Via Location SA Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Via Location SA faces moderate supplier power, rising buyer expectations, and niche competitive rivalry driven by specialized location services and tech differentiation. Substitute threats and regulatory shifts shape margin pressure while scale advantages favor established players. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Via Location SA.

Suppliers Bargaining Power

Concentrated OEM vehicle base

Industrial/commercial vehicle supply is concentrated among a few OEMs (Renault Trucks, Mercedes-Benz, MAN, Iveco), with the top OEMs accounting for roughly 80% of the EU commercial vehicle market in 2024, creating moderate supplier leverage. Model availability and allocation can tighten in cyclical upswings, pressuring discounts and delivery times. Via Location mitigates this via multi-brand sourcing and staggered orders. Long-term relationships and volume commitments secure better terms.

Dependence on parts and maintenance networks

In 2024 aftermarket parts, tires and authorized service centers remain critical to meeting uptime SLAs, with major suppliers such as Michelin, Bridgestone and Goodyear driving pricing dynamics for specialized vehicles.

Authorized workshops and OEM tire dominance increase supplier bargaining power, while framework contracts and predictive maintenance programs demonstrably cut unplanned spend and downtime.

Geographic spread of parts and service partners is essential to avoid bottlenecks across wide-route operations and seasonal demand peaks.

Energy and emerging tech suppliers

Diesel suppliers remain low-differentiation but 2024 saw heightened price volatility tied to oil-market swings, increasing operating cost risk for fleets. Electricity and public charging providers introduce new dependencies as grid and roaming tariffs affect total cost of ownership. Telematics and FMS vendors frequently create switching costs via deep integrations—many platforms advertise 100+ third-party connections. Via Location can defend bargaining power through interoperable platforms, multi-utility contracts and co-investments in charging to dilute single-supplier exposure.

Financial capital providers

Via Location SA is capital-intensive, depending on banks, lessors and ABS markets; with the US federal funds rate at 5.25–5.50% at end‑2024 interest cycles materially shift fleet economics and give lenders leverage via covenants. Diversifying funding sources and laddering tenor reduces refinancing and rate shock exposure, while disciplined residual value management improves lease coverage and secures better financing terms.

- Funding mix: banks, lessors, ABS

- Rate risk: fed funds 5.25–5.50% (end‑2024)

- Mitigants: tenor laddering, diversification, residual value control

Bodybuilders and customization partners

- Specialized suppliers: limited capacity

- Lead times 12–20 weeks (2024)

- Standardize modules to regain leverage

- Dual‑source critical builds

OEMs hold ~80% EU share; fleet operators cut exposure via multi-brand sourcing, modular builds

Supplier power is moderate: top OEMs hold ~80% EU market (2024), aftermarket leaders set parts/tyre pricing, and specialized bodybuilders show 12–20 week lead times. Fuel price volatility and fed funds 5.25–5.50% (end‑2024) raise operating and financing risk. Via Location reduces exposure via multi‑brand sourcing, modular builds, dual‑sourcing and financing diversification.

| Metric | 2024 value |

|---|---|

| Top OEM market share | ~80% |

| Bodybuilder lead times | 12–20 wks |

| Fed funds | 5.25–5.50% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively to Via Location SA, identifying disruptive forces and substitutes that threaten market share. Evaluates supplier and buyer power, pricing influence, and barriers that deter new entrants to guide strategic decisions and investor materials.

