Vectrus SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Vectrus faces steady defense-sector demand, strong government contracting expertise, and operational scale, but it also contends with contract concentration, margin pressure, and regulatory risks. Our full SWOT unpacks these dynamics with financial context and tactical recommendations. Purchase the complete, editable Word + Excel report to strategize, present, and invest with confidence.

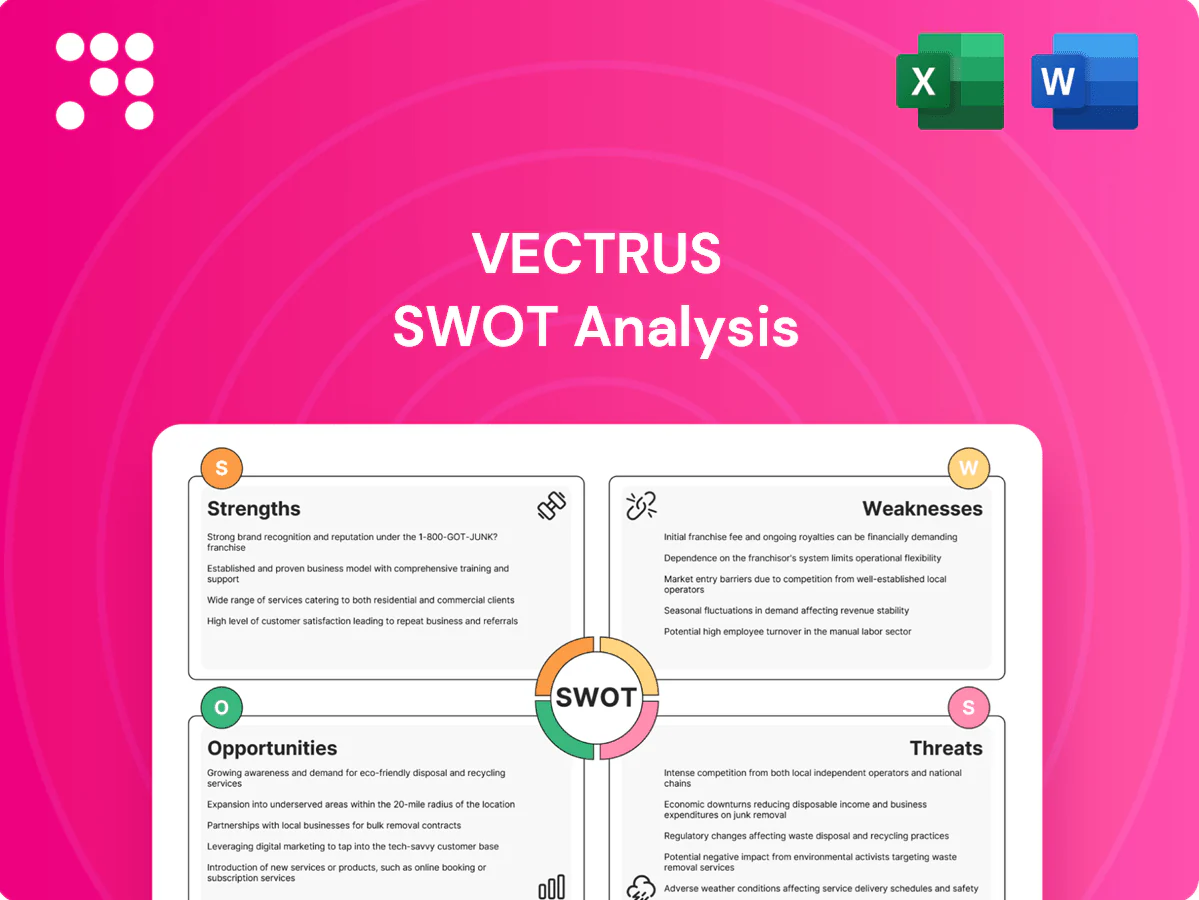

Strengths

Deep government mission expertise

Vectrus brings decades of government-facing mission expertise supporting U.S. and allied defense operations in austere, contested environments, which materially reduces execution risk and accelerates mobilization on new task orders.

