Virbac Porter's Five Forces Analysis

From Overview to Strategy Blueprint

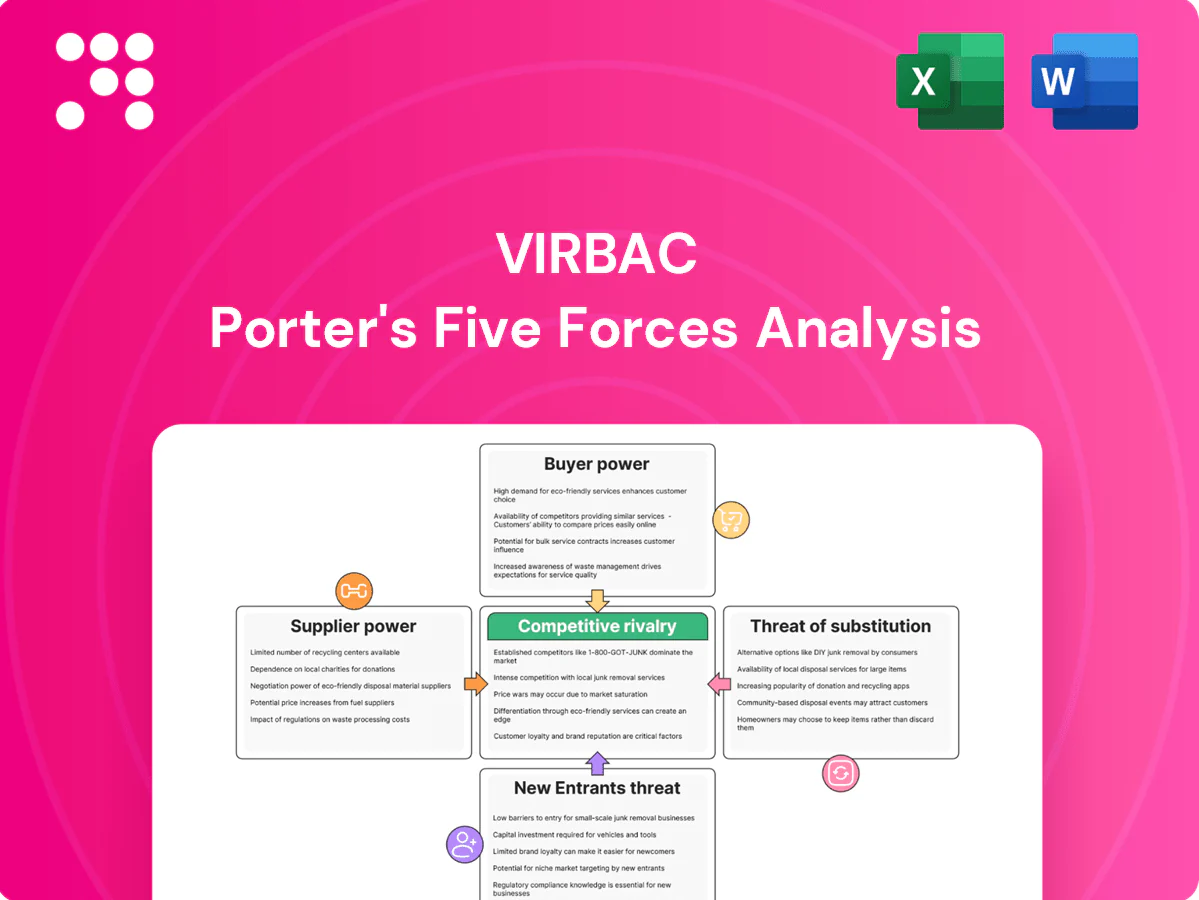

Virbac faces moderate supplier power and steady buyer demand, while rivalry in veterinary pharma remains intense due to product differentiation and global competitors; regulatory barriers temper new entrants but innovation and generics pose substitution risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Virbac’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized API/antigen inputs

Virbac depends on niche biologicals (antigens, adjuvants) and veterinary-grade APIs from a small set of qualified suppliers, giving suppliers elevated leverage; scarcity and tight quality specs increase lead times and price sensitivity. Dual-sourcing and long-term purchase agreements reduce but do not remove dependency. Disruptions can quickly ripple across vaccine and parasiticide portfolios, risking material impact on Virbac’s ~€2.0bn 2024 sales base.

Regulatory-grade manufacturing

In 2024 Virbacs regulatory-grade manufacturing means GMP/GLP compliance narrows the pool of approved raw- and packaging-material providers. Audits, validation and traceability requirements materially raise supplier switching costs and due diligence burdens. Approved-vendor lists concentrate spend with few partners, strengthening supplier leverage. Any requalification of a supplier extends lead times and elevates supply-chain risk.