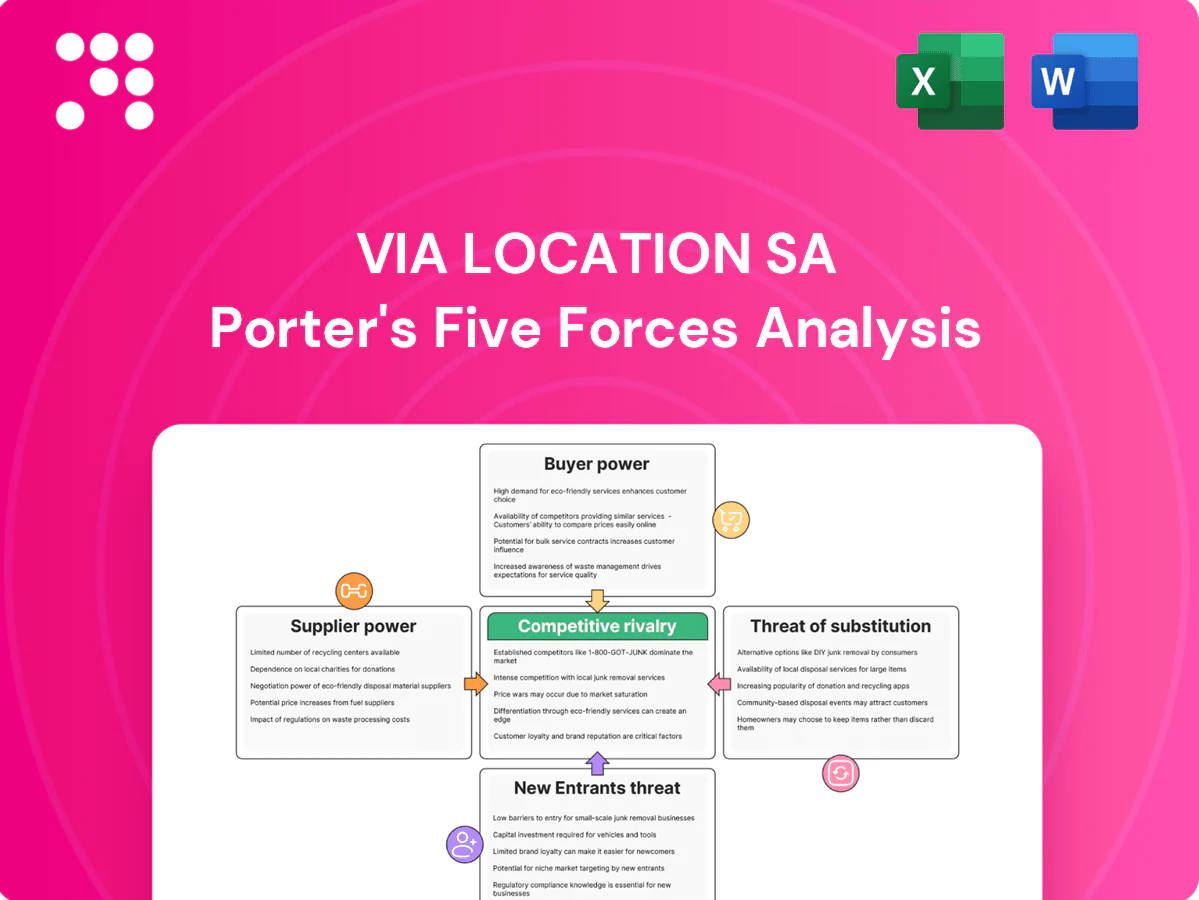

Clear, one-sheet Porter's Five Forces for Via Location SA—visualize competitor, supplier, buyer, substitute, and entrant pressures to reduce analysis time and simplify strategic decisions for boards and investors.

Customers Bargaining Power

Large B2B clients with RFPs

Large B2B clients—logistics firms, retail chains and industrials—routinely buy via competitive RFPs, with the global 3PL market ~1.1 trillion USD in 2024 intensifying scale-driven price pressure and multi-year volume demands. Their bargaining power forces service-level and price concessions, so Via Location must differentiate on uptime, operational flexibility and rigorous TCO analytics. Multi-site support and explicit KPI guarantees help defend margins.

High price transparency and TCO focus

Clients benchmark monthly rates, maintenance and residual assumptions across 3–5 providers, using visible fuel, tires and downtime data—fuel often represents about 30% of operating cost—sharpening negotiation leverage. TCO dashboards and performance-linked pricing align incentives by tying fees to utilization and uptime. Bundled value-adds such as telematics and managed maintenance shift focus from pure price to net TCO.

