Visiativ Porter's Five Forces Analysis

Don't Miss the Bigger Picture

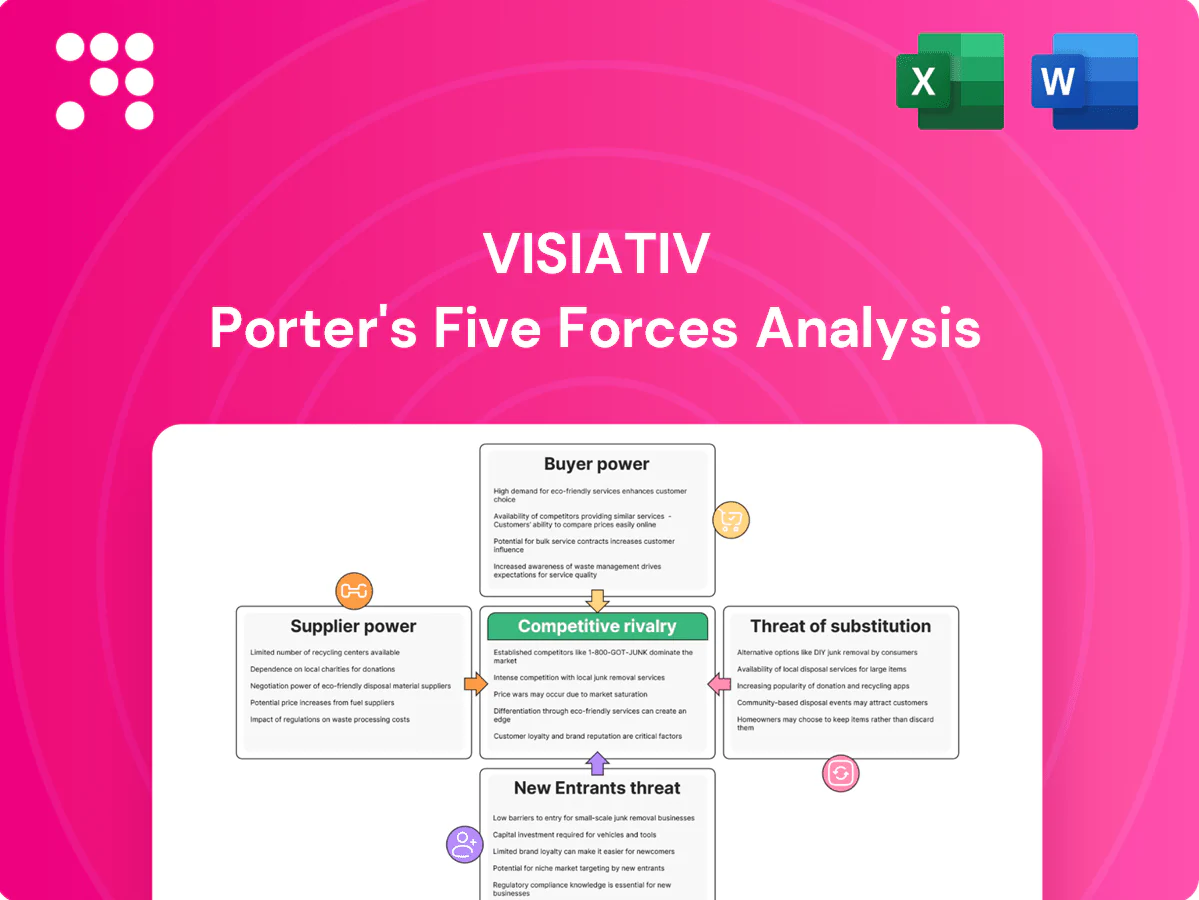

Visiativ’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, and substitute risks shaping its market position. It outlines strategic implications for growth, partnerships, and pricing but stops short of full force-by-force ratings and visuals. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Visiativ’s competitive dynamics and actionable insights in detail.

Suppliers Bargaining Power

Dassault Systèmes dependency

Visiativ relies heavily on Dassault Systèmes for core CAD/PLM products, APIs and certifications, giving Dassault meaningful influence over pricing and product roadmaps. Longstanding partnerships and volume commitments help Visiativ secure more favorable terms, but strategic dependence on Dassault remains material. Visiativ’s proprietary platforms and integration services partially dilute this supplier power by adding unique customer value.

