Verallia Porter's Five Forces Analysis

From Overview to Strategy Blueprint

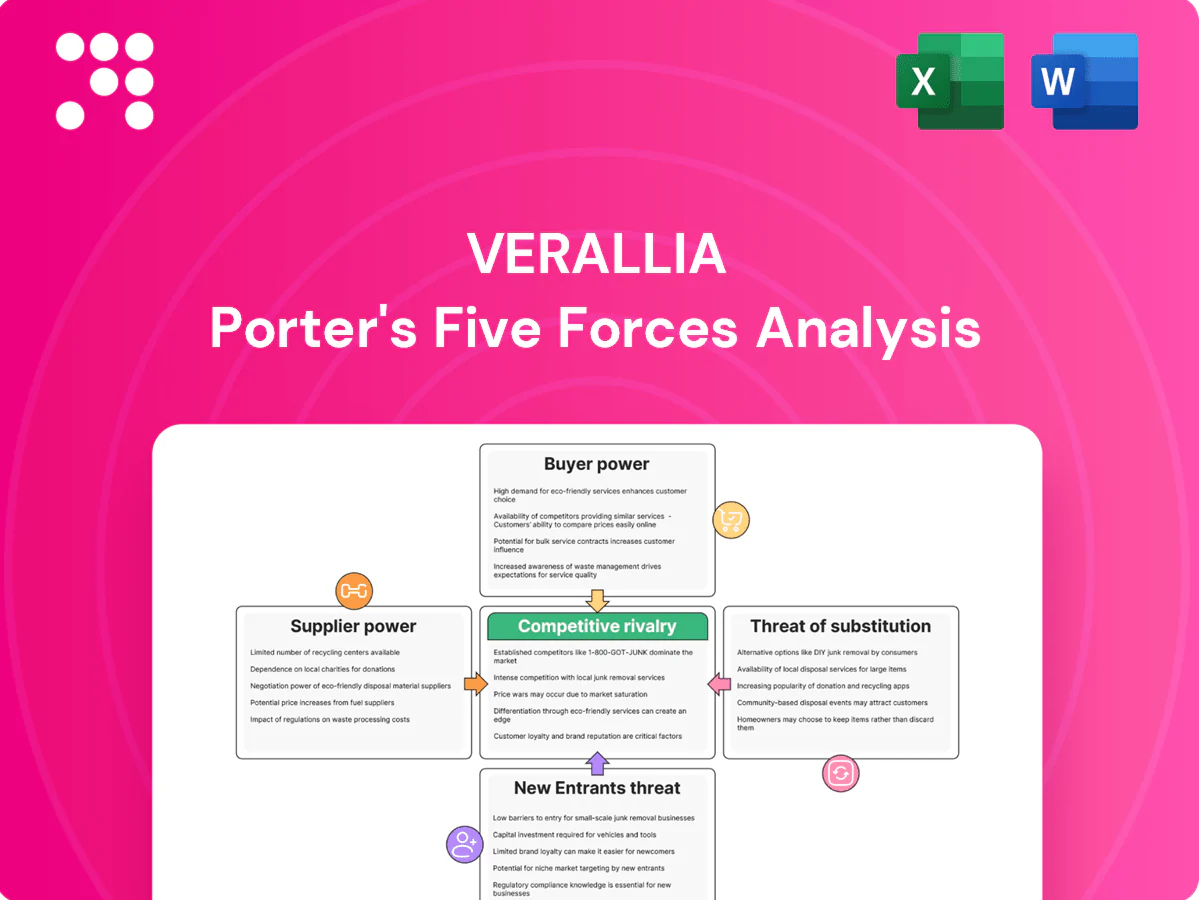

Verallia’s Porter's Five Forces snapshot highlights strong buyer power, concentrated supplier dynamics, moderate threat of new entrants due to capex and regulations, tangible substitute risks from alternative packaging, and intense rivalry among glassmakers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Verallia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy-intensive inputs

Glass melting depends on steady natural gas and electricity supplies, giving energy providers pricing and continuity leverage; EU industrial users faced pronounced volatility in 2022–24 and carbon costs rose with the EU ETS near €100/tCO2 in 2024, transmitting into COGS. Hedging reduces short-term swings but does not remove exposure, while regional energy rules and carbon pricing amplify supplier influence.

