Verbund PESTLE Analysis

Your Shortcut to Market Insight Starts Here

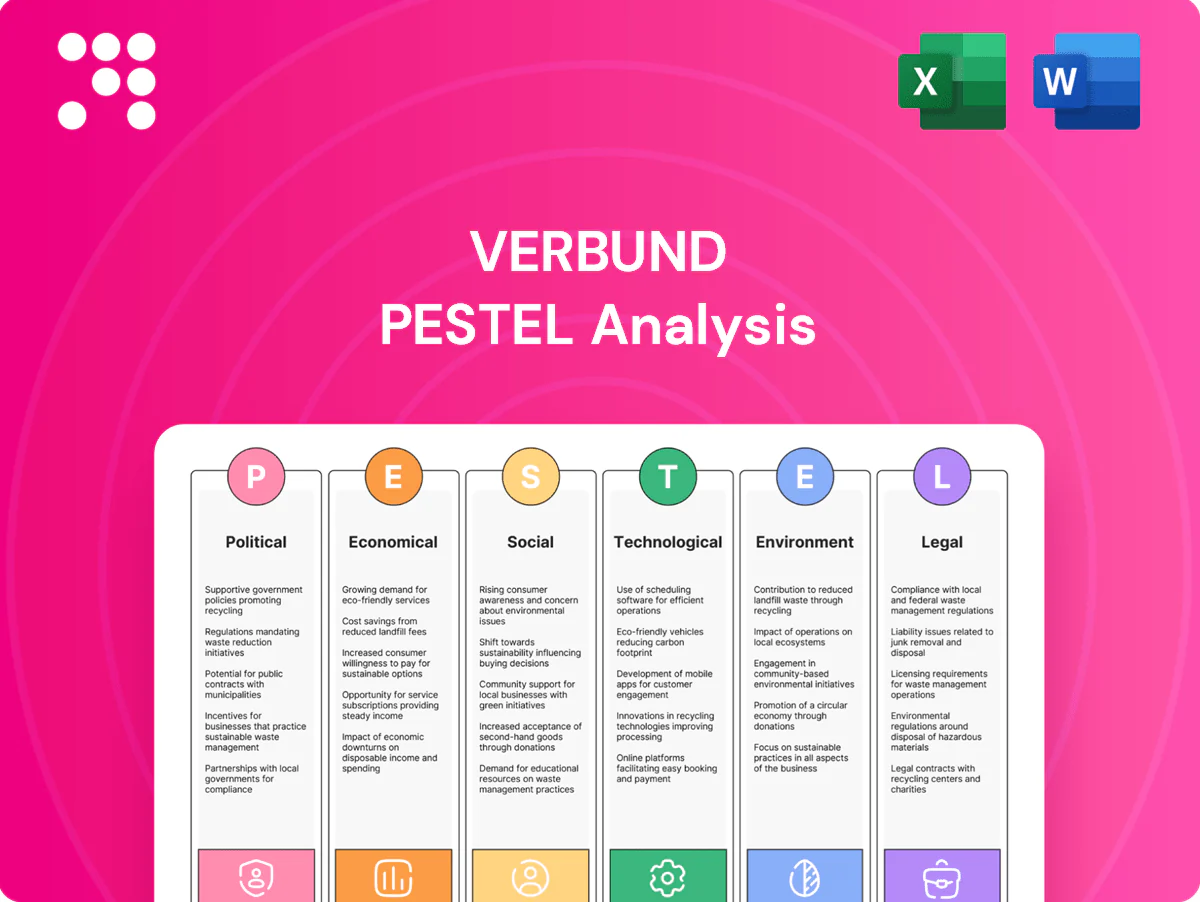

Explore how political, economic, social, technological, legal and environmental forces shape Verbund's trajectory in our concise PESTLE summary—perfect for investors and strategists. Buy the full analysis to access actionable insights, forecasts and ready-to-use slides for smarter decisions.

Political factors

EU Green Deal alignment

Verbund benefits directly from the EU Green Deal and Fit for 55 framework targeting at least 55% GHG cuts by 2030 and climate neutrality by 2050, which prioritizes renewables and grid expansion. Access to EU funding programmes such as the €723.8bn Recovery and Resilience Facility and the €5.84bn Connecting Europe Facility can lower project costs and de-risk large investments. Stable EU policy enables multi-decade planning, while any delays in permitting or EU rulemaking could slow project pipelines and compress near-term cash flows.

