Ventia Services Porter's Five Forces Analysis

Don't Miss the Bigger Picture

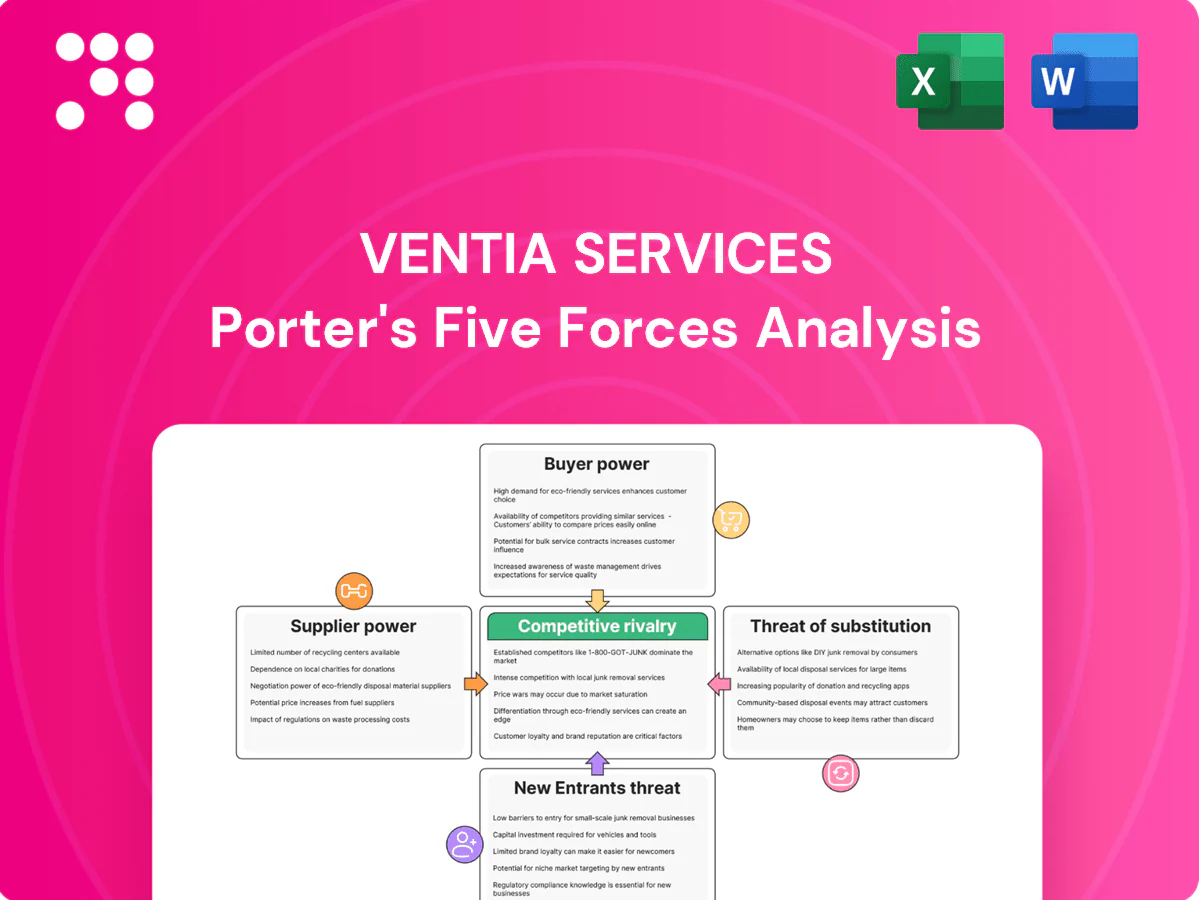

Ventia Services faces a complex competitive landscape where buyer and supplier power, rivalry intensity, and entry barriers shape margins and growth prospects. Our snapshot highlights key pressure points—contracting dynamics, service commoditization, and regulatory influence—that could alter strategy and valuation. Want granular force-by-force ratings, visuals, and tactical implications? Unlock the full Porter's Five Forces Analysis to inform smarter investment and strategic choices.

