Vital Farms Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

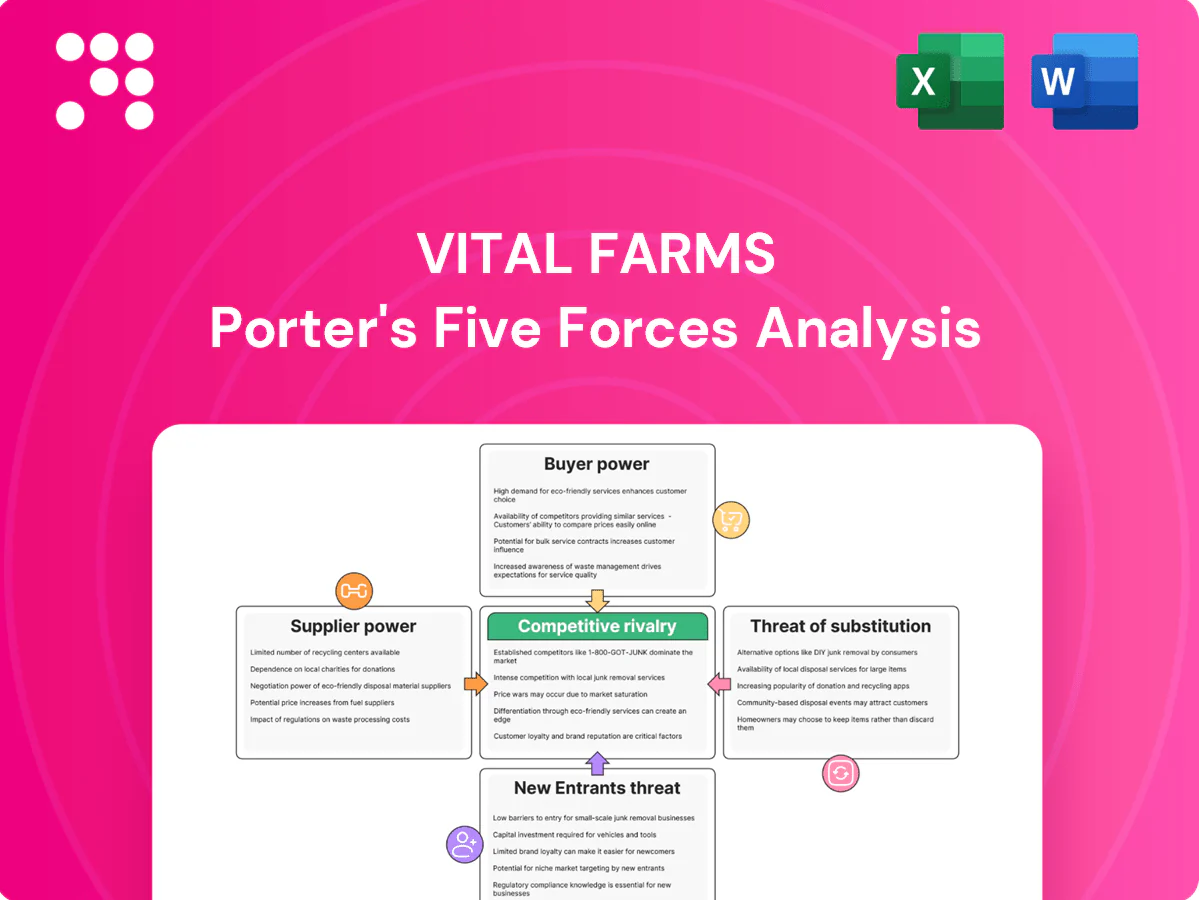

Vital Farms faces unique competitive dynamics—strong buyer awareness for ethical eggs, concentrated supplier risks in pasture-raised supply chains, and moderate threat from branded and private-label substitutes. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report for actionable insights and decision-ready guidance.