Austrian energy policy support

Austrian energy policy prioritizes hydropower optimization, wind/solar build‑out and storage, aligning with VERBUND’s core (hydro accounts for ≈90% of its generation). The Republic holds about 51% of VERBUND, aligning state interests with security of supply and price stability. Austria targets 100% renewable electricity by 2030, and domestic incentives can speed hydro modernization. Political shifts could recalibrate subsidies or tariff regimes, impacting returns.

Market design and price caps

EU electricity market design reform adopted in 2023 reshapes revenue models for generators and storage, and several member states applied temporary windfall taxes or price caps in 2022–24 that compressed margins during high-price episodes. Capacity, flexibility and ancillary-services mechanisms implemented at national level can create incremental revenue streams. Regulatory clarity is crucial to secure financing for Verbund’s large capex in hydropower and renewables.

Cross-border integration

ENTSO-E's interconnector policies and coordinated market rules (ENTSO-E comprises 42 TSOs across 36 countries) increase cross-border trading and system balancing, while favorable allocation rules and congestion income can materially support earnings for grid owners. Geopolitical shocks — for example the Nord Stream pipeline halt since September 2022 — have shifted gas and power flows, driving price volatility and altering dispatch economics; regional coordination changes hydropower dispatch value.

- Interconnector policy: boosts trading, balancing

- ENTSO-E: 42 TSOs / 36 countries

- Allocation & congestion income: supports earnings

- Geopolitics (Nord Stream halt Sep 2022): shifts flows, raises price volatility

- Regional coordination: changes hydropower dispatch value

Public investment and resilience

Public investment via NextGenerationEU and the Recovery and Resilience Facility (RRF, ~€700bn) plus InvestEU can catalyze grids, storage and hydro refurbishment projects; political prioritization of resilience after the 2022 energy crisis strengthens support for hydro refurbishments. Disaster-recovery frameworks affect insurance payouts and restoration timelines, while funding competition can delay allocations.

- EU RRF/NextGenerationEU: ~€700bn mobilised

- InvestEU/CEF target energy infrastructure funding

- Disaster-recovery rules shape insurance/restoration speed

Austrian hydro mix ≈90%; 100% renewables by 2030

EU Green Deal/Fit for 55 and market reform (2023) materially favor Verbund’s hydro-led mix (≈90% generation) and enable multi-decade planning, while permitting delays or windfall taxes can compress near-term cash flows. Austria owns ≈51% of Verbund and targets 100% renewables by 2030, supporting hydro modernization. EU funds (RRF ≈€723.8bn, CEF €5.84bn) and ENTSO-E coordination boost cross‑border revenues; geopolitics (Nord Stream halt Sep 2022) raises price volatility.

| Item | Key figure |

|---|---|

| Verbund hydro share | ≈90% |

| State ownership | ≈51% |

| Austria 2030 target | 100% renewables |

| RRF | ≈€723.8bn |

| CEF | €5.84bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Verbund, with data-backed, region- and industry-specific insights designed for executives and investors; each section includes detailed sub-points and forward-looking analysis ready for plans, decks, or reports.

A concise, visually segmented PESTLE summary for Verbund that distills regulatory, environmental, and market risks into an easily shareable slide or note, enabling rapid alignment across teams and clearer discussion of strategic responses during planning sessions.

Economic factors

Power price volatility

Hydrology and fuel-price movements drive wholesale power swings—prices have spiked to several hundred EUR/MWh in stress periods—directly affecting VERBUND’s merchant revenues. Merchant exposure can boost returns in tight markets but increases earnings volatility. Active hedging and PPAs stabilize cash flows while capping upside. Price volatility also dictates investment timing and the balance between flexible hydro and long-term contracted assets.

Interest rates and capex

Higher interest rates — with the ECB policy rate near 3.75% in mid‑2025 — have pushed WACC up several hundred basis points, squeezing IRRs for renewables and grid capex and making marginal projects less viable.

VERBUND’s investment‑grade balance sheet and low leverage help preserve market access and favorable terms, evidenced by active refinancing and green bond issuance to lock cheaper, long‑dated funding.