Suppliers Bargaining Power

Skilled labour dependence

Highly skilled, often unionised technicians and engineers are critical to Ventia’s transport, utilities, defence and telco operations; in 2024 Ventia’s workforce was roughly 16,000, concentrating skill gaps in regional Australia and remote sites. Scarcity of security‑cleared roles and regional specialists lifts wage pressure and reduces rostering flexibility, with union density around 14% in 2024 increasing bargaining leverage. Enterprise bargaining agreements and strict safety compliance add rigidity to shift patterns and fixed cost bases, and supplier power spikes during peak project cycles or remote deployments.

OEM equipment and spares

OEMs for specialised fleet, plant, SCADA and network equipment control proprietary parts, software and maintenance protocols, creating vendor lock‑in that raises switching costs and allows premium service fees. Global supply‑chain disruptions through 2024 lengthened lead times for critical spares and pushed spot prices higher. Long‑term framework agreements provide partial hedges on pricing and availability risk by securing priority allocations and fixed pricing terms.

Materials and utilities inputs

Materials and utilities inputs — bitumen, steel, aggregates, chemicals and energy — represent roughly 30–40% of direct costs for maintenance and project work at Ventia. Commodity volatility (Brent ~US$80/bbl average in 2024) and logistics constraints can compress margins on fixed‑price contracts, with swings of up to ±10–15% on key inputs reported across the sector. Indexation clauses and hedging mitigate risk but are not universal. Preferred supplier panels boost supply reliability while narrowing short‑term negotiating leverage.

Specialist subcontractors

Ventia relies on niche subcontractors for trades, inspection and regional coverage; in 2024 tight labour markets saw high-utilisation subs command premium rates and selective allocation. Performance and safety records limit substitution on critical assets, while deep relationships and multi-year volume pipelines can gradually temper supplier pricing power.

- 2024: niche subs critical

- Premium rates in tight markets

- Safety/performance constrain substitution

- Long-term volume reduces price pressure

Technology and data providers

IoT sensors, digital twins, GIS and field-service platforms are core to Ventia’s productivity and 99.9% SLA expectations; about 14.4 billion connected IoT devices existed in 2024, increasing dependency on vendor stacks. Licensing, integration and data-portability clauses create lock-in; cyber, uptime and sector compliance narrow viable suppliers. Co-development and open standards lower lock-in but need upfront CAPEX and integration effort.

- IoT scale: 14.4B devices (2024)

- SLA pressure: 99.9% uptime

- Risk: licensing + data portability = vendor dependency

- Mitigation: co-dev/open standards require upfront investment

Supplier power rises: skilled‑labour squeeze, IoT lock‑in and commodity swings

Suppliers hold moderate‑high power: skilled labour scarcity (Ventia ~16,000 staff in 2024; union density ~14%) and niche subs push wage and rate premiums. OEM lock‑in and IoT dependency (14.4B devices in 2024) raise switching costs; materials volatility (Brent ~US$80/bbl avg 2024) can swing input costs ±10–15%. Long‑term panels and framework contracts partially mitigate risk.

| Metric | 2024 | Impact |

|---|---|---|

| Workforce | 16,000 | labour premiums |

| Union density | ~14% | bargaining leverage |

| IoT devices | 14.4B | vendor lock‑in |

| Brent | ~US$80/bbl | input volatility ±10–15% |

What is included in the product

Provides a concise Porter's Five Forces assessment tailored to Ventia Services, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and regulatory or technological disruptors that shape its pricing power and profitability.

Concise one-sheet Porter's Five Forces for Ventia Services—instantly highlights procurement and subcontractor pressures, regulatory and bidding intensity, and gives clear strategic levers to reduce supplier dependency, strengthen contract wins, and mitigate regulatory risk.

Customers Bargaining Power

Government and utility buyers

Clients are concentrated public agencies, defence, councils and regulated utilities with professional procurement teams; public procurement accounts for about 12% of GDP on average (OECD). Scale and budget authority give buyers strong negotiating leverage and enforce rigorous KPI/SLA frameworks. Payment terms are often buyer‑favourable (commonly 30 days) and shift risk to suppliers. Political and regulatory oversight increases price visibility and benchmarking pressure.

