Village Farms PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Village Farms reveals how political regulation, economic cycles, social trends, technological innovation, environmental pressures, and legal shifts together shape its strategic outlook. This concise briefing highlights risks and opportunities investors and managers need to know. Purchase the full, downloadable report for actionable, ready-to-use insights.

Political factors

US–Canada policy alignment

Operating in both Canada and the US exposes Village Farms to differing agricultural and cannabis policies: Canada legalized recreational cannabis federally in October 2018 while US cannabis remains Schedule I at federal level, with 24 states plus DC allowing adult-use and 38 states with medical programs as of July 2025.

Cross-border export of cannabis is prohibited under US federal law, so policy divergence creates duplicate compliance and restricts supply chain integration.

Monitoring federal–provincial and federal–state interplay is critical for capacity and product-mix decisions, and consistent engagement with policymakers helps anticipate shifts that affect market access and costs.

Cannabis legalization pace

Speed and scope of legalization directly expand Village Farms’ addressable market and product formats; US legal cannabis sales reached roughly $35B in 2024 while Canadian retail sales were about C$3.1B in 2023, underscoring scale upside from liberalization. Delays or restrictive frameworks compress growth and pricing power, whereas liberalization opens new channels and margin leverage. Municipal licensing caps can be as binding as national law, and optionality across provinces and states mitigates concentration risk.

Trade and USMCA effects

USMCA, in effect since July 1, 2020, improves predictability for produce trade but expressly leaves cannabis cross-border commerce closed. Tariffs, inspections and seasonal protection measures still compress greenhouse produce margins and raise logistics costs. Any phytosanitary or port-entry policy shift can rapidly disrupt freshness-sensitive supply chains. Diversifying routes and growing near key US markets reduces exposure.

Subsidies and energy policy

Greenhouse operators like Village Farms are highly sensitive to power and heat costs driven by provincial/state energy policy; US Inflation Reduction Act offers up to a 30% investment tax credit for qualifying clean energy investments, lowering capex payback on renewables and CHP. Canada's federal carbon price rose to CAD 65/t in 2023 and is scheduled to reach CAD 170/t by 2030, shifting competitiveness versus field-grown imports and making timing of efficiency capex material.

- IR A 30% ITC for energy property

- Canada carbon price: CAD 65/t (2023) → CAD 170/t (2030)

- Energy policy can materially cut unit costs via renewables/CHP

- Policy changes risk competitiveness; proactive capex captures tailwinds

Public health priorities

Government stances on nutrition, vaping and substance use shape product rules and campaigns; 24 states plus DC allow adult‑use cannabis (2025) while 14% of US high‑schoolers reported e‑cigarette use in 2023 (CDC). Produce benefits from healthy‑eating initiatives (WHO: noncommunicable diseases = 74% of global deaths), whereas cannabis faces restrictive marketing; tighter lab testing/contaminant thresholds raise SKU and cost pressures, and alignment with public‑health narratives improves stakeholder acceptance.

Cross-border cannabis rules, carbon pricing and IRA credits reshape costs and market access

Operating in Canada and the US exposes Village Farms to divergent cannabis and agricultural rules, with Canada federally legal since 2018 and US cannabis federally illegal while 24 states plus DC allow adult use (2025). Cross‑border cannabis trade is barred, forcing duplicate compliance and blocking supply integration. Energy, carbon and subsidy policies (IRA, Canada carbon pricing) materially affect capex and unit costs. Municipal licensing and testing standards constrain market access and SKU economics.

| Item | Value |

|---|---|

| US adult‑use states | 24 + DC (2025) |

| US legal cannabis sales | $35B (2024) |

| Canada retail cannabis | C$3.1B (2023) |

| Canada carbon price | CAD65/t (2023) → CAD170/t (2030) |

| IRA energy ITC | Up to 30% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Village Farms, combining data-driven trends and region-specific regulatory context to identify risks, opportunities and forward-looking scenarios for executives, investors and strategists.

A concise PESTLE summary for Village Farms that highlights regulatory, environmental and market risks, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline strategic discussions and risk mitigation.

Economic factors

Inflation and input costs

Rising energy, fertilizer, substrate and packaging costs continue to compress margins in controlled-environment agriculture; fertilizer prices, for example, declined roughly 40% from 2022 peaks by 2024 but remain elevated vs pre‑pandemic levels. Long‑term power purchase agreements (often 10–20 years) and efficiency technologies (LEDs, HVAC optimization) help buffer volatility. Retail pass‑through is constrained by growing private‑label share (~18–20% of US grocery sales), making cost discipline and product‑mix optimization critical.