Cold-chain and logistics

Vaccines require robust cold-chain; WHO estimates up to 50% of vaccines are wasted globally due to cold-chain failures, so few logistics partners consistently meet standards across regions. Seasonal spikes (e.g., flu cycles) and complex routes raise bargaining power of specialized carriers, who can command price premiums as logistics can account for ~20–30% of delivery costs. Diversifying lanes partially mitigates but does not eliminate reliance on reliable carriers.

Equipment and single-use systems

Biologic production relies on proprietary single-use bioreactors, filters and consumables from dominant suppliers such as Thermo Fisher, Merck, Sartorius and Cytiva, creating vendor lock-in. Technical compatibility and validation timelines make switching costly and slow, enabling suppliers to exert pricing power, especially when global capacity is tight. Long-term volume commitments and multi-year contracts are common levers to secure supply and better terms.

Commodity vs. specialty split

Bargaining power of suppliers splits between low-power commodity excipients/packaging and higher-power specialty inputs like APIs/biologics; Virbac’s 2024 sales mix (around €1.6bn group turnover) tilts net exposure depending on vaccine and specialty product weight. Strategic buffering, elevated safety stock and multi-sourcing reduced 2024 input shocks; collaborative demand forecasting improved allocation with key suppliers.

- Commodity: low power, many suppliers

- Specialty: concentrated, high power

- Mix-dependent net effect

- Hedge: inventory, multi-source, forecasting

Supplier concentration, cold-chain risks threaten €2.0bn sales

Suppliers of specialty APIs, biologics and single-use bioreactor consumables (Thermo Fisher, Merck, Sartorius, Cytiva) hold elevated leverage due to certification, validation and concentrated capacity, risking Virbac’s ~€2.0bn 2024 sales base. Cold-chain and logistics constraints (WHO vaccine waste ~50%; logistics ~20–30% of delivery costs) further increase supplier bargaining power. Long-term contracts, dual-sourcing and inventory buffers partly mitigate but switching remains costly and slow.

| Category | Key suppliers | 2024 metric | Mitigation |

|---|---|---|---|

| Biologics/APIs | Thermo Fisher, Merck, Sartorius, Cytiva | High concentration; impacts on €2.0bn sales | Long-term contracts, validation |

| Logistics | Specialized cold-chain carriers | WHO waste ~50%; delivery 20–30% | Lane diversification, partners |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Virbac; provides a detailed assessment of supplier and buyer power, substitutes, new entrants and industry rivalry to highlight pricing leverage, disruptive threats and strategic defensibility.

A concise one-sheet Porter's Five Forces for Virbac—clearly visualizes competitive pressures (suppliers, buyers, rivalry, entrants, substitutes) so teams can quickly pinpoint strategic pain points and adapt pricing, R&D, distribution or M&A responses.

Customers Bargaining Power

Veterinarians and clinics

Veterinarians shape product choice through trust and clinical protocols, and Virbac — reporting 2024 revenue of €1.46bn and ~6,800 employees — targets this influence with clinical evidence and detailing that reduce price sensitivity; fragmented independent clinics coexist with consolidation as group purchasing and chains concentrate demand, and switching occurs rapidly if efficacy or supply falter.

Distributors and wholesalers

In 2024 distributors and wholesalers aggregated Virbac orders to negotiate discounts, rebates and payment terms, using consolidated volumes as leverage. Their control of shelf-space and national reach materially influences Virbac’s access to veterinarians and pet owners. Multi-supplier portfolios raise distributors’ bargaining power, while performance-based incentives (sales targets, co-op funds) are commonly used to align interests and protect shelf presence.

Livestock producers/tenders

Large commercial farms and government/NGO tenders exert strong bargaining power—competitive bids and volume leverage frequently secure double‑digit discounts; institutional buyers account for the bulk of vaccine and parasiticide procurement. In 2024 the global animal health market was ~USD 44–48 billion, concentrating purchasing power among large integrators. Strict biosecurity rules keep reliability and service premiums, and total cost‑of‑use often offsets headline price pressure.

Companion animal owners

Switching and formulary control

Once clinic protocols are set, switching Virbac products requires staff retraining and risks to patient outcomes, which reduces buyer power; demonstrable differentiation and 2024 real-world evidence (post-market studies, practice-level outcomes) are key to defending share. Formularies at consolidated corporate vet groups can reallocate volume quickly, and stock-outs prompt rapid substitution within days to weeks.

