Veracyte Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

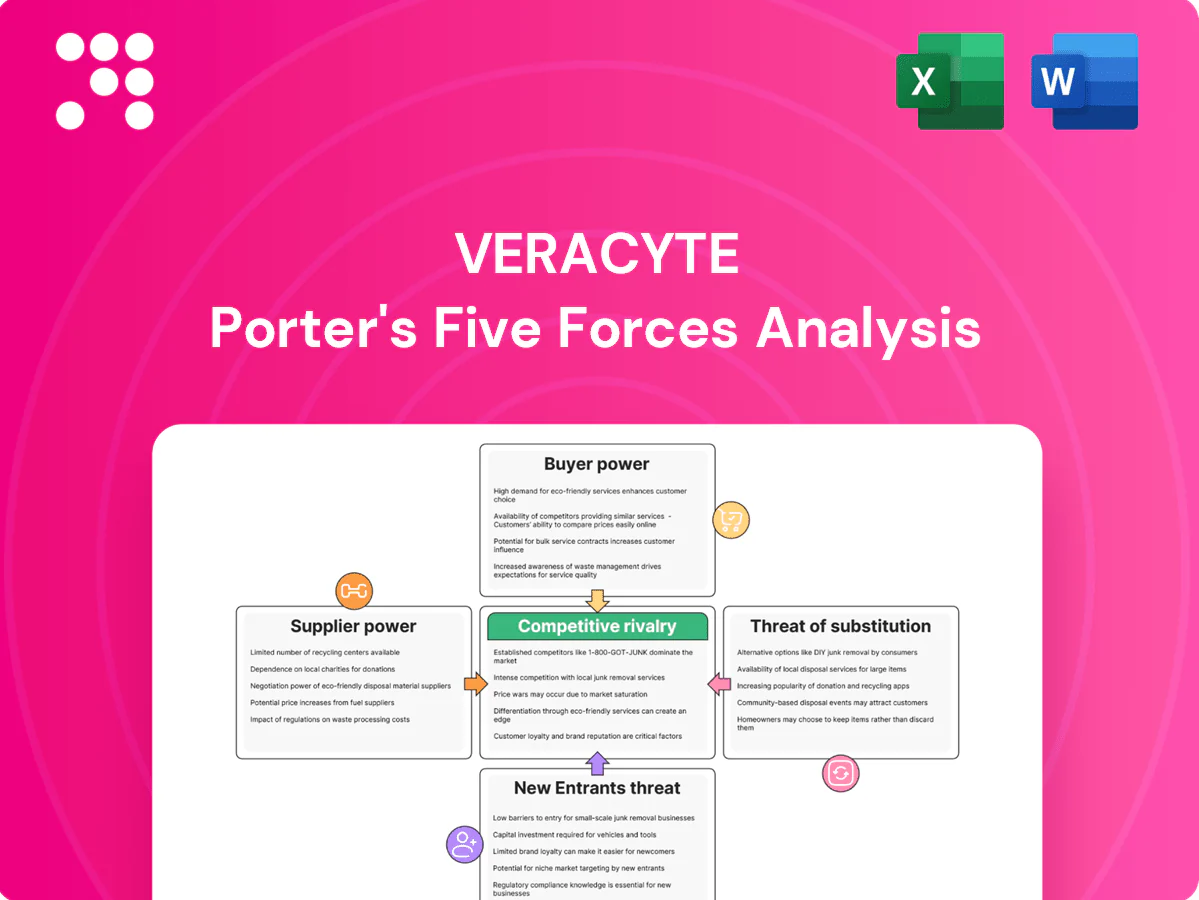

Veracyte faces moderate buyer power, specialized supplier leverage, significant regulatory and reimbursement barriers deterring new entrants, and escalating substitute diagnostics—while rivalry among genomics peers intensifies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Veracyte’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated sequencing platforms

Veracyte depends on a concentrated set of NGS platform providers—Illumina (~65% installed base in 2024) and Thermo Fisher (~25% in 2024)—creating supplier concentration risk. Platform lock-in and regulatory/clinical validation requirements raise switching costs and extend revalidation timelines. Vendors can thus influence reagent pricing, service levels, and roadmap priorities. Designing multi-platform assays mitigates dependency but incurs materially higher development and validation costs.