Consumer spending cycles

Produce demand remains relatively resilient—industry produce volumes rose about 3% YoY in 2023—while premium cannabis and high-end produce tiers saw discretionary spend swings of roughly 10–15% in downturns. Recessions shift consumer preference to value SKUs and larger pack sizes, increasing their share by ~8–12%. Retailer bargaining strengthens in weak markets, often extracting 5–10% price concessions; flexible promotion planning helps preserve volume.

FX CAD–USD exposure

Cross-border revenues and costs expose Village Farms to CAD–USD translation and transaction risk; a 1% CAD move can meaningfully change reported USD margins. A weaker CAD (around 0.73 USD in mid-2025) aids Canadian exports but raises the cost of imported inputs and capital. Hedging programs and natural operational offsets are used to reduce earnings volatility. Pricing in contracts can incorporate FX clauses where feasible.

Capital access for cannabis

Financing costs and availability remain uneven as cannabis carries a higher sector risk premium; regulatory easing (federal banking reform) could compress yields by several hundred basis points and unlock bank lending, lowering WACC. Until then, Village Farms must rely on internal cash generation and disciplined capex sequencing. Strategic partnerships and JV structures can substitute for balance-sheet heavy expansion.

Retail channel dynamics

Consolidation among grocers and cannabis retailers shifts margin capture downstream, pressuring suppliers like Village Farms to accept lower net prices. Private-label produce captured 17.6% of U.S. grocery dollars in 2023 (NielsenIQ), putting branded pricing under pressure. E-commerce and delivery—≈10% of grocery sales in 2024—expand reach but add fulfillment costs and complexity. Data-sharing agreements with retailers can improve shelf allocation and sell-through.

- Consolidation: downstream margin pressure

- Private label 2023: 17.6% US grocery dollars

- Online grocery 2024: ~10% of sales

- Data-sharing: better allocation/sell-through

Cross-border cannabis rules, carbon pricing and IRA credits reshape costs and market access

Rising input costs (fertilizer down ~40% from 2022 peaks by 2024 yet above pre‑pandemic) and energy push margin pressure despite efficiency and long‑term PPAs. Demand steady (produce volumes +3% YoY 2023) but premium SKUs swing ~10–15% in downturns; private‑label 17.6% (2023) and online grocery ~10% (2024) constrain retail pass‑through. FX (CAD ~0.73 USD mid‑2025) and elevated sector credit spreads raise financing costs.