Suppliers Bargaining Power

Fragmented small-farm network

Most egg supply comes from a fragmented network of over 800 family farms as of 2024, so no single farm holds material leverage. Coordinated expectations around pasture standards and audits, however, let farmers exert collective influence on pricing and practices. Vital Farms must actively manage relationships and compliance to keep supply steady, giving suppliers measurable but soft bargaining power.

Welfare standards raise costs

Pasture-raised protocols demand more land, labor, and compliance, raising farm cost structures and contributing to industry feed and input cost shocks—feed costs rose roughly 20% from 2021–24, squeezing margins. Suppliers therefore press for price adjustments to cover these burdens, especially during cost spikes. Vital Farms’ brand depends on strict adherence to pasture standards, limiting its flexibility to trade down and enhancing supplier bargaining power.

Feed and input concentration

Feed, chicks, packaging and logistics for Vital Farms are procured from concentrated upstream markets, increasing supplier leverage; grain costs, for example, surged roughly 20–25% from 2021–23 and remained elevated into 2024, tightening margins for egg producers. When grain prices rise or supply tightens, input providers can demand higher prices or stricter terms, making cost pass-through to farms and retailers a core negotiation. This concentration thus amplifies supplier power cyclically, pressuring Vital Farms’ pricing and margin management.

Biosecurity, weather, and seasonality

Disease outbreaks and extreme weather constrain pasture-based output; as of 2024 USDA monitoring continued after more than 58 million poultry losses from HPAI through 2023, tightening supply and raising the value of compliant producers.

Vital Farms may pay premiums to secure volumes and continuity, so supply shocks and seasonality shift bargaining power toward suppliers, increasing input costs and contract leverage.

- Higher supplier leverage from disease/weather

- Premiums likely paid for continuity

- Compliance raises supplier value

- Seasonal swings amplify supply risk

Switching constraints and certification

Onboarding new farms requires audits, training and months to meet Vital Farms standards, creating switching frictions that raise dependence on existing suppliers. Farms certified to the brand’s pasture-raised and animal welfare specs are relatively scarce assets, strengthening their negotiating stance. This scarcity increases supplier bargaining power, especially during supply tightness or egg-price volatility.

- Onboarding friction: audits + training + months

- Certified farms: scarce, high-value suppliers

- Effect: stronger supplier leverage, potential input-cost pressure

HPAI cuts 58M, feed +20%, onboarding 3-6mo

Vital Farms sources from ~800 family farms (2024), giving individual farms low leverage but certified pasture-raised suppliers scarce; feed costs rose ~20% (2021–24) squeezing margins, and HPAI caused ~58M poultry losses through 2023, tightening supply and raising supplier power. Onboarding certified farms takes months, and premiums are often paid to secure continuity, amplifying supplier bargaining power.

| Metric | Value | Impact |

|---|---|---|

| Family farms | ~800 (2024) | Fragmented but scarce certified suppliers |

| Feed cost change | +~20% (2021–24) | Margin pressure |

| HPAI losses | ~58M (through 2023) | Supply tightening |

| Onboarding time | 3–6 months | Switching friction |

What is included in the product

Analyzes competitive forces shaping Vital Farms' market — supplier and buyer power, industry rivalry, substitutes, and entry threats — with strategic insights for investors and managers.

A one-sheet Porter's Five Forces for Vital Farms that clarifies competitive pressure and supplier dynamics at a glance—ideal for rapid strategy decisions and easy slide insertion.

Customers Bargaining Power

Retailer concentration

Large grocers control shelf access and pricing power; Walmart alone held about 25% of US grocery sales in 2024 and Kroger roughly 9%, concentrating influence over assortment and margins.

These chains routinely demand trade spend, slotting fees and promotional support, increasing Vital Farms’ cost to maintain shelf presence.

Losing a major chain would materially reduce distribution reach and sales velocity, so this retailer concentration heightens buyer power and execution risk for Vital Farms.

Shelf space and category management

Retailers curate limited egg and butter facings, intensifying competition for placement and often favoring private labels or higher‑margin SKUs; U.S. private‑label grocery share was about 18% in 2024. Vital Farms must fund promotions and trade spend—CPG trade spend averaged roughly 13% of net sales in 2024—to sustain velocity and space, which buyers leverage to extract better terms and allowances.