Specialized reagents and consumables

Proprietary kits, enzymes, and probes for Veracyte diagnostics are often single-sourced, creating concentrated supplier power. Batch consistency, quality and lead times directly affect test performance and turnaround time. Long-term supply agreements mitigate risk but commonly contain minimum purchase obligations and price escalators. Any supplier disruption can quickly curtail lab throughput and compress margins.

Clinical samples and biobank access

High-quality annotated specimens are essential for Veracyte’s test validation and iteration, yet access is concentrated in 3,000+ academic biobanks that wield bargaining leverage; data-use agreements and IRB constraints typically add 3–9 month delays to access and increase operational costs. Strategic collaborations and material-transfer agreements secure supply lines but often require revenue-sharing or milestone payments, compressing margins and tying sample availability to partner priorities.

Cloud, bioinformatics, and data infrastructure

Computational pipelines rely on dominant cloud vendors (AWS ~32%, Azure ~23%, Google Cloud ~11% in 2024) and licensed genomic databases; switching clouds is feasible but revalidation and security work add meaningful one-time and ongoing costs. Sudden storage/compute price hikes can compress gross margins; preferred-pricing and multi-year contracts help dampen volatility.

- Dependence: high on top 3 clouds

- Switch cost: revalidation/security overhead

- Risk: price hikes → margin pressure

- Mitigation: preferred pricing, multi-year deals

IP licensing and patented biomarkers

IP licensing for signatures and patented biomarkers forces Veracyte to pay royalties and accept field-of-use limits, raising COGS and constraining clinical and geographic expansion; litigation over patents further strengthens supplier leverage. Building Veracyte-owned IP and filing defensive patents reduces dependency and lowers long-term margin pressure.

Platform concentration and cloud dependence raise revalidation costs and margin pressure

Supplier power is high: Illumina (~65% installed base in 2024) and Thermo Fisher (~25%) create platform concentration; proprietary reagents, IP royalties and 3,000+ biobanks (3–9 month access delays) further strengthen suppliers. Cloud dependence (AWS ~32%, Azure ~23%, Google ~11% in 2024) and single-source kits raise switching/revalidation costs and margin risk.

| Item | 2024 Metric |

|---|---|

| Illumina share | ~65% |

| Thermo Fisher share | ~25% |

| AWS | ~32% |

| Azure | ~23% |

| Google Cloud | ~11% |

| Biobanks | 3,000+ (3–9 mo delays) |

| Impact | Higher COGS, revalidation costs, margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Veracyte that uncovers key drivers of competition, buyer and supplier power, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Detailed, strategic commentary highlights dynamics that deter new entrants, influence pricing and profitability, and support investor or internal strategy use.

Clear one-sheet Porter's Five Forces for Veracyte—reduces analysis time and highlights competitive pressures at a glance, customizable with new data and ready to drop into pitch decks or executive reports.

Customers Bargaining Power

Payers drive reimbursement and coverage

Private insurers and CMS set coverage and rates, controlling reimbursement for over 50% of US health spend (~$4.5T in 2023), concentrating buyer power. Strict evidence thresholds and utilization management make demand highly elastic for Veracyte tests. Repricing cycles and prior authorization commonly delay collections by 4–12 weeks. Strong health-economic data and guideline inclusion can secure high-single to low-double-digit uplift in negotiated reimbursement.

Health systems and IDNs consolidate volume

Large health systems, GPOs and reference labs now aggregate most testing volume and can demand discounts, EMR integration and strict SLAs; Veracyte reported full‑year 2024 revenue of $373.8 million, so major contract wins or losses materially shift share and quarterly results. Embedded workflows and EMR integration raise switching costs for buyers, favoring Veracyte when contracts lock in referrals and operational pathways.