Integrated ops, logistics, and IT

Vectrus combines base ops, supply chain and C5ISR/IT into turnkey offerings, enabling single-throat-to-choke accountability and lifecycle efficiencies; this integrated model supports cross-selling across adjacent lines and helped underpin fiscal 2024 revenue near $1.6B with backlog above $3B, giving customers fewer interfaces and measurably stronger performance metrics and SLA adherence.

Global footprint and rapid deployment

Vectrus operates across multiple continents with established in‑theater infrastructure and vetted vendors, enabling fast stand‑up in complex locations and continuity under difficult conditions. The company’s global scale supports surge requirements and contingency operations, while structured lessons‑learned feedback loops continuously improve reliability and readiness. This operational footprint underpins mission resilience for defense and government customers.

Strong compliance and contracting acumen

Vectrus leverages deep FAR/DFARS, export-control, and cybersecurity (CMMC/NIST-aligned) expertise to win complex federal work, reducing proposal friction and protest exposure.

Its robust business systems and cost accounting support auditability and competitive pricing, strengthening performance on IDIQs and MACs and driving recurring task orders.

- NYSE: VEC — federal services specialist

- Strength: FAR/DFARS and export-control proficiency

- Strength: CMMC/NIST-aligned cybersecurity compliance

- Strength: Audit-ready accounting enabling competitive bids

Post‑merger scale synergies (V2X)

Combining with The Vertex Company expanded Vectrus capabilities into training, aviation, and technology services, creating a more comprehensive service mix across defense and civil markets. Greater scale improves overhead absorption and enhances proposal competitiveness for larger, integrated contracts. A broader portfolio diversifies revenue by customer and mission while cross-domain integration enables higher-value solutioning.

- Expanded capabilities: training, aviation, technology

- Improved overhead absorption and win competitiveness

- Revenue diversification by customer and mission

- Cross-domain integration for higher-value solutions

Defense turnkey integrator — $1.6B revenue, >$3.0B backlog

Vectrus offers decades of government-facing mission expertise, integrated base-ops/C5ISR/supply-chain turnkey solutions, and in‑theater global infrastructure that reduce execution risk and accelerate mobilization; FAR/DFARS and CMMC/NIST proficiency plus audit-ready accounting improve win rates on IDIQs/MACs. The Vertex combination adds training, aviation and tech, diversifying revenue and boosting proposal competitiveness.

| Metric | Value | Notes |

|---|---|---|

| FY2024 Revenue | $1.6B | reported near $1.6B |

| Backlog | >$3.0B | multi-year task orders |

| Ticker | VEC | NYSE |

What is included in the product

Provides a concise SWOT overview of Vectrus by highlighting its strengths in government contracting, technical services, and global footprint; weaknesses like contract concentration and margin pressures; opportunities from rising defense and cybersecurity spending and international expansion; and threats including budget cuts, competitive pressure, and geopolitical risk.

Provides a concise, visual SWOT matrix tailored to Vectrus for rapid alignment of defense-industry strategy and contract risk management, easing stakeholder briefings and decision-making.

Weaknesses

High customer concentration

Vectrus relies on the U.S. DoD and allied governments for over 85% of revenue, concentrating sales among a few buyers and leaving the company exposed to budget shifts and recompetes. Annual revenue was roughly $1.1 billion in FY2024, so contract losses or DoD funding cuts could materially impact results. Pricing pressure across services further limits pricing power and predictability, squeezing margins during recompetes.

Low-margin, labor‑intensive model

Service contracts are often cost‑plus or fixed‑price with tight margins, leaving Vectrus exposed when costs rise; utilization and pass‑through mix drive revenue volatility. Wage inflation (BLS shows private average hourly earnings up about 4% in 2023) and supply disruptions can compress profitability. Scaling profits requires rigorous cost control, higher utilization and automation to protect thin operating margins.