Raw materials concentration

Silica sand, soda ash, limestone and specialty additives are globally traded but sourced in regional clusters, with soda ash global production about 58 million tonnes (USGS 2022) and major suppliers including Solvay, Ciner and Tata Chemicals. Strict quality and consistency specs narrow the viable supplier pool for Verallia, raising switching costs. Transport bottlenecks or regional disruptions can quickly elevate supplier power and prices. Long-term contracts mitigate supply risk but lock in terms and limit flexibility.

Cullet availability constraints

Recycled glass (cullet) is critical for Verallia’s cost base, delivering up to ~30% melting energy savings and significant CO2 reductions; availability hinges on local collection systems and deposit return schemes, causing regional scarcities in 2024. Where supply is tight, cullet processors exercise pricing power, raising input costs. Strict quality needs—color sorting, low contamination—further limit substitutability and raise procurement complexity.

Specialized equipment and refractory

Furnace refractories, molds and forming machinery for Verallia come from specialized vendors, with refractory relines typically occurring every 5–7 years and mold lead times of 12–20 weeks, raising effective switching costs; supplier-held technical IP and multi-month lead times let vendors command tighter contract terms and price premia, while service support and uptime SLAs (often 98–99%) are used as key negotiation levers.

- reline cycle: 5–7 years

- mold lead time: 12–20 weeks

- typical uptime SLAs: 98–99%

Logistics and glass fragility

Heavy, fragile glass forces Verallia to rely on specialized carriers and Euro-pallet systems, concentrating supplier power as reliable handling is non-negotiable. Fuel surcharges and 2024 capacity tightness pushed carrier leverage higher, with market surcharges reported up to double-digit percentiles during peak months. Plant-customer proximity lowers but does not eliminate dependency on capable logistics. Contracted lanes mitigate spot exposure yet often lock in higher base rates.

- Specialized carriers increase switching costs

- 2024 fuel/capacity spikes amplified carrier bargaining

- Proximity reduces but does not remove logistics dependence

- Contracted lanes hedge risk at cost of elevated base rates

EU ETS €100/tCO2, gas shocks and regional input constraints squeeze glass margins

Energy and carbon (EU ETS ~€100/tCO2 in 2024) and natural gas give suppliers strong leverage; hedging helps but exposure remains. Key inputs—soda ash ~58 Mt (USGS 2022), cullet (~30% energy savings) and specialty refractories/molds (reline 5–7y, molds 12–20w, uptime 98–99%)—are regionally constrained, raising switching costs. Logistics/fuel spikes in 2024 pushed carrier leverage and double-digit surcharges.

| Input | Metric | 2024 signal |

|---|---|---|

| EU ETS | €/tCO2 | ~100 |

| Soda ash | Global prod. | ~58 Mt (2022) |

| Cullet | Energy saving | ~30% |

| Molds/Refractories | Lead/relines | 12–20w / 5–7y |

| Logistics | Surcharges | Double-digit peaks 2024 |

What is included in the product

Concise Porter’s Five Forces for Verallia, diagnosing competitive rivalry, supplier and buyer power, entry barriers, and substitute risks with strategic implications.

Clear one-sheet Porter's Five Forces for Verallia—instantly visualizes competitive pressure and strategic risks so leadership can make faster, data-driven decisions.

Customers Bargaining Power

Concentrated beverage majors

Global brewers (AB InBev, Heineken), soft-drink giants (Coca-Cola, PepsiCo) and spirits leaders (Diageo, Pernod Ricard) buy glass at scale, using multi-year tenders to extract lower prices and favoured allocation. They routinely dual-source to maintain pricing pressure and switch volumes quickly. Suppliers trade price for higher service levels and innovation, such as lightweighting and custom finishes, to retain these consolidated accounts.

