Vertex Resource Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

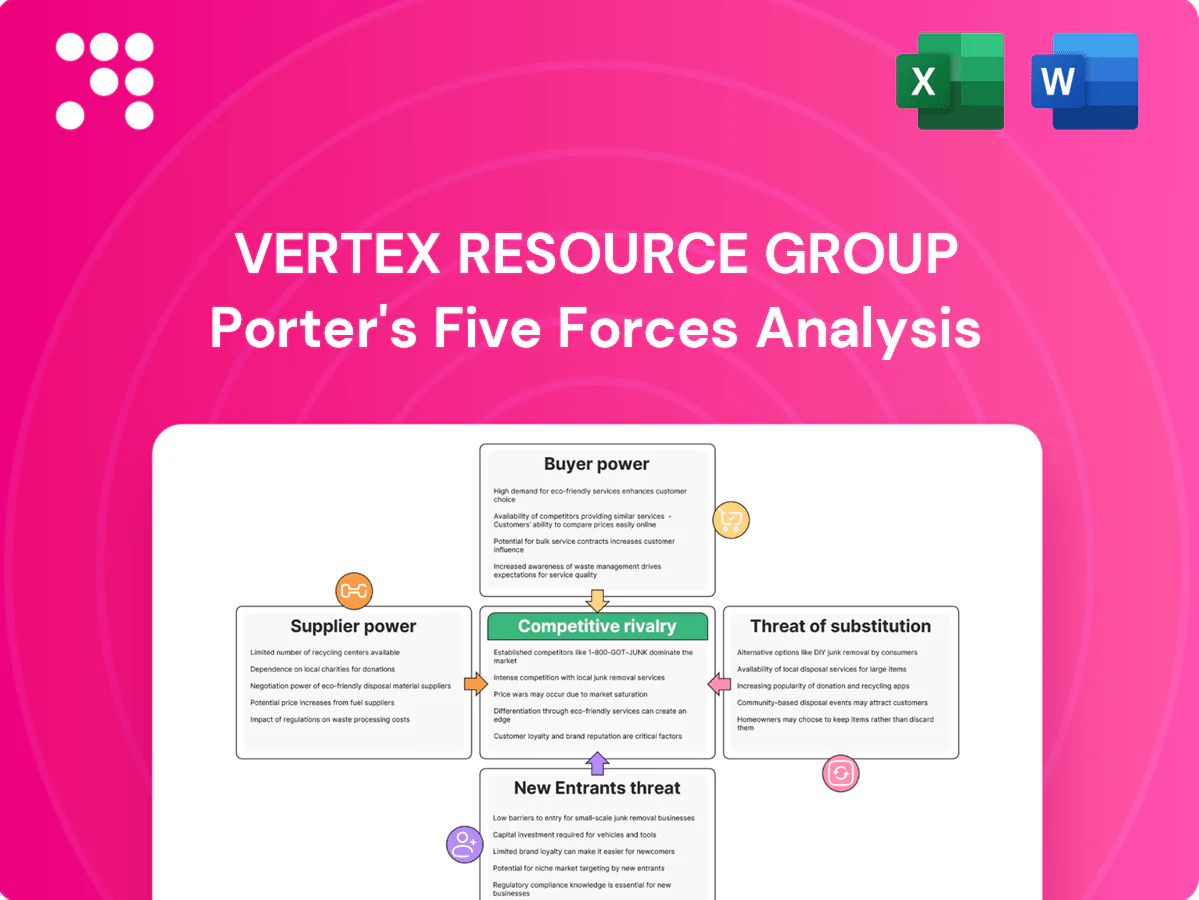

Vertex Resource Group faces moderate buyer power, evolving regulatory pressures, and meaningful barriers for new entrants, while supplier concentration and substitute threats vary by service line. This snapshot highlights competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and strategic recommendations tailored to Vertex.

