Vitesse Energy Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Vitesse Energy faces moderate supplier power, growing buyer scrutiny, and intensifying rivalry as renewable incumbents scale; regulatory shifts and tech substitution heighten external pressure. This brief snapshot only scratches the surface—unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy tailored to Vitesse Energy.

Suppliers Bargaining Power

Operator concentration risk

As a non-operator, Vitesse depends on a concentrated set of Williston Basin operators who set AFEs, schedules and design standards, constraining Vitesse’s negotiating leverage. In 2024 the top five operators accounted for approximately 60% of basin production, amplifying their pricing and timing power. Ongoing consolidation has increased operator clout, and while spreading activity across operators reduces exposure, structural dependence persists.

Oilfield services and labor tightness

Drilling, completion, and workover capacity tightened in 2024 as Baker Hughes reported the US rig count climbing to about 730 by late 2024, allowing service firms and specialized crews to command premium pricing that raises well costs Vitesse must accept through AFEs. Efficiency gains from pad drilling and digitalization can offset some margin pressure, but timing and quality risk shifts to non-operators. Local weather and seasonality, notably Rockies winters and Gulf hurricane season, further exacerbate scarcity.

Midstream and takeaway constraints

Pipelines, gas processing and water-handling firms often have localized monopoly power, especially in basins like the Permian where 2024 takeaway constraints kept differentials at several dollars per barrel; fees and flaring limits therefore directly depress realized prices and volumes. Capacity tightness lets midstream set higher tariffs and restrict deliveries, while connection timing—set by operators and midstream—can delay cash flow by weeks to months. Long-term takeaway and processing contracts are typically sticky, often exceeding five years, and are hard to renegotiate without a material change of circumstance.

Mineral/leasehold availability

Capital and hedging counterparties

Credit providers and hedge counterparties strongly influence Vitesse Energy’s liquidity and risk management; in 2024 Brent averaged about 86 USD/bbl, keeping hedging activity elevated and funding needs large. In volatile periods counterparties raised collateral demands and widened bid-ask spreads, increasing hedging and roll costs; exchanges and brokers increased energy margins by up to 40% at times in 2022–24. Counterparty selectivity narrows options for smaller non-ops, and strong balance sheets reduce but do not remove this leverage.

- Credit concentration: limits access for smaller firms

- Collateral/margin: up to 40% higher (2022–24 peak)

- Market volatility: 2024 Brent ~86 USD/bbl

- Balance sheet: mitigates but does not eliminate counterparty leverage

Top-five operators drove ~60% of Williston; rigs ~730, Brent ~86 USD/bbl

Vitesse’s supplier leverage is high: top-five operators drove ~60% of Williston output in 2024, concentrating AFE and schedule power. Tight service capacity (US rig count ~730 late 2024) and midstream bottlenecks raised costs and tariffs; Brent averaged ~86 USD/bbl in 2024, keeping hedging and collateral needs elevated.

| Metric | 2024 |

|---|---|

| Top-5 operator share | ~60% |

| US rig count | ~730 |

| Brent | ~86 USD/bbl |

What is included in the product

Comprehensive Porter's Five Forces analysis for Vitesse Energy that uncovers competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and strategic levers to defend margins and market position.

A clear one-sheet summary of Vitesse Energy's Five Forces for quick decision-making, with customizable pressure levels and an instant spider chart to visualize strategic pressure—clean layout ready for pitch decks and seamless Excel integration.

Customers Bargaining Power

Commodity price takers

Vitesse sells into global commodity markets where benchmarks like Brent and Henry Hub — with world oil demand ~101.5 million barrels per day in 2024 — let buyers set prices, leaving individual producers price takers. Individual producers have minimal ability to influence crude and gas pricing, giving high aggregate buyer power. Realized differentials, often amounting to several dollars per barrel, reflect buyer preferences and logistics.

