Vistra Energy Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

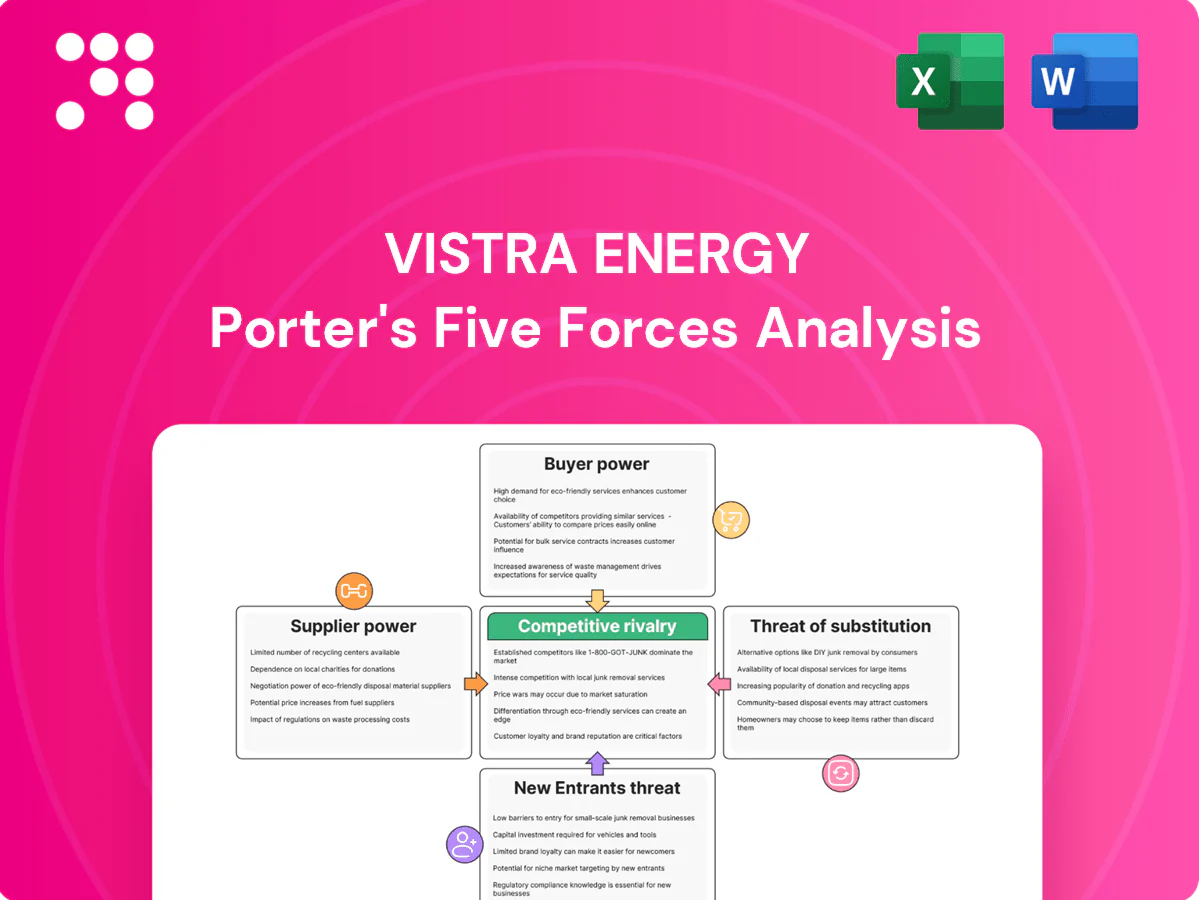

Vistra Energy faces moderate buyer power, significant regulatory and supplier pressures, and evolving substitute threats as the power sector shifts to renewables; these forces shape its margins and strategic choices. This snapshot highlights key competitive dynamics and risk areas. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy decisions.

Suppliers Bargaining Power

Concentrated fuel suppliers

Vistra, with roughly 39 GW of generation (2024), depends on regionally concentrated natural gas, coal and nuclear markets, giving key suppliers pricing leverage. Pipeline constraints and seasonal coal logistics can tighten fuel availability during peaks. Long-term fuel contracts and hedges blunt volatility but do not erase scarcity premiums. Nuclear fuel supply is specialized, dominated by vendors like Westinghouse and Framatome, with long lead times.