Cloud and infrastructure vendors

Hyperscalers dominate infrastructure spend—AWS ~32% and Azure ~23% of the 2024 cloud market—offering standardized pricing tiers that simplify procurement. Switching is feasible, but migration complexity and egress fees (eg, S3 egress up to ~$0.09/GB) create friction. Reserved instances and savings plans can cut compute costs up to ~72% and widespread multi-cloud adoption (~92% of enterprises in 2024) reduces exposure. Vendor-specific managed services, however, reintroduce lock-in dynamics.

Specialist talent providers

Visiativ competes for scarce SOLIDWORKS/PLM consultants and developers, which raises supplier power of labor as wage inflation and poaching risk intensified in 2024. Internal academies, certification pathways and nearshore delivery centers mitigate dependency by growing in-house talent pools. Rigorous utilization management and standardized delivery playbooks further reduce volatility and lower marginal labor cost risks.

Niche ISVs and data providers

Niche ISVs and data providers can be critical for Visiativ’s vertical add-ons, connectors and proprietary data, giving some suppliers pricing power; fragmentation of suppliers, however, gives Visiativ negotiation flexibility while unique-IP holders can command premiums. Building in-house alternatives or adopting open standards and co-marketing deals reduces supplier leverage; 2024 enterprise software spend was estimated at about $650B (IDC).

- Fragmentation: allows negotiation flexibility

- Unique IP: commands premiums

- In-house/open standards: reduces leverage

- Co-marketing: balances commercial terms

Training and certification bodies

Training and certification bodies wield notable supplier power over Visiativ: access to official training, exams, and partner badges materially affects credibility and partner-sourced deal flow, with 2024 industry studies reporting a 20–30% uplift in pipeline for certified partners. Gatekeepers can set fees and requirements that raise onboarding and renewal costs. Developing proprietary enablement reduces dependence but cannot fully replace vendor recognition; strong compliance discipline limits surprise downside.

- Certification impact: +20–30% partner pipeline (2024 studies)

- Gatekeeper leverage: fees, renewal thresholds increase costs

- Proprietary enablement: lowers but does not eliminate vendor reliance

- Compliance discipline: caps surprise regulatory/contract risk

PLM vendor lock-in vs hyperscaler control ~55%, egress fee ~$0.09/GB

Visiativ’s dependence on Dassault Systèmes for SOLIDWORKS/PLM gives Dassault meaningful pricing and roadmap influence, though volume deals limit impact. Hyperscalers (AWS ~32% / Azure ~23% of 2024 cloud market) create lock-in via migration complexity and egress fees (~$0.09/GB) despite reserved-savings discounts. Labor and niche-ISV scarcity raise costs; in-house academies, nearshore centers and open-standards reduce supplier power.

| Supplier | 2024 Metric | Influence | Mitigation |

|---|---|---|---|

| Dassault | Core PLM provider | High | Volume deals, proprietary integrations |

| Hyperscalers | AWS 32% / Azure 23% | Medium | Multi-cloud, reserved pricing |

| Labor/ISVs | Talent tight; enterprise SW spend ~$650B | Medium | Academies, nearshore, open standards |

What is included in the product

Comprehensive Porter's Five Forces analysis of Visiativ, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes, and rivalry. Identifies disruptive threats, pricing pressures, and strategic levers to protect and grow Visiativ's market position.

Visiativ’s Porter's Five Forces one-sheet clarifies competitive pressures with a radar chart and customizable inputs, so teams quickly assess threats and opportunities while swapping data or scenarios without macros—ready for decks or deeper reports.

Customers Bargaining Power

SME price sensitivity

Core customers are SMEs/mid-market—SMEs account for 99.8% of EU enterprises and roughly 67% of employment (Eurostat)—so constrained budgets drive strong negotiation on total cost of ownership and time-to-value. Bundled offers and outcome-based pricing reduce churn and price pressure. Demonstrable ROI and quick wins (pilot savings within 3–6 months) are pivotal to close deals.

RFP-driven procurement

Formal RFP-driven procurement increases comparability among integrators, with 2024 procurement surveys indicating about 60% of enterprise tech deals used formal tenders, amplifying buyer leverage on rates, SLAs and scope. Differentiated IP and accelerators allow premium pricing—Vendors with proven IP can command 10–25% higher fees. Reference cases and certifications remain key tie-breakers in final selection.

Switching costs from integration

Customized workflows, proprietary data models and user training create high exit barriers that lower buyer power after implementation, with Visiativ reporting pro-forma revenue near €170m in 2023 reflecting recurring service penetration (company disclosures, 2023–2024 reporting).