Refiners and marketers concentration

Regional refiners, marketers and gas processors can be highly concentrated for certain crude grades, and U.S. refinery capacity stood at about 19 million barrels per day (EIA 2024), underscoring limited local demand outlets. Limited buyers can compress netbacks through grade-specific discounts, while dedicated offtake secures sales but entrenches contracted pricing formulas. Buyer competition and discounting ebb and flow with macro cycles, widening in tight markets and narrowing in oversupply.

Quality and spec sensitivity

Buyers pay premiums for consistent gravity and low contaminants; pipeline gas specs typically center around 1,030 BTU/ft3 (±20 BTU), and deviations widen differentials. Variability from field mix or processing shifts BTU and NGL yields, with NGL content often accounting for up to 5–10% of product value. Strict buyer specs raise sellers’ switching costs while strengthening buyer-negotiated terms.

Logistics dependence

Pipeline nominations, rail access and trucking availability determine buyer leverage for Vitesse Energy; regions with takeaway utilization above 90% in 2024 saw sharper buyer discounts as constrained nominations allowed purchasers to press for lower field prices. Multiple outlets—rail, truck, terminal or pipeline—reduce dependence on any single buyer and compress negotiating power. Scheduling control often rests with midstream-linked buyers who set nomination windows and fees.

- Takeaway utilization >90% raises buyer leverage

- Multiple outlets lower single-buyer dependence

- Midstream-linked buyers control scheduling/nominations

Hedged sales dynamics

Hedging locks in prices but basis and counterparty terms often favor financial buyers, concentrating negotiating leverage; while hedges reduce volatility they also cap upside, with Henry Hub averaging about 3.00 $/MMBtu in 2024. Margining requirements can strain liquidity in adverse moves, and buyers of hedged volumes gain predictability, strengthening their position.

- Basis differentials: 0.10–0.30 $/MMBtu typical

- 2024 Henry Hub avg: ~3.00 $/MMBtu

- Margin risk: higher cash calls in stress

- Buyer leverage: improved forecasting and planning

Buyers seize leverage: 101.5 mbpd demand, refineries >90% utilized

Buyers have high leverage: global benchmarks (Brent, Henry Hub) make producers price takers; world oil demand ~101.5 mbpd (2024) and U.S. refinery capacity ~19 mbpd concentrate purchasing power. Takeaway constraints (>90% utilization) and concentrated refiners compress netbacks; hedging (Henry Hub ~3.00 $/MMBtu in 2024) limits upside and favors sophisticated buyers.

