach vs Japan pop ~125M in 2024) exert strong rate-setting power; creators and agencies (influencer market ~$24B 2024) extract premiums. Sticky MarTech (global spend >$100B 2024) raises TCO; first-party data and multi-platform expertise reduce supplier leverage.

| Supplier | Power | Metric (2023/2024) |

|---|---|---|

| Platforms | High | Google $224.5B, Meta $116.6B |

| Publishers | High | Japan pop ~125M (2024) |

| Creators | High | Influencer market ~$24B (2024) |

| MarTech | Sticky | Spend >$100B (2024) |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Vector, highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and market entry barriers to inform strategic, investor, or academic use.

Quickly distill competitive pressure into a single, customizable Five Forces dashboard—ideal for fast strategic decisions and investor decks.

Customers Bargaining Power

Enterprise procurement rigor

Enterprise procurement rigor in 2024 sees large Japanese corporates using competitive RFPs and framework agreements to compress fees and narrow scopes, while vendor consolidation further tightens margins. Demonstrable ROI and a strong compliance track record are decisive selection criteria in these procurements. Securing multi-year framework wins offsets pricing pressure by delivering volume stability and predictable revenue streams.

Low switching costs in PR/marketing

Clients commonly rotate PR/marketing agencies by campaign or fiscal year, with WARC/ISBA 2024 reporting global client churn around 12%. Knowledge-transfer frictions exist but are routinely managed via playbooks and documentation, cutting onboarding time significantly. Performance slumps trigger rapid reallocations, keeping bargaining power high. Deep embedding in strategy and analytics, however, raises exit costs and can reduce churn by an estimated 20–30%.

In-house teams as alternatives

By 2024 many companies increasingly benchmark agency pricing against growing in-house PR and digital teams, pushing agencies to justify fees. Agencies must therefore deliver capabilities or speed—content scale, analytics, crisis IR—that in-house units cannot match. Hybrid models shifting execution to clients compress agency margins while strategic advisory and investor relations expertise preserve premium value.

Outcome-based and risk-sharing models

Clients increasingly demand KPI-linked, outcome-based fees to de-risk spend, shifting performance risk to agencies and raising revenue volatility; measurement changes and cookie deprecation in 2024 accelerated this shift. Agencies protect economics through robust measurement frameworks, disciplined test-and-learn and clear scope guardrails to prevent value leakage.

- Clients: KPI-linked fees shift risk to agencies

- Impact: higher revenue volatility

- Mitigation: strong measurement & test-and-learn

- Control: clear scope guardrails to prevent leakage

Startups and VC portfolio dynamics

Startups are price sensitive with constrained budgets yet can scale quickly, keeping buyer power high early but diminishing as customers grow; Vector’s VC arm builds pipeline and stickiness by embedding offerings in portfolio companies, reducing churn. Equity-for-services aligns incentives and boosts lifetime value while introducing concentration and valuation risk. Documented portfolio wins increase cross-sell credibility and negotiating leverage.

- VC-driven pipeline: boosts retention

- Equity-for-services: aligns incentives, raises risk

- Startups: high price sensitivity, rapid scale potential

- Case studies: improve cross-sell and reduce buyer leverage

Client leverage: 12% churn; embedding lowers 20–30%

Clients exhibit high bargaining power: global client churn ~12% in 2024 (WARC/ISBA), with KPI-linked, outcome-based fees increasing revenue volatility. Multi-year framework wins and deep strategic embedding reduce churn by 20–30% and stabilize margins. Agencies must prove ROI, compliance and unique capabilities to resist fee compression.

| Metric | 2024 | Impact |

|---|---|---|

| Client churn | 12% | High buyer leverage |

| Embedding effect | 20–30% churn ↓ | Revenue stability |

Preview Before You Purchase

Vector Porter's Five Forces Analysis

This preview shows the exact Vector Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Vector's Porter's Five Forces snapshot outlines competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry to clarify industry pressure points. It highlights where Vector holds advantage and where strategic risks lie. This preview points to actionable themes for strategy and investment. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and tailored recommendations.

Suppliers Bargaining Power

Dominant ad/tech platforms

Google (Alphabet reported $224.5B ad revenue in 2023) and Meta ($116.6B in 2023), plus X (~500M MAUs) and LINE (Japan ~86M MAUs), concentrate reach and data, giving rate-setting power; algorithm changes can raise CPMs or erode campaign ROI with little notice. Vector must maintain multi-platform expertise to mitigate dependency; long-term spend commitments can secure better rates but increase client and platform lock-in risk.

Media outlets and publishers

Tier-1 Japanese media and key vertical publishers control scarce earned-media inventory, creating access bottlenecks across national audiences (Japan population ~125 million in 2024). Exclusive editorial calendars and longstanding relationships concentrate influence despite high internet penetration (~93% in 2024). Strong PR craft and clear newsworthiness can offset publisher leverage but cannot fully neutralize it. Seasonal spikes (New Year, Golden Week) sharply increase placement competition and pricing.