Suppliers Bargaining Power

Specialized equipment vendors

Vertex depends on niche gear—mobile water treatment units, sampling instruments, drones and heavy earthmoving—so suppliers with proprietary tech or certifications can extract favorable terms, especially as the commercial drone market reached about $27.4B in 2024. Multi-sourcing and standardization of interfaces reduce that supplier leverage. Long-term OEM service bundles and multi-year purchase agreements help stabilize maintenance and capex costs.

Skilled labor and certifications

Certified technicians, environmental scientists, and safety-qualified field crews are scarce during peak cycles, giving labor supplier-like power; industry reports showed retention bonuses rose about 15% in 2024 and skilled-hire lead times extended by several months. Training, accreditations, and strong safety records further strengthen bargaining positions, pressuring margins through wage inflation. Apprenticeships and internal training pipelines have reduced external dependency for many firms.

Chemicals, consumables, and media

Remediation chemicals, absorbents, filter media and PPE are core inputs for Vertex’s services; commodity feedstock volatility has caused input cost swings exceeding 20% in some chemical segments during 2023–24, while regulated approved-product lists constrain supplier switching; aggregated purchasing and inventory planning across projects has been shown in industry benchmarks to cut realized cost volatility roughly 10–15%.

Data, software, and lab services

Environmental labs, GIS, and compliance platforms are core to Vertex deliverables, with ISO/IEC 17025 remaining the primary accreditation for testing labs in 2024, concentrating power among accredited providers. Turnaround-time SLAs create pricing and service premiums and raise switching costs as integrated data pipelines lock in clients. API-enabled tools and dual-sourcing labs are primary mitigants of supplier risk.

Subcontractors and specialty trades

Projects routinely rely on drilling, hydrovac, waste hauling and civil works subcontractors, and local capacity constraints at remote sites can push sub rates up 15–25% in 2024, increasing supplier leverage; Vertex mitigates this with prequalified networks and frame rates to stabilize pricing. Performance KPIs and disciplined workload allocation enforce accountability and limit pass-through cost inflation.

- Prequalified networks: reduce spot-price volatility

- Frame rates: target 5–10% cost control

- KPIs: uptime, safety, on‑time delivery

- Workload allocation: preserves capacity balance

Drone services face supplier pricing, labor squeeze and chemical volatility; multi-sourcing helps

Vertex faces concentrated supplier power from proprietary equipment (commercial drone market $27.4B in 2024), scarce certified crews (retention bonuses +15% in 2024) and volatile chemical inputs (>20% swings 2023–24); accredited labs (ISO/IEC 17025) and SLA lock‑in raise switching costs; mitigants: multi‑sourcing, long‑term OEMs, prequalified subcontractor networks and internal training.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Drones/equipment | $27.4B market | High pricing leverage |

| Labor | Retention +15% | Wage inflation |

| Chemicals | >20% volatility | Cost swings |

What is included in the product

Tailored Porter's Five Forces analysis for Vertex Resource Group uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic levers that influence pricing, margins, and market resilience.

A concise Porter's Five Forces one-sheet for Vertex Resource Group that highlights supplier/buyer power, competitive rivalry, substitutes and entry threats—instantly pinpointing strategic pain points and prioritized mitigation actions. Ready to drop into decks, customize with live data, and accelerate decision-making across leadership and investor meetings.

Customers Bargaining Power

Large O&G and utilities dominance

Enterprise O&G and utility clients pool procurement, enforce strict multi‑year, multi‑million‑dollar MSAs and push hard on price and contractual terms, leveraging volume to secure rate concessions. The scale of their spend can materially influence win rates, yet complex work scopes, stringent safety and regulatory requirements limit pure price competition. Deep operational relationships and documented past performance with Vertex materially soften customer bargaining power.

Competitive tendering dynamics

RFPs and panel frameworks force head-to-head pricing for Vertex, making transparent scoring weigh fees alongside safety and ESG metrics. Incumbency raises renewal odds but does not secure contracts when scoring favors cost or sustainability performance. Demonstrable differentiated capabilities and bundled service offers raise win probability and allow margin preservation without deep discounting.