Price sensitivity tiers

Consumers segment into conventional, cage-free, organic and pasture-raised; pasture-raised often command 2–4x price premiums versus conventional, attracting premium shoppers who tolerate higher prices but switch when close substitutes narrow gaps. Trade-down risk increased during 2022–24 inflation (U.S. CPI ~3–4%), constraining shelf pricing. This tiered sensitivity moderates Vital Farms’ pricing power.

Brand equity and trust

Vital Farms’ ethical stance and transparent sourcing drive customer loyalty and some price inelasticity, supported by distribution in 20,000+ U.S. stores (2024). Strong brand reduces retailer substitution risk and increases leverage in joint marketing and assortment negotiations. Yet that loyalty must be defended through consistent quality and reliable supply.

- Ethical trust: stronger loyalty

- Retail leverage: better promo/assortment

- Distribution: 20,000+ stores (2024)

- Risk: quality consistency required

Data and omni-channel influence

Retail media networks and e-commerce rankings increasingly dictate product discovery and demand, with US retail media ad spend about $60B in 2024 concentrating placement power at major retailers. Buyers now expect data-sharing and performance guarantees, and retailers leverage these requirements to extract increased marketing investment from brands, boosting ongoing buyer negotiating power.

- Retail media spend: ~$60B (US, 2024)

- Top 4 retailers ≈70% grocery e‑commerce share

- Performance guarantees and data access drive price/placement leverage

Top grocers pricing and slotting power squeeze CPG margins despite wide store reach

Large grocers (Walmart ~25% of US grocery sales; Kroger ~9% in 2024) dominate shelf access and pricing. Retailers extract slotting/trade spend (CPG trade spend ≈13% of net sales) and private‑label share ≈18%, raising Vital Farms’ costs. Brand strength, 20,000+ store distribution and pasture‑premium pricing mitigate but retail media ($60B) and top‑4 ≈70% e‑comm share concentrate buyer power.

| Metric | 2024 |

|---|---|

| Walmart share | ~25% |

| CPG trade spend | ~13% net sales |

| Retail media spend | $60B |

What You See Is What You Get

Vital Farms Porter's Five Forces Analysis

This preview shows the exact Vital Farms Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. It’s the full, professionally formatted document ready for download and use the moment you buy. What you see is what you get.

Go Beyond the Preview—Access the Full Strategic Report

Vital Farms faces unique competitive dynamics—strong buyer awareness for ethical eggs, concentrated supplier risks in pasture-raised supply chains, and moderate threat from branded and private-label substitutes. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report for actionable insights and decision-ready guidance.

Suppliers Bargaining Power

Fragmented small-farm network

Most egg supply comes from a fragmented network of over 800 family farms as of 2024, so no single farm holds material leverage. Coordinated expectations around pasture standards and audits, however, let farmers exert collective influence on pricing and practices. Vital Farms must actively manage relationships and compliance to keep supply steady, giving suppliers measurable but soft bargaining power.

Welfare standards raise costs

Pasture-raised protocols demand more land, labor, and compliance, raising farm cost structures and contributing to industry feed and input cost shocks—feed costs rose roughly 20% from 2021–24, squeezing margins. Suppliers therefore press for price adjustments to cover these burdens, especially during cost spikes. Vital Farms’ brand depends on strict adherence to pasture standards, limiting its flexibility to trade down and enhancing supplier bargaining power.

Feed and input concentration

Feed, chicks, packaging and logistics for Vital Farms are procured from concentrated upstream markets, increasing supplier leverage; grain costs, for example, surged roughly 20–25% from 2021–23 and remained elevated into 2024, tightening margins for egg producers. When grain prices rise or supply tightens, input providers can demand higher prices or stricter terms, making cost pass-through to farms and retailers a core negotiation. This concentration thus amplifies supplier power cyclically, pressuring Vital Farms’ pricing and margin management.

