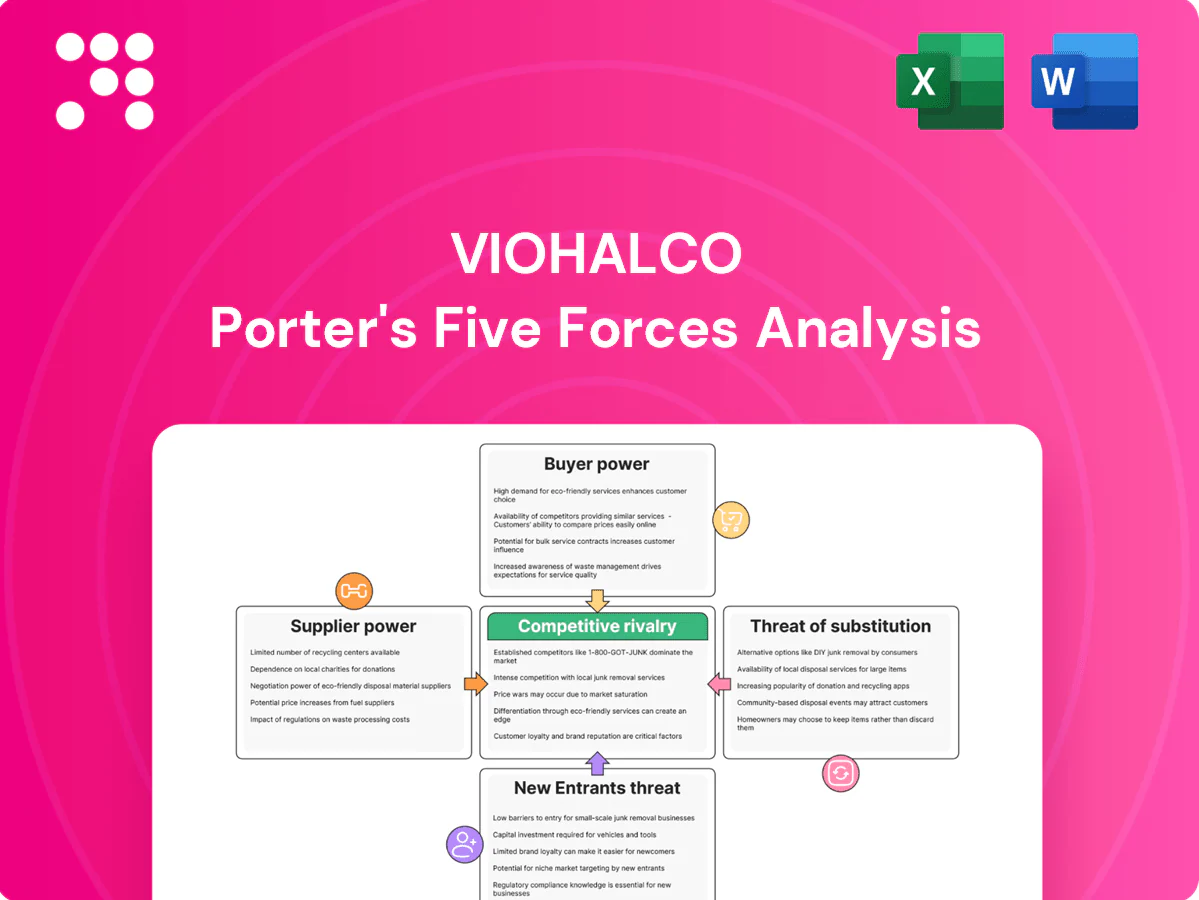

Viohalco Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Viohalco faces moderate buyer power, concentrated supplier relationships, growing substitute risks from alternative materials, and intense rivalry among regional metals producers. Capital intensity and regulatory barriers limit new entrants but raise operational risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Viohalco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Raw material concentration is high: in 2024 Chile and Peru together supplied about 40% of global copper mine output, Australia accounted for roughly 60% of bauxite exports, and China produced around 70% of key ferroalloys, raising supplier leverage over Viohalco.