Switching costs and continuity

Site history, data continuity and regulator familiarity create high switching costs for Vertex clients, since mid-project transitions often risk permitting and compliance delays. Buyers therefore weigh continuity and regulatory certainty against potential price savings. Documented methodologies and data portability provisions help lower perceived lock-in by enabling smoother handovers.

Regulatory and ESG expectations

Buyers demand demonstrable compliance, emissions tracking and Indigenous engagement; failure to meet EU CSRD requirements (phased from 2024, covering ~50,000 companies) or equivalent procurement rules risks disqualification or price pressure. Vendors meeting advanced ESG criteria can justify premiums; transparent, verified reporting and third-party metrics materially elevate contract value.

- Compliance: CSRD 2024 scope ~50,000 firms

- Emissions: verified tracking required

- Indigenous: documented engagement mandated

- Value: verified ESG → premium pricing

Payment terms and risk transfer

Bargaining power of customers on payment terms forces Vertex Resource Group into extended terms, holdbacks and indemnities that shift risk to the contractor and strain cash flow for field-heavy projects; milestone billing and mobilization fees are increasingly used to rebalance that risk. A strong safety record and low incident rates reduce customers' demand for onerous contingencies and improve negotiating leverage for Vertex.

- Extended terms

- Holdbacks & indemnities

- Milestone billing & mobilization fees

- Safety record reduces contingencies

Enterprise buyers extract concessions in multi‑million MSAs; CSRD, RFPs and incumbency shape pricing

Enterprise buyers wield strong leverage via multi‑year, multi‑million‑dollar MSAs, pressing price and contractual terms, while complex scopes, safety and regulatory needs limit pure price competition. RFPs/panels force transparent scoring; incumbency, ESG and documented performance raise switching costs and enable premium pricing. CSRD (2024) covers ~50,000 firms, increasing ESG-driven selection and contract risk.

| Metric | Value |

|---|---|

| Contract size | Multi‑million‑dollar MSAs |

| Procurement leverage | High — volume buyers enforce RFPs/panels |

| ESG regulation | CSRD scope ~50,000 firms (2024) |

| Payment terms | Extended terms, holdbacks common |

Full Version Awaits

Vertex Resource Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Vertex Resource Group you'll receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download upon purchase. Use it as-is for decision-making or reporting.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Vertex Resource Group faces moderate buyer power, evolving regulatory pressures, and meaningful barriers for new entrants, while supplier concentration and substitute threats vary by service line. This snapshot highlights competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and strategic recommendations tailored to Vertex.

Suppliers Bargaining Power

Specialized equipment vendors

Vertex depends on niche gear—mobile water treatment units, sampling instruments, drones and heavy earthmoving—so suppliers with proprietary tech or certifications can extract favorable terms, especially as the commercial drone market reached about $27.4B in 2024. Multi-sourcing and standardization of interfaces reduce that supplier leverage. Long-term OEM service bundles and multi-year purchase agreements help stabilize maintenance and capex costs.

Skilled labor and certifications

Certified technicians, environmental scientists, and safety-qualified field crews are scarce during peak cycles, giving labor supplier-like power; industry reports showed retention bonuses rose about 15% in 2024 and skilled-hire lead times extended by several months. Training, accreditations, and strong safety records further strengthen bargaining positions, pressuring margins through wage inflation. Apprenticeships and internal training pipelines have reduced external dependency for many firms.

Chemicals, consumables, and media

Remediation chemicals, absorbents, filter media and PPE are core inputs for Vertex’s services; commodity feedstock volatility has caused input cost swings exceeding 20% in some chemical segments during 2023–24, while regulated approved-product lists constrain supplier switching; aggregated purchasing and inventory planning across projects has been shown in industry benchmarks to cut realized cost volatility roughly 10–15%.

