Vital Energy SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Vital Energy's SWOT highlights competitive strengths, emerging risks, and untapped growth levers—essential context for investors and strategists. Want the full story and actionable recommendations? Purchase the complete SWOT for a research-backed, editable Word report plus an Excel matrix to plan, pitch, and invest with confidence.

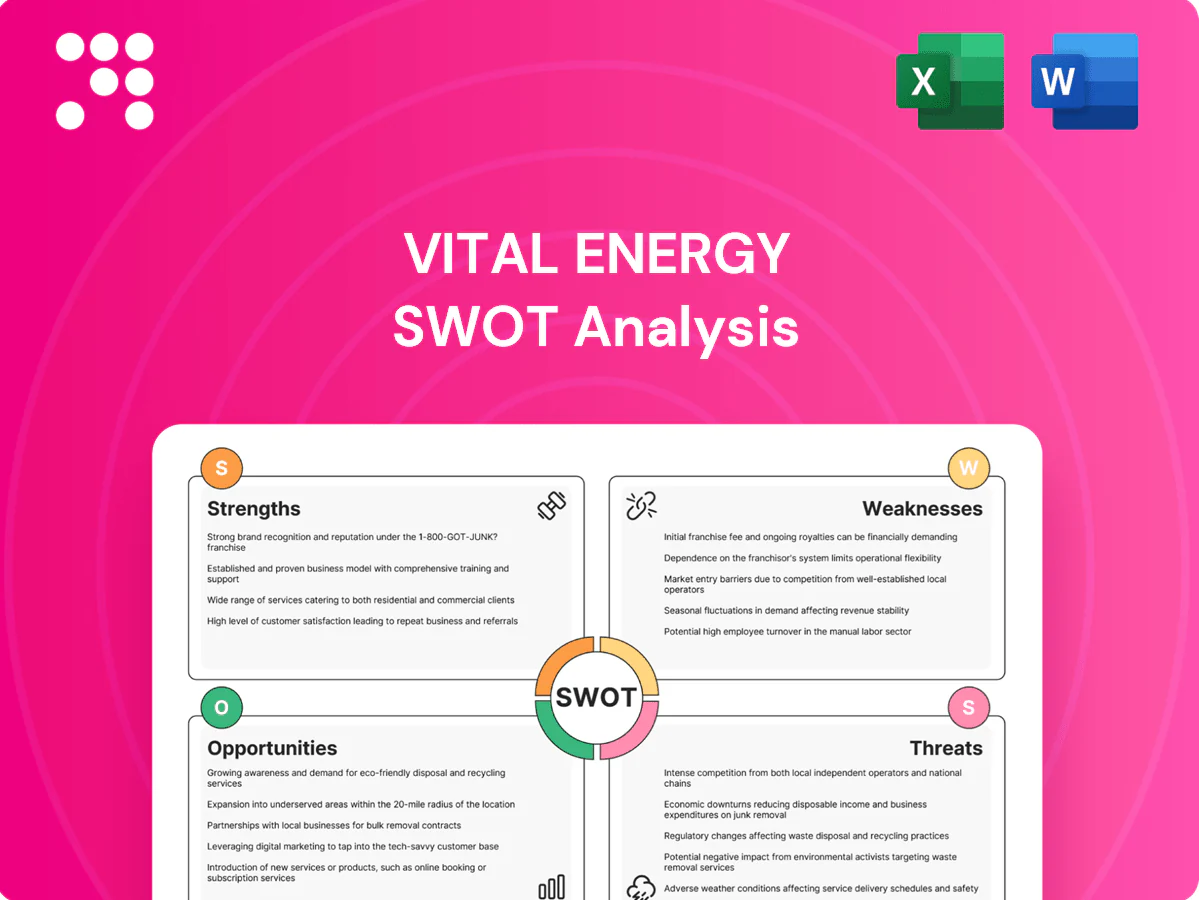

Strengths

Permian Basin focus

Concentration in the Permian Basin gives Vital Energy access to high-quality rock, stacked pay and established infrastructure supporting lower finding and development costs and competitive breakevens. Scale and single-basin learnings shorten cycle times and improve capital efficiency. Proximity to takeaway capacity—Permian crude output was about 5.5 million b/d in 2024 per EIA—aids reliable marketing and pricing.

Operational discipline

Operational discipline: targeted development drilling and pad optimization reduce per‑well cycle times and, per 2024 industry benchmarks, can lower unit costs by ~15–25% while lifting EURs ~10–20%, enhancing recovery. Consistent execution stabilizes production profiles and supports predictable free cash flow. Data‑driven well placement and repeatable completions mitigate subsurface and execution risk across inventory.