Normalization or cuts in rates would materially improve project economics and unlock more marginal renewables and grid investments.

Inflation and supply chains

Component and EPC costs for solar, wind and grid projects face inflationary pressure against a euro-area inflation backdrop of about 2.4% in 2024, raising project budgets and contingency needs. Indexation clauses in PPAs and regulated tariffs partially offset cost drift. Logistics bottlenecks and commodity price swings disrupt delivery schedules. Supplier diversification and framework contracts reduce procurement and timing risk.

Hydrology-driven output

Verbund's earnings are highly sensitive to precipitation, snowpack and river flows; hydropower comprises roughly 90% of its generation, so dry years compress volumes and ancillary-service revenue while wet years boost low-cost output and margins. The 2023 European low-flow episode reduced run-off in parts of the Alps by up to 20%, highlighting volatility; expanding wind and solar smooths this variability.

- Hydrology sensitivity: ~90% hydro

- 2023 low flows: up to 20% run-off drop

- Drought impact: lower volumes and ancillary revenues

- Diversification: wind/solar reduce earnings volatility

Customer demand shifts

Electrification of transport and heating raises medium-term load as Austria consumed about 65 TWh of electricity in 2023; rising EV and heat-pump uptake increases peak and seasonal demand. Industrial decarbonization shifts demand toward green power and flexibility markets under EU Fit for 55 targets. Energy efficiency lowers consumption in some end-uses while Verbund’s product mix evolves toward tailored contracts and flexibility services.

Austrian hydro mix ≈90%; 100% renewables by 2030

Verbund is highly exposed to wholesale price swings driven by hydrology and fuel costs; hydro ≈90% of generation so dry years hit volumes and merchant revenues. ECB policy rate ~3.75% (mid‑2025) and 2024 euro‑area inflation ~2.4% raise WACC and capex. Procurement and EPC inflation plus 2023 low flows (run‑off down ~20%) increase project risk; hedging, PPAs and diversification into wind/solar mitigate volatility.

| Metric | Value |

|---|---|

| Hydro share | ≈90% |

| Austria electricity (2023) | ~65 TWh |

| ECB rate (mid‑2025) | ~3.75% |

| EU inflation (2024) | ~2.4% |

| 2023 low flows | Run‑off down ≈20% |

Full Version Awaits

Verbund PESTLE Analysis

The preview of the Verbund PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the real, professionally structured file with no placeholders or teasers. After checkout you’ll be able to download this same final document instantly.

Your Shortcut to Market Insight Starts Here

Explore how political, economic, social, technological, legal and environmental forces shape Verbund's trajectory in our concise PESTLE summary—perfect for investors and strategists. Buy the full analysis to access actionable insights, forecasts and ready-to-use slides for smarter decisions.

Political factors

EU Green Deal alignment

Verbund benefits directly from the EU Green Deal and Fit for 55 framework targeting at least 55% GHG cuts by 2030 and climate neutrality by 2050, which prioritizes renewables and grid expansion. Access to EU funding programmes such as the €723.8bn Recovery and Resilience Facility and the €5.84bn Connecting Europe Facility can lower project costs and de-risk large investments. Stable EU policy enables multi-decade planning, while any delays in permitting or EU rulemaking could slow project pipelines and compress near-term cash flows.

Austrian energy policy support

Austrian energy policy prioritizes hydropower optimization, wind/solar build‑out and storage, aligning with VERBUND’s core (hydro accounts for ≈90% of its generation). The Republic holds about 51% of VERBUND, aligning state interests with security of supply and price stability. Austria targets 100% renewable electricity by 2030, and domestic incentives can speed hydro modernization. Political shifts could recalibrate subsidies or tariff regimes, impacting returns.

Market design and price caps

EU electricity market design reform adopted in 2023 reshapes revenue models for generators and storage, and several member states applied temporary windfall taxes or price caps in 2022–24 that compressed margins during high-price episodes. Capacity, flexibility and ancillary-services mechanisms implemented at national level can create incremental revenue streams. Regulatory clarity is crucial to secure financing for Verbund’s large capex in hydropower and renewables.