Biosecurity, weather, and seasonality

Disease outbreaks and extreme weather constrain pasture-based output; as of 2024 USDA monitoring continued after more than 58 million poultry losses from HPAI through 2023, tightening supply and raising the value of compliant producers.

Vital Farms may pay premiums to secure volumes and continuity, so supply shocks and seasonality shift bargaining power toward suppliers, increasing input costs and contract leverage.

- Higher supplier leverage from disease/weather

- Premiums likely paid for continuity

- Compliance raises supplier value

- Seasonal swings amplify supply risk

Switching constraints and certification

Onboarding new farms requires audits, training and months to meet Vital Farms standards, creating switching frictions that raise dependence on existing suppliers. Farms certified to the brand’s pasture-raised and animal welfare specs are relatively scarce assets, strengthening their negotiating stance. This scarcity increases supplier bargaining power, especially during supply tightness or egg-price volatility.

- Onboarding friction: audits + training + months

- Certified farms: scarce, high-value suppliers

- Effect: stronger supplier leverage, potential input-cost pressure

HPAI cuts 58M, feed +20%, onboarding 3-6mo

Vital Farms sources from ~800 family farms (2024), giving individual farms low leverage but certified pasture-raised suppliers scarce; feed costs rose ~20% (2021–24) squeezing margins, and HPAI caused ~58M poultry losses through 2023, tightening supply and raising supplier power. Onboarding certified farms takes months, and premiums are often paid to secure continuity, amplifying supplier bargaining power.

| Metric | Value | Impact |

|---|---|---|

| Family farms | ~800 (2024) | Fragmented but scarce certified suppliers |

| Feed cost change | +~20% (2021–24) | Margin pressure |

| HPAI losses | ~58M (through 2023) | Supply tightening |

| Onboarding time | 3–6 months | Switching friction |

What is included in the product

Analyzes competitive forces shaping Vital Farms' market — supplier and buyer power, industry rivalry, substitutes, and entry threats — with strategic insights for investors and managers.

A one-sheet Porter's Five Forces for Vital Farms that clarifies competitive pressure and supplier dynamics at a glance—ideal for rapid strategy decisions and easy slide insertion.

Customers Bargaining Power

Retailer concentration

Large grocers control shelf access and pricing power; Walmart alone held about 25% of US grocery sales in 2024 and Kroger roughly 9%, concentrating influence over assortment and margins.

These chains routinely demand trade spend, slotting fees and promotional support, increasing Vital Farms’ cost to maintain shelf presence.

Losing a major chain would materially reduce distribution reach and sales velocity, so this retailer concentration heightens buyer power and execution risk for Vital Farms.

Shelf space and category management

Retailers curate limited egg and butter facings, intensifying competition for placement and often favoring private labels or higher‑margin SKUs; U.S. private‑label grocery share was about 18% in 2024. Vital Farms must fund promotions and trade spend—CPG trade spend averaged roughly 13% of net sales in 2024—to sustain velocity and space, which buyers leverage to extract better terms and allowances.

Price sensitivity tiers

Consumers segment into conventional, cage-free, organic and pasture-raised; pasture-raised often command 2–4x price premiums versus conventional, attracting premium shoppers who tolerate higher prices but switch when close substitutes narrow gaps. Trade-down risk increased during 2022–24 inflation (U.S. CPI ~3–4%), constraining shelf pricing. This tiered sensitivity moderates Vital Farms’ pricing power.

Brand equity and trust

Vital Farms’ ethical stance and transparent sourcing drive customer loyalty and some price inelasticity, supported by distribution in 20,000+ U.S. stores (2024). Strong brand reduces retailer substitution risk and increases leverage in joint marketing and assortment negotiations. Yet that loyalty must be defended through consistent quality and reliable supply.

- Ethical trust: stronger loyalty

- Retail leverage: better promo/assortment

- Distribution: 20,000+ stores (2024)

- Risk: quality consistency required

Data and omni-channel influence

Retail media networks and e-commerce rankings increasingly dictate product discovery and demand, with US retail media ad spend about $60B in 2024 concentrating placement power at major retailers. Buyers now expect data-sharing and performance guarantees, and retailers leverage these requirements to extract increased marketing investment from brands, boosting ongoing buyer negotiating power.