Switching and qualification costs

Changing bottle suppliers requires mold transfers, line trials and food-safety qualification that typically take 4–12 weeks; direct costs commonly range €20k–€100k for certification and €50k–€250k for trials/mold moves, modestly reducing buyer power short-term. Large buyers often have in-house teams to speed transitions, while contractual penalties and delivery timelines remain levers for both sides.

Price sensitivity by segment

Value and private-label segments are highly price elastic, increasing buyer leverage as retailers chase margins; Verallia reported €2.4bn sales in 2024 with heavy exposure to these channels. Premium wine and spirits customers accept higher unit prices for design and brand equity, reducing price pressure. Seasonal demand and promo cycles create order volatility and negotiation leverage. Rising ESG targets shift procurement discussions toward total cost of ownership and recycled-content premiums.

Specification control

Buyers dictate designs, colors and performance specs, constraining Verallia’s product discretion and margin flexibility; by 2024 key accounts pushed custom molds that deepen buyer dependence while often remaining buyer-owned. Demand-forecasting and VMI arrangements in 2024 shifted inventory carrying costs toward suppliers, and OTIF penalties further amplified buyer leverage.

- Buyers set specs, limiting supplier options

- Custom molds increase switch costs; often buyer-owned

- VMI/demand forecasts shift inventory risk to supplier

- OTIF penalties raise financial exposure

Alternative packaging options

Access to PET, aluminum, cans and cartons gives buyers credible outside options, enabling cross-material benchmarking that forces Verallia to concede on price and lead times; marketing repositioning and sustainability narratives (e.g., life-cycle claims) make material switches more acceptable to brands.

- cross-material benchmarking

- sustainability-driven substitutability

- marketing enables switches

Tenders lock buyers: switch 4-12 weeks; certification €20k–€100k; trials €50k–€250k

Global brewers and soft‑drink giants extract scale-based discounts via multi‑year tenders; Verallia reported €2.4bn sales in 2024. Switching suppliers takes 4–12 weeks with certification costs €20k–€100k and trials/mold moves €50k–€250k, reducing short‑term buyer power. VMI, OTIF penalties and buyer-owned molds shift risk and lock in specifications, while cross‑material options raise price pressure.

| Metric | Value (2024) |

|---|---|

| Verallia sales | €2.4bn |

| Supplier switch time | 4–12 weeks |

| Certification cost | €20k–€100k |

| Trials/mold moves | €50k–€250k |

Same Document Delivered

Verallia Porter's Five Forces Analysis

This preview shows the exact Verallia Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, ready for download and use the moment you buy. You're viewing the final, complete deliverable.

From Overview to Strategy Blueprint

Verallia’s Porter's Five Forces snapshot highlights strong buyer power, concentrated supplier dynamics, moderate threat of new entrants due to capex and regulations, tangible substitute risks from alternative packaging, and intense rivalry among glassmakers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Verallia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy-intensive inputs

Glass melting depends on steady natural gas and electricity supplies, giving energy providers pricing and continuity leverage; EU industrial users faced pronounced volatility in 2022–24 and carbon costs rose with the EU ETS near €100/tCO2 in 2024, transmitting into COGS. Hedging reduces short-term swings but does not remove exposure, while regional energy rules and carbon pricing amplify supplier influence.

Raw materials concentration

Silica sand, soda ash, limestone and specialty additives are globally traded but sourced in regional clusters, with soda ash global production about 58 million tonnes (USGS 2022) and major suppliers including Solvay, Ciner and Tata Chemicals. Strict quality and consistency specs narrow the viable supplier pool for Verallia, raising switching costs. Transport bottlenecks or regional disruptions can quickly elevate supplier power and prices. Long-term contracts mitigate supply risk but lock in terms and limit flexibility.

Cullet availability constraints

Recycled glass (cullet) is critical for Verallia’s cost base, delivering up to ~30% melting energy savings and significant CO2 reductions; availability hinges on local collection systems and deposit return schemes, causing regional scarcities in 2024. Where supply is tight, cullet processors exercise pricing power, raising input costs. Strict quality needs—color sorting, low contamination—further limit substitutability and raise procurement complexity.