Cross-border integration

ENTSO-E's interconnector policies and coordinated market rules (ENTSO-E comprises 42 TSOs across 36 countries) increase cross-border trading and system balancing, while favorable allocation rules and congestion income can materially support earnings for grid owners. Geopolitical shocks — for example the Nord Stream pipeline halt since September 2022 — have shifted gas and power flows, driving price volatility and altering dispatch economics; regional coordination changes hydropower dispatch value.

- Interconnector policy: boosts trading, balancing

- ENTSO-E: 42 TSOs / 36 countries

- Allocation & congestion income: supports earnings

- Geopolitics (Nord Stream halt Sep 2022): shifts flows, raises price volatility

- Regional coordination: changes hydropower dispatch value

Public investment and resilience

Public investment via NextGenerationEU and the Recovery and Resilience Facility (RRF, ~€700bn) plus InvestEU can catalyze grids, storage and hydro refurbishment projects; political prioritization of resilience after the 2022 energy crisis strengthens support for hydro refurbishments. Disaster-recovery frameworks affect insurance payouts and restoration timelines, while funding competition can delay allocations.

- EU RRF/NextGenerationEU: ~€700bn mobilised

- InvestEU/CEF target energy infrastructure funding

- Disaster-recovery rules shape insurance/restoration speed

Austrian hydro mix ≈90%; 100% renewables by 2030

EU Green Deal/Fit for 55 and market reform (2023) materially favor Verbund’s hydro-led mix (≈90% generation) and enable multi-decade planning, while permitting delays or windfall taxes can compress near-term cash flows. Austria owns ≈51% of Verbund and targets 100% renewables by 2030, supporting hydro modernization. EU funds (RRF ≈€723.8bn, CEF €5.84bn) and ENTSO-E coordination boost cross‑border revenues; geopolitics (Nord Stream halt Sep 2022) raises price volatility.

| Item | Key figure |

|---|---|

| Verbund hydro share | ≈90% |

| State ownership | ≈51% |

| Austria 2030 target | 100% renewables |

| RRF | ≈€723.8bn |

| CEF | €5.84bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Verbund, with data-backed, region- and industry-specific insights designed for executives and investors; each section includes detailed sub-points and forward-looking analysis ready for plans, decks, or reports.

A concise, visually segmented PESTLE summary for Verbund that distills regulatory, environmental, and market risks into an easily shareable slide or note, enabling rapid alignment across teams and clearer discussion of strategic responses during planning sessions.

Economic factors

Power price volatility

Hydrology and fuel-price movements drive wholesale power swings—prices have spiked to several hundred EUR/MWh in stress periods—directly affecting VERBUND’s merchant revenues. Merchant exposure can boost returns in tight markets but increases earnings volatility. Active hedging and PPAs stabilize cash flows while capping upside. Price volatility also dictates investment timing and the balance between flexible hydro and long-term contracted assets.

Interest rates and capex

Higher interest rates — with the ECB policy rate near 3.75% in mid‑2025 — have pushed WACC up several hundred basis points, squeezing IRRs for renewables and grid capex and making marginal projects less viable.

VERBUND’s investment‑grade balance sheet and low leverage help preserve market access and favorable terms, evidenced by active refinancing and green bond issuance to lock cheaper, long‑dated funding.

Normalization or cuts in rates would materially improve project economics and unlock more marginal renewables and grid investments.

Inflation and supply chains

Component and EPC costs for solar, wind and grid projects face inflationary pressure against a euro-area inflation backdrop of about 2.4% in 2024, raising project budgets and contingency needs. Indexation clauses in PPAs and regulated tariffs partially offset cost drift. Logistics bottlenecks and commodity price swings disrupt delivery schedules. Supplier diversification and framework contracts reduce procurement and timing risk.

Hydrology-driven output

Verbund's earnings are highly sensitive to precipitation, snowpack and river flows; hydropower comprises roughly 90% of its generation, so dry years compress volumes and ancillary-service revenue while wet years boost low-cost output and margins. The 2023 European low-flow episode reduced run-off in parts of the Alps by up to 20%, highlighting volatility; expanding wind and solar smooths this variability.

- Hydrology sensitivity: ~90% hydro

- 2023 low flows: up to 20% run-off drop

- Drought impact: lower volumes and ancillary revenues

- Diversification: wind/solar reduce earnings volatility

Customer demand shifts

Electrification of transport and heating raises medium-term load as Austria consumed about 65 TWh of electricity in 2023; rising EV and heat-pump uptake increases peak and seasonal demand. Industrial decarbonization shifts demand toward green power and flexibility markets under EU Fit for 55 targets. Energy efficiency lowers consumption in some end-uses while Verbund’s product mix evolves toward tailored contracts and flexibility services.