Tender intensity and panels

Work is awarded via competitive tenders and standing panels that commonly involve 3–6 qualified bidders, with panel terms typically lasting 2–4 years; standardised scopes and transparent criteria heighten price competition. Buyers routinely rebid or retender at renewal (often every 2–4 years) to reset pricing and secure savings. Incumbency offers advantage but is contingent on meeting KPIs and performance metrics, which increasingly determine retention.

Long-term O&M contracts

Multi‑year O&M contracts deliver volume certainty but embed abatements, penalties and gainshare clauses that shift risk to suppliers and tighten margins. In 2024 buyers leaned on real‑time performance dashboards to demand continuous improvement and trigger financial adjustments. Price reopeners and indexation clauses limit suppliers' exposure to cost shocks while capping upside. Renewal options create leverage at contract breakpoints, compressing renegotiation outcomes.

Ability to unbundle or bundle

Buyers in 2024 increasingly disaggregate services to extract lower prices or bundle for scale efficiencies, putting margin pressure on commoditised tasks; vendors must quantify integration synergies to justify premiums. Demonstrable niche capability and a strong safety culture help sustain price resilience and contract retention.

- Unbundle to lower cost

- Bundle for scale

- Integration synergies defend margin

- Niche skills and safety sustain pricing

Switching and reputational risk

Switching costs for Ventia are moderate given asset criticality and mobilisation needs, but manifested failures can prompt clients to switch despite transition expenses. Strong safety, compliance and delivery records measurably lower buyer propensity to disengage. In government markets referenceability materially affects win rates and contract retention.

- Moderate switching costs: mobilisation & asset criticality

- Poor performance speeds defections despite costs

- Safety/compliance reduce switching propensity

- Referenceability drives government win rates

Public buyers and utilities exert procurement leverage; tenders and dashboards tighten margins

Public buyers (≈12% of GDP OECD) and large utilities exert strong leverage via professional procurement, 30‑day payment norms and KPI/SLA enforcement. Competitive tenders (typically 3–6 bidders) and 2–4 year panels reset pricing at renewals; 2024 saw wider use of real‑time dashboards and price reopeners that compress supplier margins. Strong safety/compliance and niche capabilities mitigate switching risk.

| Metric | Value (2024) |

|---|---|

| Public procurement share | ≈12% GDP (OECD) |

| Typical bidders | 3–6 |

| Panel length | 2–4 years |

| Payment terms | ~30 days |

Full Version Awaits

Ventia Services Porter's Five Forces Analysis

This preview shows the exact Ventia Services Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, comprehensive, and ready for download and use the moment you buy. You're getting the final deliverable instantly.

Don't Miss the Bigger Picture

Ventia Services faces a complex competitive landscape where buyer and supplier power, rivalry intensity, and entry barriers shape margins and growth prospects. Our snapshot highlights key pressure points—contracting dynamics, service commoditization, and regulatory influence—that could alter strategy and valuation. Want granular force-by-force ratings, visuals, and tactical implications? Unlock the full Porter's Five Forces Analysis to inform smarter investment and strategic choices.

Suppliers Bargaining Power

Skilled labour dependence

Highly skilled, often unionised technicians and engineers are critical to Ventia’s transport, utilities, defence and telco operations; in 2024 Ventia’s workforce was roughly 16,000, concentrating skill gaps in regional Australia and remote sites. Scarcity of security‑cleared roles and regional specialists lifts wage pressure and reduces rostering flexibility, with union density around 14% in 2024 increasing bargaining leverage. Enterprise bargaining agreements and strict safety compliance add rigidity to shift patterns and fixed cost bases, and supplier power spikes during peak project cycles or remote deployments.

OEM equipment and spares

OEMs for specialised fleet, plant, SCADA and network equipment control proprietary parts, software and maintenance protocols, creating vendor lock‑in that raises switching costs and allows premium service fees. Global supply‑chain disruptions through 2024 lengthened lead times for critical spares and pushed spot prices higher. Long‑term framework agreements provide partial hedges on pricing and availability risk by securing priority allocations and fixed pricing terms.

Materials and utilities inputs

Materials and utilities inputs — bitumen, steel, aggregates, chemicals and energy — represent roughly 30–40% of direct costs for maintenance and project work at Ventia. Commodity volatility (Brent ~US$80/bbl average in 2024) and logistics constraints can compress margins on fixed‑price contracts, with swings of up to ±10–15% on key inputs reported across the sector. Indexation clauses and hedging mitigate risk but are not universal. Preferred supplier panels boost supply reliability while narrowing short‑term negotiating leverage.