Moderate switching costs

Contracts are multi-year (commonly 3–5 years) yet fleets can be transitioned at term with adequate planning; custom builds and telematics integrations raise technical and operational switching costs, often extending migration timelines. Excellent service and flexible upgrade paths increase customer stickiness, while early-termination fees provide a contractual deterrent to churn.

Demand cyclicality and seasonality

Demand cyclicality and seasonality drive client bargaining: economic downturns shrink fleet needs and increase renegotiation leverage—IMF projected global growth 3.0% for 2024, signaling softer demand. Seasonal peaks force short-term flex solutions; Via Location can deploy mixed terms (core + flex) to capture upside while protecting base pricing. Tight utilization management is essential to preserve margin stability.

- Renegotiation leverage in downturns

- Seasonal peaks require short-term flex

- Mixed terms (core + flex) to protect base pricing

- Utilization management key to margin stability

Sector-specific requirements

Sector-specific needs—cold-chain, ADR and last-mile eLCV—force detailed, tailored specs; with the global cold-chain market ~USD 290 billion in 2024, buyers routinely use customization requests to extract price and service concessions. Via Location’s catalog of pre‑engineered configurations shortens lead times and caps bespoke cost creep, while ADR and compliance expertise reduces clients’ operational risk and strengthens Via’s negotiating position.

- Tailored specs enable buyer leverage

- Catalog limits bespoke cost growth

- Compliance expertise = reduced client risk

- Cold‑chain market ~USD 290bn (2024)

B2B 3PL $1.1T: uptime, TCO tools, flex core+spot terms defend margins

Large B2B clients (global 3PL ~1.1 trillion USD in 2024) exert strong price and SLA pressure, leveraging monthly benchmarked TCO (fuel ~30% of Opex) and 3–5 year contracts to drive concessions. Via Location defends margins with uptime guarantees, TCO dashboards, pre‑engineered configs and flex core+spot terms to manage seasonality and downturn renegotiation.

| Metric | 2024 Value |

|---|---|

| Global 3PL market | ~1.1 trillion USD |

| Fuel share of Opex | ~30% |

| Cold‑chain market | ~290 billion USD |

Full Version Awaits

Via Location SA Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Via Location SA you’ll receive immediately after purchase, containing the full, professionally formatted assessment with no placeholders. It’s the final document—ready for download and use the moment you buy, comprehensive and complete.

Go Beyond the Preview—Access the Full Strategic Report

Via Location SA faces moderate supplier power, rising buyer expectations, and niche competitive rivalry driven by specialized location services and tech differentiation. Substitute threats and regulatory shifts shape margin pressure while scale advantages favor established players. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Via Location SA.

Suppliers Bargaining Power

Concentrated OEM vehicle base

Industrial/commercial vehicle supply is concentrated among a few OEMs (Renault Trucks, Mercedes-Benz, MAN, Iveco), with the top OEMs accounting for roughly 80% of the EU commercial vehicle market in 2024, creating moderate supplier leverage. Model availability and allocation can tighten in cyclical upswings, pressuring discounts and delivery times. Via Location mitigates this via multi-brand sourcing and staggered orders. Long-term relationships and volume commitments secure better terms.

Dependence on parts and maintenance networks

In 2024 aftermarket parts, tires and authorized service centers remain critical to meeting uptime SLAs, with major suppliers such as Michelin, Bridgestone and Goodyear driving pricing dynamics for specialized vehicles.

Authorized workshops and OEM tire dominance increase supplier bargaining power, while framework contracts and predictive maintenance programs demonstrably cut unplanned spend and downtime.

Geographic spread of parts and service partners is essential to avoid bottlenecks across wide-route operations and seasonal demand peaks.

Energy and emerging tech suppliers

Diesel suppliers remain low-differentiation but 2024 saw heightened price volatility tied to oil-market swings, increasing operating cost risk for fleets. Electricity and public charging providers introduce new dependencies as grid and roaming tariffs affect total cost of ownership. Telematics and FMS vendors frequently create switching costs via deep integrations—many platforms advertise 100+ third-party connections. Via Location can defend bargaining power through interoperable platforms, multi-utility contracts and co-investments in charging to dilute single-supplier exposure.