Supply disruptions, mine grade declines or trader hoarding can tighten terms and force price pass-through; spot premia spiked in 2022–24 during outages.

Viohalco mitigates risk via multi-sourcing and increased recycled inputs (significant scrap use across its copper/aluminum plants), but upstream concentration still affects price and availability.

Energy dependency

Metals processing is highly energy-intensive, so electricity and gas suppliers are structurally important to Viohalco; European day‑ahead power markets saw 2024 price volatility with intra‑year peaks above €200/MWh, shifting negotiating leverage toward utilities. EU ETS carbon costs traded around €90–110/t in 2024, further raising input expense risk. Long‑term hedges and PPAs can materially temper exposure, while energy‑efficiency investments partially offset but do not eliminate dependence.

Scrap market dynamics

Scrap metal, tied to benchmarks like LME (aluminium averaged about $2,300/t in 2024) and regional steel indices, is critical for Viohalco’s routes; fragmented suppliers limit single-supplier power but tight 2024 markets raised aggregate leverage, quality/contamination specs strengthen buyer negotiation points, and regional logistics (port costs, inland haul) shift contract terms.

Specification-critical inputs

Specification-critical inputs such as specialty alloying elements and certified cathodes limit the pool of qualified suppliers, raising supplier bargaining power; as of 2024 rigorous certification and testing protocols commonly extend qualification timelines and materially increase switching costs. Suppliers of niche inputs often command measurable premiums, while dual-qualification programs enable Viohalco to balance quality assurance with greater procurement flexibility.

- Limited qualified suppliers

- Certification raises switching costs

- Niche suppliers command premiums

- Dual-qualification reduces supply risk

Logistics and freight

Bulk shipping, warehousing and port handling drive inbound flows for Viohalco; tight freight capacity or disruptions such as 2024 canal constraints and port strikes markedly increase logistics providers’ leverage and push spot rates and lead times higher, compressing margins.

- Diversify routes/partners to cut exposure

- Vertical coordination across plants and ports preserves margins

- Bulk shipping + warehousing = critical cost center

Concentration, energy-cost spikes and scrap tightness boost supplier power; diversify and recycle

Raw material concentration raises supplier leverage: Chile+Peru ~40% copper, Australia ~60% bauxite exports, China ~70% ferroalloys (2024).

Energy and carbon cost spikes (day‑ahead peaks >€200/MWh; EU ETS €90–110/t in 2024) increased supplier power.

Scrap tightness (LME aluminium ≈$2,300/t) plus certification/specialty inputs and logistics disruptions raise switching costs; multi‑sourcing, PPAs and recycling mitigate risk.

| Input | 2024 metric |

|---|---|

| Copper | Chile+Peru ~40% |

| Bauxite | Australia ~60% |

| Ferroalloys | China ~70% |

| Power | Peaks >€200/MWh |

| EU ETS | €90–110/t |

| Aluminium LME | ≈$2,300/t |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Viohalco, detailing supplier/buyer power, threat of substitutes, rivalry intensity and barriers to entry; highlights disruptive threats, strategic levers and actionable implications for pricing, profitability and market positioning.

A one-sheet Viohalco Porter's Five Forces summary that instantly highlights competitive pain points and strategic relief levers for faster decision-making. Customize pressure levels and swap in your data to model scenarios and present clear actions to management or investors.

Customers Bargaining Power

Large OEM buyers

Large OEMs in automotive, construction, energy, HVAC and packaging buy at scale—tenders often cover 1,000–50,000 tonnes and drive 2–7% price concessions in 2024, increasing bargaining leverage. Frame agreements and competitive tenders compress margins and service terms. Viohalco can defend via multi‑year supply (commonly 3–5 years), value‑added processing and superior on‑time reliability, with discount depth tied to volume alignment.

Commodity price transparency

LME and other indices published daily prices and inventories throughout 2024, giving buyers clear benchmarks to demand pass‑throughs. This shifts negotiations to premiums and conversion fees as the main battleground, with surcharges and indexed contracts used to balance volatility. Sophisticated buyers exploited timing and optionality in 2024 to optimize margins and lower effective delivered cost.