Austrian hydro mix ≈90%; 100% renewables by 2030

Verbund is highly exposed to wholesale price swings driven by hydrology and fuel costs; hydro ≈90% of generation so dry years hit volumes and merchant revenues. ECB policy rate ~3.75% (mid‑2025) and 2024 euro‑area inflation ~2.4% raise WACC and capex. Procurement and EPC inflation plus 2023 low flows (run‑off down ~20%) increase project risk; hedging, PPAs and diversification into wind/solar mitigate volatility.

| Metric | Value |

|---|---|

| Hydro share | ≈90% |

| Austria electricity (2023) | ~65 TWh |

| ECB rate (mid‑2025) | ~3.75% |

| EU inflation (2024) | ~2.4% |

| 2023 low flows | Run‑off down ≈20% |

Full Version Awaits

Verbund PESTLE Analysis

The preview of the Verbund PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the real, professionally structured file with no placeholders or teasers. After checkout you’ll be able to download this same final document instantly.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Explore how political, economic, social, technological, legal and environmental forces shape Verbund's trajectory in our concise PESTLE summary—perfect for investors and strategists. Buy the full analysis to access actionable insights, forecasts and ready-to-use slides for smarter decisions.

Political factors

EU Green Deal alignment

Verbund benefits directly from the EU Green Deal and Fit for 55 framework targeting at least 55% GHG cuts by 2030 and climate neutrality by 2050, which prioritizes renewables and grid expansion. Access to EU funding programmes such as the €723.8bn Recovery and Resilience Facility and the €5.84bn Connecting Europe Facility can lower project costs and de-risk large investments. Stable EU policy enables multi-decade planning, while any delays in permitting or EU rulemaking could slow project pipelines and compress near-term cash flows.

Austrian energy policy support

Austrian energy policy prioritizes hydropower optimization, wind/solar build‑out and storage, aligning with VERBUND’s core (hydro accounts for ≈90% of its generation). The Republic holds about 51% of VERBUND, aligning state interests with security of supply and price stability. Austria targets 100% renewable electricity by 2030, and domestic incentives can speed hydro modernization. Political shifts could recalibrate subsidies or tariff regimes, impacting returns.

Market design and price caps

EU electricity market design reform adopted in 2023 reshapes revenue models for generators and storage, and several member states applied temporary windfall taxes or price caps in 2022–24 that compressed margins during high-price episodes. Capacity, flexibility and ancillary-services mechanisms implemented at national level can create incremental revenue streams. Regulatory clarity is crucial to secure financing for Verbund’s large capex in hydropower and renewables.

Cross-border integration

ENTSO-E's interconnector policies and coordinated market rules (ENTSO-E comprises 42 TSOs across 36 countries) increase cross-border trading and system balancing, while favorable allocation rules and congestion income can materially support earnings for grid owners. Geopolitical shocks — for example the Nord Stream pipeline halt since September 2022 — have shifted gas and power flows, driving price volatility and altering dispatch economics; regional coordination changes hydropower dispatch value.

- Interconnector policy: boosts trading, balancing

- ENTSO-E: 42 TSOs / 36 countries

- Allocation & congestion income: supports earnings

- Geopolitics (Nord Stream halt Sep 2022): shifts flows, raises price volatility

- Regional coordination: changes hydropower dispatch value

Public investment and resilience

Public investment via NextGenerationEU and the Recovery and Resilience Facility (RRF, ~€700bn) plus InvestEU can catalyze grids, storage and hydro refurbishment projects; political prioritization of resilience after the 2022 energy crisis strengthens support for hydro refurbishments. Disaster-recovery frameworks affect insurance payouts and restoration timelines, while funding competition can delay allocations.