Specialist physicians as gatekeepers

Pulmonologists, endocrinologists and pathologists act as gatekeepers for Veracyte tests, prioritizing turnaround time, ease of use and demonstrated clinical validity when deciding adoption. In 2024 KOL endorsements and peer‑reviewed outcomes continued to lower perceived risk and accelerate referrals. When comparable in‑house alternatives exist, clinicians exhibit higher price sensitivity, reducing Veracyte's negotiating leverage.

Patients and advocacy groups

Patients have limited direct bargaining power but can sway payer policy through organized advocacy; groups focused on lung disease and ILD have helped accelerate coverage for diagnostic genomic tools. Out-of-pocket exposure suppresses uptake in marginal cases, while transparent reports and patient support programs lower financial and administrative friction.

- Patients influence payer decisions via advocacy

- Advocacy speeds coverage in lung/ILD

- Out-of-pocket costs reduce demand

- Transparent reports/support cut uptake friction

International distributors and partners

Outside the U.S., international distributors and partners control market access and negotiate margins, exclusivity, and regulatory support, giving buyers strong bargaining power; currency fluctuations and public tender dynamics further amplify leverage, while co-development and localization strategies can rebalance negotiating strength in Veracyte’s favor.

- Partner control: market access

- Negotiation: margins, exclusivity, regulatory support

- External factors: currency, tenders

- Mitigants: co-development, localization

Payer concentration controls reimbursement, causing 4–12 week collection delays

Payers (private+CMS) concentrate power, controlling reimbursement amid >50% of US health spend (~$4.5T in 2023), making demand elastic for Veracyte. Repricing/prior auth commonly delay collections 4–12 weeks; strong HEOR/guideline inclusion can lift negotiated rates high-single to low-double digits. Large systems/GPOs and labs demand discounts; Veracyte full‑year 2024 revenue was $373.8M. Patients influence payers via advocacy but limited direct bargaining power.

| Metric | Value |

|---|---|

| US health spend (2023) | $4.5T |

| Veracyte FY2024 revenue | $373.8M |

| Reimbursement delay | 4–12 weeks |

Preview the Actual Deliverable

Veracyte Porter's Five Forces Analysis

This preview shows the exact Veracyte Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample text. It is the full, professionally formatted document ready for download and use the moment you buy. You're viewing the final deliverable, identical to the file provided post-payment. No surprises, just immediate access to the complete analysis.

A Must-Have Tool for Decision-Makers

Veracyte faces moderate buyer power, specialized supplier leverage, significant regulatory and reimbursement barriers deterring new entrants, and escalating substitute diagnostics—while rivalry among genomics peers intensifies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Veracyte’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated sequencing platforms

Veracyte depends on a concentrated set of NGS platform providers—Illumina (~65% installed base in 2024) and Thermo Fisher (~25% in 2024)—creating supplier concentration risk. Platform lock-in and regulatory/clinical validation requirements raise switching costs and extend revalidation timelines. Vendors can thus influence reagent pricing, service levels, and roadmap priorities. Designing multi-platform assays mitigates dependency but incurs materially higher development and validation costs.

Specialized reagents and consumables

Proprietary kits, enzymes, and probes for Veracyte diagnostics are often single-sourced, creating concentrated supplier power. Batch consistency, quality and lead times directly affect test performance and turnaround time. Long-term supply agreements mitigate risk but commonly contain minimum purchase obligations and price escalators. Any supplier disruption can quickly curtail lab throughput and compress margins.

Clinical samples and biobank access

High-quality annotated specimens are essential for Veracyte’s test validation and iteration, yet access is concentrated in 3,000+ academic biobanks that wield bargaining leverage; data-use agreements and IRB constraints typically add 3–9 month delays to access and increase operational costs. Strategic collaborations and material-transfer agreements secure supply lines but often require revenue-sharing or milestone payments, compressing margins and tying sample availability to partner priorities.