OEMs and maintenance vendors

Original equipment manufacturers such as General Electric, Siemens and Mitsubishi control most utility-scale turbines, boilers and control systems, creating parts dependence and switching costs for Vistra, which owns about 39 GW of generation capacity (2024). Outage scheduling and limited specialized labor during peak overhaul windows strengthen vendor bargaining power. Multi-year service agreements standardize pricing, while fleet-wide bundling helps Vistra secure volume discounts.

Transmission and market operators

Access to the seven US ISOs/RTOs is essential for Vistra, creating quasi-supplier power as congestion and interconnection timelines constrain dispatch and margins. Curtailments, forced outages or interconnection delays materially affect utilization and realized spark spreads. Administrative tariff fees and market rules limit Vistra’s bilateral leverage. Strategic siting and congestion hedges are used to reduce exposure.

Environmental credits and compliance inputs

Emissions allowances, RECs and compliance reagents (ammonia, lime) can tighten, pushing Vistra’s fuel‑adjusted input costs higher and creating episodic cost spikes; regulatory shifts (state/federal rules) can abruptly reprice these inputs. Long‑dated procurement contracts and diversified sourcing reduce exposure. Vistra’s shift toward gas and renewables changes its net allowance needs and market position.

- Inputs: allowances, RECs, reagents

- Risk: abrupt regulatory repricing

- Mitigation: long‑dated buys, diversified supply

- Impact: generation mix alters net allowance balance

Skilled labor and contractor availability

Outage, construction, and nuclear-qualified labor pools remain tight in 2024, constraining suppliers for Vistra’s largely thermal and Comanche Peak nuclear operations; Vistra’s ~39 GW fleet and two-unit Comanche Peak increase dependence on scarce nuclear technicians. Wage pressures and overtime during regional maintenance seasons elevate costs. Long-term workforce planning and preferred-vendor lists reduce supplier leverage. Geographic diversification smooths outage timing across the fleet.

- 2024 Vistra scale: ~39 GW capacity

- Comanche Peak: 2-unit nuclear site—nuclear-qualified labor scarce

- Wage/overtime premiums spike during peak outage seasons

- Preferred vendors and workforce planning temper supplier bargaining power

Power generators' suppliers exert moderate-high power in 2024; fuel, OEMs, nuclear, labor.

Vistra’s suppliers exert moderate-high power in 2024: fuel (gas/coal/nuclear) regionality plus pipeline/coal logistics create scarcity premiums; OEMs (GE, Siemens, Mitsubishi) and nuclear vendors (Westinghouse, Framatome) raise switching costs; labor shortages for outages and Comanche Peak’s 2-unit nuclear site increase service pricing. Long-term contracts and hedges partially offset risk.

| Metric | 2024 |

|---|---|

| Capacity | ~39 GW |

| Comanche Peak | 2 units |

| Key OEMs | GE, Siemens, Mitsubishi |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes and disruptive threats specific to Vistra Energy, with strategic implications for pricing, profitability and market positioning.

A concise, one-sheet Porter’s Five Forces for Vistra Energy—instantly clarifies competitive pressures and regulatory risks to speed boardroom decisions. Swap in updated market data or duplicate for scenarios (pre/post regulation, renewables shift) with no complex setup, ideal for decks or executive summaries.

Customers Bargaining Power

Retail choice and low switching costs

In competitive retail markets residential and small commercial customers can switch providers easily, driving higher price sensitivity; in 2024 the median residential electricity contract length remained about 12 months, keeping churn elevated. Comparison sites and short-term offers amplify buyer power, while differentiation through brand, green plans and superior service reduces churn. Loyalty programs and fixed-rate offers further lock in customers.

Large C&I buyers with hedging sophistication

Large C&I buyers with hedging sophistication frequently demand bespoke products, volume discounts, and risk-sharing arrangements, leveraging alternative procurement routes such as PPAs and direct access where available to strengthen bargaining power. Vistra responds with structured, integrated generation-backed offers and tailored hedges to retain volume and margins. Credit requirements and collateral terms are used as negotiation levers to balance counterparty risk and pricing.

Demand elasticity during price spikes

During extreme price events (eg. ERCOT max clearing price reaching 9,000 USD/MWh in Feb 2021) buyers curtail load or shift to demand response, compressing Vistra’s pricing latitude and turnover. Post-event regulatory scrutiny in Texas led to cap/pass-through limits and refund pressures on generators and retailers. Offering DR programs aligns incentives and helps retain customers. A disciplined hedging program is critical to protect margins without overcharging customers.