Specialized equipment and refractory

Furnace refractories, molds and forming machinery for Verallia come from specialized vendors, with refractory relines typically occurring every 5–7 years and mold lead times of 12–20 weeks, raising effective switching costs; supplier-held technical IP and multi-month lead times let vendors command tighter contract terms and price premia, while service support and uptime SLAs (often 98–99%) are used as key negotiation levers.

- reline cycle: 5–7 years

- mold lead time: 12–20 weeks

- typical uptime SLAs: 98–99%

Logistics and glass fragility

Heavy, fragile glass forces Verallia to rely on specialized carriers and Euro-pallet systems, concentrating supplier power as reliable handling is non-negotiable. Fuel surcharges and 2024 capacity tightness pushed carrier leverage higher, with market surcharges reported up to double-digit percentiles during peak months. Plant-customer proximity lowers but does not eliminate dependency on capable logistics. Contracted lanes mitigate spot exposure yet often lock in higher base rates.

- Specialized carriers increase switching costs

- 2024 fuel/capacity spikes amplified carrier bargaining

- Proximity reduces but does not remove logistics dependence

- Contracted lanes hedge risk at cost of elevated base rates

EU ETS €100/tCO2, gas shocks and regional input constraints squeeze glass margins

Energy and carbon (EU ETS ~€100/tCO2 in 2024) and natural gas give suppliers strong leverage; hedging helps but exposure remains. Key inputs—soda ash ~58 Mt (USGS 2022), cullet (~30% energy savings) and specialty refractories/molds (reline 5–7y, molds 12–20w, uptime 98–99%)—are regionally constrained, raising switching costs. Logistics/fuel spikes in 2024 pushed carrier leverage and double-digit surcharges.

| Input | Metric | 2024 signal |

|---|---|---|

| EU ETS | €/tCO2 | ~100 |

| Soda ash | Global prod. | ~58 Mt (2022) |

| Cullet | Energy saving | ~30% |

| Molds/Refractories | Lead/relines | 12–20w / 5–7y |

| Logistics | Surcharges | Double-digit peaks 2024 |

What is included in the product

Concise Porter’s Five Forces for Verallia, diagnosing competitive rivalry, supplier and buyer power, entry barriers, and substitute risks with strategic implications.

Clear one-sheet Porter's Five Forces for Verallia—instantly visualizes competitive pressure and strategic risks so leadership can make faster, data-driven decisions.

Customers Bargaining Power

Concentrated beverage majors

Global brewers (AB InBev, Heineken), soft-drink giants (Coca-Cola, PepsiCo) and spirits leaders (Diageo, Pernod Ricard) buy glass at scale, using multi-year tenders to extract lower prices and favoured allocation. They routinely dual-source to maintain pricing pressure and switch volumes quickly. Suppliers trade price for higher service levels and innovation, such as lightweighting and custom finishes, to retain these consolidated accounts.

Switching and qualification costs

Changing bottle suppliers requires mold transfers, line trials and food-safety qualification that typically take 4–12 weeks; direct costs commonly range €20k–€100k for certification and €50k–€250k for trials/mold moves, modestly reducing buyer power short-term. Large buyers often have in-house teams to speed transitions, while contractual penalties and delivery timelines remain levers for both sides.

Price sensitivity by segment

Value and private-label segments are highly price elastic, increasing buyer leverage as retailers chase margins; Verallia reported €2.4bn sales in 2024 with heavy exposure to these channels. Premium wine and spirits customers accept higher unit prices for design and brand equity, reducing price pressure. Seasonal demand and promo cycles create order volatility and negotiation leverage. Rising ESG targets shift procurement discussions toward total cost of ownership and recycled-content premiums.

Specification control

Buyers dictate designs, colors and performance specs, constraining Verallia’s product discretion and margin flexibility; by 2024 key accounts pushed custom molds that deepen buyer dependence while often remaining buyer-owned. Demand-forecasting and VMI arrangements in 2024 shifted inventory carrying costs toward suppliers, and OTIF penalties further amplified buyer leverage.