Specialist subcontractors

Ventia relies on niche subcontractors for trades, inspection and regional coverage; in 2024 tight labour markets saw high-utilisation subs command premium rates and selective allocation. Performance and safety records limit substitution on critical assets, while deep relationships and multi-year volume pipelines can gradually temper supplier pricing power.

- 2024: niche subs critical

- Premium rates in tight markets

- Safety/performance constrain substitution

- Long-term volume reduces price pressure

Technology and data providers

IoT sensors, digital twins, GIS and field-service platforms are core to Ventia’s productivity and 99.9% SLA expectations; about 14.4 billion connected IoT devices existed in 2024, increasing dependency on vendor stacks. Licensing, integration and data-portability clauses create lock-in; cyber, uptime and sector compliance narrow viable suppliers. Co-development and open standards lower lock-in but need upfront CAPEX and integration effort.

- IoT scale: 14.4B devices (2024)

- SLA pressure: 99.9% uptime

- Risk: licensing + data portability = vendor dependency

- Mitigation: co-dev/open standards require upfront investment

Supplier power rises: skilled‑labour squeeze, IoT lock‑in and commodity swings

Suppliers hold moderate‑high power: skilled labour scarcity (Ventia ~16,000 staff in 2024; union density ~14%) and niche subs push wage and rate premiums. OEM lock‑in and IoT dependency (14.4B devices in 2024) raise switching costs; materials volatility (Brent ~US$80/bbl avg 2024) can swing input costs ±10–15%. Long‑term panels and framework contracts partially mitigate risk.

| Metric | 2024 | Impact |

|---|---|---|

| Workforce | 16,000 | labour premiums |

| Union density | ~14% | bargaining leverage |

| IoT devices | 14.4B | vendor lock‑in |

| Brent | ~US$80/bbl | input volatility ±10–15% |

What is included in the product

Provides a concise Porter's Five Forces assessment tailored to Ventia Services, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and regulatory or technological disruptors that shape its pricing power and profitability.

Concise one-sheet Porter's Five Forces for Ventia Services—instantly highlights procurement and subcontractor pressures, regulatory and bidding intensity, and gives clear strategic levers to reduce supplier dependency, strengthen contract wins, and mitigate regulatory risk.

Customers Bargaining Power

Government and utility buyers

Clients are concentrated public agencies, defence, councils and regulated utilities with professional procurement teams; public procurement accounts for about 12% of GDP on average (OECD). Scale and budget authority give buyers strong negotiating leverage and enforce rigorous KPI/SLA frameworks. Payment terms are often buyer‑favourable (commonly 30 days) and shift risk to suppliers. Political and regulatory oversight increases price visibility and benchmarking pressure.

Tender intensity and panels

Work is awarded via competitive tenders and standing panels that commonly involve 3–6 qualified bidders, with panel terms typically lasting 2–4 years; standardised scopes and transparent criteria heighten price competition. Buyers routinely rebid or retender at renewal (often every 2–4 years) to reset pricing and secure savings. Incumbency offers advantage but is contingent on meeting KPIs and performance metrics, which increasingly determine retention.

Long-term O&M contracts

Multi‑year O&M contracts deliver volume certainty but embed abatements, penalties and gainshare clauses that shift risk to suppliers and tighten margins. In 2024 buyers leaned on real‑time performance dashboards to demand continuous improvement and trigger financial adjustments. Price reopeners and indexation clauses limit suppliers' exposure to cost shocks while capping upside. Renewal options create leverage at contract breakpoints, compressing renegotiation outcomes.

Ability to unbundle or bundle

Buyers in 2024 increasingly disaggregate services to extract lower prices or bundle for scale efficiencies, putting margin pressure on commoditised tasks; vendors must quantify integration synergies to justify premiums. Demonstrable niche capability and a strong safety culture help sustain price resilience and contract retention.

- Unbundle to lower cost

- Bundle for scale

- Integration synergies defend margin

- Niche skills and safety sustain pricing

Switching and reputational risk

Switching costs for Ventia are moderate given asset criticality and mobilisation needs, but manifested failures can prompt clients to switch despite transition expenses. Strong safety, compliance and delivery records measurably lower buyer propensity to disengage. In government markets referenceability materially affects win rates and contract retention.