Acquisition capability

Vital Energy’s proven acquisition capability has expanded inventory depth and contiguous acreage, enabling consolidation that captures synergies in LOE, G&A and gathering costs. Strategic bolt-ons support longer laterals and improved development spacing, lowering per‑well capital intensity. Strong integration skills accelerate cash returns and measurable reserve growth through faster tie‑ins and optimized drilling programs.

Marketing and infrastructure

Access to midstream, water and takeaway networks reduces bottlenecks and basis risk, enabling multi-market sales optionality that can improve realized pricing; firm transport and hedging further support cash-flow stability while infrastructure proximity lowers capex per lateral foot.

- reduces basis risk

- multi-market optionality

- firm transport + hedging = stable cash flow

- lower capex per lateral foot

ESG commitment

Vital Energy's strong ESG commitment — including emissions, flaring and water-management programs — supports stakeholder acceptance and regulatory alignment, lowering operational risk and targeting up to 15% OPEX savings from efficiency gains observed in sector pilots through 2024.

Permian scale 5.5m b/d: 15–25% cost cuts, 10–20% EUR gains

Concentration in the Permian (5.5m b/d in 2024 per EIA) delivers low F&D and competitive breakevens; single-basin scale shortens cycles and raises capital efficiency. Operational discipline cuts unit costs ~15–25% and lifts EURs ~10–20%; ESG and water programs target ~15% OPEX savings, while midstream access reduces basis risk and stabilizes cash flow.

| Metric | 2024/2025 |

|---|---|

| Permian output | 5.5m b/d (EIA 2024) |

| Unit cost reduction | 15–25% |

| EUR uplift | 10–20% |

| OPEX savings (ESG) | up to 15% |

What is included in the product

Delivers a strategic overview of Vital Energy’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and key risks.

Provides a concise SWOT matrix tailored to Vital Energy for rapid identification and mitigation of strategic pain points, enabling focused actions to address operational and market risks.

Weaknesses

Commodity exposure

Revenue is highly sensitive to oil and gas price swings: Brent averaged about $86/bbl in 2024 with a roughly $69–$119 range, exposing Vital Energy to volatile top-line moves. Hedging reduces downside but caps upside and introduces basis risk between benchmarks and field prices. Cash flows and capital budgets can swing materially with macro cycles, while reserve bookings shift as companies reset price decks.

Geographic concentration

Permian-centric assets expose Vital Energy to regional regulatory shifts, weather and midstream constraints—Permian crude production was about 5.6 million b/d in 2024 (EIA), amplifying local bottleneck effects. Limited basin/commodity diversification increases exposure to Western Texas differentials and price swings. Operational disruption in the Permian can disproportionately hit EBITDA and cashflow, constraining portfolio flexibility.

Acquisition integration risk

Combining assets and teams can strain systems and culture, and industry studies show roughly 70% of mergers fail to deliver planned synergies. Synergy realization often lags expectations, with capture rates commonly below 60%. Acquired acreage data and type‑curves may deviate materially, driving reserve revisions; integration requires substantial capital and senior-management bandwidth.

Capital intensity

Unconventional development forces continuous drilling to sustain volumes; EIA reports median first-year decline for U.S. tight oil around 69%, driving high reinvestment needs that can strain free cash flow in down cycles. Persistent service cost inflation and supply-chain tightness since 2021 have raised operating expenses, eroding returns on new wells. Decline curves demand disciplined capital allocation to avoid value destruction.

- Continuous drilling requirement — 69% median first-year decline (EIA)

- High reinvestment pressure — stresses free cash flow in downturns

- Service cost inflation — compresses margins

- Decline curves — require strict capital discipline

Balance sheet sensitivity

Balance sheet sensitivity: leverage can rise with acquisitions and capex cycles, raising interest expense as benchmark policy rates sat near 5.25–5.50% in 2024 and tightening refinance windows. Refinancing risk grows in tight credit markets; ratings and access to capital hinge on commodity prices and execution, where downgrades materially increase funding costs.