Financial capital providers

Via Location SA is capital-intensive, depending on banks, lessors and ABS markets; with the US federal funds rate at 5.25–5.50% at end‑2024 interest cycles materially shift fleet economics and give lenders leverage via covenants. Diversifying funding sources and laddering tenor reduces refinancing and rate shock exposure, while disciplined residual value management improves lease coverage and secures better financing terms.

- Funding mix: banks, lessors, ABS

- Rate risk: fed funds 5.25–5.50% (end‑2024)

- Mitigants: tenor laddering, diversification, residual value control

Bodybuilders and customization partners

- Specialized suppliers: limited capacity

- Lead times 12–20 weeks (2024)

- Standardize modules to regain leverage

- Dual‑source critical builds

OEMs hold ~80% EU share; fleet operators cut exposure via multi-brand sourcing, modular builds

Supplier power is moderate: top OEMs hold ~80% EU market (2024), aftermarket leaders set parts/tyre pricing, and specialized bodybuilders show 12–20 week lead times. Fuel price volatility and fed funds 5.25–5.50% (end‑2024) raise operating and financing risk. Via Location reduces exposure via multi‑brand sourcing, modular builds, dual‑sourcing and financing diversification.

| Metric | 2024 value |

|---|---|

| Top OEM market share | ~80% |

| Bodybuilder lead times | 12–20 wks |

| Fed funds | 5.25–5.50% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively to Via Location SA, identifying disruptive forces and substitutes that threaten market share. Evaluates supplier and buyer power, pricing influence, and barriers that deter new entrants to guide strategic decisions and investor materials.

Clear, one-sheet Porter's Five Forces for Via Location SA—visualize competitor, supplier, buyer, substitute, and entrant pressures to reduce analysis time and simplify strategic decisions for boards and investors.

Customers Bargaining Power

Large B2B clients with RFPs

Large B2B clients—logistics firms, retail chains and industrials—routinely buy via competitive RFPs, with the global 3PL market ~1.1 trillion USD in 2024 intensifying scale-driven price pressure and multi-year volume demands. Their bargaining power forces service-level and price concessions, so Via Location must differentiate on uptime, operational flexibility and rigorous TCO analytics. Multi-site support and explicit KPI guarantees help defend margins.

High price transparency and TCO focus

Clients benchmark monthly rates, maintenance and residual assumptions across 3–5 providers, using visible fuel, tires and downtime data—fuel often represents about 30% of operating cost—sharpening negotiation leverage. TCO dashboards and performance-linked pricing align incentives by tying fees to utilization and uptime. Bundled value-adds such as telematics and managed maintenance shift focus from pure price to net TCO.

Moderate switching costs

Contracts are multi-year (commonly 3–5 years) yet fleets can be transitioned at term with adequate planning; custom builds and telematics integrations raise technical and operational switching costs, often extending migration timelines. Excellent service and flexible upgrade paths increase customer stickiness, while early-termination fees provide a contractual deterrent to churn.

Demand cyclicality and seasonality

Demand cyclicality and seasonality drive client bargaining: economic downturns shrink fleet needs and increase renegotiation leverage—IMF projected global growth 3.0% for 2024, signaling softer demand. Seasonal peaks force short-term flex solutions; Via Location can deploy mixed terms (core + flex) to capture upside while protecting base pricing. Tight utilization management is essential to preserve margin stability.

- Renegotiation leverage in downturns

- Seasonal peaks require short-term flex

- Mixed terms (core + flex) to protect base pricing

- Utilization management key to margin stability

Sector-specific requirements

Sector-specific needs—cold-chain, ADR and last-mile eLCV—force detailed, tailored specs; with the global cold-chain market ~USD 290 billion in 2024, buyers routinely use customization requests to extract price and service concessions. Via Location’s catalog of pre‑engineered configurations shortens lead times and caps bespoke cost creep, while ADR and compliance expertise reduces clients’ operational risk and strengthens Via’s negotiating position.