| Metric | Value |

|---|---|

| Fertilizer change | −40% from 2022 peaks (2024) |

| Produce volumes | +3% YoY (2023) |

| Private‑label | 17.6% (2023) |

| Online grocery | ~10% (2024) |

| CAD/USD | ~0.73 (mid‑2025) |

Preview the Actual Deliverable

Village Farms PESTLE Analysis

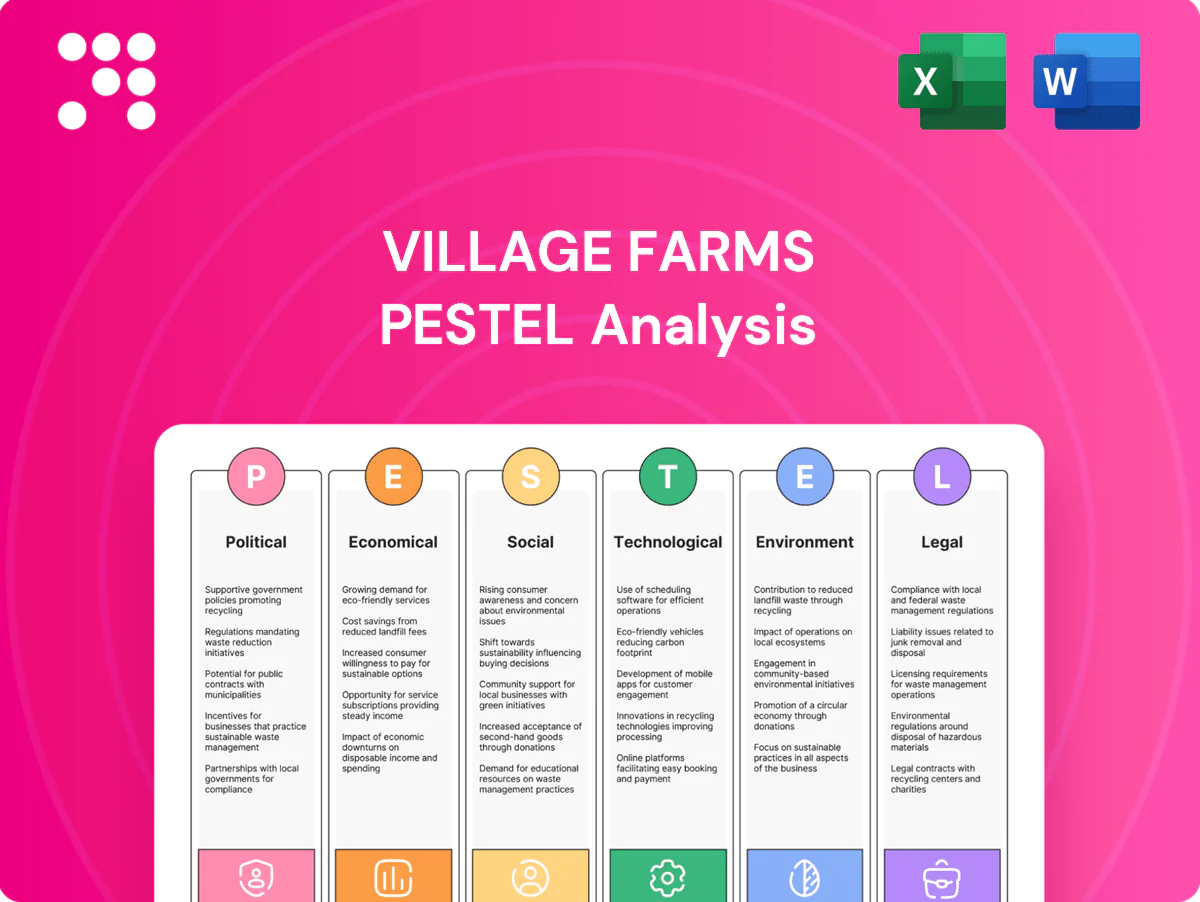

The Village Farms PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying, with no placeholders or teasers. After payment you’ll instantly download this same finished file.

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Village Farms reveals how political regulation, economic cycles, social trends, technological innovation, environmental pressures, and legal shifts together shape its strategic outlook. This concise briefing highlights risks and opportunities investors and managers need to know. Purchase the full, downloadable report for actionable, ready-to-use insights.

Political factors

US–Canada policy alignment

Operating in both Canada and the US exposes Village Farms to differing agricultural and cannabis policies: Canada legalized recreational cannabis federally in October 2018 while US cannabis remains Schedule I at federal level, with 24 states plus DC allowing adult-use and 38 states with medical programs as of July 2025.

Cross-border export of cannabis is prohibited under US federal law, so policy divergence creates duplicate compliance and restricts supply chain integration.

Monitoring federal–provincial and federal–state interplay is critical for capacity and product-mix decisions, and consistent engagement with policymakers helps anticipate shifts that affect market access and costs.

Cannabis legalization pace

Speed and scope of legalization directly expand Village Farms’ addressable market and product formats; US legal cannabis sales reached roughly $35B in 2024 while Canadian retail sales were about C$3.1B in 2023, underscoring scale upside from liberalization. Delays or restrictive frameworks compress growth and pricing power, whereas liberalization opens new channels and margin leverage. Municipal licensing caps can be as binding as national law, and optionality across provinces and states mitigates concentration risk.

Trade and USMCA effects

USMCA, in effect since July 1, 2020, improves predictability for produce trade but expressly leaves cannabis cross-border commerce closed. Tariffs, inspections and seasonal protection measures still compress greenhouse produce margins and raise logistics costs. Any phytosanitary or port-entry policy shift can rapidly disrupt freshness-sensitive supply chains. Diversifying routes and growing near key US markets reduces exposure.