Nevertheless, customers often unbundle run services—industry patterns show 10–25% of managed services can be reprocured—allowing partial vendor displacement.

Robust customer success and roadmap co-creation increase stickiness and reduce churn risk.

Alternative vendor ecosystems

Buyers can pivot to Siemens (Digital Industries Software ~€4.5B in 2024), Autodesk (~$5.2B FY2024) or PTC (~$1.8B FY2024), using comparative pilots and vendor incentives to strengthen negotiating leverage. Interoperability tools lower switch friction, but data migration and integration costs remain meaningful. Multi-year contracts with built-in flexibility and exit options are commonly used to counteract churn.

- Vendor options: Siemens/Autodesk/PTC

- Negotiation: pilots + incentives

- Switch friction: interoperability ↑, migration cost ↑

- Retention: flexible multi-year deals

Large accounts concentration

Enterprise and multi-site clients can dictate terms via volume, demanding tailored SLAs, governance frameworks and significant discounts; in 2024 these buyers increasingly leveraged centralized procurement to extract concessions. Visiativ counters with account-based teams and executive sponsorship to retain margins and align delivery to complex needs.

- Large accounts drive pricing pressure

- Tailored SLAs & governance expected

- Account teams + exec sponsors mitigate churn

- Diversify client base to lower concentration risk

SME tenders increase price/time-to-value pressure; incumbents enable easy switching

Buyers (SMEs = 99.8% EU firms; 67% employment) exert strong price/time-to-value pressure; ~60% of tech deals used formal tenders in 2024, increasing comparability. Visiativ reported pro-forma revenue ~€170m (2023); managed services reprocurement runs 10–25%, limiting lock-in. Large accounts leverage volume discounts; competitors (Siemens €4.5B, Autodesk $5.2B, PTC $1.8B 2024) enable pilots and switch options.

| Metric | Value |

|---|---|

| SME share (EU) | 99.8% / 67% employment (Eurostat) |

| Formal tenders | ~60% (2024) |

| Visiativ revenue | ~€170m (2023) |

| Competitor scale | Siemens €4.5B; Autodesk $5.2B; PTC $1.8B (2024) |

Same Document Delivered

Visiativ Porter's Five Forces Analysis

You’re previewing the Visiativ Porter’s Five Forces Analysis — the exact professionally written document you’ll receive after purchase. It’s fully formatted, ready to download and use immediately, with no placeholders or mockups. Instant access upon payment, no surprises.

Don't Miss the Bigger Picture

Visiativ’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, and substitute risks shaping its market position. It outlines strategic implications for growth, partnerships, and pricing but stops short of full force-by-force ratings and visuals. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Visiativ’s competitive dynamics and actionable insights in detail.

Suppliers Bargaining Power

Dassault Systèmes dependency

Visiativ relies heavily on Dassault Systèmes for core CAD/PLM products, APIs and certifications, giving Dassault meaningful influence over pricing and product roadmaps. Longstanding partnerships and volume commitments help Visiativ secure more favorable terms, but strategic dependence on Dassault remains material. Visiativ’s proprietary platforms and integration services partially dilute this supplier power by adding unique customer value.

Cloud and infrastructure vendors

Hyperscalers dominate infrastructure spend—AWS ~32% and Azure ~23% of the 2024 cloud market—offering standardized pricing tiers that simplify procurement. Switching is feasible, but migration complexity and egress fees (eg, S3 egress up to ~$0.09/GB) create friction. Reserved instances and savings plans can cut compute costs up to ~72% and widespread multi-cloud adoption (~92% of enterprises in 2024) reduces exposure. Vendor-specific managed services, however, reintroduce lock-in dynamics.

Specialist talent providers

Visiativ competes for scarce SOLIDWORKS/PLM consultants and developers, which raises supplier power of labor as wage inflation and poaching risk intensified in 2024. Internal academies, certification pathways and nearshore delivery centers mitigate dependency by growing in-house talent pools. Rigorous utilization management and standardized delivery playbooks further reduce volatility and lower marginal labor cost risks.

Niche ISVs and data providers

Niche ISVs and data providers can be critical for Visiativ’s vertical add-ons, connectors and proprietary data, giving some suppliers pricing power; fragmentation of suppliers, however, gives Visiativ negotiation flexibility while unique-IP holders can command premiums. Building in-house alternatives or adopting open standards and co-marketing deals reduces supplier leverage; 2024 enterprise software spend was estimated at about $650B (IDC).