- EU RRF/NextGenerationEU: ~€700bn mobilised

- InvestEU/CEF target energy infrastructure funding

- Disaster-recovery rules shape insurance/restoration speed

Austrian hydro mix ≈90%; 100% renewables by 2030

EU Green Deal/Fit for 55 and market reform (2023) materially favor Verbund’s hydro-led mix (≈90% generation) and enable multi-decade planning, while permitting delays or windfall taxes can compress near-term cash flows. Austria owns ≈51% of Verbund and targets 100% renewables by 2030, supporting hydro modernization. EU funds (RRF ≈€723.8bn, CEF €5.84bn) and ENTSO-E coordination boost cross‑border revenues; geopolitics (Nord Stream halt Sep 2022) raises price volatility.

| Item | Key figure |

|---|---|

| Verbund hydro share | ≈90% |

| State ownership | ≈51% |

| Austria 2030 target | 100% renewables |

| RRF | ≈€723.8bn |

| CEF | €5.84bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Verbund, with data-backed, region- and industry-specific insights designed for executives and investors; each section includes detailed sub-points and forward-looking analysis ready for plans, decks, or reports.

A concise, visually segmented PESTLE summary for Verbund that distills regulatory, environmental, and market risks into an easily shareable slide or note, enabling rapid alignment across teams and clearer discussion of strategic responses during planning sessions.

Economic factors

Power price volatility

Hydrology and fuel-price movements drive wholesale power swings—prices have spiked to several hundred EUR/MWh in stress periods—directly affecting VERBUND’s merchant revenues. Merchant exposure can boost returns in tight markets but increases earnings volatility. Active hedging and PPAs stabilize cash flows while capping upside. Price volatility also dictates investment timing and the balance between flexible hydro and long-term contracted assets.

Interest rates and capex

Higher interest rates — with the ECB policy rate near 3.75% in mid‑2025 — have pushed WACC up several hundred basis points, squeezing IRRs for renewables and grid capex and making marginal projects less viable.

VERBUND’s investment‑grade balance sheet and low leverage help preserve market access and favorable terms, evidenced by active refinancing and green bond issuance to lock cheaper, long‑dated funding.

Normalization or cuts in rates would materially improve project economics and unlock more marginal renewables and grid investments.

Inflation and supply chains

Component and EPC costs for solar, wind and grid projects face inflationary pressure against a euro-area inflation backdrop of about 2.4% in 2024, raising project budgets and contingency needs. Indexation clauses in PPAs and regulated tariffs partially offset cost drift. Logistics bottlenecks and commodity price swings disrupt delivery schedules. Supplier diversification and framework contracts reduce procurement and timing risk.

Hydrology-driven output

Verbund's earnings are highly sensitive to precipitation, snowpack and river flows; hydropower comprises roughly 90% of its generation, so dry years compress volumes and ancillary-service revenue while wet years boost low-cost output and margins. The 2023 European low-flow episode reduced run-off in parts of the Alps by up to 20%, highlighting volatility; expanding wind and solar smooths this variability.

- Hydrology sensitivity: ~90% hydro

- 2023 low flows: up to 20% run-off drop

- Drought impact: lower volumes and ancillary revenues

- Diversification: wind/solar reduce earnings volatility

Customer demand shifts

Electrification of transport and heating raises medium-term load as Austria consumed about 65 TWh of electricity in 2023; rising EV and heat-pump uptake increases peak and seasonal demand. Industrial decarbonization shifts demand toward green power and flexibility markets under EU Fit for 55 targets. Energy efficiency lowers consumption in some end-uses while Verbund’s product mix evolves toward tailored contracts and flexibility services.

Austrian hydro mix ≈90%; 100% renewables by 2030

Verbund is highly exposed to wholesale price swings driven by hydrology and fuel costs; hydro ≈90% of generation so dry years hit volumes and merchant revenues. ECB policy rate ~3.75% (mid‑2025) and 2024 euro‑area inflation ~2.4% raise WACC and capex. Procurement and EPC inflation plus 2023 low flows (run‑off down ~20%) increase project risk; hedging, PPAs and diversification into wind/solar mitigate volatility.

| Metric | Value |

|---|---|

| Hydro share | ≈90% |

| Austria electricity (2023) | ~65 TWh |

| ECB rate (mid‑2025) | ~3.75% |

| EU inflation (2024) | ~2.4% |

| 2023 low flows | Run‑off down ≈20% |

Full Version Awaits

Verbund PESTLE Analysis

The preview of the Verbund PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is the real, professionally structured file with no placeholders or teasers. After checkout you’ll be able to download this same final document instantly.