Influencers and talent agencies

High-demand creators and talent agencies extract premium fees—the influencer market reached about $24 billion in 2024—while top creators can command six-figure single-post deals and agencies charge 10–30% commissions. Availability constraints and strict brand-safety filters raise transaction complexity and vetting costs. Direct marketplaces cut intermediary layers but cannot eliminate star power premiums. Long-term ambassador contracts (12–36 months) stabilize rates yet reduce flexibility.

Creative/freelance specialists

Top creatives, videographers and niche translators remain scarce, giving suppliers leverage while project timing pressures enable freelancers to charge rush premiums typically 15–50%; 2024 platform sign-ups rose ~12% increasing available talent but not eliminating skill gaps.

- Scarcity: high demand for niche skills

- Rush premium: 15–50%

- Mitigation: preferred rosters, internal training, remote hiring

Data/MarTech and measurement providers

Attribution, social listening and IR tools become highly sticky once embedded, driving renewal dependence and allowing vendors to push price escalators and tiered-features that raise total cost of ownership; global MarTech spend topped $100B in 2024, amplifying supplier leverage. Privacy and API shifts (e.g., recent platform API deprecations) can force costly re-integration, while diversified vendor stacks and stronger first-party data reduce supplier bargaining power.

- Sticky integrations

- Price escalators/TCO

- Privacy/API risk

- First-party data strengthens buyers

Platform giants, top publishers and creators set ad rates; first-party data cuts supplier leverage

Platform giants (Google ad rev $224.5B 2023; Meta ad rev $116.6B 2023) and top Japanese publishers (reach vs Japan pop ~125M in 2024) exert strong rate-setting power; creators and agencies (influencer market ~$24B 2024) extract premiums. Sticky MarTech (global spend >$100B 2024) raises TCO; first-party data and multi-platform expertise reduce supplier leverage.

| Supplier | Power | Metric (2023/2024) |

|---|---|---|

| Platforms | High | Google $224.5B, Meta $116.6B |

| Publishers | High | Japan pop ~125M (2024) |

| Creators | High | Influencer market ~$24B (2024) |

| MarTech | Sticky | Spend >$100B (2024) |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Vector, highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and market entry barriers to inform strategic, investor, or academic use.

Quickly distill competitive pressure into a single, customizable Five Forces dashboard—ideal for fast strategic decisions and investor decks.

Customers Bargaining Power

Enterprise procurement rigor

Enterprise procurement rigor in 2024 sees large Japanese corporates using competitive RFPs and framework agreements to compress fees and narrow scopes, while vendor consolidation further tightens margins. Demonstrable ROI and a strong compliance track record are decisive selection criteria in these procurements. Securing multi-year framework wins offsets pricing pressure by delivering volume stability and predictable revenue streams.

Low switching costs in PR/marketing

Clients commonly rotate PR/marketing agencies by campaign or fiscal year, with WARC/ISBA 2024 reporting global client churn around 12%. Knowledge-transfer frictions exist but are routinely managed via playbooks and documentation, cutting onboarding time significantly. Performance slumps trigger rapid reallocations, keeping bargaining power high. Deep embedding in strategy and analytics, however, raises exit costs and can reduce churn by an estimated 20–30%.

In-house teams as alternatives

By 2024 many companies increasingly benchmark agency pricing against growing in-house PR and digital teams, pushing agencies to justify fees. Agencies must therefore deliver capabilities or speed—content scale, analytics, crisis IR—that in-house units cannot match. Hybrid models shifting execution to clients compress agency margins while strategic advisory and investor relations expertise preserve premium value.

Outcome-based and risk-sharing models

Clients increasingly demand KPI-linked, outcome-based fees to de-risk spend, shifting performance risk to agencies and raising revenue volatility; measurement changes and cookie deprecation in 2024 accelerated this shift. Agencies protect economics through robust measurement frameworks, disciplined test-and-learn and clear scope guardrails to prevent value leakage.

- Clients: KPI-linked fees shift risk to agencies

- Impact: higher revenue volatility

- Mitigation: strong measurement & test-and-learn

- Control: clear scope guardrails to prevent leakage

Startups and VC portfolio dynamics

Startups are price sensitive with constrained budgets yet can scale quickly, keeping buyer power high early but diminishing as customers grow; Vector’s VC arm builds pipeline and stickiness by embedding offerings in portfolio companies, reducing churn. Equity-for-services aligns incentives and boosts lifetime value while introducing concentration and valuation risk. Documented portfolio wins increase cross-sell credibility and negotiating leverage.

- VC-driven pipeline: boosts retention

- Equity-for-services: aligns incentives, raises risk

- Startups: high price sensitivity, rapid scale potential

- Case studies: improve cross-sell and reduce buyer leverage

Client leverage: 12% churn; embedding lowers 20–30%

Clients exhibit high bargaining power: global client churn ~12% in 2024 (WARC/ISBA), with KPI-linked, outcome-based fees increasing revenue volatility. Multi-year framework wins and deep strategic embedding reduce churn by 20–30% and stabilize margins. Agencies must prove ROI, compliance and unique capabilities to resist fee compression.

| Metric | 2024 | Impact |

|---|---|---|

| Client churn | 12% | High buyer leverage |

| Embedding effect | 20–30% churn ↓ | Revenue stability |

Preview Before You Purchase

Vector Porter's Five Forces Analysis

This preview shows the exact Vector Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this same file.