- Moderate switching costs: mobilisation & asset criticality

- Poor performance speeds defections despite costs

- Safety/compliance reduce switching propensity

- Referenceability drives government win rates

Public buyers and utilities exert procurement leverage; tenders and dashboards tighten margins

Public buyers (≈12% of GDP OECD) and large utilities exert strong leverage via professional procurement, 30‑day payment norms and KPI/SLA enforcement. Competitive tenders (typically 3–6 bidders) and 2–4 year panels reset pricing at renewals; 2024 saw wider use of real‑time dashboards and price reopeners that compress supplier margins. Strong safety/compliance and niche capabilities mitigate switching risk.

| Metric | Value (2024) |

|---|---|

| Public procurement share | ≈12% GDP (OECD) |

| Typical bidders | 3–6 |

| Panel length | 2–4 years |

| Payment terms | ~30 days |

Full Version Awaits

Ventia Services Porter's Five Forces Analysis

This preview shows the exact Ventia Services Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, comprehensive, and ready for download and use the moment you buy. You're getting the final deliverable instantly.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ventia Services faces a complex competitive landscape where buyer and supplier power, rivalry intensity, and entry barriers shape margins and growth prospects. Our snapshot highlights key pressure points—contracting dynamics, service commoditization, and regulatory influence—that could alter strategy and valuation. Want granular force-by-force ratings, visuals, and tactical implications? Unlock the full Porter's Five Forces Analysis to inform smarter investment and strategic choices.

Suppliers Bargaining Power

Skilled labour dependence

Highly skilled, often unionised technicians and engineers are critical to Ventia’s transport, utilities, defence and telco operations; in 2024 Ventia’s workforce was roughly 16,000, concentrating skill gaps in regional Australia and remote sites. Scarcity of security‑cleared roles and regional specialists lifts wage pressure and reduces rostering flexibility, with union density around 14% in 2024 increasing bargaining leverage. Enterprise bargaining agreements and strict safety compliance add rigidity to shift patterns and fixed cost bases, and supplier power spikes during peak project cycles or remote deployments.

OEM equipment and spares

OEMs for specialised fleet, plant, SCADA and network equipment control proprietary parts, software and maintenance protocols, creating vendor lock‑in that raises switching costs and allows premium service fees. Global supply‑chain disruptions through 2024 lengthened lead times for critical spares and pushed spot prices higher. Long‑term framework agreements provide partial hedges on pricing and availability risk by securing priority allocations and fixed pricing terms.

Materials and utilities inputs

Materials and utilities inputs — bitumen, steel, aggregates, chemicals and energy — represent roughly 30–40% of direct costs for maintenance and project work at Ventia. Commodity volatility (Brent ~US$80/bbl average in 2024) and logistics constraints can compress margins on fixed‑price contracts, with swings of up to ±10–15% on key inputs reported across the sector. Indexation clauses and hedging mitigate risk but are not universal. Preferred supplier panels boost supply reliability while narrowing short‑term negotiating leverage.

Specialist subcontractors

Ventia relies on niche subcontractors for trades, inspection and regional coverage; in 2024 tight labour markets saw high-utilisation subs command premium rates and selective allocation. Performance and safety records limit substitution on critical assets, while deep relationships and multi-year volume pipelines can gradually temper supplier pricing power.

- 2024: niche subs critical

- Premium rates in tight markets

- Safety/performance constrain substitution

- Long-term volume reduces price pressure

Technology and data providers

IoT sensors, digital twins, GIS and field-service platforms are core to Ventia’s productivity and 99.9% SLA expectations; about 14.4 billion connected IoT devices existed in 2024, increasing dependency on vendor stacks. Licensing, integration and data-portability clauses create lock-in; cyber, uptime and sector compliance narrow viable suppliers. Co-development and open standards lower lock-in but need upfront CAPEX and integration effort.