Green and ESG product preferences

Customers increasingly demand renewable plans and transparency, shifting bargaining power toward suppliers that can certify attributes; those unable to offer credible green options face discounting or churn, especially as corporate buyers push net-zero targets in 2024. Vistra’s access to RECs and owned renewables supports premium offerings, while verified claims and bundled services (storage, demand response) enhance customer stickiness.

- Higher bargaining power for verified green suppliers

- Risk of churn/discounting for non-credible offerings

- Vistra advantage: RECs, renewables, bundled services

Credit risk and payment terms

Economic cycles drive delinquencies and bad-debt expense, forcing Vistra in 2024 to tighten credit screens or offer pricing concessions during softer demand; payment flexibility has grown as a buyer demand. Prepay, customer deposits and usage-based billing are used to mitigate losses, and Vistra’s portfolio diversification across ERCOT, PJM and ISO-NE balances exposure across segments and regions.

- 2024: increased credit screening and deposit use

- Prepay/deposits reduce receivable risk

- Diversified mix mitigates regional defaults

Retail churn, corporate PPA demands and ERCOT price shocks reshape power contracts

Customers hold elevated bargaining power: retail churn stays high with median residential contracts ~12 months in 2024, comparison sites and short-term offers increase price sensitivity, while corporate buyers demand bespoke PPAs and hedges. Vistra mitigates with generation-backed offers, RECs/renewables and credit/collateral terms; demand response and fixed-rate or loyalty plans reduce churn. Extreme events (ERCOT 9,000 USD/MWh Feb 2021) compress pricing latitude and heighten regulatory risk.

| Metric | Value |

|---|---|

| Median residential contract | ~12 months (2024) |

| Key regions | ERCOT, PJM, ISO-NE |

| Significant price event | ERCOT 9,000 USD/MWh (Feb 2021) |

Preview Before You Purchase

Vistra Energy Porter's Five Forces Analysis

This preview shows the exact Vistra Energy Porter’s Five Forces analysis you’ll receive after purchase—no mockups or placeholders. The document is the final, professionally formatted file covering competitive rivalry, supplier and buyer power, threats of new entrants and substitutes. You’ll have immediate access to this same ready-to-use report upon payment.

A Must-Have Tool for Decision-Makers

Vistra Energy faces moderate buyer power, significant regulatory and supplier pressures, and evolving substitute threats as the power sector shifts to renewables; these forces shape its margins and strategic choices. This snapshot highlights key competitive dynamics and risk areas. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy decisions.

Suppliers Bargaining Power

Concentrated fuel suppliers

Vistra, with roughly 39 GW of generation (2024), depends on regionally concentrated natural gas, coal and nuclear markets, giving key suppliers pricing leverage. Pipeline constraints and seasonal coal logistics can tighten fuel availability during peaks. Long-term fuel contracts and hedges blunt volatility but do not erase scarcity premiums. Nuclear fuel supply is specialized, dominated by vendors like Westinghouse and Framatome, with long lead times.

OEMs and maintenance vendors

Original equipment manufacturers such as General Electric, Siemens and Mitsubishi control most utility-scale turbines, boilers and control systems, creating parts dependence and switching costs for Vistra, which owns about 39 GW of generation capacity (2024). Outage scheduling and limited specialized labor during peak overhaul windows strengthen vendor bargaining power. Multi-year service agreements standardize pricing, while fleet-wide bundling helps Vistra secure volume discounts.

Transmission and market operators

Access to the seven US ISOs/RTOs is essential for Vistra, creating quasi-supplier power as congestion and interconnection timelines constrain dispatch and margins. Curtailments, forced outages or interconnection delays materially affect utilization and realized spark spreads. Administrative tariff fees and market rules limit Vistra’s bilateral leverage. Strategic siting and congestion hedges are used to reduce exposure.

Environmental credits and compliance inputs

Emissions allowances, RECs and compliance reagents (ammonia, lime) can tighten, pushing Vistra’s fuel‑adjusted input costs higher and creating episodic cost spikes; regulatory shifts (state/federal rules) can abruptly reprice these inputs. Long‑dated procurement contracts and diversified sourcing reduce exposure. Vistra’s shift toward gas and renewables changes its net allowance needs and market position.