Data, software, and lab services

Environmental labs, GIS, and compliance platforms are core to Vertex deliverables, with ISO/IEC 17025 remaining the primary accreditation for testing labs in 2024, concentrating power among accredited providers. Turnaround-time SLAs create pricing and service premiums and raise switching costs as integrated data pipelines lock in clients. API-enabled tools and dual-sourcing labs are primary mitigants of supplier risk.

Subcontractors and specialty trades

Projects routinely rely on drilling, hydrovac, waste hauling and civil works subcontractors, and local capacity constraints at remote sites can push sub rates up 15–25% in 2024, increasing supplier leverage; Vertex mitigates this with prequalified networks and frame rates to stabilize pricing. Performance KPIs and disciplined workload allocation enforce accountability and limit pass-through cost inflation.

- Prequalified networks: reduce spot-price volatility

- Frame rates: target 5–10% cost control

- KPIs: uptime, safety, on‑time delivery

- Workload allocation: preserves capacity balance

Drone services face supplier pricing, labor squeeze and chemical volatility; multi-sourcing helps

Vertex faces concentrated supplier power from proprietary equipment (commercial drone market $27.4B in 2024), scarce certified crews (retention bonuses +15% in 2024) and volatile chemical inputs (>20% swings 2023–24); accredited labs (ISO/IEC 17025) and SLA lock‑in raise switching costs; mitigants: multi‑sourcing, long‑term OEMs, prequalified subcontractor networks and internal training.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Drones/equipment | $27.4B market | High pricing leverage |

| Labor | Retention +15% | Wage inflation |

| Chemicals | >20% volatility | Cost swings |

What is included in the product

Tailored Porter's Five Forces analysis for Vertex Resource Group uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic levers that influence pricing, margins, and market resilience.

A concise Porter's Five Forces one-sheet for Vertex Resource Group that highlights supplier/buyer power, competitive rivalry, substitutes and entry threats—instantly pinpointing strategic pain points and prioritized mitigation actions. Ready to drop into decks, customize with live data, and accelerate decision-making across leadership and investor meetings.

Customers Bargaining Power

Large O&G and utilities dominance

Enterprise O&G and utility clients pool procurement, enforce strict multi‑year, multi‑million‑dollar MSAs and push hard on price and contractual terms, leveraging volume to secure rate concessions. The scale of their spend can materially influence win rates, yet complex work scopes, stringent safety and regulatory requirements limit pure price competition. Deep operational relationships and documented past performance with Vertex materially soften customer bargaining power.

Competitive tendering dynamics

RFPs and panel frameworks force head-to-head pricing for Vertex, making transparent scoring weigh fees alongside safety and ESG metrics. Incumbency raises renewal odds but does not secure contracts when scoring favors cost or sustainability performance. Demonstrable differentiated capabilities and bundled service offers raise win probability and allow margin preservation without deep discounting.

Switching costs and continuity

Site history, data continuity and regulator familiarity create high switching costs for Vertex clients, since mid-project transitions often risk permitting and compliance delays. Buyers therefore weigh continuity and regulatory certainty against potential price savings. Documented methodologies and data portability provisions help lower perceived lock-in by enabling smoother handovers.

Regulatory and ESG expectations

Buyers demand demonstrable compliance, emissions tracking and Indigenous engagement; failure to meet EU CSRD requirements (phased from 2024, covering ~50,000 companies) or equivalent procurement rules risks disqualification or price pressure. Vendors meeting advanced ESG criteria can justify premiums; transparent, verified reporting and third-party metrics materially elevate contract value.

- Compliance: CSRD 2024 scope ~50,000 firms

- Emissions: verified tracking required

- Indigenous: documented engagement mandated

- Value: verified ESG → premium pricing

Payment terms and risk transfer

Bargaining power of customers on payment terms forces Vertex Resource Group into extended terms, holdbacks and indemnities that shift risk to the contractor and strain cash flow for field-heavy projects; milestone billing and mobilization fees are increasingly used to rebalance that risk. A strong safety record and low incident rates reduce customers' demand for onerous contingencies and improve negotiating leverage for Vertex.