- Switching friction lowers buyer power

- Formularies can shift share rapidly

- Real-world data defends position

- Stock-outs cause fast substitution

Vet prescriptions, distributors shape access; global animal health market USD 44–48bn

Veterinarians and clinic formularies drive purchases, limiting price sensitivity; Virbac reported 2024 revenue of €1.46bn and defends share with real‑world evidence. Distributors and large farms/tenders wield volume leverage—global animal health market ~USD 44–48bn (2024)—securing discounts and influencing access. Pet owners show brand loyalty, while e-commerce raises price transparency and substitution risk during stock‑outs.

| Metric | 2024 Value |

|---|---|

| Virbac revenue | €1.46bn |

| Global market | USD 44–48bn |

| US pet spend (2023) | USD 136.8bn |

Full Version Awaits

Virbac Porter's Five Forces Analysis

This preview shows the exact Virbac Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download upon purchase. What you see here is the complete, final file prepared for practical use.

From Overview to Strategy Blueprint

Virbac faces moderate supplier power and steady buyer demand, while rivalry in veterinary pharma remains intense due to product differentiation and global competitors; regulatory barriers temper new entrants but innovation and generics pose substitution risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Virbac’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized API/antigen inputs

Virbac depends on niche biologicals (antigens, adjuvants) and veterinary-grade APIs from a small set of qualified suppliers, giving suppliers elevated leverage; scarcity and tight quality specs increase lead times and price sensitivity. Dual-sourcing and long-term purchase agreements reduce but do not remove dependency. Disruptions can quickly ripple across vaccine and parasiticide portfolios, risking material impact on Virbac’s ~€2.0bn 2024 sales base.

Regulatory-grade manufacturing

In 2024 Virbacs regulatory-grade manufacturing means GMP/GLP compliance narrows the pool of approved raw- and packaging-material providers. Audits, validation and traceability requirements materially raise supplier switching costs and due diligence burdens. Approved-vendor lists concentrate spend with few partners, strengthening supplier leverage. Any requalification of a supplier extends lead times and elevates supply-chain risk.

Cold-chain and logistics

Vaccines require robust cold-chain; WHO estimates up to 50% of vaccines are wasted globally due to cold-chain failures, so few logistics partners consistently meet standards across regions. Seasonal spikes (e.g., flu cycles) and complex routes raise bargaining power of specialized carriers, who can command price premiums as logistics can account for ~20–30% of delivery costs. Diversifying lanes partially mitigates but does not eliminate reliance on reliable carriers.

Equipment and single-use systems

Biologic production relies on proprietary single-use bioreactors, filters and consumables from dominant suppliers such as Thermo Fisher, Merck, Sartorius and Cytiva, creating vendor lock-in. Technical compatibility and validation timelines make switching costly and slow, enabling suppliers to exert pricing power, especially when global capacity is tight. Long-term volume commitments and multi-year contracts are common levers to secure supply and better terms.

Commodity vs. specialty split

Bargaining power of suppliers splits between low-power commodity excipients/packaging and higher-power specialty inputs like APIs/biologics; Virbac’s 2024 sales mix (around €1.6bn group turnover) tilts net exposure depending on vaccine and specialty product weight. Strategic buffering, elevated safety stock and multi-sourcing reduced 2024 input shocks; collaborative demand forecasting improved allocation with key suppliers.

- Commodity: low power, many suppliers

- Specialty: concentrated, high power

- Mix-dependent net effect

- Hedge: inventory, multi-source, forecasting

Supplier concentration, cold-chain risks threaten €2.0bn sales

Suppliers of specialty APIs, biologics and single-use bioreactor consumables (Thermo Fisher, Merck, Sartorius, Cytiva) hold elevated leverage due to certification, validation and concentrated capacity, risking Virbac’s ~€2.0bn 2024 sales base. Cold-chain and logistics constraints (WHO vaccine waste ~50%; logistics ~20–30% of delivery costs) further increase supplier bargaining power. Long-term contracts, dual-sourcing and inventory buffers partly mitigate but switching remains costly and slow.

| Category | Key suppliers | 2024 metric | Mitigation |

|---|---|---|---|

| Biologics/APIs | Thermo Fisher, Merck, Sartorius, Cytiva | High concentration; impacts on €2.0bn sales | Long-term contracts, validation |

| Logistics | Specialized cold-chain carriers | WHO waste ~50%; delivery 20–30% | Lane diversification, partners |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Virbac; provides a detailed assessment of supplier and buyer power, substitutes, new entrants and industry rivalry to highlight pricing leverage, disruptive threats and strategic defensibility.