- Fragmentation: allows negotiation flexibility

- Unique IP: commands premiums

- In-house/open standards: reduces leverage

- Co-marketing: balances commercial terms

Training and certification bodies

Training and certification bodies wield notable supplier power over Visiativ: access to official training, exams, and partner badges materially affects credibility and partner-sourced deal flow, with 2024 industry studies reporting a 20–30% uplift in pipeline for certified partners. Gatekeepers can set fees and requirements that raise onboarding and renewal costs. Developing proprietary enablement reduces dependence but cannot fully replace vendor recognition; strong compliance discipline limits surprise downside.

- Certification impact: +20–30% partner pipeline (2024 studies)

- Gatekeeper leverage: fees, renewal thresholds increase costs

- Proprietary enablement: lowers but does not eliminate vendor reliance

- Compliance discipline: caps surprise regulatory/contract risk

PLM vendor lock-in vs hyperscaler control ~55%, egress fee ~$0.09/GB

Visiativ’s dependence on Dassault Systèmes for SOLIDWORKS/PLM gives Dassault meaningful pricing and roadmap influence, though volume deals limit impact. Hyperscalers (AWS ~32% / Azure ~23% of 2024 cloud market) create lock-in via migration complexity and egress fees (~$0.09/GB) despite reserved-savings discounts. Labor and niche-ISV scarcity raise costs; in-house academies, nearshore centers and open-standards reduce supplier power.

| Supplier | 2024 Metric | Influence | Mitigation |

|---|---|---|---|

| Dassault | Core PLM provider | High | Volume deals, proprietary integrations |

| Hyperscalers | AWS 32% / Azure 23% | Medium | Multi-cloud, reserved pricing |

| Labor/ISVs | Talent tight; enterprise SW spend ~$650B | Medium | Academies, nearshore, open standards |

What is included in the product

Comprehensive Porter's Five Forces analysis of Visiativ, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes, and rivalry. Identifies disruptive threats, pricing pressures, and strategic levers to protect and grow Visiativ's market position.

Visiativ’s Porter's Five Forces one-sheet clarifies competitive pressures with a radar chart and customizable inputs, so teams quickly assess threats and opportunities while swapping data or scenarios without macros—ready for decks or deeper reports.

Customers Bargaining Power

SME price sensitivity

Core customers are SMEs/mid-market—SMEs account for 99.8% of EU enterprises and roughly 67% of employment (Eurostat)—so constrained budgets drive strong negotiation on total cost of ownership and time-to-value. Bundled offers and outcome-based pricing reduce churn and price pressure. Demonstrable ROI and quick wins (pilot savings within 3–6 months) are pivotal to close deals.

RFP-driven procurement

Formal RFP-driven procurement increases comparability among integrators, with 2024 procurement surveys indicating about 60% of enterprise tech deals used formal tenders, amplifying buyer leverage on rates, SLAs and scope. Differentiated IP and accelerators allow premium pricing—Vendors with proven IP can command 10–25% higher fees. Reference cases and certifications remain key tie-breakers in final selection.

Switching costs from integration

Customized workflows, proprietary data models and user training create high exit barriers that lower buyer power after implementation, with Visiativ reporting pro-forma revenue near €170m in 2023 reflecting recurring service penetration (company disclosures, 2023–2024 reporting).

Nevertheless, customers often unbundle run services—industry patterns show 10–25% of managed services can be reprocured—allowing partial vendor displacement.

Robust customer success and roadmap co-creation increase stickiness and reduce churn risk.

Alternative vendor ecosystems

Buyers can pivot to Siemens (Digital Industries Software ~€4.5B in 2024), Autodesk (~$5.2B FY2024) or PTC (~$1.8B FY2024), using comparative pilots and vendor incentives to strengthen negotiating leverage. Interoperability tools lower switch friction, but data migration and integration costs remain meaningful. Multi-year contracts with built-in flexibility and exit options are commonly used to counteract churn.

- Vendor options: Siemens/Autodesk/PTC

- Negotiation: pilots + incentives

- Switch friction: interoperability ↑, migration cost ↑

- Retention: flexible multi-year deals

Large accounts concentration

Enterprise and multi-site clients can dictate terms via volume, demanding tailored SLAs, governance frameworks and significant discounts; in 2024 these buyers increasingly leveraged centralized procurement to extract concessions. Visiativ counters with account-based teams and executive sponsorship to retain margins and align delivery to complex needs.

