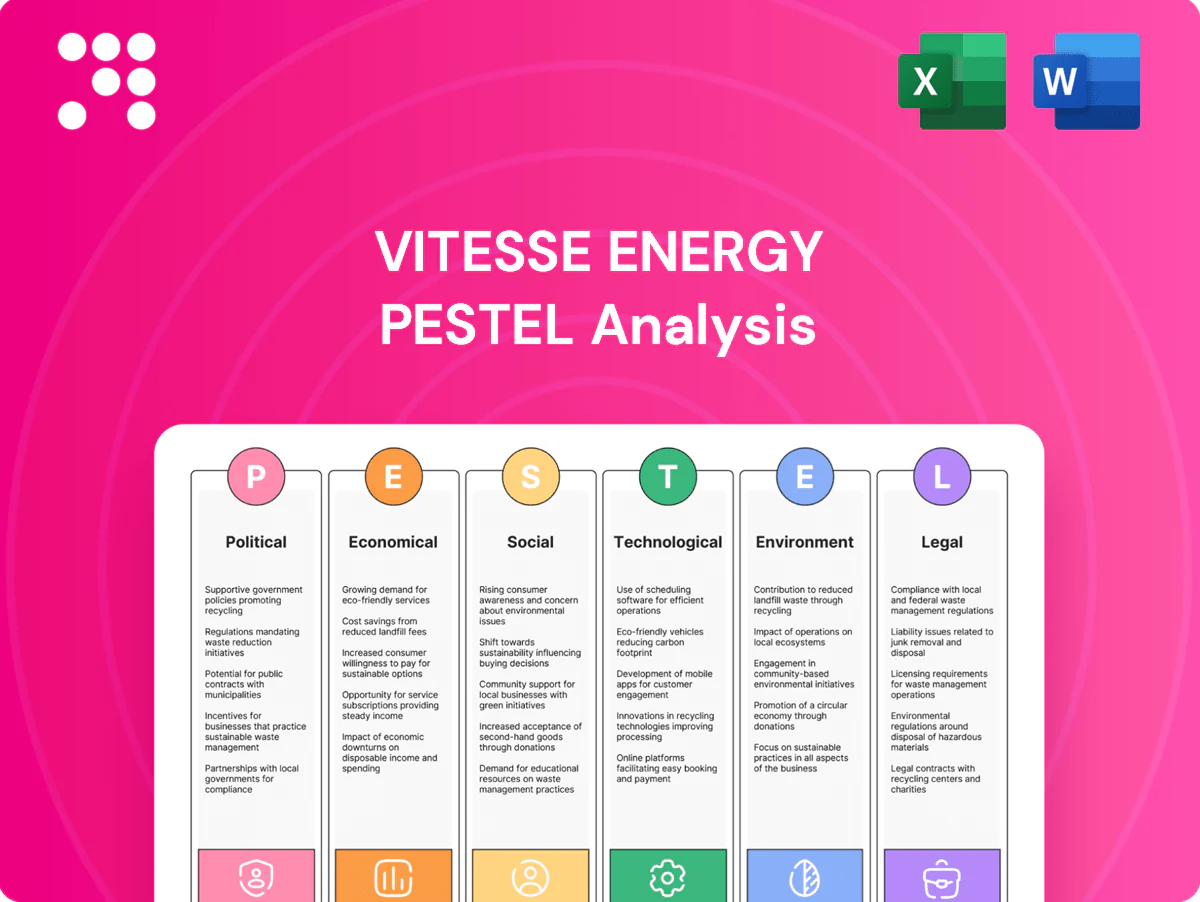

Vitesse Energy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological advances are shaping Vitesse Energy’s strategic landscape in our targeted PESTLE analysis. This concise, expert-grade report highlights risks and growth levers you can act on now. Purchase the full PESTLE to access detailed, ready-to-use insights and strengthen your investment or strategy decisions.

Political factors

Federal energy policy shifts

Changes in federal leasing, permitting and emissions policy can quickly shift development pace and costs for Bakken assets, where regional crude output stood around 1.2 million b/d in 2024 versus US production ~12.8 million b/d. As a non-operator, Vitesse is exposed to partners’ compliance timing and cost pass-throughs. Administration swings drive pipeline approvals, methane rules and tax incentives, and policy predictability is critical for acquisition underwriting and free-cash-flow visibility.

State-level regimes ND and MT

North Dakota (Bakken ~1.1 million b/d) and Montana (~40 kb/d) set drilling, spacing, flaring and reclamation rules that dictate well timing and economics; ND Industrial Commission rulings directly shape Bakken development intensity. Changes to severance tax rates or flaring limits materially shift operator netbacks and capex cadence, altering non-operated AFE timing. Regulatory stability supports predictable non-op AFE cycles and capital planning.