- Leverage pressure

- Higher interest costs (Fed ~5.25–5.50% 2024)

- Refinancing risk

- Ratings tied to price/execution

Brent-driven cash flow risk; Permian concentration, ~69% first‑year decline

Revenue and cash flow remain highly sensitive to oil prices (Brent avg $86/bbl in 2024), exposing earnings to volatility and hedging basis risk. Permian concentration (≈5.6 million b/d 2024) amplifies regional midstream, weather and differential risk. High decline (median first‑year ~69% EIA) forces heavy reinvestment while rates (~5.25–5.50% 2024) raise refinancing and interest costs.

| Metric | 2024/2025 value |

|---|---|

| Brent average | $86/bbl (2024) |

| Permian production | ≈5.6 million b/d (2024 EIA) |

| First‑year decline (tight oil) | ~69% (EIA) |

| Policy rates | ~5.25–5.50% (2024) |

Same Document Delivered

Vital Energy SWOT Analysis

This is a real excerpt from the complete Vital Energy SWOT analysis you’ll receive upon purchase — professional, structured, and ready to use. The preview below is taken directly from the full report; no samples or placeholders. Buy now to unlock the editable, full-length document and access the complete strengths, weaknesses, opportunities, and threats assessment for Vital Energy.

Make Insightful Decisions Backed by Expert Research

Vital Energy's SWOT highlights competitive strengths, emerging risks, and untapped growth levers—essential context for investors and strategists. Want the full story and actionable recommendations? Purchase the complete SWOT for a research-backed, editable Word report plus an Excel matrix to plan, pitch, and invest with confidence.

Strengths

Permian Basin focus

Concentration in the Permian Basin gives Vital Energy access to high-quality rock, stacked pay and established infrastructure supporting lower finding and development costs and competitive breakevens. Scale and single-basin learnings shorten cycle times and improve capital efficiency. Proximity to takeaway capacity—Permian crude output was about 5.5 million b/d in 2024 per EIA—aids reliable marketing and pricing.

Operational discipline

Operational discipline: targeted development drilling and pad optimization reduce per‑well cycle times and, per 2024 industry benchmarks, can lower unit costs by ~15–25% while lifting EURs ~10–20%, enhancing recovery. Consistent execution stabilizes production profiles and supports predictable free cash flow. Data‑driven well placement and repeatable completions mitigate subsurface and execution risk across inventory.

Acquisition capability

Vital Energy’s proven acquisition capability has expanded inventory depth and contiguous acreage, enabling consolidation that captures synergies in LOE, G&A and gathering costs. Strategic bolt-ons support longer laterals and improved development spacing, lowering per‑well capital intensity. Strong integration skills accelerate cash returns and measurable reserve growth through faster tie‑ins and optimized drilling programs.

Marketing and infrastructure

Access to midstream, water and takeaway networks reduces bottlenecks and basis risk, enabling multi-market sales optionality that can improve realized pricing; firm transport and hedging further support cash-flow stability while infrastructure proximity lowers capex per lateral foot.

- reduces basis risk

- multi-market optionality

- firm transport + hedging = stable cash flow

- lower capex per lateral foot

ESG commitment

Vital Energy's strong ESG commitment — including emissions, flaring and water-management programs — supports stakeholder acceptance and regulatory alignment, lowering operational risk and targeting up to 15% OPEX savings from efficiency gains observed in sector pilots through 2024.

Permian scale 5.5m b/d: 15–25% cost cuts, 10–20% EUR gains

Concentration in the Permian (5.5m b/d in 2024 per EIA) delivers low F&D and competitive breakevens; single-basin scale shortens cycles and raises capital efficiency. Operational discipline cuts unit costs ~15–25% and lifts EURs ~10–20%; ESG and water programs target ~15% OPEX savings, while midstream access reduces basis risk and stabilizes cash flow.

| Metric | 2024/2025 |

|---|---|

| Permian output | 5.5m b/d (EIA 2024) |

| Unit cost reduction | 15–25% |

| EUR uplift | 10–20% |

| OPEX savings (ESG) | up to 15% |

What is included in the product

Delivers a strategic overview of Vital Energy’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and key risks.

Provides a concise SWOT matrix tailored to Vital Energy for rapid identification and mitigation of strategic pain points, enabling focused actions to address operational and market risks.

Weaknesses

Commodity exposure

Revenue is highly sensitive to oil and gas price swings: Brent averaged about $86/bbl in 2024 with a roughly $69–$119 range, exposing Vital Energy to volatile top-line moves. Hedging reduces downside but caps upside and introduces basis risk between benchmarks and field prices. Cash flows and capital budgets can swing materially with macro cycles, while reserve bookings shift as companies reset price decks.

Geographic concentration

Permian-centric assets expose Vital Energy to regional regulatory shifts, weather and midstream constraints—Permian crude production was about 5.6 million b/d in 2024 (EIA), amplifying local bottleneck effects. Limited basin/commodity diversification increases exposure to Western Texas differentials and price swings. Operational disruption in the Permian can disproportionately hit EBITDA and cashflow, constraining portfolio flexibility.