- Inputs: allowances, RECs, reagents

- Risk: abrupt regulatory repricing

- Mitigation: long‑dated buys, diversified supply

- Impact: generation mix alters net allowance balance

Skilled labor and contractor availability

Outage, construction, and nuclear-qualified labor pools remain tight in 2024, constraining suppliers for Vistra’s largely thermal and Comanche Peak nuclear operations; Vistra’s ~39 GW fleet and two-unit Comanche Peak increase dependence on scarce nuclear technicians. Wage pressures and overtime during regional maintenance seasons elevate costs. Long-term workforce planning and preferred-vendor lists reduce supplier leverage. Geographic diversification smooths outage timing across the fleet.

- 2024 Vistra scale: ~39 GW capacity

- Comanche Peak: 2-unit nuclear site—nuclear-qualified labor scarce

- Wage/overtime premiums spike during peak outage seasons

- Preferred vendors and workforce planning temper supplier bargaining power

Power generators' suppliers exert moderate-high power in 2024; fuel, OEMs, nuclear, labor.

Vistra’s suppliers exert moderate-high power in 2024: fuel (gas/coal/nuclear) regionality plus pipeline/coal logistics create scarcity premiums; OEMs (GE, Siemens, Mitsubishi) and nuclear vendors (Westinghouse, Framatome) raise switching costs; labor shortages for outages and Comanche Peak’s 2-unit nuclear site increase service pricing. Long-term contracts and hedges partially offset risk.

| Metric | 2024 |

|---|---|

| Capacity | ~39 GW |

| Comanche Peak | 2 units |

| Key OEMs | GE, Siemens, Mitsubishi |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes and disruptive threats specific to Vistra Energy, with strategic implications for pricing, profitability and market positioning.

A concise, one-sheet Porter’s Five Forces for Vistra Energy—instantly clarifies competitive pressures and regulatory risks to speed boardroom decisions. Swap in updated market data or duplicate for scenarios (pre/post regulation, renewables shift) with no complex setup, ideal for decks or executive summaries.

Customers Bargaining Power

Retail choice and low switching costs

In competitive retail markets residential and small commercial customers can switch providers easily, driving higher price sensitivity; in 2024 the median residential electricity contract length remained about 12 months, keeping churn elevated. Comparison sites and short-term offers amplify buyer power, while differentiation through brand, green plans and superior service reduces churn. Loyalty programs and fixed-rate offers further lock in customers.

Large C&I buyers with hedging sophistication

Large C&I buyers with hedging sophistication frequently demand bespoke products, volume discounts, and risk-sharing arrangements, leveraging alternative procurement routes such as PPAs and direct access where available to strengthen bargaining power. Vistra responds with structured, integrated generation-backed offers and tailored hedges to retain volume and margins. Credit requirements and collateral terms are used as negotiation levers to balance counterparty risk and pricing.

Demand elasticity during price spikes

During extreme price events (eg. ERCOT max clearing price reaching 9,000 USD/MWh in Feb 2021) buyers curtail load or shift to demand response, compressing Vistra’s pricing latitude and turnover. Post-event regulatory scrutiny in Texas led to cap/pass-through limits and refund pressures on generators and retailers. Offering DR programs aligns incentives and helps retain customers. A disciplined hedging program is critical to protect margins without overcharging customers.

Green and ESG product preferences

Customers increasingly demand renewable plans and transparency, shifting bargaining power toward suppliers that can certify attributes; those unable to offer credible green options face discounting or churn, especially as corporate buyers push net-zero targets in 2024. Vistra’s access to RECs and owned renewables supports premium offerings, while verified claims and bundled services (storage, demand response) enhance customer stickiness.

- Higher bargaining power for verified green suppliers

- Risk of churn/discounting for non-credible offerings

- Vistra advantage: RECs, renewables, bundled services

Credit risk and payment terms

Economic cycles drive delinquencies and bad-debt expense, forcing Vistra in 2024 to tighten credit screens or offer pricing concessions during softer demand; payment flexibility has grown as a buyer demand. Prepay, customer deposits and usage-based billing are used to mitigate losses, and Vistra’s portfolio diversification across ERCOT, PJM and ISO-NE balances exposure across segments and regions.