Infrastructure politics and pipelines

Pipeline permitting and controversies such as Dakota Access Pipeline (DAPL) affect takeaway capacity and differentials; DAPL capacity is about 570,000 barrels per day. Political backing for midstream expansions can reduce bottlenecks and price discounts, while permitting delays widen differentials. Delays have historically shifted volumes to crude-by-rail—peaking at about 1.2 million bpd in 2014—raising costs and risks. Vitesse’s realized pricing depends on operators securing reliable transport routes.

Local government and community stance

County-level road-use agreements, impact fees and siting approvals in 2025 materially shape Vitesse Energy’s execution logistics, determining haul routes, timing and cost exposure; positive local relations can accelerate permit timelines and cut non-technical delays to weeks rather than months. Opposition raises mitigation, monitoring and community benefit obligations, increasing operating costs. Non-operators depend on partners’ on-the-ground engagement to preserve access and social license.

- Road-use & siting: local approvals dictate logistics

- Permitting: good relations shorten timelines

- Opposition: higher mitigation/monitoring costs

- Non-operators: rely on partner community engagement

Geopolitical supply shocks

Geopolitical supply shocks—notably OPEC+ cuts of ~2.2 million b/d and lingering Russia-related disruptions—drive WTI/Brent swings and crack-spread volatility, with intra-year price moves exceeding 20% in 2024. Those swings alter operator activity cycles, shifting Vitesse volumes and AFEs; higher sanctions-driven tightness can expand cash margins while demand shocks compress drilling and distributions.

- OPEC+ cuts ~2.2m b/d

- US crude ~13.1m b/d (2024)

- Price volatility >20% (2024)

Bakken costs surge as over 20% 2024 price swings and pipeline limits bite

Federal leasing, methane and tax policy shifts alter Bakken development costs and timing; regional output ~1.2m b/d (2024) vs US ~13.1m b/d. State/local rules (ND ~1.1m b/d, MT ~40kb/d) and road-use fees affect capex cadence for non-operators. Pipeline bottlenecks (DAPL 570kb/d) and OPEC+ cuts ~2.2m b/d drive >20% price swings in 2024, impacting realized pricing and AFEs.

| Factor | Key metric |

|---|---|

| Bakken output | ~1.2m b/d (2024) |

| DAPL capacity | 570k b/d |

| OPEC+ cuts | ~2.2m b/d |

| US crude | ~13.1m b/d (2024) |

What is included in the product

Explores how macro-environmental factors uniquely impact Vitesse Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific context. Designed for executives and investors to identify actionable threats, opportunities, and forward-looking scenarios for strategy and funding decisions.

A concise, visually segmented PESTLE summary for Vitesse Energy that streamlines meeting prep, is easily editable for regional or business-line notes, and can be dropped into presentations or shared across teams to align on external risks and strategic positioning.

Economic factors

WTI price volatility and basis

Bakken realizations track WTI, which averaged about $78/bbl in H1 2025, with regional Williston basis differentials historically ranging from -5 to -20/bbl. Wider Williston discounts compress margins and slow capital-efficient development. Improved takeaway since 2024 narrowed basis toward -5/bbl, materially boosting free cash flow. A disciplined hedging program smooths cash yields amid WTI and basis swings.

Service cost inflation/deflation

Pressure pumping, rigs and tubulars can drive up to 30% or more of total well costs, so service-cost inflation directly raises operator AFEs and erodes returns. A 10% rise in service pricing can materially cut projected IRRs on new wells, while deflation can quickly re-open idle inventory and boost activity. As a non-operator, Vitesse’s exposure is indirect but still material to capital efficiency and unit economics. Cycle-aware acquisition pricing is therefore critical to preserve returns across commodity and service cycles.

Capital markets and rates

Rising benchmark rates (Fed funds 5.25–5.50% and US 10-yr around 4.2% in mid-2025) raise borrowing costs and compress E&P equity valuations, reducing drilling budgets and non-op growth when credit tightens. Companies with strong cash generation and net debt/EBITDA under ~1.5x show greater resilience and M&A optionality. Narrow market windows driven by yields dictate timing for asset acquisitions and divestitures.

M&A and mineral/working interest market

M&A and non-operated working interest availability and pricing set Vitesse Energy’s external growth ceiling; U.S. upstream divestiture volumes topped roughly $20bn in 2024, intensifying competitive bidding and compressing returns.