Cloud, bioinformatics, and data infrastructure

Computational pipelines rely on dominant cloud vendors (AWS ~32%, Azure ~23%, Google Cloud ~11% in 2024) and licensed genomic databases; switching clouds is feasible but revalidation and security work add meaningful one-time and ongoing costs. Sudden storage/compute price hikes can compress gross margins; preferred-pricing and multi-year contracts help dampen volatility.

- Dependence: high on top 3 clouds

- Switch cost: revalidation/security overhead

- Risk: price hikes → margin pressure

- Mitigation: preferred pricing, multi-year deals

IP licensing and patented biomarkers

IP licensing for signatures and patented biomarkers forces Veracyte to pay royalties and accept field-of-use limits, raising COGS and constraining clinical and geographic expansion; litigation over patents further strengthens supplier leverage. Building Veracyte-owned IP and filing defensive patents reduces dependency and lowers long-term margin pressure.

Platform concentration and cloud dependence raise revalidation costs and margin pressure

Supplier power is high: Illumina (~65% installed base in 2024) and Thermo Fisher (~25%) create platform concentration; proprietary reagents, IP royalties and 3,000+ biobanks (3–9 month access delays) further strengthen suppliers. Cloud dependence (AWS ~32%, Azure ~23%, Google ~11% in 2024) and single-source kits raise switching/revalidation costs and margin risk.

| Item | 2024 Metric |

|---|---|

| Illumina share | ~65% |

| Thermo Fisher share | ~25% |

| AWS | ~32% |

| Azure | ~23% |

| Google Cloud | ~11% |

| Biobanks | 3,000+ (3–9 mo delays) |

| Impact | Higher COGS, revalidation costs, margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Veracyte that uncovers key drivers of competition, buyer and supplier power, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Detailed, strategic commentary highlights dynamics that deter new entrants, influence pricing and profitability, and support investor or internal strategy use.

Clear one-sheet Porter's Five Forces for Veracyte—reduces analysis time and highlights competitive pressures at a glance, customizable with new data and ready to drop into pitch decks or executive reports.

Customers Bargaining Power

Payers drive reimbursement and coverage

Private insurers and CMS set coverage and rates, controlling reimbursement for over 50% of US health spend (~$4.5T in 2023), concentrating buyer power. Strict evidence thresholds and utilization management make demand highly elastic for Veracyte tests. Repricing cycles and prior authorization commonly delay collections by 4–12 weeks. Strong health-economic data and guideline inclusion can secure high-single to low-double-digit uplift in negotiated reimbursement.

Health systems and IDNs consolidate volume

Large health systems, GPOs and reference labs now aggregate most testing volume and can demand discounts, EMR integration and strict SLAs; Veracyte reported full‑year 2024 revenue of $373.8 million, so major contract wins or losses materially shift share and quarterly results. Embedded workflows and EMR integration raise switching costs for buyers, favoring Veracyte when contracts lock in referrals and operational pathways.

Specialist physicians as gatekeepers

Pulmonologists, endocrinologists and pathologists act as gatekeepers for Veracyte tests, prioritizing turnaround time, ease of use and demonstrated clinical validity when deciding adoption. In 2024 KOL endorsements and peer‑reviewed outcomes continued to lower perceived risk and accelerate referrals. When comparable in‑house alternatives exist, clinicians exhibit higher price sensitivity, reducing Veracyte's negotiating leverage.

Patients and advocacy groups

Patients have limited direct bargaining power but can sway payer policy through organized advocacy; groups focused on lung disease and ILD have helped accelerate coverage for diagnostic genomic tools. Out-of-pocket exposure suppresses uptake in marginal cases, while transparent reports and patient support programs lower financial and administrative friction.

- Patients influence payer decisions via advocacy

- Advocacy speeds coverage in lung/ILD

- Out-of-pocket costs reduce demand

- Transparent reports/support cut uptake friction

International distributors and partners

Outside the U.S., international distributors and partners control market access and negotiate margins, exclusivity, and regulatory support, giving buyers strong bargaining power; currency fluctuations and public tender dynamics further amplify leverage, while co-development and localization strategies can rebalance negotiating strength in Veracyte’s favor.