- Tailored specs enable buyer leverage

- Catalog limits bespoke cost growth

- Compliance expertise = reduced client risk

- Cold‑chain market ~USD 290bn (2024)

B2B 3PL $1.1T: uptime, TCO tools, flex core+spot terms defend margins

Large B2B clients (global 3PL ~1.1 trillion USD in 2024) exert strong price and SLA pressure, leveraging monthly benchmarked TCO (fuel ~30% of Opex) and 3–5 year contracts to drive concessions. Via Location defends margins with uptime guarantees, TCO dashboards, pre‑engineered configs and flex core+spot terms to manage seasonality and downturn renegotiation.

| Metric | 2024 Value |

|---|---|

| Global 3PL market | ~1.1 trillion USD |

| Fuel share of Opex | ~30% |

| Cold‑chain market | ~290 billion USD |

Full Version Awaits

Via Location SA Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Via Location SA you’ll receive immediately after purchase, containing the full, professionally formatted assessment with no placeholders. It’s the final document—ready for download and use the moment you buy, comprehensive and complete.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Via Location SA faces moderate supplier power, rising buyer expectations, and niche competitive rivalry driven by specialized location services and tech differentiation. Substitute threats and regulatory shifts shape margin pressure while scale advantages favor established players. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Via Location SA.

Suppliers Bargaining Power

Concentrated OEM vehicle base

Industrial/commercial vehicle supply is concentrated among a few OEMs (Renault Trucks, Mercedes-Benz, MAN, Iveco), with the top OEMs accounting for roughly 80% of the EU commercial vehicle market in 2024, creating moderate supplier leverage. Model availability and allocation can tighten in cyclical upswings, pressuring discounts and delivery times. Via Location mitigates this via multi-brand sourcing and staggered orders. Long-term relationships and volume commitments secure better terms.

Dependence on parts and maintenance networks

In 2024 aftermarket parts, tires and authorized service centers remain critical to meeting uptime SLAs, with major suppliers such as Michelin, Bridgestone and Goodyear driving pricing dynamics for specialized vehicles.

Authorized workshops and OEM tire dominance increase supplier bargaining power, while framework contracts and predictive maintenance programs demonstrably cut unplanned spend and downtime.

Geographic spread of parts and service partners is essential to avoid bottlenecks across wide-route operations and seasonal demand peaks.

Energy and emerging tech suppliers

Diesel suppliers remain low-differentiation but 2024 saw heightened price volatility tied to oil-market swings, increasing operating cost risk for fleets. Electricity and public charging providers introduce new dependencies as grid and roaming tariffs affect total cost of ownership. Telematics and FMS vendors frequently create switching costs via deep integrations—many platforms advertise 100+ third-party connections. Via Location can defend bargaining power through interoperable platforms, multi-utility contracts and co-investments in charging to dilute single-supplier exposure.

Financial capital providers

Via Location SA is capital-intensive, depending on banks, lessors and ABS markets; with the US federal funds rate at 5.25–5.50% at end‑2024 interest cycles materially shift fleet economics and give lenders leverage via covenants. Diversifying funding sources and laddering tenor reduces refinancing and rate shock exposure, while disciplined residual value management improves lease coverage and secures better financing terms.

- Funding mix: banks, lessors, ABS

- Rate risk: fed funds 5.25–5.50% (end‑2024)

- Mitigants: tenor laddering, diversification, residual value control

Bodybuilders and customization partners

- Specialized suppliers: limited capacity

- Lead times 12–20 weeks (2024)

- Standardize modules to regain leverage

- Dual‑source critical builds

OEMs hold ~80% EU share; fleet operators cut exposure via multi-brand sourcing, modular builds

Supplier power is moderate: top OEMs hold ~80% EU market (2024), aftermarket leaders set parts/tyre pricing, and specialized bodybuilders show 12–20 week lead times. Fuel price volatility and fed funds 5.25–5.50% (end‑2024) raise operating and financing risk. Via Location reduces exposure via multi‑brand sourcing, modular builds, dual‑sourcing and financing diversification.

| Metric | 2024 value |

|---|---|

| Top OEM market share | ~80% |

| Bodybuilder lead times | 12–20 wks |

| Fed funds | 5.25–5.50% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively to Via Location SA, identifying disruptive forces and substitutes that threaten market share. Evaluates supplier and buyer power, pricing influence, and barriers that deter new entrants to guide strategic decisions and investor materials.