Contract recompete risk

Large programs periodically rebid, creating cliff risks even with strong CPARS; Vectrus' roughly $1.2B revenue and ~$2.3B backlog mean loss of a major award could materially swing results. Transition-in/out costs and bid expenses—often running into millions per program—erode returns and compress margins. Incumbency advantages are real but not guaranteed, and protests (GAO sustain rates near 30% in recent years) can delay awards and cash flows.

Integration execution post‑merger

Post‑merger integration of V2X exposes Vectrus to operational risk as melding systems, cultures, and offerings can delay synergy capture and extend timelines for planned cost savings; distractions from integration may temporarily reduce contract delivery and win rates, while duplicative processes can depress efficiency until rationalized.

- Integration risk: systems and culture mismatch

- Synergy timing: capture may lag plans

- Distraction impact: delivery and capture rates down

- Process duplication: temporary efficiency drag

Limited proprietary IP

Vectrus remains services-heavy with limited proprietary IP, so differentiation relies on contract performance and past performance rather than defensible patents or platforms; services constitute the majority of company revenue and government contract wins. This positioning intensifies price competition on recompetes and smaller task orders where barriers to entry are moderate. Lack of IP can constrain margin expansion versus platform-led peers.

- Services-led revenue concentration

- Differentiation: performance over tech

- Higher price sensitivity on small orders

- Moderate barriers to entry for task orders

DoD‑dependent contractor — >85% revenue, FY2024 $1.1B, $2.3B backlog; margin & recompete risk

Vectrus derives >85% of revenue from U.S. DoD/allies, with FY2024 revenue ~$1.1B and backlog ~$2.3B, concentrating buyer risk. Thin margins on cost‑plus/fixed‑price contracts and 4% wage inflation (2023) squeeze profitability. Recompete/cliff risk (major program losses, GAO sustain ~30%) plus V2X integration delays threaten cash flow and synergies.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.1B |

| Backlog | $2.3B |

| DoD dependence | >85% |

| GAO sustain rate | ~30% |

Preview Before You Purchase

Vectrus SWOT Analysis

This is the actual Vectrus SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in the download. Buy now to unlock the complete, in-depth version with all strengths, weaknesses, opportunities and threats fully detailed.

Dive Deeper Into the Company’s Strategic Blueprint

Vectrus faces steady defense-sector demand, strong government contracting expertise, and operational scale, but it also contends with contract concentration, margin pressure, and regulatory risks. Our full SWOT unpacks these dynamics with financial context and tactical recommendations. Purchase the complete, editable Word + Excel report to strategize, present, and invest with confidence.

Strengths

Deep government mission expertise

Vectrus brings decades of government-facing mission expertise supporting U.S. and allied defense operations in austere, contested environments, which materially reduces execution risk and accelerates mobilization on new task orders.

Integrated ops, logistics, and IT

Vectrus combines base ops, supply chain and C5ISR/IT into turnkey offerings, enabling single-throat-to-choke accountability and lifecycle efficiencies; this integrated model supports cross-selling across adjacent lines and helped underpin fiscal 2024 revenue near $1.6B with backlog above $3B, giving customers fewer interfaces and measurably stronger performance metrics and SLA adherence.

Global footprint and rapid deployment

Vectrus operates across multiple continents with established in‑theater infrastructure and vetted vendors, enabling fast stand‑up in complex locations and continuity under difficult conditions. The company’s global scale supports surge requirements and contingency operations, while structured lessons‑learned feedback loops continuously improve reliability and readiness. This operational footprint underpins mission resilience for defense and government customers.

Strong compliance and contracting acumen

Vectrus leverages deep FAR/DFARS, export-control, and cybersecurity (CMMC/NIST-aligned) expertise to win complex federal work, reducing proposal friction and protest exposure.