- Retail media spend: ~$60B (US, 2024)

- Top 4 retailers ≈70% grocery e‑commerce share

- Performance guarantees and data access drive price/placement leverage

Top grocers pricing and slotting power squeeze CPG margins despite wide store reach

Large grocers (Walmart ~25% of US grocery sales; Kroger ~9% in 2024) dominate shelf access and pricing. Retailers extract slotting/trade spend (CPG trade spend ≈13% of net sales) and private‑label share ≈18%, raising Vital Farms’ costs. Brand strength, 20,000+ store distribution and pasture‑premium pricing mitigate but retail media ($60B) and top‑4 ≈70% e‑comm share concentrate buyer power.

| Metric | 2024 |

|---|---|

| Walmart share | ~25% |

| CPG trade spend | ~13% net sales |

| Retail media spend | $60B |

What You See Is What You Get

Vital Farms Porter's Five Forces Analysis

This preview shows the exact Vital Farms Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. It’s the full, professionally formatted document ready for download and use the moment you buy. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Vital Farms faces unique competitive dynamics—strong buyer awareness for ethical eggs, concentrated supplier risks in pasture-raised supply chains, and moderate threat from branded and private-label substitutes. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications. Purchase the complete report for actionable insights and decision-ready guidance.

Suppliers Bargaining Power

Fragmented small-farm network

Most egg supply comes from a fragmented network of over 800 family farms as of 2024, so no single farm holds material leverage. Coordinated expectations around pasture standards and audits, however, let farmers exert collective influence on pricing and practices. Vital Farms must actively manage relationships and compliance to keep supply steady, giving suppliers measurable but soft bargaining power.

Welfare standards raise costs

Pasture-raised protocols demand more land, labor, and compliance, raising farm cost structures and contributing to industry feed and input cost shocks—feed costs rose roughly 20% from 2021–24, squeezing margins. Suppliers therefore press for price adjustments to cover these burdens, especially during cost spikes. Vital Farms’ brand depends on strict adherence to pasture standards, limiting its flexibility to trade down and enhancing supplier bargaining power.

Feed and input concentration

Feed, chicks, packaging and logistics for Vital Farms are procured from concentrated upstream markets, increasing supplier leverage; grain costs, for example, surged roughly 20–25% from 2021–23 and remained elevated into 2024, tightening margins for egg producers. When grain prices rise or supply tightens, input providers can demand higher prices or stricter terms, making cost pass-through to farms and retailers a core negotiation. This concentration thus amplifies supplier power cyclically, pressuring Vital Farms’ pricing and margin management.

Biosecurity, weather, and seasonality

Disease outbreaks and extreme weather constrain pasture-based output; as of 2024 USDA monitoring continued after more than 58 million poultry losses from HPAI through 2023, tightening supply and raising the value of compliant producers.

Vital Farms may pay premiums to secure volumes and continuity, so supply shocks and seasonality shift bargaining power toward suppliers, increasing input costs and contract leverage.

- Higher supplier leverage from disease/weather

- Premiums likely paid for continuity

- Compliance raises supplier value

- Seasonal swings amplify supply risk

Switching constraints and certification

Onboarding new farms requires audits, training and months to meet Vital Farms standards, creating switching frictions that raise dependence on existing suppliers. Farms certified to the brand’s pasture-raised and animal welfare specs are relatively scarce assets, strengthening their negotiating stance. This scarcity increases supplier bargaining power, especially during supply tightness or egg-price volatility.