Switching costs and specs

For Viohalco standard products switching costs are moderate, increasing buyer bargaining power as customers can re-source commodity coils and rods relatively quickly in 2024. Applications needing certified alloys, tight tolerances or pipe qualifications impose higher switching costs and procurement lead times, reducing buyer power. Inclusion on approved vendor lists and provision of technical support and joint engineering significantly deepen customer stickiness.

Service and lead times

In cyclical upswings Viohalco faces softer buyer power as limited capacity and lead times rise; global steel capacity utilization was about 72% in 2024 (World Steel Association), tightening supply. In downturns excess capacity restores buyer leverage. Value-added services such as slitting, coatings and JIT shift focus from pure price; delivery reliability often outweighs small price deltas.

- Lead times: rise during upswings

- Value-added services: reduce price sensitivity

- Delivery reliability: key negotiator

Customer concentration

Exposure to a few large accounts amplifies buyer leverage over pricing and payment cycles; Viohalco reported consolidated turnover near €3.1bn in 2023, heightening focus on major clients. Diversification across sectors and geographies and intra-group cross-selling via subsidiaries dilutes single-buyer risk. Contract structures balancing volume commitments and flexibility mitigate cashflow and renegotiation exposure.

OEM tenders cut prices 2–7% in 2024; 72% capacity boosts buyers

Large OEM tenders (1,000–50,000t) and frame agreements drove 2–7% price concessions in 2024, boosting buyer leverage; value‑added services, multi‑year supply and reliability partially defend margins. LME pricing transparency in 2024 shifted bargaining to premiums and conversion fees, while certified alloys and tight tolerances raise switching costs. Top‑customer concentration (Viohalco turnover ~€3.1bn in 2023) amplifies buyer power amid 72% global steel capacity use in 2024.

| Metric | Value (2024/2023) |

|---|---|

| Tender size | 1,000–50,000 t |

| Price concessions | 2–7% |

| Steel capacity utilization | 72% (2024) |

| Viohalco turnover | ~€3.1bn (2023) |

Same Document Delivered

Viohalco Porter's Five Forces Analysis

This preview shows the exact Viohalco Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The full document is professionally formatted, ready for immediate download and use, and contains the complete strategic assessment as presented here.

From Overview to Strategy Blueprint

Viohalco faces moderate buyer power, concentrated supplier relationships, growing substitute risks from alternative materials, and intense rivalry among regional metals producers. Capital intensity and regulatory barriers limit new entrants but raise operational risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Viohalco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Raw material concentration is high: in 2024 Chile and Peru together supplied about 40% of global copper mine output, Australia accounted for roughly 60% of bauxite exports, and China produced around 70% of key ferroalloys, raising supplier leverage over Viohalco.

Supply disruptions, mine grade declines or trader hoarding can tighten terms and force price pass-through; spot premia spiked in 2022–24 during outages.

Viohalco mitigates risk via multi-sourcing and increased recycled inputs (significant scrap use across its copper/aluminum plants), but upstream concentration still affects price and availability.

Energy dependency

Metals processing is highly energy-intensive, so electricity and gas suppliers are structurally important to Viohalco; European day‑ahead power markets saw 2024 price volatility with intra‑year peaks above €200/MWh, shifting negotiating leverage toward utilities. EU ETS carbon costs traded around €90–110/t in 2024, further raising input expense risk. Long‑term hedges and PPAs can materially temper exposure, while energy‑efficiency investments partially offset but do not eliminate dependence.

Scrap market dynamics

Scrap metal, tied to benchmarks like LME (aluminium averaged about $2,300/t in 2024) and regional steel indices, is critical for Viohalco’s routes; fragmented suppliers limit single-supplier power but tight 2024 markets raised aggregate leverage, quality/contamination specs strengthen buyer negotiation points, and regional logistics (port costs, inland haul) shift contract terms.