- Partner control: market access

- Negotiation: margins, exclusivity, regulatory support

- External factors: currency, tenders

- Mitigants: co-development, localization

Payer concentration controls reimbursement, causing 4–12 week collection delays

Payers (private+CMS) concentrate power, controlling reimbursement amid >50% of US health spend (~$4.5T in 2023), making demand elastic for Veracyte. Repricing/prior auth commonly delay collections 4–12 weeks; strong HEOR/guideline inclusion can lift negotiated rates high-single to low-double digits. Large systems/GPOs and labs demand discounts; Veracyte full‑year 2024 revenue was $373.8M. Patients influence payers via advocacy but limited direct bargaining power.

| Metric | Value |

|---|---|

| US health spend (2023) | $4.5T |

| Veracyte FY2024 revenue | $373.8M |

| Reimbursement delay | 4–12 weeks |

Preview the Actual Deliverable

Veracyte Porter's Five Forces Analysis

This preview shows the exact Veracyte Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample text. It is the full, professionally formatted document ready for download and use the moment you buy. You're viewing the final deliverable, identical to the file provided post-payment. No surprises, just immediate access to the complete analysis.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Veracyte faces moderate buyer power, specialized supplier leverage, significant regulatory and reimbursement barriers deterring new entrants, and escalating substitute diagnostics—while rivalry among genomics peers intensifies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Veracyte’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated sequencing platforms

Veracyte depends on a concentrated set of NGS platform providers—Illumina (~65% installed base in 2024) and Thermo Fisher (~25% in 2024)—creating supplier concentration risk. Platform lock-in and regulatory/clinical validation requirements raise switching costs and extend revalidation timelines. Vendors can thus influence reagent pricing, service levels, and roadmap priorities. Designing multi-platform assays mitigates dependency but incurs materially higher development and validation costs.

Specialized reagents and consumables

Proprietary kits, enzymes, and probes for Veracyte diagnostics are often single-sourced, creating concentrated supplier power. Batch consistency, quality and lead times directly affect test performance and turnaround time. Long-term supply agreements mitigate risk but commonly contain minimum purchase obligations and price escalators. Any supplier disruption can quickly curtail lab throughput and compress margins.

Clinical samples and biobank access

High-quality annotated specimens are essential for Veracyte’s test validation and iteration, yet access is concentrated in 3,000+ academic biobanks that wield bargaining leverage; data-use agreements and IRB constraints typically add 3–9 month delays to access and increase operational costs. Strategic collaborations and material-transfer agreements secure supply lines but often require revenue-sharing or milestone payments, compressing margins and tying sample availability to partner priorities.

Cloud, bioinformatics, and data infrastructure

Computational pipelines rely on dominant cloud vendors (AWS ~32%, Azure ~23%, Google Cloud ~11% in 2024) and licensed genomic databases; switching clouds is feasible but revalidation and security work add meaningful one-time and ongoing costs. Sudden storage/compute price hikes can compress gross margins; preferred-pricing and multi-year contracts help dampen volatility.

- Dependence: high on top 3 clouds

- Switch cost: revalidation/security overhead

- Risk: price hikes → margin pressure

- Mitigation: preferred pricing, multi-year deals

IP licensing and patented biomarkers

IP licensing for signatures and patented biomarkers forces Veracyte to pay royalties and accept field-of-use limits, raising COGS and constraining clinical and geographic expansion; litigation over patents further strengthens supplier leverage. Building Veracyte-owned IP and filing defensive patents reduces dependency and lowers long-term margin pressure.