Acquisition integration risk

Combining assets and teams can strain systems and culture, and industry studies show roughly 70% of mergers fail to deliver planned synergies. Synergy realization often lags expectations, with capture rates commonly below 60%. Acquired acreage data and type‑curves may deviate materially, driving reserve revisions; integration requires substantial capital and senior-management bandwidth.

Capital intensity

Unconventional development forces continuous drilling to sustain volumes; EIA reports median first-year decline for U.S. tight oil around 69%, driving high reinvestment needs that can strain free cash flow in down cycles. Persistent service cost inflation and supply-chain tightness since 2021 have raised operating expenses, eroding returns on new wells. Decline curves demand disciplined capital allocation to avoid value destruction.

- Continuous drilling requirement — 69% median first-year decline (EIA)

- High reinvestment pressure — stresses free cash flow in downturns

- Service cost inflation — compresses margins

- Decline curves — require strict capital discipline

Balance sheet sensitivity

Balance sheet sensitivity: leverage can rise with acquisitions and capex cycles, raising interest expense as benchmark policy rates sat near 5.25–5.50% in 2024 and tightening refinance windows. Refinancing risk grows in tight credit markets; ratings and access to capital hinge on commodity prices and execution, where downgrades materially increase funding costs.

- Leverage pressure

- Higher interest costs (Fed ~5.25–5.50% 2024)

- Refinancing risk

- Ratings tied to price/execution

Brent-driven cash flow risk; Permian concentration, ~69% first‑year decline

Revenue and cash flow remain highly sensitive to oil prices (Brent avg $86/bbl in 2024), exposing earnings to volatility and hedging basis risk. Permian concentration (≈5.6 million b/d 2024) amplifies regional midstream, weather and differential risk. High decline (median first‑year ~69% EIA) forces heavy reinvestment while rates (~5.25–5.50% 2024) raise refinancing and interest costs.

| Metric | 2024/2025 value |

|---|---|

| Brent average | $86/bbl (2024) |

| Permian production | ≈5.6 million b/d (2024 EIA) |

| First‑year decline (tight oil) | ~69% (EIA) |

| Policy rates | ~5.25–5.50% (2024) |

Same Document Delivered

Vital Energy SWOT Analysis

This is a real excerpt from the complete Vital Energy SWOT analysis you’ll receive upon purchase — professional, structured, and ready to use. The preview below is taken directly from the full report; no samples or placeholders. Buy now to unlock the editable, full-length document and access the complete strengths, weaknesses, opportunities, and threats assessment for Vital Energy.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Vital Energy's SWOT highlights competitive strengths, emerging risks, and untapped growth levers—essential context for investors and strategists. Want the full story and actionable recommendations? Purchase the complete SWOT for a research-backed, editable Word report plus an Excel matrix to plan, pitch, and invest with confidence.

Strengths

Permian Basin focus

Concentration in the Permian Basin gives Vital Energy access to high-quality rock, stacked pay and established infrastructure supporting lower finding and development costs and competitive breakevens. Scale and single-basin learnings shorten cycle times and improve capital efficiency. Proximity to takeaway capacity—Permian crude output was about 5.5 million b/d in 2024 per EIA—aids reliable marketing and pricing.

Operational discipline

Operational discipline: targeted development drilling and pad optimization reduce per‑well cycle times and, per 2024 industry benchmarks, can lower unit costs by ~15–25% while lifting EURs ~10–20%, enhancing recovery. Consistent execution stabilizes production profiles and supports predictable free cash flow. Data‑driven well placement and repeatable completions mitigate subsurface and execution risk across inventory.

Acquisition capability

Vital Energy’s proven acquisition capability has expanded inventory depth and contiguous acreage, enabling consolidation that captures synergies in LOE, G&A and gathering costs. Strategic bolt-ons support longer laterals and improved development spacing, lowering per‑well capital intensity. Strong integration skills accelerate cash returns and measurable reserve growth through faster tie‑ins and optimized drilling programs.

Marketing and infrastructure

Access to midstream, water and takeaway networks reduces bottlenecks and basis risk, enabling multi-market sales optionality that can improve realized pricing; firm transport and hedging further support cash-flow stability while infrastructure proximity lowers capex per lateral foot.