Its robust business systems and cost accounting support auditability and competitive pricing, strengthening performance on IDIQs and MACs and driving recurring task orders.

- NYSE: VEC — federal services specialist

- Strength: FAR/DFARS and export-control proficiency

- Strength: CMMC/NIST-aligned cybersecurity compliance

- Strength: Audit-ready accounting enabling competitive bids

Post‑merger scale synergies (V2X)

Combining with The Vertex Company expanded Vectrus capabilities into training, aviation, and technology services, creating a more comprehensive service mix across defense and civil markets. Greater scale improves overhead absorption and enhances proposal competitiveness for larger, integrated contracts. A broader portfolio diversifies revenue by customer and mission while cross-domain integration enables higher-value solutioning.

- Expanded capabilities: training, aviation, technology

- Improved overhead absorption and win competitiveness

- Revenue diversification by customer and mission

- Cross-domain integration for higher-value solutions

Defense turnkey integrator — $1.6B revenue, >$3.0B backlog

Vectrus offers decades of government-facing mission expertise, integrated base-ops/C5ISR/supply-chain turnkey solutions, and in‑theater global infrastructure that reduce execution risk and accelerate mobilization; FAR/DFARS and CMMC/NIST proficiency plus audit-ready accounting improve win rates on IDIQs/MACs. The Vertex combination adds training, aviation and tech, diversifying revenue and boosting proposal competitiveness.

| Metric | Value | Notes |

|---|---|---|

| FY2024 Revenue | $1.6B | reported near $1.6B |

| Backlog | >$3.0B | multi-year task orders |

| Ticker | VEC | NYSE |

What is included in the product

Provides a concise SWOT overview of Vectrus by highlighting its strengths in government contracting, technical services, and global footprint; weaknesses like contract concentration and margin pressures; opportunities from rising defense and cybersecurity spending and international expansion; and threats including budget cuts, competitive pressure, and geopolitical risk.

Provides a concise, visual SWOT matrix tailored to Vectrus for rapid alignment of defense-industry strategy and contract risk management, easing stakeholder briefings and decision-making.

Weaknesses

High customer concentration

Vectrus relies on the U.S. DoD and allied governments for over 85% of revenue, concentrating sales among a few buyers and leaving the company exposed to budget shifts and recompetes. Annual revenue was roughly $1.1 billion in FY2024, so contract losses or DoD funding cuts could materially impact results. Pricing pressure across services further limits pricing power and predictability, squeezing margins during recompetes.

Low-margin, labor‑intensive model

Service contracts are often cost‑plus or fixed‑price with tight margins, leaving Vectrus exposed when costs rise; utilization and pass‑through mix drive revenue volatility. Wage inflation (BLS shows private average hourly earnings up about 4% in 2023) and supply disruptions can compress profitability. Scaling profits requires rigorous cost control, higher utilization and automation to protect thin operating margins.

Contract recompete risk

Large programs periodically rebid, creating cliff risks even with strong CPARS; Vectrus' roughly $1.2B revenue and ~$2.3B backlog mean loss of a major award could materially swing results. Transition-in/out costs and bid expenses—often running into millions per program—erode returns and compress margins. Incumbency advantages are real but not guaranteed, and protests (GAO sustain rates near 30% in recent years) can delay awards and cash flows.

Integration execution post‑merger

Post‑merger integration of V2X exposes Vectrus to operational risk as melding systems, cultures, and offerings can delay synergy capture and extend timelines for planned cost savings; distractions from integration may temporarily reduce contract delivery and win rates, while duplicative processes can depress efficiency until rationalized.

- Integration risk: systems and culture mismatch

- Synergy timing: capture may lag plans

- Distraction impact: delivery and capture rates down

- Process duplication: temporary efficiency drag

Limited proprietary IP

Vectrus remains services-heavy with limited proprietary IP, so differentiation relies on contract performance and past performance rather than defensible patents or platforms; services constitute the majority of company revenue and government contract wins. This positioning intensifies price competition on recompetes and smaller task orders where barriers to entry are moderate. Lack of IP can constrain margin expansion versus platform-led peers.