| Metric | 2024 |

|---|---|

| World oil demand | 101.5 mbpd |

| US refinery cap | 19 mbpd |

| Henry Hub avg | $3.00/MMBtu |

| Takeaway utilization | >90% raises buyer leverage |

Preview Before You Purchase

Vitesse Energy Porter's Five Forces Analysis

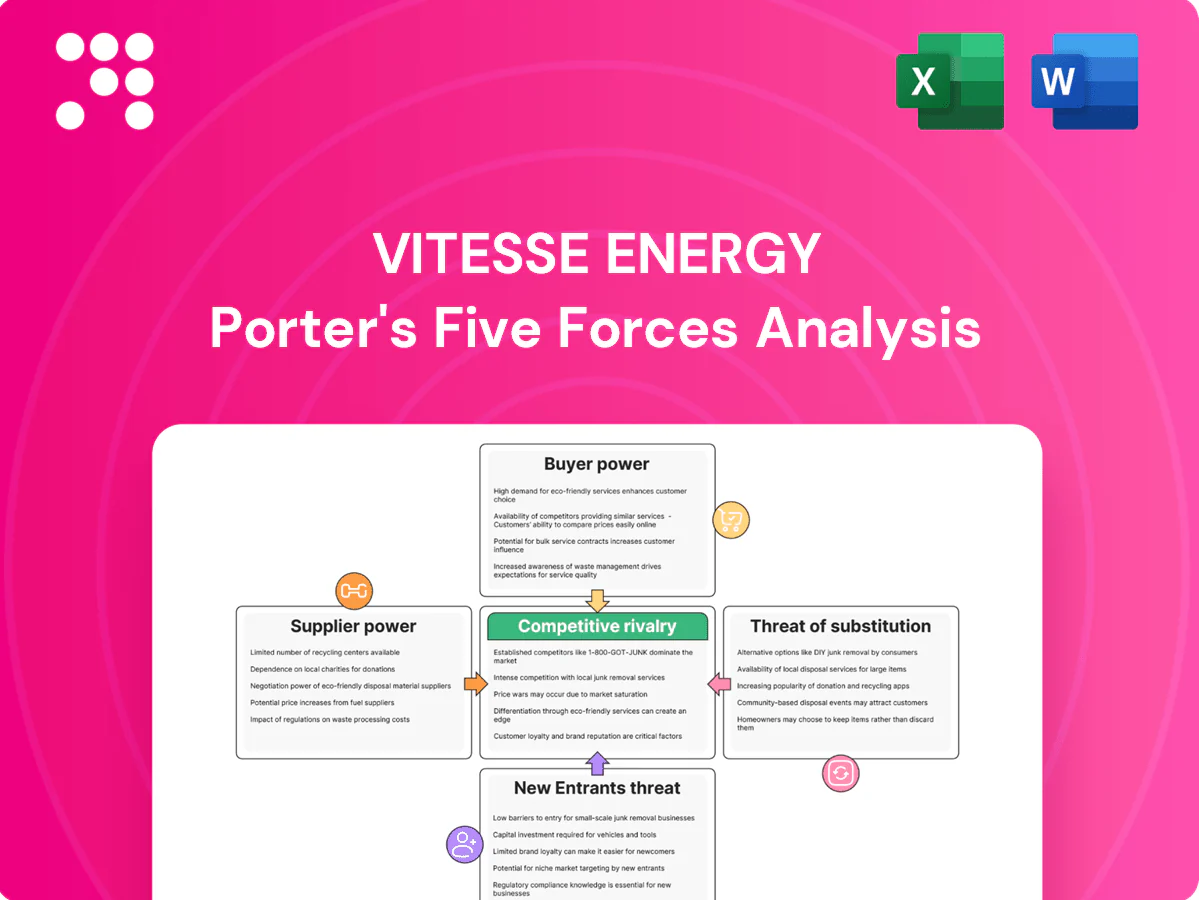

This preview shows the exact Vitesse Energy Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The analysis addresses competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications for Vitesse Energy.

Don't Miss the Bigger Picture

Vitesse Energy faces moderate supplier power, growing buyer scrutiny, and intensifying rivalry as renewable incumbents scale; regulatory shifts and tech substitution heighten external pressure. This brief snapshot only scratches the surface—unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy tailored to Vitesse Energy.

Suppliers Bargaining Power

Operator concentration risk

As a non-operator, Vitesse depends on a concentrated set of Williston Basin operators who set AFEs, schedules and design standards, constraining Vitesse’s negotiating leverage. In 2024 the top five operators accounted for approximately 60% of basin production, amplifying their pricing and timing power. Ongoing consolidation has increased operator clout, and while spreading activity across operators reduces exposure, structural dependence persists.

Oilfield services and labor tightness

Drilling, completion, and workover capacity tightened in 2024 as Baker Hughes reported the US rig count climbing to about 730 by late 2024, allowing service firms and specialized crews to command premium pricing that raises well costs Vitesse must accept through AFEs. Efficiency gains from pad drilling and digitalization can offset some margin pressure, but timing and quality risk shifts to non-operators. Local weather and seasonality, notably Rockies winters and Gulf hurricane season, further exacerbate scarcity.

Midstream and takeaway constraints

Pipelines, gas processing and water-handling firms often have localized monopoly power, especially in basins like the Permian where 2024 takeaway constraints kept differentials at several dollars per barrel; fees and flaring limits therefore directly depress realized prices and volumes. Capacity tightness lets midstream set higher tariffs and restrict deliveries, while connection timing—set by operators and midstream—can delay cash flow by weeks to months. Long-term takeaway and processing contracts are typically sticky, often exceeding five years, and are hard to renegotiate without a material change of circumstance.