Specification-critical inputs

Specification-critical inputs such as specialty alloying elements and certified cathodes limit the pool of qualified suppliers, raising supplier bargaining power; as of 2024 rigorous certification and testing protocols commonly extend qualification timelines and materially increase switching costs. Suppliers of niche inputs often command measurable premiums, while dual-qualification programs enable Viohalco to balance quality assurance with greater procurement flexibility.

- Limited qualified suppliers

- Certification raises switching costs

- Niche suppliers command premiums

- Dual-qualification reduces supply risk

Logistics and freight

Bulk shipping, warehousing and port handling drive inbound flows for Viohalco; tight freight capacity or disruptions such as 2024 canal constraints and port strikes markedly increase logistics providers’ leverage and push spot rates and lead times higher, compressing margins.

- Diversify routes/partners to cut exposure

- Vertical coordination across plants and ports preserves margins

- Bulk shipping + warehousing = critical cost center

Concentration, energy-cost spikes and scrap tightness boost supplier power; diversify and recycle

Raw material concentration raises supplier leverage: Chile+Peru ~40% copper, Australia ~60% bauxite exports, China ~70% ferroalloys (2024).

Energy and carbon cost spikes (day‑ahead peaks >€200/MWh; EU ETS €90–110/t in 2024) increased supplier power.

Scrap tightness (LME aluminium ≈$2,300/t) plus certification/specialty inputs and logistics disruptions raise switching costs; multi‑sourcing, PPAs and recycling mitigate risk.

| Input | 2024 metric |

|---|---|

| Copper | Chile+Peru ~40% |

| Bauxite | Australia ~60% |

| Ferroalloys | China ~70% |

| Power | Peaks >€200/MWh |

| EU ETS | €90–110/t |

| Aluminium LME | ≈$2,300/t |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Viohalco, detailing supplier/buyer power, threat of substitutes, rivalry intensity and barriers to entry; highlights disruptive threats, strategic levers and actionable implications for pricing, profitability and market positioning.

A one-sheet Viohalco Porter's Five Forces summary that instantly highlights competitive pain points and strategic relief levers for faster decision-making. Customize pressure levels and swap in your data to model scenarios and present clear actions to management or investors.

Customers Bargaining Power

Large OEM buyers

Large OEMs in automotive, construction, energy, HVAC and packaging buy at scale—tenders often cover 1,000–50,000 tonnes and drive 2–7% price concessions in 2024, increasing bargaining leverage. Frame agreements and competitive tenders compress margins and service terms. Viohalco can defend via multi‑year supply (commonly 3–5 years), value‑added processing and superior on‑time reliability, with discount depth tied to volume alignment.

Commodity price transparency

LME and other indices published daily prices and inventories throughout 2024, giving buyers clear benchmarks to demand pass‑throughs. This shifts negotiations to premiums and conversion fees as the main battleground, with surcharges and indexed contracts used to balance volatility. Sophisticated buyers exploited timing and optionality in 2024 to optimize margins and lower effective delivered cost.

Switching costs and specs

For Viohalco standard products switching costs are moderate, increasing buyer bargaining power as customers can re-source commodity coils and rods relatively quickly in 2024. Applications needing certified alloys, tight tolerances or pipe qualifications impose higher switching costs and procurement lead times, reducing buyer power. Inclusion on approved vendor lists and provision of technical support and joint engineering significantly deepen customer stickiness.

Service and lead times

In cyclical upswings Viohalco faces softer buyer power as limited capacity and lead times rise; global steel capacity utilization was about 72% in 2024 (World Steel Association), tightening supply. In downturns excess capacity restores buyer leverage. Value-added services such as slitting, coatings and JIT shift focus from pure price; delivery reliability often outweighs small price deltas.

- Lead times: rise during upswings

- Value-added services: reduce price sensitivity

- Delivery reliability: key negotiator

Customer concentration

Exposure to a few large accounts amplifies buyer leverage over pricing and payment cycles; Viohalco reported consolidated turnover near €3.1bn in 2023, heightening focus on major clients. Diversification across sectors and geographies and intra-group cross-selling via subsidiaries dilutes single-buyer risk. Contract structures balancing volume commitments and flexibility mitigate cashflow and renegotiation exposure.