Disciplined underwriting preserves FCF per share while portfolio high-grading—targeting higher-margin wells—reduces decline and lifts cash margins.

Counterparty quality drives execution risk and timely payouts, materially affecting realized proceeds.

- Market volume: ~ $20bn (2024)

- Competitive bids compress IRR

- High-grading cuts decline, boosts margins

- Counterparty credit = payout certainty

Production declines and terminal value

Shale wells commonly exhibit 60–70% first-year declines, front-loading returns and compressing long-term production.

Maintaining a PDP-heavy vs PUD mix stabilizes near-term cash while PUDs drive growth; portfolio balance affects cashflow volatility.

Refrac and infill can extend asset life and lift EURs by ~20–40%, so decline-rate assumptions directly drive NAV and dividend sustainability.

- decline-rate: 60–70% 1st year

- EUR uplift (refrac/infill): ~20–40%

- PDP/PUD mix: tradeoff cash stability vs growth

Bakken costs surge as over 20% 2024 price swings and pipeline limits bite

WTI averaged ~$78/bbl H1 2025 with Williston basis -5 to -20/bbl; improved takeaway since 2024 narrowed basis toward -5, boosting FCF. Service inflation (pressure pumping/rigs/tubulars ~30% of well cost) and Fed funds 5.25–5.50%/US10yr ~4.2% raise breakevens; 2024 US upstream divestitures ~ $20bn. First-year declines 60–70%; refrac/infill can lift EURs ~20–40%.

| Metric | Value |

|---|---|

| WTI H1 2025 | $78/bbl |

| Williston basis | -5 to -20 /bbl |

| Service cost share | ~30% |

| Fed funds / US10yr | 5.25–5.50% / ~4.2% |

| 2024 divestitures | ~$20bn |

What You See Is What You Get

Vitesse Energy PESTLE Analysis

The preview shown here is the exact Vitesse Energy PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, sociocultural, technological, legal and environmental assessment tailored to Vitesse Energy. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase. Downloadable immediately after payment.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological advances are shaping Vitesse Energy’s strategic landscape in our targeted PESTLE analysis. This concise, expert-grade report highlights risks and growth levers you can act on now. Purchase the full PESTLE to access detailed, ready-to-use insights and strengthen your investment or strategy decisions.

Political factors

Federal energy policy shifts

Changes in federal leasing, permitting and emissions policy can quickly shift development pace and costs for Bakken assets, where regional crude output stood around 1.2 million b/d in 2024 versus US production ~12.8 million b/d. As a non-operator, Vitesse is exposed to partners’ compliance timing and cost pass-throughs. Administration swings drive pipeline approvals, methane rules and tax incentives, and policy predictability is critical for acquisition underwriting and free-cash-flow visibility.

State-level regimes ND and MT

North Dakota (Bakken ~1.1 million b/d) and Montana (~40 kb/d) set drilling, spacing, flaring and reclamation rules that dictate well timing and economics; ND Industrial Commission rulings directly shape Bakken development intensity. Changes to severance tax rates or flaring limits materially shift operator netbacks and capex cadence, altering non-operated AFE timing. Regulatory stability supports predictable non-op AFE cycles and capital planning.

Infrastructure politics and pipelines

Pipeline permitting and controversies such as Dakota Access Pipeline (DAPL) affect takeaway capacity and differentials; DAPL capacity is about 570,000 barrels per day. Political backing for midstream expansions can reduce bottlenecks and price discounts, while permitting delays widen differentials. Delays have historically shifted volumes to crude-by-rail—peaking at about 1.2 million bpd in 2014—raising costs and risks. Vitesse’s realized pricing depends on operators securing reliable transport routes.

Local government and community stance

County-level road-use agreements, impact fees and siting approvals in 2025 materially shape Vitesse Energy’s execution logistics, determining haul routes, timing and cost exposure; positive local relations can accelerate permit timelines and cut non-technical delays to weeks rather than months. Opposition raises mitigation, monitoring and community benefit obligations, increasing operating costs. Non-operators depend on partners’ on-the-ground engagement to preserve access and social license.

- Road-use & siting: local approvals dictate logistics

- Permitting: good relations shorten timelines

- Opposition: higher mitigation/monitoring costs

- Non-operators: rely on partner community engagement

Geopolitical supply shocks

Geopolitical supply shocks—notably OPEC+ cuts of ~2.2 million b/d and lingering Russia-related disruptions—drive WTI/Brent swings and crack-spread volatility, with intra-year price moves exceeding 20% in 2024. Those swings alter operator activity cycles, shifting Vitesse volumes and AFEs; higher sanctions-driven tightness can expand cash margins while demand shocks compress drilling and distributions.