Mineral/leasehold availability

Capital and hedging counterparties

Credit providers and hedge counterparties strongly influence Vitesse Energy’s liquidity and risk management; in 2024 Brent averaged about 86 USD/bbl, keeping hedging activity elevated and funding needs large. In volatile periods counterparties raised collateral demands and widened bid-ask spreads, increasing hedging and roll costs; exchanges and brokers increased energy margins by up to 40% at times in 2022–24. Counterparty selectivity narrows options for smaller non-ops, and strong balance sheets reduce but do not remove this leverage.

- Credit concentration: limits access for smaller firms

- Collateral/margin: up to 40% higher (2022–24 peak)

- Market volatility: 2024 Brent ~86 USD/bbl

- Balance sheet: mitigates but does not eliminate counterparty leverage

Top-five operators drove ~60% of Williston; rigs ~730, Brent ~86 USD/bbl

Vitesse’s supplier leverage is high: top-five operators drove ~60% of Williston output in 2024, concentrating AFE and schedule power. Tight service capacity (US rig count ~730 late 2024) and midstream bottlenecks raised costs and tariffs; Brent averaged ~86 USD/bbl in 2024, keeping hedging and collateral needs elevated.

| Metric | 2024 |

|---|---|

| Top-5 operator share | ~60% |

| US rig count | ~730 |

| Brent | ~86 USD/bbl |

What is included in the product

Comprehensive Porter's Five Forces analysis for Vitesse Energy that uncovers competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and strategic levers to defend margins and market position.

A clear one-sheet summary of Vitesse Energy's Five Forces for quick decision-making, with customizable pressure levels and an instant spider chart to visualize strategic pressure—clean layout ready for pitch decks and seamless Excel integration.

Customers Bargaining Power

Commodity price takers

Vitesse sells into global commodity markets where benchmarks like Brent and Henry Hub — with world oil demand ~101.5 million barrels per day in 2024 — let buyers set prices, leaving individual producers price takers. Individual producers have minimal ability to influence crude and gas pricing, giving high aggregate buyer power. Realized differentials, often amounting to several dollars per barrel, reflect buyer preferences and logistics.

Refiners and marketers concentration

Regional refiners, marketers and gas processors can be highly concentrated for certain crude grades, and U.S. refinery capacity stood at about 19 million barrels per day (EIA 2024), underscoring limited local demand outlets. Limited buyers can compress netbacks through grade-specific discounts, while dedicated offtake secures sales but entrenches contracted pricing formulas. Buyer competition and discounting ebb and flow with macro cycles, widening in tight markets and narrowing in oversupply.

Quality and spec sensitivity

Buyers pay premiums for consistent gravity and low contaminants; pipeline gas specs typically center around 1,030 BTU/ft3 (±20 BTU), and deviations widen differentials. Variability from field mix or processing shifts BTU and NGL yields, with NGL content often accounting for up to 5–10% of product value. Strict buyer specs raise sellers’ switching costs while strengthening buyer-negotiated terms.

Logistics dependence

Pipeline nominations, rail access and trucking availability determine buyer leverage for Vitesse Energy; regions with takeaway utilization above 90% in 2024 saw sharper buyer discounts as constrained nominations allowed purchasers to press for lower field prices. Multiple outlets—rail, truck, terminal or pipeline—reduce dependence on any single buyer and compress negotiating power. Scheduling control often rests with midstream-linked buyers who set nomination windows and fees.

- Takeaway utilization >90% raises buyer leverage

- Multiple outlets lower single-buyer dependence

- Midstream-linked buyers control scheduling/nominations

Hedged sales dynamics

Hedging locks in prices but basis and counterparty terms often favor financial buyers, concentrating negotiating leverage; while hedges reduce volatility they also cap upside, with Henry Hub averaging about 3.00 $/MMBtu in 2024. Margining requirements can strain liquidity in adverse moves, and buyers of hedged volumes gain predictability, strengthening their position.