- IoT scale: 14.4B devices (2024)

- SLA pressure: 99.9% uptime

- Risk: licensing + data portability = vendor dependency

- Mitigation: co-dev/open standards require upfront investment

Supplier power rises: skilled‑labour squeeze, IoT lock‑in and commodity swings

Suppliers hold moderate‑high power: skilled labour scarcity (Ventia ~16,000 staff in 2024; union density ~14%) and niche subs push wage and rate premiums. OEM lock‑in and IoT dependency (14.4B devices in 2024) raise switching costs; materials volatility (Brent ~US$80/bbl avg 2024) can swing input costs ±10–15%. Long‑term panels and framework contracts partially mitigate risk.

| Metric | 2024 | Impact |

|---|---|---|

| Workforce | 16,000 | labour premiums |

| Union density | ~14% | bargaining leverage |

| IoT devices | 14.4B | vendor lock‑in |

| Brent | ~US$80/bbl | input volatility ±10–15% |

What is included in the product

Provides a concise Porter's Five Forces assessment tailored to Ventia Services, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and regulatory or technological disruptors that shape its pricing power and profitability.

Concise one-sheet Porter's Five Forces for Ventia Services—instantly highlights procurement and subcontractor pressures, regulatory and bidding intensity, and gives clear strategic levers to reduce supplier dependency, strengthen contract wins, and mitigate regulatory risk.

Customers Bargaining Power

Government and utility buyers

Clients are concentrated public agencies, defence, councils and regulated utilities with professional procurement teams; public procurement accounts for about 12% of GDP on average (OECD). Scale and budget authority give buyers strong negotiating leverage and enforce rigorous KPI/SLA frameworks. Payment terms are often buyer‑favourable (commonly 30 days) and shift risk to suppliers. Political and regulatory oversight increases price visibility and benchmarking pressure.

Tender intensity and panels

Work is awarded via competitive tenders and standing panels that commonly involve 3–6 qualified bidders, with panel terms typically lasting 2–4 years; standardised scopes and transparent criteria heighten price competition. Buyers routinely rebid or retender at renewal (often every 2–4 years) to reset pricing and secure savings. Incumbency offers advantage but is contingent on meeting KPIs and performance metrics, which increasingly determine retention.

Long-term O&M contracts

Multi‑year O&M contracts deliver volume certainty but embed abatements, penalties and gainshare clauses that shift risk to suppliers and tighten margins. In 2024 buyers leaned on real‑time performance dashboards to demand continuous improvement and trigger financial adjustments. Price reopeners and indexation clauses limit suppliers' exposure to cost shocks while capping upside. Renewal options create leverage at contract breakpoints, compressing renegotiation outcomes.

Ability to unbundle or bundle

Buyers in 2024 increasingly disaggregate services to extract lower prices or bundle for scale efficiencies, putting margin pressure on commoditised tasks; vendors must quantify integration synergies to justify premiums. Demonstrable niche capability and a strong safety culture help sustain price resilience and contract retention.

- Unbundle to lower cost

- Bundle for scale

- Integration synergies defend margin

- Niche skills and safety sustain pricing

Switching and reputational risk

Switching costs for Ventia are moderate given asset criticality and mobilisation needs, but manifested failures can prompt clients to switch despite transition expenses. Strong safety, compliance and delivery records measurably lower buyer propensity to disengage. In government markets referenceability materially affects win rates and contract retention.

- Moderate switching costs: mobilisation & asset criticality

- Poor performance speeds defections despite costs

- Safety/compliance reduce switching propensity

- Referenceability drives government win rates

Public buyers and utilities exert procurement leverage; tenders and dashboards tighten margins

Public buyers (≈12% of GDP OECD) and large utilities exert strong leverage via professional procurement, 30‑day payment norms and KPI/SLA enforcement. Competitive tenders (typically 3–6 bidders) and 2–4 year panels reset pricing at renewals; 2024 saw wider use of real‑time dashboards and price reopeners that compress supplier margins. Strong safety/compliance and niche capabilities mitigate switching risk.

| Metric | Value (2024) |

|---|---|

| Public procurement share | ≈12% GDP (OECD) |

| Typical bidders | 3–6 |

| Panel length | 2–4 years |

| Payment terms | ~30 days |

Full Version Awaits

Ventia Services Porter's Five Forces Analysis

This preview shows the exact Ventia Services Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, comprehensive, and ready for download and use the moment you buy. You're getting the final deliverable instantly.