OEM tenders cut prices 2–7% in 2024; 72% capacity boosts buyers

Large OEM tenders (1,000–50,000t) and frame agreements drove 2–7% price concessions in 2024, boosting buyer leverage; value‑added services, multi‑year supply and reliability partially defend margins. LME pricing transparency in 2024 shifted bargaining to premiums and conversion fees, while certified alloys and tight tolerances raise switching costs. Top‑customer concentration (Viohalco turnover ~€3.1bn in 2023) amplifies buyer power amid 72% global steel capacity use in 2024.

| Metric | Value (2024/2023) |

|---|---|

| Tender size | 1,000–50,000 t |

| Price concessions | 2–7% |

| Steel capacity utilization | 72% (2024) |

| Viohalco turnover | ~€3.1bn (2023) |

Same Document Delivered

Viohalco Porter's Five Forces Analysis

This preview shows the exact Viohalco Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The full document is professionally formatted, ready for immediate download and use, and contains the complete strategic assessment as presented here.

Description

From Overview to Strategy Blueprint

Viohalco faces moderate buyer power, concentrated supplier relationships, growing substitute risks from alternative materials, and intense rivalry among regional metals producers. Capital intensity and regulatory barriers limit new entrants but raise operational risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Viohalco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Raw material concentration is high: in 2024 Chile and Peru together supplied about 40% of global copper mine output, Australia accounted for roughly 60% of bauxite exports, and China produced around 70% of key ferroalloys, raising supplier leverage over Viohalco.

Supply disruptions, mine grade declines or trader hoarding can tighten terms and force price pass-through; spot premia spiked in 2022–24 during outages.

Viohalco mitigates risk via multi-sourcing and increased recycled inputs (significant scrap use across its copper/aluminum plants), but upstream concentration still affects price and availability.

Energy dependency

Metals processing is highly energy-intensive, so electricity and gas suppliers are structurally important to Viohalco; European day‑ahead power markets saw 2024 price volatility with intra‑year peaks above €200/MWh, shifting negotiating leverage toward utilities. EU ETS carbon costs traded around €90–110/t in 2024, further raising input expense risk. Long‑term hedges and PPAs can materially temper exposure, while energy‑efficiency investments partially offset but do not eliminate dependence.

Scrap market dynamics

Scrap metal, tied to benchmarks like LME (aluminium averaged about $2,300/t in 2024) and regional steel indices, is critical for Viohalco’s routes; fragmented suppliers limit single-supplier power but tight 2024 markets raised aggregate leverage, quality/contamination specs strengthen buyer negotiation points, and regional logistics (port costs, inland haul) shift contract terms.

Specification-critical inputs

Specification-critical inputs such as specialty alloying elements and certified cathodes limit the pool of qualified suppliers, raising supplier bargaining power; as of 2024 rigorous certification and testing protocols commonly extend qualification timelines and materially increase switching costs. Suppliers of niche inputs often command measurable premiums, while dual-qualification programs enable Viohalco to balance quality assurance with greater procurement flexibility.

- Limited qualified suppliers

- Certification raises switching costs

- Niche suppliers command premiums

- Dual-qualification reduces supply risk

Logistics and freight

Bulk shipping, warehousing and port handling drive inbound flows for Viohalco; tight freight capacity or disruptions such as 2024 canal constraints and port strikes markedly increase logistics providers’ leverage and push spot rates and lead times higher, compressing margins.

- Diversify routes/partners to cut exposure

- Vertical coordination across plants and ports preserves margins

- Bulk shipping + warehousing = critical cost center

Concentration, energy-cost spikes and scrap tightness boost supplier power; diversify and recycle

Raw material concentration raises supplier leverage: Chile+Peru ~40% copper, Australia ~60% bauxite exports, China ~70% ferroalloys (2024).