Clear, one-sheet Porter's Five Forces for Via Location SA—visualize competitor, supplier, buyer, substitute, and entrant pressures to reduce analysis time and simplify strategic decisions for boards and investors.

Customers Bargaining Power

Large B2B clients with RFPs

Large B2B clients—logistics firms, retail chains and industrials—routinely buy via competitive RFPs, with the global 3PL market ~1.1 trillion USD in 2024 intensifying scale-driven price pressure and multi-year volume demands. Their bargaining power forces service-level and price concessions, so Via Location must differentiate on uptime, operational flexibility and rigorous TCO analytics. Multi-site support and explicit KPI guarantees help defend margins.

High price transparency and TCO focus

Clients benchmark monthly rates, maintenance and residual assumptions across 3–5 providers, using visible fuel, tires and downtime data—fuel often represents about 30% of operating cost—sharpening negotiation leverage. TCO dashboards and performance-linked pricing align incentives by tying fees to utilization and uptime. Bundled value-adds such as telematics and managed maintenance shift focus from pure price to net TCO.

Moderate switching costs

Contracts are multi-year (commonly 3–5 years) yet fleets can be transitioned at term with adequate planning; custom builds and telematics integrations raise technical and operational switching costs, often extending migration timelines. Excellent service and flexible upgrade paths increase customer stickiness, while early-termination fees provide a contractual deterrent to churn.

Demand cyclicality and seasonality

Demand cyclicality and seasonality drive client bargaining: economic downturns shrink fleet needs and increase renegotiation leverage—IMF projected global growth 3.0% for 2024, signaling softer demand. Seasonal peaks force short-term flex solutions; Via Location can deploy mixed terms (core + flex) to capture upside while protecting base pricing. Tight utilization management is essential to preserve margin stability.

- Renegotiation leverage in downturns

- Seasonal peaks require short-term flex

- Mixed terms (core + flex) to protect base pricing

- Utilization management key to margin stability

Sector-specific requirements

Sector-specific needs—cold-chain, ADR and last-mile eLCV—force detailed, tailored specs; with the global cold-chain market ~USD 290 billion in 2024, buyers routinely use customization requests to extract price and service concessions. Via Location’s catalog of pre‑engineered configurations shortens lead times and caps bespoke cost creep, while ADR and compliance expertise reduces clients’ operational risk and strengthens Via’s negotiating position.

- Tailored specs enable buyer leverage

- Catalog limits bespoke cost growth

- Compliance expertise = reduced client risk

- Cold‑chain market ~USD 290bn (2024)

B2B 3PL $1.1T: uptime, TCO tools, flex core+spot terms defend margins

Large B2B clients (global 3PL ~1.1 trillion USD in 2024) exert strong price and SLA pressure, leveraging monthly benchmarked TCO (fuel ~30% of Opex) and 3–5 year contracts to drive concessions. Via Location defends margins with uptime guarantees, TCO dashboards, pre‑engineered configs and flex core+spot terms to manage seasonality and downturn renegotiation.

| Metric | 2024 Value |

|---|---|

| Global 3PL market | ~1.1 trillion USD |

| Fuel share of Opex | ~30% |

| Cold‑chain market | ~290 billion USD |

Full Version Awaits

Via Location SA Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Via Location SA you’ll receive immediately after purchase, containing the full, professionally formatted assessment with no placeholders. It’s the final document—ready for download and use the moment you buy, comprehensive and complete.