- Services-led revenue concentration

- Differentiation: performance over tech

- Higher price sensitivity on small orders

- Moderate barriers to entry for task orders

DoD‑dependent contractor — >85% revenue, FY2024 $1.1B, $2.3B backlog; margin & recompete risk

Vectrus derives >85% of revenue from U.S. DoD/allies, with FY2024 revenue ~$1.1B and backlog ~$2.3B, concentrating buyer risk. Thin margins on cost‑plus/fixed‑price contracts and 4% wage inflation (2023) squeeze profitability. Recompete/cliff risk (major program losses, GAO sustain ~30%) plus V2X integration delays threaten cash flow and synergies.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.1B |

| Backlog | $2.3B |

| DoD dependence | >85% |

| GAO sustain rate | ~30% |

Preview Before You Purchase

Vectrus SWOT Analysis

This is the actual Vectrus SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in the download. Buy now to unlock the complete, in-depth version with all strengths, weaknesses, opportunities and threats fully detailed.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Vectrus faces steady defense-sector demand, strong government contracting expertise, and operational scale, but it also contends with contract concentration, margin pressure, and regulatory risks. Our full SWOT unpacks these dynamics with financial context and tactical recommendations. Purchase the complete, editable Word + Excel report to strategize, present, and invest with confidence.

Strengths

Deep government mission expertise

Vectrus brings decades of government-facing mission expertise supporting U.S. and allied defense operations in austere, contested environments, which materially reduces execution risk and accelerates mobilization on new task orders.

Integrated ops, logistics, and IT

Vectrus combines base ops, supply chain and C5ISR/IT into turnkey offerings, enabling single-throat-to-choke accountability and lifecycle efficiencies; this integrated model supports cross-selling across adjacent lines and helped underpin fiscal 2024 revenue near $1.6B with backlog above $3B, giving customers fewer interfaces and measurably stronger performance metrics and SLA adherence.

Global footprint and rapid deployment

Vectrus operates across multiple continents with established in‑theater infrastructure and vetted vendors, enabling fast stand‑up in complex locations and continuity under difficult conditions. The company’s global scale supports surge requirements and contingency operations, while structured lessons‑learned feedback loops continuously improve reliability and readiness. This operational footprint underpins mission resilience for defense and government customers.

Strong compliance and contracting acumen

Vectrus leverages deep FAR/DFARS, export-control, and cybersecurity (CMMC/NIST-aligned) expertise to win complex federal work, reducing proposal friction and protest exposure.

Its robust business systems and cost accounting support auditability and competitive pricing, strengthening performance on IDIQs and MACs and driving recurring task orders.

- NYSE: VEC — federal services specialist

- Strength: FAR/DFARS and export-control proficiency

- Strength: CMMC/NIST-aligned cybersecurity compliance

- Strength: Audit-ready accounting enabling competitive bids

Post‑merger scale synergies (V2X)

Combining with The Vertex Company expanded Vectrus capabilities into training, aviation, and technology services, creating a more comprehensive service mix across defense and civil markets. Greater scale improves overhead absorption and enhances proposal competitiveness for larger, integrated contracts. A broader portfolio diversifies revenue by customer and mission while cross-domain integration enables higher-value solutioning.