- Basis differentials: 0.10–0.30 $/MMBtu typical

- 2024 Henry Hub avg: ~3.00 $/MMBtu

- Margin risk: higher cash calls in stress

- Buyer leverage: improved forecasting and planning

Buyers seize leverage: 101.5 mbpd demand, refineries >90% utilized

Buyers have high leverage: global benchmarks (Brent, Henry Hub) make producers price takers; world oil demand ~101.5 mbpd (2024) and U.S. refinery capacity ~19 mbpd concentrate purchasing power. Takeaway constraints (>90% utilization) and concentrated refiners compress netbacks; hedging (Henry Hub ~3.00 $/MMBtu in 2024) limits upside and favors sophisticated buyers.

| Metric | 2024 |

|---|---|

| World oil demand | 101.5 mbpd |

| US refinery cap | 19 mbpd |

| Henry Hub avg | $3.00/MMBtu |

| Takeaway utilization | >90% raises buyer leverage |

Preview Before You Purchase

Vitesse Energy Porter's Five Forces Analysis

This preview shows the exact Vitesse Energy Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The analysis addresses competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications for Vitesse Energy.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Vitesse Energy faces moderate supplier power, growing buyer scrutiny, and intensifying rivalry as renewable incumbents scale; regulatory shifts and tech substitution heighten external pressure. This brief snapshot only scratches the surface—unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy tailored to Vitesse Energy.

Suppliers Bargaining Power

Operator concentration risk

As a non-operator, Vitesse depends on a concentrated set of Williston Basin operators who set AFEs, schedules and design standards, constraining Vitesse’s negotiating leverage. In 2024 the top five operators accounted for approximately 60% of basin production, amplifying their pricing and timing power. Ongoing consolidation has increased operator clout, and while spreading activity across operators reduces exposure, structural dependence persists.

Oilfield services and labor tightness

Drilling, completion, and workover capacity tightened in 2024 as Baker Hughes reported the US rig count climbing to about 730 by late 2024, allowing service firms and specialized crews to command premium pricing that raises well costs Vitesse must accept through AFEs. Efficiency gains from pad drilling and digitalization can offset some margin pressure, but timing and quality risk shifts to non-operators. Local weather and seasonality, notably Rockies winters and Gulf hurricane season, further exacerbate scarcity.

Midstream and takeaway constraints

Pipelines, gas processing and water-handling firms often have localized monopoly power, especially in basins like the Permian where 2024 takeaway constraints kept differentials at several dollars per barrel; fees and flaring limits therefore directly depress realized prices and volumes. Capacity tightness lets midstream set higher tariffs and restrict deliveries, while connection timing—set by operators and midstream—can delay cash flow by weeks to months. Long-term takeaway and processing contracts are typically sticky, often exceeding five years, and are hard to renegotiate without a material change of circumstance.

Mineral/leasehold availability

Capital and hedging counterparties

Credit providers and hedge counterparties strongly influence Vitesse Energy’s liquidity and risk management; in 2024 Brent averaged about 86 USD/bbl, keeping hedging activity elevated and funding needs large. In volatile periods counterparties raised collateral demands and widened bid-ask spreads, increasing hedging and roll costs; exchanges and brokers increased energy margins by up to 40% at times in 2022–24. Counterparty selectivity narrows options for smaller non-ops, and strong balance sheets reduce but do not remove this leverage.

- Credit concentration: limits access for smaller firms

- Collateral/margin: up to 40% higher (2022–24 peak)

- Market volatility: 2024 Brent ~86 USD/bbl

- Balance sheet: mitigates but does not eliminate counterparty leverage

Top-five operators drove ~60% of Williston; rigs ~730, Brent ~86 USD/bbl

Vitesse’s supplier leverage is high: top-five operators drove ~60% of Williston output in 2024, concentrating AFE and schedule power. Tight service capacity (US rig count ~730 late 2024) and midstream bottlenecks raised costs and tariffs; Brent averaged ~86 USD/bbl in 2024, keeping hedging and collateral needs elevated.

| Metric | 2024 |

|---|---|

| Top-5 operator share | ~60% |

| US rig count | ~730 |

| Brent | ~86 USD/bbl |

What is included in the product

Comprehensive Porter's Five Forces analysis for Vitesse Energy that uncovers competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and strategic levers to defend margins and market position.