- Extended terms

- Holdbacks & indemnities

- Milestone billing & mobilization fees

- Safety record reduces contingencies

Enterprise buyers extract concessions in multi‑million MSAs; CSRD, RFPs and incumbency shape pricing

Enterprise buyers wield strong leverage via multi‑year, multi‑million‑dollar MSAs, pressing price and contractual terms, while complex scopes, safety and regulatory needs limit pure price competition. RFPs/panels force transparent scoring; incumbency, ESG and documented performance raise switching costs and enable premium pricing. CSRD (2024) covers ~50,000 firms, increasing ESG-driven selection and contract risk.

| Metric | Value |

|---|---|

| Contract size | Multi‑million‑dollar MSAs |

| Procurement leverage | High — volume buyers enforce RFPs/panels |

| ESG regulation | CSRD scope ~50,000 firms (2024) |

| Payment terms | Extended terms, holdbacks common |

Full Version Awaits

Vertex Resource Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Vertex Resource Group you'll receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download upon purchase. Use it as-is for decision-making or reporting.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Vertex Resource Group faces moderate buyer power, evolving regulatory pressures, and meaningful barriers for new entrants, while supplier concentration and substitute threats vary by service line. This snapshot highlights competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to see force-by-force ratings, visuals, and strategic recommendations tailored to Vertex.

Suppliers Bargaining Power

Specialized equipment vendors

Vertex depends on niche gear—mobile water treatment units, sampling instruments, drones and heavy earthmoving—so suppliers with proprietary tech or certifications can extract favorable terms, especially as the commercial drone market reached about $27.4B in 2024. Multi-sourcing and standardization of interfaces reduce that supplier leverage. Long-term OEM service bundles and multi-year purchase agreements help stabilize maintenance and capex costs.

Skilled labor and certifications

Certified technicians, environmental scientists, and safety-qualified field crews are scarce during peak cycles, giving labor supplier-like power; industry reports showed retention bonuses rose about 15% in 2024 and skilled-hire lead times extended by several months. Training, accreditations, and strong safety records further strengthen bargaining positions, pressuring margins through wage inflation. Apprenticeships and internal training pipelines have reduced external dependency for many firms.

Chemicals, consumables, and media

Remediation chemicals, absorbents, filter media and PPE are core inputs for Vertex’s services; commodity feedstock volatility has caused input cost swings exceeding 20% in some chemical segments during 2023–24, while regulated approved-product lists constrain supplier switching; aggregated purchasing and inventory planning across projects has been shown in industry benchmarks to cut realized cost volatility roughly 10–15%.

Data, software, and lab services

Environmental labs, GIS, and compliance platforms are core to Vertex deliverables, with ISO/IEC 17025 remaining the primary accreditation for testing labs in 2024, concentrating power among accredited providers. Turnaround-time SLAs create pricing and service premiums and raise switching costs as integrated data pipelines lock in clients. API-enabled tools and dual-sourcing labs are primary mitigants of supplier risk.

Subcontractors and specialty trades

Projects routinely rely on drilling, hydrovac, waste hauling and civil works subcontractors, and local capacity constraints at remote sites can push sub rates up 15–25% in 2024, increasing supplier leverage; Vertex mitigates this with prequalified networks and frame rates to stabilize pricing. Performance KPIs and disciplined workload allocation enforce accountability and limit pass-through cost inflation.