- Onboarding friction: audits + training + months

- Certified farms: scarce, high-value suppliers

- Effect: stronger supplier leverage, potential input-cost pressure

HPAI cuts 58M, feed +20%, onboarding 3-6mo

Vital Farms sources from ~800 family farms (2024), giving individual farms low leverage but certified pasture-raised suppliers scarce; feed costs rose ~20% (2021–24) squeezing margins, and HPAI caused ~58M poultry losses through 2023, tightening supply and raising supplier power. Onboarding certified farms takes months, and premiums are often paid to secure continuity, amplifying supplier bargaining power.

| Metric | Value | Impact |

|---|---|---|

| Family farms | ~800 (2024) | Fragmented but scarce certified suppliers |

| Feed cost change | +~20% (2021–24) | Margin pressure |

| HPAI losses | ~58M (through 2023) | Supply tightening |

| Onboarding time | 3–6 months | Switching friction |

What is included in the product

Analyzes competitive forces shaping Vital Farms' market — supplier and buyer power, industry rivalry, substitutes, and entry threats — with strategic insights for investors and managers.

A one-sheet Porter's Five Forces for Vital Farms that clarifies competitive pressure and supplier dynamics at a glance—ideal for rapid strategy decisions and easy slide insertion.

Customers Bargaining Power

Retailer concentration

Large grocers control shelf access and pricing power; Walmart alone held about 25% of US grocery sales in 2024 and Kroger roughly 9%, concentrating influence over assortment and margins.

These chains routinely demand trade spend, slotting fees and promotional support, increasing Vital Farms’ cost to maintain shelf presence.

Losing a major chain would materially reduce distribution reach and sales velocity, so this retailer concentration heightens buyer power and execution risk for Vital Farms.

Shelf space and category management

Retailers curate limited egg and butter facings, intensifying competition for placement and often favoring private labels or higher‑margin SKUs; U.S. private‑label grocery share was about 18% in 2024. Vital Farms must fund promotions and trade spend—CPG trade spend averaged roughly 13% of net sales in 2024—to sustain velocity and space, which buyers leverage to extract better terms and allowances.

Price sensitivity tiers

Consumers segment into conventional, cage-free, organic and pasture-raised; pasture-raised often command 2–4x price premiums versus conventional, attracting premium shoppers who tolerate higher prices but switch when close substitutes narrow gaps. Trade-down risk increased during 2022–24 inflation (U.S. CPI ~3–4%), constraining shelf pricing. This tiered sensitivity moderates Vital Farms’ pricing power.

Brand equity and trust

Vital Farms’ ethical stance and transparent sourcing drive customer loyalty and some price inelasticity, supported by distribution in 20,000+ U.S. stores (2024). Strong brand reduces retailer substitution risk and increases leverage in joint marketing and assortment negotiations. Yet that loyalty must be defended through consistent quality and reliable supply.

- Ethical trust: stronger loyalty

- Retail leverage: better promo/assortment

- Distribution: 20,000+ stores (2024)

- Risk: quality consistency required

Data and omni-channel influence

Retail media networks and e-commerce rankings increasingly dictate product discovery and demand, with US retail media ad spend about $60B in 2024 concentrating placement power at major retailers. Buyers now expect data-sharing and performance guarantees, and retailers leverage these requirements to extract increased marketing investment from brands, boosting ongoing buyer negotiating power.

- Retail media spend: ~$60B (US, 2024)

- Top 4 retailers ≈70% grocery e‑commerce share

- Performance guarantees and data access drive price/placement leverage

Top grocers pricing and slotting power squeeze CPG margins despite wide store reach

Large grocers (Walmart ~25% of US grocery sales; Kroger ~9% in 2024) dominate shelf access and pricing. Retailers extract slotting/trade spend (CPG trade spend ≈13% of net sales) and private‑label share ≈18%, raising Vital Farms’ costs. Brand strength, 20,000+ store distribution and pasture‑premium pricing mitigate but retail media ($60B) and top‑4 ≈70% e‑comm share concentrate buyer power.

| Metric | 2024 |

|---|---|

| Walmart share | ~25% |

| CPG trade spend | ~13% net sales |

| Retail media spend | $60B |

What You See Is What You Get

Vital Farms Porter's Five Forces Analysis

This preview shows the exact Vital Farms Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples. It’s the full, professionally formatted document ready for download and use the moment you buy. What you see is what you get.