- Expanded capabilities: training, aviation, technology

- Improved overhead absorption and win competitiveness

- Revenue diversification by customer and mission

- Cross-domain integration for higher-value solutions

Defense turnkey integrator — $1.6B revenue, >$3.0B backlog

Vectrus offers decades of government-facing mission expertise, integrated base-ops/C5ISR/supply-chain turnkey solutions, and in‑theater global infrastructure that reduce execution risk and accelerate mobilization; FAR/DFARS and CMMC/NIST proficiency plus audit-ready accounting improve win rates on IDIQs/MACs. The Vertex combination adds training, aviation and tech, diversifying revenue and boosting proposal competitiveness.

| Metric | Value | Notes |

|---|---|---|

| FY2024 Revenue | $1.6B | reported near $1.6B |

| Backlog | >$3.0B | multi-year task orders |

| Ticker | VEC | NYSE |

What is included in the product

Provides a concise SWOT overview of Vectrus by highlighting its strengths in government contracting, technical services, and global footprint; weaknesses like contract concentration and margin pressures; opportunities from rising defense and cybersecurity spending and international expansion; and threats including budget cuts, competitive pressure, and geopolitical risk.

Provides a concise, visual SWOT matrix tailored to Vectrus for rapid alignment of defense-industry strategy and contract risk management, easing stakeholder briefings and decision-making.

Weaknesses

High customer concentration

Vectrus relies on the U.S. DoD and allied governments for over 85% of revenue, concentrating sales among a few buyers and leaving the company exposed to budget shifts and recompetes. Annual revenue was roughly $1.1 billion in FY2024, so contract losses or DoD funding cuts could materially impact results. Pricing pressure across services further limits pricing power and predictability, squeezing margins during recompetes.

Low-margin, labor‑intensive model

Service contracts are often cost‑plus or fixed‑price with tight margins, leaving Vectrus exposed when costs rise; utilization and pass‑through mix drive revenue volatility. Wage inflation (BLS shows private average hourly earnings up about 4% in 2023) and supply disruptions can compress profitability. Scaling profits requires rigorous cost control, higher utilization and automation to protect thin operating margins.

Contract recompete risk

Large programs periodically rebid, creating cliff risks even with strong CPARS; Vectrus' roughly $1.2B revenue and ~$2.3B backlog mean loss of a major award could materially swing results. Transition-in/out costs and bid expenses—often running into millions per program—erode returns and compress margins. Incumbency advantages are real but not guaranteed, and protests (GAO sustain rates near 30% in recent years) can delay awards and cash flows.

Integration execution post‑merger

Post‑merger integration of V2X exposes Vectrus to operational risk as melding systems, cultures, and offerings can delay synergy capture and extend timelines for planned cost savings; distractions from integration may temporarily reduce contract delivery and win rates, while duplicative processes can depress efficiency until rationalized.

- Integration risk: systems and culture mismatch

- Synergy timing: capture may lag plans

- Distraction impact: delivery and capture rates down

- Process duplication: temporary efficiency drag

Limited proprietary IP

Vectrus remains services-heavy with limited proprietary IP, so differentiation relies on contract performance and past performance rather than defensible patents or platforms; services constitute the majority of company revenue and government contract wins. This positioning intensifies price competition on recompetes and smaller task orders where barriers to entry are moderate. Lack of IP can constrain margin expansion versus platform-led peers.

- Services-led revenue concentration

- Differentiation: performance over tech

- Higher price sensitivity on small orders

- Moderate barriers to entry for task orders

DoD‑dependent contractor — >85% revenue, FY2024 $1.1B, $2.3B backlog; margin & recompete risk

Vectrus derives >85% of revenue from U.S. DoD/allies, with FY2024 revenue ~$1.1B and backlog ~$2.3B, concentrating buyer risk. Thin margins on cost‑plus/fixed‑price contracts and 4% wage inflation (2023) squeeze profitability. Recompete/cliff risk (major program losses, GAO sustain ~30%) plus V2X integration delays threaten cash flow and synergies.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.1B |

| Backlog | $2.3B |

| DoD dependence | >85% |

| GAO sustain rate | ~30% |

Preview Before You Purchase

Vectrus SWOT Analysis

This is the actual Vectrus SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in the download. Buy now to unlock the complete, in-depth version with all strengths, weaknesses, opportunities and threats fully detailed.