- Buyers set specs, limiting supplier options

- Custom molds increase switch costs; often buyer-owned

- VMI/demand forecasts shift inventory risk to supplier

- OTIF penalties raise financial exposure

Alternative packaging options

Access to PET, aluminum, cans and cartons gives buyers credible outside options, enabling cross-material benchmarking that forces Verallia to concede on price and lead times; marketing repositioning and sustainability narratives (e.g., life-cycle claims) make material switches more acceptable to brands.

- cross-material benchmarking

- sustainability-driven substitutability

- marketing enables switches

Tenders lock buyers: switch 4-12 weeks; certification €20k–€100k; trials €50k–€250k

Global brewers and soft‑drink giants extract scale-based discounts via multi‑year tenders; Verallia reported €2.4bn sales in 2024. Switching suppliers takes 4–12 weeks with certification costs €20k–€100k and trials/mold moves €50k–€250k, reducing short‑term buyer power. VMI, OTIF penalties and buyer-owned molds shift risk and lock in specifications, while cross‑material options raise price pressure.

| Metric | Value (2024) |

|---|---|

| Verallia sales | €2.4bn |

| Supplier switch time | 4–12 weeks |

| Certification cost | €20k–€100k |

| Trials/mold moves | €50k–€250k |

Same Document Delivered

Verallia Porter's Five Forces Analysis

This preview shows the exact Verallia Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, ready for download and use the moment you buy. You're viewing the final, complete deliverable.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Verallia’s Porter's Five Forces snapshot highlights strong buyer power, concentrated supplier dynamics, moderate threat of new entrants due to capex and regulations, tangible substitute risks from alternative packaging, and intense rivalry among glassmakers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Verallia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy-intensive inputs

Glass melting depends on steady natural gas and electricity supplies, giving energy providers pricing and continuity leverage; EU industrial users faced pronounced volatility in 2022–24 and carbon costs rose with the EU ETS near €100/tCO2 in 2024, transmitting into COGS. Hedging reduces short-term swings but does not remove exposure, while regional energy rules and carbon pricing amplify supplier influence.

Raw materials concentration

Silica sand, soda ash, limestone and specialty additives are globally traded but sourced in regional clusters, with soda ash global production about 58 million tonnes (USGS 2022) and major suppliers including Solvay, Ciner and Tata Chemicals. Strict quality and consistency specs narrow the viable supplier pool for Verallia, raising switching costs. Transport bottlenecks or regional disruptions can quickly elevate supplier power and prices. Long-term contracts mitigate supply risk but lock in terms and limit flexibility.

Cullet availability constraints

Recycled glass (cullet) is critical for Verallia’s cost base, delivering up to ~30% melting energy savings and significant CO2 reductions; availability hinges on local collection systems and deposit return schemes, causing regional scarcities in 2024. Where supply is tight, cullet processors exercise pricing power, raising input costs. Strict quality needs—color sorting, low contamination—further limit substitutability and raise procurement complexity.

Specialized equipment and refractory

Furnace refractories, molds and forming machinery for Verallia come from specialized vendors, with refractory relines typically occurring every 5–7 years and mold lead times of 12–20 weeks, raising effective switching costs; supplier-held technical IP and multi-month lead times let vendors command tighter contract terms and price premia, while service support and uptime SLAs (often 98–99%) are used as key negotiation levers.

- reline cycle: 5–7 years

- mold lead time: 12–20 weeks

- typical uptime SLAs: 98–99%

Logistics and glass fragility

Heavy, fragile glass forces Verallia to rely on specialized carriers and Euro-pallet systems, concentrating supplier power as reliable handling is non-negotiable. Fuel surcharges and 2024 capacity tightness pushed carrier leverage higher, with market surcharges reported up to double-digit percentiles during peak months. Plant-customer proximity lowers but does not eliminate dependency on capable logistics. Contracted lanes mitigate spot exposure yet often lock in higher base rates.