Platform concentration and cloud dependence raise revalidation costs and margin pressure

Supplier power is high: Illumina (~65% installed base in 2024) and Thermo Fisher (~25%) create platform concentration; proprietary reagents, IP royalties and 3,000+ biobanks (3–9 month access delays) further strengthen suppliers. Cloud dependence (AWS ~32%, Azure ~23%, Google ~11% in 2024) and single-source kits raise switching/revalidation costs and margin risk.

| Item | 2024 Metric |

|---|---|

| Illumina share | ~65% |

| Thermo Fisher share | ~25% |

| AWS | ~32% |

| Azure | ~23% |

| Google Cloud | ~11% |

| Biobanks | 3,000+ (3–9 mo delays) |

| Impact | Higher COGS, revalidation costs, margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Veracyte that uncovers key drivers of competition, buyer and supplier power, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Detailed, strategic commentary highlights dynamics that deter new entrants, influence pricing and profitability, and support investor or internal strategy use.

Clear one-sheet Porter's Five Forces for Veracyte—reduces analysis time and highlights competitive pressures at a glance, customizable with new data and ready to drop into pitch decks or executive reports.

Customers Bargaining Power

Payers drive reimbursement and coverage

Private insurers and CMS set coverage and rates, controlling reimbursement for over 50% of US health spend (~$4.5T in 2023), concentrating buyer power. Strict evidence thresholds and utilization management make demand highly elastic for Veracyte tests. Repricing cycles and prior authorization commonly delay collections by 4–12 weeks. Strong health-economic data and guideline inclusion can secure high-single to low-double-digit uplift in negotiated reimbursement.

Health systems and IDNs consolidate volume

Large health systems, GPOs and reference labs now aggregate most testing volume and can demand discounts, EMR integration and strict SLAs; Veracyte reported full‑year 2024 revenue of $373.8 million, so major contract wins or losses materially shift share and quarterly results. Embedded workflows and EMR integration raise switching costs for buyers, favoring Veracyte when contracts lock in referrals and operational pathways.

Specialist physicians as gatekeepers

Pulmonologists, endocrinologists and pathologists act as gatekeepers for Veracyte tests, prioritizing turnaround time, ease of use and demonstrated clinical validity when deciding adoption. In 2024 KOL endorsements and peer‑reviewed outcomes continued to lower perceived risk and accelerate referrals. When comparable in‑house alternatives exist, clinicians exhibit higher price sensitivity, reducing Veracyte's negotiating leverage.

Patients and advocacy groups

Patients have limited direct bargaining power but can sway payer policy through organized advocacy; groups focused on lung disease and ILD have helped accelerate coverage for diagnostic genomic tools. Out-of-pocket exposure suppresses uptake in marginal cases, while transparent reports and patient support programs lower financial and administrative friction.

- Patients influence payer decisions via advocacy

- Advocacy speeds coverage in lung/ILD

- Out-of-pocket costs reduce demand

- Transparent reports/support cut uptake friction

International distributors and partners

Outside the U.S., international distributors and partners control market access and negotiate margins, exclusivity, and regulatory support, giving buyers strong bargaining power; currency fluctuations and public tender dynamics further amplify leverage, while co-development and localization strategies can rebalance negotiating strength in Veracyte’s favor.

- Partner control: market access

- Negotiation: margins, exclusivity, regulatory support

- External factors: currency, tenders

- Mitigants: co-development, localization

Payer concentration controls reimbursement, causing 4–12 week collection delays

Payers (private+CMS) concentrate power, controlling reimbursement amid >50% of US health spend (~$4.5T in 2023), making demand elastic for Veracyte. Repricing/prior auth commonly delay collections 4–12 weeks; strong HEOR/guideline inclusion can lift negotiated rates high-single to low-double digits. Large systems/GPOs and labs demand discounts; Veracyte full‑year 2024 revenue was $373.8M. Patients influence payers via advocacy but limited direct bargaining power.

| Metric | Value |

|---|---|

| US health spend (2023) | $4.5T |

| Veracyte FY2024 revenue | $373.8M |

| Reimbursement delay | 4–12 weeks |

Preview the Actual Deliverable

Veracyte Porter's Five Forces Analysis

This preview shows the exact Veracyte Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample text. It is the full, professionally formatted document ready for download and use the moment you buy. You're viewing the final deliverable, identical to the file provided post-payment. No surprises, just immediate access to the complete analysis.