- reduces basis risk

- multi-market optionality

- firm transport + hedging = stable cash flow

- lower capex per lateral foot

ESG commitment

Vital Energy's strong ESG commitment — including emissions, flaring and water-management programs — supports stakeholder acceptance and regulatory alignment, lowering operational risk and targeting up to 15% OPEX savings from efficiency gains observed in sector pilots through 2024.

Permian scale 5.5m b/d: 15–25% cost cuts, 10–20% EUR gains

Concentration in the Permian (5.5m b/d in 2024 per EIA) delivers low F&D and competitive breakevens; single-basin scale shortens cycles and raises capital efficiency. Operational discipline cuts unit costs ~15–25% and lifts EURs ~10–20%; ESG and water programs target ~15% OPEX savings, while midstream access reduces basis risk and stabilizes cash flow.

| Metric | 2024/2025 |

|---|---|

| Permian output | 5.5m b/d (EIA 2024) |

| Unit cost reduction | 15–25% |

| EUR uplift | 10–20% |

| OPEX savings (ESG) | up to 15% |

What is included in the product

Delivers a strategic overview of Vital Energy’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and key risks.

Provides a concise SWOT matrix tailored to Vital Energy for rapid identification and mitigation of strategic pain points, enabling focused actions to address operational and market risks.

Weaknesses

Commodity exposure

Revenue is highly sensitive to oil and gas price swings: Brent averaged about $86/bbl in 2024 with a roughly $69–$119 range, exposing Vital Energy to volatile top-line moves. Hedging reduces downside but caps upside and introduces basis risk between benchmarks and field prices. Cash flows and capital budgets can swing materially with macro cycles, while reserve bookings shift as companies reset price decks.

Geographic concentration

Permian-centric assets expose Vital Energy to regional regulatory shifts, weather and midstream constraints—Permian crude production was about 5.6 million b/d in 2024 (EIA), amplifying local bottleneck effects. Limited basin/commodity diversification increases exposure to Western Texas differentials and price swings. Operational disruption in the Permian can disproportionately hit EBITDA and cashflow, constraining portfolio flexibility.

Acquisition integration risk

Combining assets and teams can strain systems and culture, and industry studies show roughly 70% of mergers fail to deliver planned synergies. Synergy realization often lags expectations, with capture rates commonly below 60%. Acquired acreage data and type‑curves may deviate materially, driving reserve revisions; integration requires substantial capital and senior-management bandwidth.

Capital intensity

Unconventional development forces continuous drilling to sustain volumes; EIA reports median first-year decline for U.S. tight oil around 69%, driving high reinvestment needs that can strain free cash flow in down cycles. Persistent service cost inflation and supply-chain tightness since 2021 have raised operating expenses, eroding returns on new wells. Decline curves demand disciplined capital allocation to avoid value destruction.

- Continuous drilling requirement — 69% median first-year decline (EIA)

- High reinvestment pressure — stresses free cash flow in downturns

- Service cost inflation — compresses margins

- Decline curves — require strict capital discipline

Balance sheet sensitivity

Balance sheet sensitivity: leverage can rise with acquisitions and capex cycles, raising interest expense as benchmark policy rates sat near 5.25–5.50% in 2024 and tightening refinance windows. Refinancing risk grows in tight credit markets; ratings and access to capital hinge on commodity prices and execution, where downgrades materially increase funding costs.

- Leverage pressure

- Higher interest costs (Fed ~5.25–5.50% 2024)

- Refinancing risk

- Ratings tied to price/execution

Brent-driven cash flow risk; Permian concentration, ~69% first‑year decline

Revenue and cash flow remain highly sensitive to oil prices (Brent avg $86/bbl in 2024), exposing earnings to volatility and hedging basis risk. Permian concentration (≈5.6 million b/d 2024) amplifies regional midstream, weather and differential risk. High decline (median first‑year ~69% EIA) forces heavy reinvestment while rates (~5.25–5.50% 2024) raise refinancing and interest costs.

| Metric | 2024/2025 value |

|---|---|

| Brent average | $86/bbl (2024) |

| Permian production | ≈5.6 million b/d (2024 EIA) |

| First‑year decline (tight oil) | ~69% (EIA) |

| Policy rates | ~5.25–5.50% (2024) |

Same Document Delivered

Vital Energy SWOT Analysis

This is a real excerpt from the complete Vital Energy SWOT analysis you’ll receive upon purchase — professional, structured, and ready to use. The preview below is taken directly from the full report; no samples or placeholders. Buy now to unlock the editable, full-length document and access the complete strengths, weaknesses, opportunities, and threats assessment for Vital Energy.