- Prequalified networks: reduce spot-price volatility

- Frame rates: target 5–10% cost control

- KPIs: uptime, safety, on‑time delivery

- Workload allocation: preserves capacity balance

Drone services face supplier pricing, labor squeeze and chemical volatility; multi-sourcing helps

Vertex faces concentrated supplier power from proprietary equipment (commercial drone market $27.4B in 2024), scarce certified crews (retention bonuses +15% in 2024) and volatile chemical inputs (>20% swings 2023–24); accredited labs (ISO/IEC 17025) and SLA lock‑in raise switching costs; mitigants: multi‑sourcing, long‑term OEMs, prequalified subcontractor networks and internal training.

| Factor | 2024 Metric | Impact |

|---|---|---|

| Drones/equipment | $27.4B market | High pricing leverage |

| Labor | Retention +15% | Wage inflation |

| Chemicals | >20% volatility | Cost swings |

What is included in the product

Tailored Porter's Five Forces analysis for Vertex Resource Group uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic levers that influence pricing, margins, and market resilience.

A concise Porter's Five Forces one-sheet for Vertex Resource Group that highlights supplier/buyer power, competitive rivalry, substitutes and entry threats—instantly pinpointing strategic pain points and prioritized mitigation actions. Ready to drop into decks, customize with live data, and accelerate decision-making across leadership and investor meetings.

Customers Bargaining Power

Large O&G and utilities dominance

Enterprise O&G and utility clients pool procurement, enforce strict multi‑year, multi‑million‑dollar MSAs and push hard on price and contractual terms, leveraging volume to secure rate concessions. The scale of their spend can materially influence win rates, yet complex work scopes, stringent safety and regulatory requirements limit pure price competition. Deep operational relationships and documented past performance with Vertex materially soften customer bargaining power.

Competitive tendering dynamics

RFPs and panel frameworks force head-to-head pricing for Vertex, making transparent scoring weigh fees alongside safety and ESG metrics. Incumbency raises renewal odds but does not secure contracts when scoring favors cost or sustainability performance. Demonstrable differentiated capabilities and bundled service offers raise win probability and allow margin preservation without deep discounting.

Switching costs and continuity

Site history, data continuity and regulator familiarity create high switching costs for Vertex clients, since mid-project transitions often risk permitting and compliance delays. Buyers therefore weigh continuity and regulatory certainty against potential price savings. Documented methodologies and data portability provisions help lower perceived lock-in by enabling smoother handovers.

Regulatory and ESG expectations

Buyers demand demonstrable compliance, emissions tracking and Indigenous engagement; failure to meet EU CSRD requirements (phased from 2024, covering ~50,000 companies) or equivalent procurement rules risks disqualification or price pressure. Vendors meeting advanced ESG criteria can justify premiums; transparent, verified reporting and third-party metrics materially elevate contract value.

- Compliance: CSRD 2024 scope ~50,000 firms

- Emissions: verified tracking required

- Indigenous: documented engagement mandated

- Value: verified ESG → premium pricing

Payment terms and risk transfer

Bargaining power of customers on payment terms forces Vertex Resource Group into extended terms, holdbacks and indemnities that shift risk to the contractor and strain cash flow for field-heavy projects; milestone billing and mobilization fees are increasingly used to rebalance that risk. A strong safety record and low incident rates reduce customers' demand for onerous contingencies and improve negotiating leverage for Vertex.

- Extended terms

- Holdbacks & indemnities

- Milestone billing & mobilization fees

- Safety record reduces contingencies

Enterprise buyers extract concessions in multi‑million MSAs; CSRD, RFPs and incumbency shape pricing

Enterprise buyers wield strong leverage via multi‑year, multi‑million‑dollar MSAs, pressing price and contractual terms, while complex scopes, safety and regulatory needs limit pure price competition. RFPs/panels force transparent scoring; incumbency, ESG and documented performance raise switching costs and enable premium pricing. CSRD (2024) covers ~50,000 firms, increasing ESG-driven selection and contract risk.

| Metric | Value |

|---|---|

| Contract size | Multi‑million‑dollar MSAs |

| Procurement leverage | High — volume buyers enforce RFPs/panels |

| ESG regulation | CSRD scope ~50,000 firms (2024) |

| Payment terms | Extended terms, holdbacks common |

Full Version Awaits

Vertex Resource Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Vertex Resource Group you'll receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download upon purchase. Use it as-is for decision-making or reporting.