- Large accounts drive pricing pressure

- Tailored SLAs & governance expected

- Account teams + exec sponsors mitigate churn

- Diversify client base to lower concentration risk

SME tenders increase price/time-to-value pressure; incumbents enable easy switching

Buyers (SMEs = 99.8% EU firms; 67% employment) exert strong price/time-to-value pressure; ~60% of tech deals used formal tenders in 2024, increasing comparability. Visiativ reported pro-forma revenue ~€170m (2023); managed services reprocurement runs 10–25%, limiting lock-in. Large accounts leverage volume discounts; competitors (Siemens €4.5B, Autodesk $5.2B, PTC $1.8B 2024) enable pilots and switch options.

| Metric | Value |

|---|---|

| SME share (EU) | 99.8% / 67% employment (Eurostat) |

| Formal tenders | ~60% (2024) |

| Visiativ revenue | ~€170m (2023) |

| Competitor scale | Siemens €4.5B; Autodesk $5.2B; PTC $1.8B (2024) |

Same Document Delivered

Visiativ Porter's Five Forces Analysis

You’re previewing the Visiativ Porter’s Five Forces Analysis — the exact professionally written document you’ll receive after purchase. It’s fully formatted, ready to download and use immediately, with no placeholders or mockups. Instant access upon payment, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Visiativ’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer pressures, and substitute risks shaping its market position. It outlines strategic implications for growth, partnerships, and pricing but stops short of full force-by-force ratings and visuals. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Visiativ’s competitive dynamics and actionable insights in detail.

Suppliers Bargaining Power

Dassault Systèmes dependency

Visiativ relies heavily on Dassault Systèmes for core CAD/PLM products, APIs and certifications, giving Dassault meaningful influence over pricing and product roadmaps. Longstanding partnerships and volume commitments help Visiativ secure more favorable terms, but strategic dependence on Dassault remains material. Visiativ’s proprietary platforms and integration services partially dilute this supplier power by adding unique customer value.

Cloud and infrastructure vendors

Hyperscalers dominate infrastructure spend—AWS ~32% and Azure ~23% of the 2024 cloud market—offering standardized pricing tiers that simplify procurement. Switching is feasible, but migration complexity and egress fees (eg, S3 egress up to ~$0.09/GB) create friction. Reserved instances and savings plans can cut compute costs up to ~72% and widespread multi-cloud adoption (~92% of enterprises in 2024) reduces exposure. Vendor-specific managed services, however, reintroduce lock-in dynamics.

Specialist talent providers

Visiativ competes for scarce SOLIDWORKS/PLM consultants and developers, which raises supplier power of labor as wage inflation and poaching risk intensified in 2024. Internal academies, certification pathways and nearshore delivery centers mitigate dependency by growing in-house talent pools. Rigorous utilization management and standardized delivery playbooks further reduce volatility and lower marginal labor cost risks.

Niche ISVs and data providers

Niche ISVs and data providers can be critical for Visiativ’s vertical add-ons, connectors and proprietary data, giving some suppliers pricing power; fragmentation of suppliers, however, gives Visiativ negotiation flexibility while unique-IP holders can command premiums. Building in-house alternatives or adopting open standards and co-marketing deals reduces supplier leverage; 2024 enterprise software spend was estimated at about $650B (IDC).

- Fragmentation: allows negotiation flexibility

- Unique IP: commands premiums

- In-house/open standards: reduces leverage

- Co-marketing: balances commercial terms

Training and certification bodies

Training and certification bodies wield notable supplier power over Visiativ: access to official training, exams, and partner badges materially affects credibility and partner-sourced deal flow, with 2024 industry studies reporting a 20–30% uplift in pipeline for certified partners. Gatekeepers can set fees and requirements that raise onboarding and renewal costs. Developing proprietary enablement reduces dependence but cannot fully replace vendor recognition; strong compliance discipline limits surprise downside.

- Certification impact: +20–30% partner pipeline (2024 studies)

- Gatekeeper leverage: fees, renewal thresholds increase costs

- Proprietary enablement: lowers but does not eliminate vendor reliance

- Compliance discipline: caps surprise regulatory/contract risk

PLM vendor lock-in vs hyperscaler control ~55%, egress fee ~$0.09/GB

Visiativ’s dependence on Dassault Systèmes for SOLIDWORKS/PLM gives Dassault meaningful pricing and roadmap influence, though volume deals limit impact. Hyperscalers (AWS ~32% / Azure ~23% of 2024 cloud market) create lock-in via migration complexity and egress fees (~$0.09/GB) despite reserved-savings discounts. Labor and niche-ISV scarcity raise costs; in-house academies, nearshore centers and open-standards reduce supplier power.