A concise one-sheet Porter's Five Forces for Virbac—clearly visualizes competitive pressures (suppliers, buyers, rivalry, entrants, substitutes) so teams can quickly pinpoint strategic pain points and adapt pricing, R&D, distribution or M&A responses.

Customers Bargaining Power

Veterinarians and clinics

Veterinarians shape product choice through trust and clinical protocols, and Virbac — reporting 2024 revenue of €1.46bn and ~6,800 employees — targets this influence with clinical evidence and detailing that reduce price sensitivity; fragmented independent clinics coexist with consolidation as group purchasing and chains concentrate demand, and switching occurs rapidly if efficacy or supply falter.

Distributors and wholesalers

In 2024 distributors and wholesalers aggregated Virbac orders to negotiate discounts, rebates and payment terms, using consolidated volumes as leverage. Their control of shelf-space and national reach materially influences Virbac’s access to veterinarians and pet owners. Multi-supplier portfolios raise distributors’ bargaining power, while performance-based incentives (sales targets, co-op funds) are commonly used to align interests and protect shelf presence.

Livestock producers/tenders

Large commercial farms and government/NGO tenders exert strong bargaining power—competitive bids and volume leverage frequently secure double‑digit discounts; institutional buyers account for the bulk of vaccine and parasiticide procurement. In 2024 the global animal health market was ~USD 44–48 billion, concentrating purchasing power among large integrators. Strict biosecurity rules keep reliability and service premiums, and total cost‑of‑use often offsets headline price pressure.

Companion animal owners

Switching and formulary control

Once clinic protocols are set, switching Virbac products requires staff retraining and risks to patient outcomes, which reduces buyer power; demonstrable differentiation and 2024 real-world evidence (post-market studies, practice-level outcomes) are key to defending share. Formularies at consolidated corporate vet groups can reallocate volume quickly, and stock-outs prompt rapid substitution within days to weeks.

- Switching friction lowers buyer power

- Formularies can shift share rapidly

- Real-world data defends position

- Stock-outs cause fast substitution

Vet prescriptions, distributors shape access; global animal health market USD 44–48bn

Veterinarians and clinic formularies drive purchases, limiting price sensitivity; Virbac reported 2024 revenue of €1.46bn and defends share with real‑world evidence. Distributors and large farms/tenders wield volume leverage—global animal health market ~USD 44–48bn (2024)—securing discounts and influencing access. Pet owners show brand loyalty, while e-commerce raises price transparency and substitution risk during stock‑outs.

| Metric | 2024 Value |

|---|---|

| Virbac revenue | €1.46bn |

| Global market | USD 44–48bn |

| US pet spend (2023) | USD 136.8bn |

Full Version Awaits

Virbac Porter's Five Forces Analysis

This preview shows the exact Virbac Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download upon purchase. What you see here is the complete, final file prepared for practical use.

Description

From Overview to Strategy Blueprint

Virbac faces moderate supplier power and steady buyer demand, while rivalry in veterinary pharma remains intense due to product differentiation and global competitors; regulatory barriers temper new entrants but innovation and generics pose substitution risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Virbac’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized API/antigen inputs

Virbac depends on niche biologicals (antigens, adjuvants) and veterinary-grade APIs from a small set of qualified suppliers, giving suppliers elevated leverage; scarcity and tight quality specs increase lead times and price sensitivity. Dual-sourcing and long-term purchase agreements reduce but do not remove dependency. Disruptions can quickly ripple across vaccine and parasiticide portfolios, risking material impact on Virbac’s ~€2.0bn 2024 sales base.

Regulatory-grade manufacturing

In 2024 Virbacs regulatory-grade manufacturing means GMP/GLP compliance narrows the pool of approved raw- and packaging-material providers. Audits, validation and traceability requirements materially raise supplier switching costs and due diligence burdens. Approved-vendor lists concentrate spend with few partners, strengthening supplier leverage. Any requalification of a supplier extends lead times and elevates supply-chain risk.

Cold-chain and logistics

Vaccines require robust cold-chain; WHO estimates up to 50% of vaccines are wasted globally due to cold-chain failures, so few logistics partners consistently meet standards across regions. Seasonal spikes (e.g., flu cycles) and complex routes raise bargaining power of specialized carriers, who can command price premiums as logistics can account for ~20–30% of delivery costs. Diversifying lanes partially mitigates but does not eliminate reliance on reliable carriers.

Equipment and single-use systems

Biologic production relies on proprietary single-use bioreactors, filters and consumables from dominant suppliers such as Thermo Fisher, Merck, Sartorius and Cytiva, creating vendor lock-in. Technical compatibility and validation timelines make switching costly and slow, enabling suppliers to exert pricing power, especially when global capacity is tight. Long-term volume commitments and multi-year contracts are common levers to secure supply and better terms.