Energy and carbon cost spikes (day‑ahead peaks >€200/MWh; EU ETS €90–110/t in 2024) increased supplier power.

Scrap tightness (LME aluminium ≈$2,300/t) plus certification/specialty inputs and logistics disruptions raise switching costs; multi‑sourcing, PPAs and recycling mitigate risk.

| Input | 2024 metric |

|---|---|

| Copper | Chile+Peru ~40% |

| Bauxite | Australia ~60% |

| Ferroalloys | China ~70% |

| Power | Peaks >€200/MWh |

| EU ETS | €90–110/t |

| Aluminium LME | ≈$2,300/t |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Viohalco, detailing supplier/buyer power, threat of substitutes, rivalry intensity and barriers to entry; highlights disruptive threats, strategic levers and actionable implications for pricing, profitability and market positioning.

A one-sheet Viohalco Porter's Five Forces summary that instantly highlights competitive pain points and strategic relief levers for faster decision-making. Customize pressure levels and swap in your data to model scenarios and present clear actions to management or investors.

Customers Bargaining Power

Large OEM buyers

Large OEMs in automotive, construction, energy, HVAC and packaging buy at scale—tenders often cover 1,000–50,000 tonnes and drive 2–7% price concessions in 2024, increasing bargaining leverage. Frame agreements and competitive tenders compress margins and service terms. Viohalco can defend via multi‑year supply (commonly 3–5 years), value‑added processing and superior on‑time reliability, with discount depth tied to volume alignment.

Commodity price transparency

LME and other indices published daily prices and inventories throughout 2024, giving buyers clear benchmarks to demand pass‑throughs. This shifts negotiations to premiums and conversion fees as the main battleground, with surcharges and indexed contracts used to balance volatility. Sophisticated buyers exploited timing and optionality in 2024 to optimize margins and lower effective delivered cost.

Switching costs and specs

For Viohalco standard products switching costs are moderate, increasing buyer bargaining power as customers can re-source commodity coils and rods relatively quickly in 2024. Applications needing certified alloys, tight tolerances or pipe qualifications impose higher switching costs and procurement lead times, reducing buyer power. Inclusion on approved vendor lists and provision of technical support and joint engineering significantly deepen customer stickiness.

Service and lead times

In cyclical upswings Viohalco faces softer buyer power as limited capacity and lead times rise; global steel capacity utilization was about 72% in 2024 (World Steel Association), tightening supply. In downturns excess capacity restores buyer leverage. Value-added services such as slitting, coatings and JIT shift focus from pure price; delivery reliability often outweighs small price deltas.

- Lead times: rise during upswings

- Value-added services: reduce price sensitivity

- Delivery reliability: key negotiator

Customer concentration

Exposure to a few large accounts amplifies buyer leverage over pricing and payment cycles; Viohalco reported consolidated turnover near €3.1bn in 2023, heightening focus on major clients. Diversification across sectors and geographies and intra-group cross-selling via subsidiaries dilutes single-buyer risk. Contract structures balancing volume commitments and flexibility mitigate cashflow and renegotiation exposure.

OEM tenders cut prices 2–7% in 2024; 72% capacity boosts buyers

Large OEM tenders (1,000–50,000t) and frame agreements drove 2–7% price concessions in 2024, boosting buyer leverage; value‑added services, multi‑year supply and reliability partially defend margins. LME pricing transparency in 2024 shifted bargaining to premiums and conversion fees, while certified alloys and tight tolerances raise switching costs. Top‑customer concentration (Viohalco turnover ~€3.1bn in 2023) amplifies buyer power amid 72% global steel capacity use in 2024.

| Metric | Value (2024/2023) |

|---|---|

| Tender size | 1,000–50,000 t |

| Price concessions | 2–7% |

| Steel capacity utilization | 72% (2024) |

| Viohalco turnover | ~€3.1bn (2023) |

Same Document Delivered

Viohalco Porter's Five Forces Analysis

This preview shows the exact Viohalco Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The full document is professionally formatted, ready for immediate download and use, and contains the complete strategic assessment as presented here.