- 2024: increased credit screening and deposit use

- Prepay/deposits reduce receivable risk

- Diversified mix mitigates regional defaults

Retail churn, corporate PPA demands and ERCOT price shocks reshape power contracts

Customers hold elevated bargaining power: retail churn stays high with median residential contracts ~12 months in 2024, comparison sites and short-term offers increase price sensitivity, while corporate buyers demand bespoke PPAs and hedges. Vistra mitigates with generation-backed offers, RECs/renewables and credit/collateral terms; demand response and fixed-rate or loyalty plans reduce churn. Extreme events (ERCOT 9,000 USD/MWh Feb 2021) compress pricing latitude and heighten regulatory risk.

| Metric | Value |

|---|---|

| Median residential contract | ~12 months (2024) |

| Key regions | ERCOT, PJM, ISO-NE |

| Significant price event | ERCOT 9,000 USD/MWh (Feb 2021) |

Preview Before You Purchase

Vistra Energy Porter's Five Forces Analysis

This preview shows the exact Vistra Energy Porter’s Five Forces analysis you’ll receive after purchase—no mockups or placeholders. The document is the final, professionally formatted file covering competitive rivalry, supplier and buyer power, threats of new entrants and substitutes. You’ll have immediate access to this same ready-to-use report upon payment.

Description

A Must-Have Tool for Decision-Makers

Vistra Energy faces moderate buyer power, significant regulatory and supplier pressures, and evolving substitute threats as the power sector shifts to renewables; these forces shape its margins and strategic choices. This snapshot highlights key competitive dynamics and risk areas. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategy decisions.

Suppliers Bargaining Power

Concentrated fuel suppliers

Vistra, with roughly 39 GW of generation (2024), depends on regionally concentrated natural gas, coal and nuclear markets, giving key suppliers pricing leverage. Pipeline constraints and seasonal coal logistics can tighten fuel availability during peaks. Long-term fuel contracts and hedges blunt volatility but do not erase scarcity premiums. Nuclear fuel supply is specialized, dominated by vendors like Westinghouse and Framatome, with long lead times.

OEMs and maintenance vendors

Original equipment manufacturers such as General Electric, Siemens and Mitsubishi control most utility-scale turbines, boilers and control systems, creating parts dependence and switching costs for Vistra, which owns about 39 GW of generation capacity (2024). Outage scheduling and limited specialized labor during peak overhaul windows strengthen vendor bargaining power. Multi-year service agreements standardize pricing, while fleet-wide bundling helps Vistra secure volume discounts.

Transmission and market operators

Access to the seven US ISOs/RTOs is essential for Vistra, creating quasi-supplier power as congestion and interconnection timelines constrain dispatch and margins. Curtailments, forced outages or interconnection delays materially affect utilization and realized spark spreads. Administrative tariff fees and market rules limit Vistra’s bilateral leverage. Strategic siting and congestion hedges are used to reduce exposure.

Environmental credits and compliance inputs

Emissions allowances, RECs and compliance reagents (ammonia, lime) can tighten, pushing Vistra’s fuel‑adjusted input costs higher and creating episodic cost spikes; regulatory shifts (state/federal rules) can abruptly reprice these inputs. Long‑dated procurement contracts and diversified sourcing reduce exposure. Vistra’s shift toward gas and renewables changes its net allowance needs and market position.

- Inputs: allowances, RECs, reagents

- Risk: abrupt regulatory repricing

- Mitigation: long‑dated buys, diversified supply

- Impact: generation mix alters net allowance balance

Skilled labor and contractor availability

Outage, construction, and nuclear-qualified labor pools remain tight in 2024, constraining suppliers for Vistra’s largely thermal and Comanche Peak nuclear operations; Vistra’s ~39 GW fleet and two-unit Comanche Peak increase dependence on scarce nuclear technicians. Wage pressures and overtime during regional maintenance seasons elevate costs. Long-term workforce planning and preferred-vendor lists reduce supplier leverage. Geographic diversification smooths outage timing across the fleet.

- 2024 Vistra scale: ~39 GW capacity

- Comanche Peak: 2-unit nuclear site—nuclear-qualified labor scarce

- Wage/overtime premiums spike during peak outage seasons

- Preferred vendors and workforce planning temper supplier bargaining power

Power generators' suppliers exert moderate-high power in 2024; fuel, OEMs, nuclear, labor.