- Specialized carriers increase switching costs

- 2024 fuel/capacity spikes amplified carrier bargaining

- Proximity reduces but does not remove logistics dependence

- Contracted lanes hedge risk at cost of elevated base rates

EU ETS €100/tCO2, gas shocks and regional input constraints squeeze glass margins

Energy and carbon (EU ETS ~€100/tCO2 in 2024) and natural gas give suppliers strong leverage; hedging helps but exposure remains. Key inputs—soda ash ~58 Mt (USGS 2022), cullet (~30% energy savings) and specialty refractories/molds (reline 5–7y, molds 12–20w, uptime 98–99%)—are regionally constrained, raising switching costs. Logistics/fuel spikes in 2024 pushed carrier leverage and double-digit surcharges.

| Input | Metric | 2024 signal |

|---|---|---|

| EU ETS | €/tCO2 | ~100 |

| Soda ash | Global prod. | ~58 Mt (2022) |

| Cullet | Energy saving | ~30% |

| Molds/Refractories | Lead/relines | 12–20w / 5–7y |

| Logistics | Surcharges | Double-digit peaks 2024 |

What is included in the product

Concise Porter’s Five Forces for Verallia, diagnosing competitive rivalry, supplier and buyer power, entry barriers, and substitute risks with strategic implications.

Clear one-sheet Porter's Five Forces for Verallia—instantly visualizes competitive pressure and strategic risks so leadership can make faster, data-driven decisions.

Customers Bargaining Power

Concentrated beverage majors

Global brewers (AB InBev, Heineken), soft-drink giants (Coca-Cola, PepsiCo) and spirits leaders (Diageo, Pernod Ricard) buy glass at scale, using multi-year tenders to extract lower prices and favoured allocation. They routinely dual-source to maintain pricing pressure and switch volumes quickly. Suppliers trade price for higher service levels and innovation, such as lightweighting and custom finishes, to retain these consolidated accounts.

Switching and qualification costs

Changing bottle suppliers requires mold transfers, line trials and food-safety qualification that typically take 4–12 weeks; direct costs commonly range €20k–€100k for certification and €50k–€250k for trials/mold moves, modestly reducing buyer power short-term. Large buyers often have in-house teams to speed transitions, while contractual penalties and delivery timelines remain levers for both sides.

Price sensitivity by segment

Value and private-label segments are highly price elastic, increasing buyer leverage as retailers chase margins; Verallia reported €2.4bn sales in 2024 with heavy exposure to these channels. Premium wine and spirits customers accept higher unit prices for design and brand equity, reducing price pressure. Seasonal demand and promo cycles create order volatility and negotiation leverage. Rising ESG targets shift procurement discussions toward total cost of ownership and recycled-content premiums.

Specification control

Buyers dictate designs, colors and performance specs, constraining Verallia’s product discretion and margin flexibility; by 2024 key accounts pushed custom molds that deepen buyer dependence while often remaining buyer-owned. Demand-forecasting and VMI arrangements in 2024 shifted inventory carrying costs toward suppliers, and OTIF penalties further amplified buyer leverage.

- Buyers set specs, limiting supplier options

- Custom molds increase switch costs; often buyer-owned

- VMI/demand forecasts shift inventory risk to supplier

- OTIF penalties raise financial exposure

Alternative packaging options

Access to PET, aluminum, cans and cartons gives buyers credible outside options, enabling cross-material benchmarking that forces Verallia to concede on price and lead times; marketing repositioning and sustainability narratives (e.g., life-cycle claims) make material switches more acceptable to brands.

- cross-material benchmarking

- sustainability-driven substitutability

- marketing enables switches

Tenders lock buyers: switch 4-12 weeks; certification €20k–€100k; trials €50k–€250k

Global brewers and soft‑drink giants extract scale-based discounts via multi‑year tenders; Verallia reported €2.4bn sales in 2024. Switching suppliers takes 4–12 weeks with certification costs €20k–€100k and trials/mold moves €50k–€250k, reducing short‑term buyer power. VMI, OTIF penalties and buyer-owned molds shift risk and lock in specifications, while cross‑material options raise price pressure.

| Metric | Value (2024) |

|---|---|

| Verallia sales | €2.4bn |

| Supplier switch time | 4–12 weeks |

| Certification cost | €20k–€100k |

| Trials/mold moves | €50k–€250k |

Same Document Delivered

Verallia Porter's Five Forces Analysis

This preview shows the exact Verallia Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, ready for download and use the moment you buy. You're viewing the final, complete deliverable.