A clear one-sheet summary of Vitesse Energy's Five Forces for quick decision-making, with customizable pressure levels and an instant spider chart to visualize strategic pressure—clean layout ready for pitch decks and seamless Excel integration.

Customers Bargaining Power

Commodity price takers

Vitesse sells into global commodity markets where benchmarks like Brent and Henry Hub — with world oil demand ~101.5 million barrels per day in 2024 — let buyers set prices, leaving individual producers price takers. Individual producers have minimal ability to influence crude and gas pricing, giving high aggregate buyer power. Realized differentials, often amounting to several dollars per barrel, reflect buyer preferences and logistics.

Refiners and marketers concentration

Regional refiners, marketers and gas processors can be highly concentrated for certain crude grades, and U.S. refinery capacity stood at about 19 million barrels per day (EIA 2024), underscoring limited local demand outlets. Limited buyers can compress netbacks through grade-specific discounts, while dedicated offtake secures sales but entrenches contracted pricing formulas. Buyer competition and discounting ebb and flow with macro cycles, widening in tight markets and narrowing in oversupply.

Quality and spec sensitivity

Buyers pay premiums for consistent gravity and low contaminants; pipeline gas specs typically center around 1,030 BTU/ft3 (±20 BTU), and deviations widen differentials. Variability from field mix or processing shifts BTU and NGL yields, with NGL content often accounting for up to 5–10% of product value. Strict buyer specs raise sellers’ switching costs while strengthening buyer-negotiated terms.

Logistics dependence

Pipeline nominations, rail access and trucking availability determine buyer leverage for Vitesse Energy; regions with takeaway utilization above 90% in 2024 saw sharper buyer discounts as constrained nominations allowed purchasers to press for lower field prices. Multiple outlets—rail, truck, terminal or pipeline—reduce dependence on any single buyer and compress negotiating power. Scheduling control often rests with midstream-linked buyers who set nomination windows and fees.

- Takeaway utilization >90% raises buyer leverage

- Multiple outlets lower single-buyer dependence

- Midstream-linked buyers control scheduling/nominations

Hedged sales dynamics

Hedging locks in prices but basis and counterparty terms often favor financial buyers, concentrating negotiating leverage; while hedges reduce volatility they also cap upside, with Henry Hub averaging about 3.00 $/MMBtu in 2024. Margining requirements can strain liquidity in adverse moves, and buyers of hedged volumes gain predictability, strengthening their position.

- Basis differentials: 0.10–0.30 $/MMBtu typical

- 2024 Henry Hub avg: ~3.00 $/MMBtu

- Margin risk: higher cash calls in stress

- Buyer leverage: improved forecasting and planning

Buyers seize leverage: 101.5 mbpd demand, refineries >90% utilized

Buyers have high leverage: global benchmarks (Brent, Henry Hub) make producers price takers; world oil demand ~101.5 mbpd (2024) and U.S. refinery capacity ~19 mbpd concentrate purchasing power. Takeaway constraints (>90% utilization) and concentrated refiners compress netbacks; hedging (Henry Hub ~3.00 $/MMBtu in 2024) limits upside and favors sophisticated buyers.

| Metric | 2024 |

|---|---|

| World oil demand | 101.5 mbpd |

| US refinery cap | 19 mbpd |

| Henry Hub avg | $3.00/MMBtu |

| Takeaway utilization | >90% raises buyer leverage |

Preview Before You Purchase

Vitesse Energy Porter's Five Forces Analysis

This preview shows the exact Vitesse Energy Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. It is the full, professionally formatted document, ready for download and use the moment you buy. The analysis addresses competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications for Vitesse Energy.