Vistra’s suppliers exert moderate-high power in 2024: fuel (gas/coal/nuclear) regionality plus pipeline/coal logistics create scarcity premiums; OEMs (GE, Siemens, Mitsubishi) and nuclear vendors (Westinghouse, Framatome) raise switching costs; labor shortages for outages and Comanche Peak’s 2-unit nuclear site increase service pricing. Long-term contracts and hedges partially offset risk.

| Metric | 2024 |

|---|---|

| Capacity | ~39 GW |

| Comanche Peak | 2 units |

| Key OEMs | GE, Siemens, Mitsubishi |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes and disruptive threats specific to Vistra Energy, with strategic implications for pricing, profitability and market positioning.

A concise, one-sheet Porter’s Five Forces for Vistra Energy—instantly clarifies competitive pressures and regulatory risks to speed boardroom decisions. Swap in updated market data or duplicate for scenarios (pre/post regulation, renewables shift) with no complex setup, ideal for decks or executive summaries.

Customers Bargaining Power

Retail choice and low switching costs

In competitive retail markets residential and small commercial customers can switch providers easily, driving higher price sensitivity; in 2024 the median residential electricity contract length remained about 12 months, keeping churn elevated. Comparison sites and short-term offers amplify buyer power, while differentiation through brand, green plans and superior service reduces churn. Loyalty programs and fixed-rate offers further lock in customers.

Large C&I buyers with hedging sophistication

Large C&I buyers with hedging sophistication frequently demand bespoke products, volume discounts, and risk-sharing arrangements, leveraging alternative procurement routes such as PPAs and direct access where available to strengthen bargaining power. Vistra responds with structured, integrated generation-backed offers and tailored hedges to retain volume and margins. Credit requirements and collateral terms are used as negotiation levers to balance counterparty risk and pricing.

Demand elasticity during price spikes

During extreme price events (eg. ERCOT max clearing price reaching 9,000 USD/MWh in Feb 2021) buyers curtail load or shift to demand response, compressing Vistra’s pricing latitude and turnover. Post-event regulatory scrutiny in Texas led to cap/pass-through limits and refund pressures on generators and retailers. Offering DR programs aligns incentives and helps retain customers. A disciplined hedging program is critical to protect margins without overcharging customers.

Green and ESG product preferences

Customers increasingly demand renewable plans and transparency, shifting bargaining power toward suppliers that can certify attributes; those unable to offer credible green options face discounting or churn, especially as corporate buyers push net-zero targets in 2024. Vistra’s access to RECs and owned renewables supports premium offerings, while verified claims and bundled services (storage, demand response) enhance customer stickiness.

- Higher bargaining power for verified green suppliers

- Risk of churn/discounting for non-credible offerings

- Vistra advantage: RECs, renewables, bundled services

Credit risk and payment terms

Economic cycles drive delinquencies and bad-debt expense, forcing Vistra in 2024 to tighten credit screens or offer pricing concessions during softer demand; payment flexibility has grown as a buyer demand. Prepay, customer deposits and usage-based billing are used to mitigate losses, and Vistra’s portfolio diversification across ERCOT, PJM and ISO-NE balances exposure across segments and regions.

- 2024: increased credit screening and deposit use

- Prepay/deposits reduce receivable risk

- Diversified mix mitigates regional defaults

Retail churn, corporate PPA demands and ERCOT price shocks reshape power contracts

Customers hold elevated bargaining power: retail churn stays high with median residential contracts ~12 months in 2024, comparison sites and short-term offers increase price sensitivity, while corporate buyers demand bespoke PPAs and hedges. Vistra mitigates with generation-backed offers, RECs/renewables and credit/collateral terms; demand response and fixed-rate or loyalty plans reduce churn. Extreme events (ERCOT 9,000 USD/MWh Feb 2021) compress pricing latitude and heighten regulatory risk.

| Metric | Value |

|---|---|

| Median residential contract | ~12 months (2024) |

| Key regions | ERCOT, PJM, ISO-NE |

| Significant price event | ERCOT 9,000 USD/MWh (Feb 2021) |

Preview Before You Purchase

Vistra Energy Porter's Five Forces Analysis

This preview shows the exact Vistra Energy Porter’s Five Forces analysis you’ll receive after purchase—no mockups or placeholders. The document is the final, professionally formatted file covering competitive rivalry, supplier and buyer power, threats of new entrants and substitutes. You’ll have immediate access to this same ready-to-use report upon payment.