| Supplier | 2024 Metric | Influence | Mitigation |

|---|---|---|---|

| Dassault | Core PLM provider | High | Volume deals, proprietary integrations |

| Hyperscalers | AWS 32% / Azure 23% | Medium | Multi-cloud, reserved pricing |

| Labor/ISVs | Talent tight; enterprise SW spend ~$650B | Medium | Academies, nearshore, open standards |

What is included in the product

Comprehensive Porter's Five Forces analysis of Visiativ, uncovering competitive drivers, customer and supplier power, entry barriers, substitutes, and rivalry. Identifies disruptive threats, pricing pressures, and strategic levers to protect and grow Visiativ's market position.

Visiativ’s Porter's Five Forces one-sheet clarifies competitive pressures with a radar chart and customizable inputs, so teams quickly assess threats and opportunities while swapping data or scenarios without macros—ready for decks or deeper reports.

Customers Bargaining Power

SME price sensitivity

Core customers are SMEs/mid-market—SMEs account for 99.8% of EU enterprises and roughly 67% of employment (Eurostat)—so constrained budgets drive strong negotiation on total cost of ownership and time-to-value. Bundled offers and outcome-based pricing reduce churn and price pressure. Demonstrable ROI and quick wins (pilot savings within 3–6 months) are pivotal to close deals.

RFP-driven procurement

Formal RFP-driven procurement increases comparability among integrators, with 2024 procurement surveys indicating about 60% of enterprise tech deals used formal tenders, amplifying buyer leverage on rates, SLAs and scope. Differentiated IP and accelerators allow premium pricing—Vendors with proven IP can command 10–25% higher fees. Reference cases and certifications remain key tie-breakers in final selection.

Switching costs from integration

Customized workflows, proprietary data models and user training create high exit barriers that lower buyer power after implementation, with Visiativ reporting pro-forma revenue near €170m in 2023 reflecting recurring service penetration (company disclosures, 2023–2024 reporting).

Nevertheless, customers often unbundle run services—industry patterns show 10–25% of managed services can be reprocured—allowing partial vendor displacement.

Robust customer success and roadmap co-creation increase stickiness and reduce churn risk.

Alternative vendor ecosystems

Buyers can pivot to Siemens (Digital Industries Software ~€4.5B in 2024), Autodesk (~$5.2B FY2024) or PTC (~$1.8B FY2024), using comparative pilots and vendor incentives to strengthen negotiating leverage. Interoperability tools lower switch friction, but data migration and integration costs remain meaningful. Multi-year contracts with built-in flexibility and exit options are commonly used to counteract churn.

- Vendor options: Siemens/Autodesk/PTC

- Negotiation: pilots + incentives

- Switch friction: interoperability ↑, migration cost ↑

- Retention: flexible multi-year deals

Large accounts concentration

Enterprise and multi-site clients can dictate terms via volume, demanding tailored SLAs, governance frameworks and significant discounts; in 2024 these buyers increasingly leveraged centralized procurement to extract concessions. Visiativ counters with account-based teams and executive sponsorship to retain margins and align delivery to complex needs.

- Large accounts drive pricing pressure

- Tailored SLAs & governance expected

- Account teams + exec sponsors mitigate churn

- Diversify client base to lower concentration risk

SME tenders increase price/time-to-value pressure; incumbents enable easy switching

Buyers (SMEs = 99.8% EU firms; 67% employment) exert strong price/time-to-value pressure; ~60% of tech deals used formal tenders in 2024, increasing comparability. Visiativ reported pro-forma revenue ~€170m (2023); managed services reprocurement runs 10–25%, limiting lock-in. Large accounts leverage volume discounts; competitors (Siemens €4.5B, Autodesk $5.2B, PTC $1.8B 2024) enable pilots and switch options.

| Metric | Value |

|---|---|

| SME share (EU) | 99.8% / 67% employment (Eurostat) |

| Formal tenders | ~60% (2024) |

| Visiativ revenue | ~€170m (2023) |

| Competitor scale | Siemens €4.5B; Autodesk $5.2B; PTC $1.8B (2024) |

Same Document Delivered

Visiativ Porter's Five Forces Analysis

You’re previewing the Visiativ Porter’s Five Forces Analysis — the exact professionally written document you’ll receive after purchase. It’s fully formatted, ready to download and use immediately, with no placeholders or mockups. Instant access upon payment, no surprises.