Subsidies and energy policy

Greenhouse operators like Village Farms are highly sensitive to power and heat costs driven by provincial/state energy policy; US Inflation Reduction Act offers up to a 30% investment tax credit for qualifying clean energy investments, lowering capex payback on renewables and CHP. Canada's federal carbon price rose to CAD 65/t in 2023 and is scheduled to reach CAD 170/t by 2030, shifting competitiveness versus field-grown imports and making timing of efficiency capex material.

- IR A 30% ITC for energy property

- Canada carbon price: CAD 65/t (2023) → CAD 170/t (2030)

- Energy policy can materially cut unit costs via renewables/CHP

- Policy changes risk competitiveness; proactive capex captures tailwinds

Public health priorities

Government stances on nutrition, vaping and substance use shape product rules and campaigns; 24 states plus DC allow adult‑use cannabis (2025) while 14% of US high‑schoolers reported e‑cigarette use in 2023 (CDC). Produce benefits from healthy‑eating initiatives (WHO: noncommunicable diseases = 74% of global deaths), whereas cannabis faces restrictive marketing; tighter lab testing/contaminant thresholds raise SKU and cost pressures, and alignment with public‑health narratives improves stakeholder acceptance.

Cross-border cannabis rules, carbon pricing and IRA credits reshape costs and market access

Operating in Canada and the US exposes Village Farms to divergent cannabis and agricultural rules, with Canada federally legal since 2018 and US cannabis federally illegal while 24 states plus DC allow adult use (2025). Cross‑border cannabis trade is barred, forcing duplicate compliance and blocking supply integration. Energy, carbon and subsidy policies (IRA, Canada carbon pricing) materially affect capex and unit costs. Municipal licensing and testing standards constrain market access and SKU economics.

| Item | Value |

|---|---|

| US adult‑use states | 24 + DC (2025) |

| US legal cannabis sales | $35B (2024) |

| Canada retail cannabis | C$3.1B (2023) |

| Canada carbon price | CAD65/t (2023) → CAD170/t (2030) |

| IRA energy ITC | Up to 30% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Village Farms, combining data-driven trends and region-specific regulatory context to identify risks, opportunities and forward-looking scenarios for executives, investors and strategists.

A concise PESTLE summary for Village Farms that highlights regulatory, environmental and market risks, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline strategic discussions and risk mitigation.

Economic factors

Inflation and input costs

Rising energy, fertilizer, substrate and packaging costs continue to compress margins in controlled-environment agriculture; fertilizer prices, for example, declined roughly 40% from 2022 peaks by 2024 but remain elevated vs pre‑pandemic levels. Long‑term power purchase agreements (often 10–20 years) and efficiency technologies (LEDs, HVAC optimization) help buffer volatility. Retail pass‑through is constrained by growing private‑label share (~18–20% of US grocery sales), making cost discipline and product‑mix optimization critical.

Consumer spending cycles

Produce demand remains relatively resilient—industry produce volumes rose about 3% YoY in 2023—while premium cannabis and high-end produce tiers saw discretionary spend swings of roughly 10–15% in downturns. Recessions shift consumer preference to value SKUs and larger pack sizes, increasing their share by ~8–12%. Retailer bargaining strengthens in weak markets, often extracting 5–10% price concessions; flexible promotion planning helps preserve volume.

FX CAD–USD exposure

Cross-border revenues and costs expose Village Farms to CAD–USD translation and transaction risk; a 1% CAD move can meaningfully change reported USD margins. A weaker CAD (around 0.73 USD in mid-2025) aids Canadian exports but raises the cost of imported inputs and capital. Hedging programs and natural operational offsets are used to reduce earnings volatility. Pricing in contracts can incorporate FX clauses where feasible.

Capital access for cannabis

Financing costs and availability remain uneven as cannabis carries a higher sector risk premium; regulatory easing (federal banking reform) could compress yields by several hundred basis points and unlock bank lending, lowering WACC. Until then, Village Farms must rely on internal cash generation and disciplined capex sequencing. Strategic partnerships and JV structures can substitute for balance-sheet heavy expansion.

Retail channel dynamics

Consolidation among grocers and cannabis retailers shifts margin capture downstream, pressuring suppliers like Village Farms to accept lower net prices. Private-label produce captured 17.6% of U.S. grocery dollars in 2023 (NielsenIQ), putting branded pricing under pressure. E-commerce and delivery—≈10% of grocery sales in 2024—expand reach but add fulfillment costs and complexity. Data-sharing agreements with retailers can improve shelf allocation and sell-through.