Commodity vs. specialty split

Bargaining power of suppliers splits between low-power commodity excipients/packaging and higher-power specialty inputs like APIs/biologics; Virbac’s 2024 sales mix (around €1.6bn group turnover) tilts net exposure depending on vaccine and specialty product weight. Strategic buffering, elevated safety stock and multi-sourcing reduced 2024 input shocks; collaborative demand forecasting improved allocation with key suppliers.

- Commodity: low power, many suppliers

- Specialty: concentrated, high power

- Mix-dependent net effect

- Hedge: inventory, multi-source, forecasting

Supplier concentration, cold-chain risks threaten €2.0bn sales

Suppliers of specialty APIs, biologics and single-use bioreactor consumables (Thermo Fisher, Merck, Sartorius, Cytiva) hold elevated leverage due to certification, validation and concentrated capacity, risking Virbac’s ~€2.0bn 2024 sales base. Cold-chain and logistics constraints (WHO vaccine waste ~50%; logistics ~20–30% of delivery costs) further increase supplier bargaining power. Long-term contracts, dual-sourcing and inventory buffers partly mitigate but switching remains costly and slow.

| Category | Key suppliers | 2024 metric | Mitigation |

|---|---|---|---|

| Biologics/APIs | Thermo Fisher, Merck, Sartorius, Cytiva | High concentration; impacts on €2.0bn sales | Long-term contracts, validation |

| Logistics | Specialized cold-chain carriers | WHO waste ~50%; delivery 20–30% | Lane diversification, partners |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Virbac; provides a detailed assessment of supplier and buyer power, substitutes, new entrants and industry rivalry to highlight pricing leverage, disruptive threats and strategic defensibility.

A concise one-sheet Porter's Five Forces for Virbac—clearly visualizes competitive pressures (suppliers, buyers, rivalry, entrants, substitutes) so teams can quickly pinpoint strategic pain points and adapt pricing, R&D, distribution or M&A responses.

Customers Bargaining Power

Veterinarians and clinics

Veterinarians shape product choice through trust and clinical protocols, and Virbac — reporting 2024 revenue of €1.46bn and ~6,800 employees — targets this influence with clinical evidence and detailing that reduce price sensitivity; fragmented independent clinics coexist with consolidation as group purchasing and chains concentrate demand, and switching occurs rapidly if efficacy or supply falter.

Distributors and wholesalers

In 2024 distributors and wholesalers aggregated Virbac orders to negotiate discounts, rebates and payment terms, using consolidated volumes as leverage. Their control of shelf-space and national reach materially influences Virbac’s access to veterinarians and pet owners. Multi-supplier portfolios raise distributors’ bargaining power, while performance-based incentives (sales targets, co-op funds) are commonly used to align interests and protect shelf presence.

Livestock producers/tenders

Large commercial farms and government/NGO tenders exert strong bargaining power—competitive bids and volume leverage frequently secure double‑digit discounts; institutional buyers account for the bulk of vaccine and parasiticide procurement. In 2024 the global animal health market was ~USD 44–48 billion, concentrating purchasing power among large integrators. Strict biosecurity rules keep reliability and service premiums, and total cost‑of‑use often offsets headline price pressure.

Companion animal owners

Switching and formulary control

Once clinic protocols are set, switching Virbac products requires staff retraining and risks to patient outcomes, which reduces buyer power; demonstrable differentiation and 2024 real-world evidence (post-market studies, practice-level outcomes) are key to defending share. Formularies at consolidated corporate vet groups can reallocate volume quickly, and stock-outs prompt rapid substitution within days to weeks.

- Switching friction lowers buyer power

- Formularies can shift share rapidly

- Real-world data defends position

- Stock-outs cause fast substitution

Vet prescriptions, distributors shape access; global animal health market USD 44–48bn

Veterinarians and clinic formularies drive purchases, limiting price sensitivity; Virbac reported 2024 revenue of €1.46bn and defends share with real‑world evidence. Distributors and large farms/tenders wield volume leverage—global animal health market ~USD 44–48bn (2024)—securing discounts and influencing access. Pet owners show brand loyalty, while e-commerce raises price transparency and substitution risk during stock‑outs.

| Metric | 2024 Value |

|---|---|

| Virbac revenue | €1.46bn |

| Global market | USD 44–48bn |

| US pet spend (2023) | USD 136.8bn |

Full Version Awaits

Virbac Porter's Five Forces Analysis

This preview shows the exact Virbac Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download upon purchase. What you see here is the complete, final file prepared for practical use.