- Consolidation: downstream margin pressure

- Private label 2023: 17.6% US grocery dollars

- Online grocery 2024: ~10% of sales

- Data-sharing: better allocation/sell-through

Cross-border cannabis rules, carbon pricing and IRA credits reshape costs and market access

Rising input costs (fertilizer down ~40% from 2022 peaks by 2024 yet above pre‑pandemic) and energy push margin pressure despite efficiency and long‑term PPAs. Demand steady (produce volumes +3% YoY 2023) but premium SKUs swing ~10–15% in downturns; private‑label 17.6% (2023) and online grocery ~10% (2024) constrain retail pass‑through. FX (CAD ~0.73 USD mid‑2025) and elevated sector credit spreads raise financing costs.

| Metric | Value |

|---|---|

| Fertilizer change | −40% from 2022 peaks (2024) |

| Produce volumes | +3% YoY (2023) |

| Private‑label | 17.6% (2023) |

| Online grocery | ~10% (2024) |

| CAD/USD | ~0.73 (mid‑2025) |

Preview the Actual Deliverable

Village Farms PESTLE Analysis

The Village Farms PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying, with no placeholders or teasers. After payment you’ll instantly download this same finished file.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Village Farms reveals how political regulation, economic cycles, social trends, technological innovation, environmental pressures, and legal shifts together shape its strategic outlook. This concise briefing highlights risks and opportunities investors and managers need to know. Purchase the full, downloadable report for actionable, ready-to-use insights.

Political factors

US–Canada policy alignment

Operating in both Canada and the US exposes Village Farms to differing agricultural and cannabis policies: Canada legalized recreational cannabis federally in October 2018 while US cannabis remains Schedule I at federal level, with 24 states plus DC allowing adult-use and 38 states with medical programs as of July 2025.

Cross-border export of cannabis is prohibited under US federal law, so policy divergence creates duplicate compliance and restricts supply chain integration.

Monitoring federal–provincial and federal–state interplay is critical for capacity and product-mix decisions, and consistent engagement with policymakers helps anticipate shifts that affect market access and costs.

Cannabis legalization pace

Speed and scope of legalization directly expand Village Farms’ addressable market and product formats; US legal cannabis sales reached roughly $35B in 2024 while Canadian retail sales were about C$3.1B in 2023, underscoring scale upside from liberalization. Delays or restrictive frameworks compress growth and pricing power, whereas liberalization opens new channels and margin leverage. Municipal licensing caps can be as binding as national law, and optionality across provinces and states mitigates concentration risk.

Trade and USMCA effects

USMCA, in effect since July 1, 2020, improves predictability for produce trade but expressly leaves cannabis cross-border commerce closed. Tariffs, inspections and seasonal protection measures still compress greenhouse produce margins and raise logistics costs. Any phytosanitary or port-entry policy shift can rapidly disrupt freshness-sensitive supply chains. Diversifying routes and growing near key US markets reduces exposure.

Subsidies and energy policy

Greenhouse operators like Village Farms are highly sensitive to power and heat costs driven by provincial/state energy policy; US Inflation Reduction Act offers up to a 30% investment tax credit for qualifying clean energy investments, lowering capex payback on renewables and CHP. Canada's federal carbon price rose to CAD 65/t in 2023 and is scheduled to reach CAD 170/t by 2030, shifting competitiveness versus field-grown imports and making timing of efficiency capex material.

- IR A 30% ITC for energy property

- Canada carbon price: CAD 65/t (2023) → CAD 170/t (2030)

- Energy policy can materially cut unit costs via renewables/CHP

- Policy changes risk competitiveness; proactive capex captures tailwinds

Public health priorities

Government stances on nutrition, vaping and substance use shape product rules and campaigns; 24 states plus DC allow adult‑use cannabis (2025) while 14% of US high‑schoolers reported e‑cigarette use in 2023 (CDC). Produce benefits from healthy‑eating initiatives (WHO: noncommunicable diseases = 74% of global deaths), whereas cannabis faces restrictive marketing; tighter lab testing/contaminant thresholds raise SKU and cost pressures, and alignment with public‑health narratives improves stakeholder acceptance.

Cross-border cannabis rules, carbon pricing and IRA credits reshape costs and market access

Operating in Canada and the US exposes Village Farms to divergent cannabis and agricultural rules, with Canada federally legal since 2018 and US cannabis federally illegal while 24 states plus DC allow adult use (2025). Cross‑border cannabis trade is barred, forcing duplicate compliance and blocking supply integration. Energy, carbon and subsidy policies (IRA, Canada carbon pricing) materially affect capex and unit costs. Municipal licensing and testing standards constrain market access and SKU economics.

| Item | Value |

|---|---|

| US adult‑use states | 24 + DC (2025) |

| US legal cannabis sales | $35B (2024) |

| Canada retail cannabis | C$3.1B (2023) |

| Canada carbon price | CAD65/t (2023) → CAD170/t (2030) |

| IRA energy ITC | Up to 30% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Village Farms, combining data-driven trends and region-specific regulatory context to identify risks, opportunities and forward-looking scenarios for executives, investors and strategists.

A concise PESTLE summary for Village Farms that highlights regulatory, environmental and market risks, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to streamline strategic discussions and risk mitigation.

Economic factors

Inflation and input costs

Rising energy, fertilizer, substrate and packaging costs continue to compress margins in controlled-environment agriculture; fertilizer prices, for example, declined roughly 40% from 2022 peaks by 2024 but remain elevated vs pre‑pandemic levels. Long‑term power purchase agreements (often 10–20 years) and efficiency technologies (LEDs, HVAC optimization) help buffer volatility. Retail pass‑through is constrained by growing private‑label share (~18–20% of US grocery sales), making cost discipline and product‑mix optimization critical.

Consumer spending cycles

Produce demand remains relatively resilient—industry produce volumes rose about 3% YoY in 2023—while premium cannabis and high-end produce tiers saw discretionary spend swings of roughly 10–15% in downturns. Recessions shift consumer preference to value SKUs and larger pack sizes, increasing their share by ~8–12%. Retailer bargaining strengthens in weak markets, often extracting 5–10% price concessions; flexible promotion planning helps preserve volume.

FX CAD–USD exposure

Cross-border revenues and costs expose Village Farms to CAD–USD translation and transaction risk; a 1% CAD move can meaningfully change reported USD margins. A weaker CAD (around 0.73 USD in mid-2025) aids Canadian exports but raises the cost of imported inputs and capital. Hedging programs and natural operational offsets are used to reduce earnings volatility. Pricing in contracts can incorporate FX clauses where feasible.

Capital access for cannabis

Financing costs and availability remain uneven as cannabis carries a higher sector risk premium; regulatory easing (federal banking reform) could compress yields by several hundred basis points and unlock bank lending, lowering WACC. Until then, Village Farms must rely on internal cash generation and disciplined capex sequencing. Strategic partnerships and JV structures can substitute for balance-sheet heavy expansion.

Retail channel dynamics

Consolidation among grocers and cannabis retailers shifts margin capture downstream, pressuring suppliers like Village Farms to accept lower net prices. Private-label produce captured 17.6% of U.S. grocery dollars in 2023 (NielsenIQ), putting branded pricing under pressure. E-commerce and delivery—≈10% of grocery sales in 2024—expand reach but add fulfillment costs and complexity. Data-sharing agreements with retailers can improve shelf allocation and sell-through.

- Consolidation: downstream margin pressure

- Private label 2023: 17.6% US grocery dollars

- Online grocery 2024: ~10% of sales

- Data-sharing: better allocation/sell-through

Cross-border cannabis rules, carbon pricing and IRA credits reshape costs and market access

Rising input costs (fertilizer down ~40% from 2022 peaks by 2024 yet above pre‑pandemic) and energy push margin pressure despite efficiency and long‑term PPAs. Demand steady (produce volumes +3% YoY 2023) but premium SKUs swing ~10–15% in downturns; private‑label 17.6% (2023) and online grocery ~10% (2024) constrain retail pass‑through. FX (CAD ~0.73 USD mid‑2025) and elevated sector credit spreads raise financing costs.

| Metric | Value |

|---|---|

| Fertilizer change | −40% from 2022 peaks (2024) |

| Produce volumes | +3% YoY (2023) |

| Private‑label | 17.6% (2023) |

| Online grocery | ~10% (2024) |

| CAD/USD | ~0.73 (mid‑2025) |

Preview the Actual Deliverable

Village Farms PESTLE Analysis

The Village Farms PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product you’re buying, with no placeholders or teasers. After payment you’ll instantly download this same finished file.