- OPEC+ cuts ~2.2m b/d

- US crude ~13.1m b/d (2024)

- Price volatility >20% (2024)

Bakken costs surge as over 20% 2024 price swings and pipeline limits bite

Federal leasing, methane and tax policy shifts alter Bakken development costs and timing; regional output ~1.2m b/d (2024) vs US ~13.1m b/d. State/local rules (ND ~1.1m b/d, MT ~40kb/d) and road-use fees affect capex cadence for non-operators. Pipeline bottlenecks (DAPL 570kb/d) and OPEC+ cuts ~2.2m b/d drive >20% price swings in 2024, impacting realized pricing and AFEs.

| Factor | Key metric |

|---|---|

| Bakken output | ~1.2m b/d (2024) |

| DAPL capacity | 570k b/d |

| OPEC+ cuts | ~2.2m b/d |

| US crude | ~13.1m b/d (2024) |

What is included in the product

Explores how macro-environmental factors uniquely impact Vitesse Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific context. Designed for executives and investors to identify actionable threats, opportunities, and forward-looking scenarios for strategy and funding decisions.

A concise, visually segmented PESTLE summary for Vitesse Energy that streamlines meeting prep, is easily editable for regional or business-line notes, and can be dropped into presentations or shared across teams to align on external risks and strategic positioning.

Economic factors

WTI price volatility and basis

Bakken realizations track WTI, which averaged about $78/bbl in H1 2025, with regional Williston basis differentials historically ranging from -5 to -20/bbl. Wider Williston discounts compress margins and slow capital-efficient development. Improved takeaway since 2024 narrowed basis toward -5/bbl, materially boosting free cash flow. A disciplined hedging program smooths cash yields amid WTI and basis swings.

Service cost inflation/deflation

Pressure pumping, rigs and tubulars can drive up to 30% or more of total well costs, so service-cost inflation directly raises operator AFEs and erodes returns. A 10% rise in service pricing can materially cut projected IRRs on new wells, while deflation can quickly re-open idle inventory and boost activity. As a non-operator, Vitesse’s exposure is indirect but still material to capital efficiency and unit economics. Cycle-aware acquisition pricing is therefore critical to preserve returns across commodity and service cycles.

Capital markets and rates

Rising benchmark rates (Fed funds 5.25–5.50% and US 10-yr around 4.2% in mid-2025) raise borrowing costs and compress E&P equity valuations, reducing drilling budgets and non-op growth when credit tightens. Companies with strong cash generation and net debt/EBITDA under ~1.5x show greater resilience and M&A optionality. Narrow market windows driven by yields dictate timing for asset acquisitions and divestitures.

M&A and mineral/working interest market

M&A and non-operated working interest availability and pricing set Vitesse Energy’s external growth ceiling; U.S. upstream divestiture volumes topped roughly $20bn in 2024, intensifying competitive bidding and compressing returns.

Disciplined underwriting preserves FCF per share while portfolio high-grading—targeting higher-margin wells—reduces decline and lifts cash margins.

Counterparty quality drives execution risk and timely payouts, materially affecting realized proceeds.

- Market volume: ~ $20bn (2024)

- Competitive bids compress IRR

- High-grading cuts decline, boosts margins

- Counterparty credit = payout certainty

Production declines and terminal value

Shale wells commonly exhibit 60–70% first-year declines, front-loading returns and compressing long-term production.

Maintaining a PDP-heavy vs PUD mix stabilizes near-term cash while PUDs drive growth; portfolio balance affects cashflow volatility.

Refrac and infill can extend asset life and lift EURs by ~20–40%, so decline-rate assumptions directly drive NAV and dividend sustainability.

- decline-rate: 60–70% 1st year

- EUR uplift (refrac/infill): ~20–40%

- PDP/PUD mix: tradeoff cash stability vs growth

Bakken costs surge as over 20% 2024 price swings and pipeline limits bite

WTI averaged ~$78/bbl H1 2025 with Williston basis -5 to -20/bbl; improved takeaway since 2024 narrowed basis toward -5, boosting FCF. Service inflation (pressure pumping/rigs/tubulars ~30% of well cost) and Fed funds 5.25–5.50%/US10yr ~4.2% raise breakevens; 2024 US upstream divestitures ~ $20bn. First-year declines 60–70%; refrac/infill can lift EURs ~20–40%.

| Metric | Value |

|---|---|

| WTI H1 2025 | $78/bbl |

| Williston basis | -5 to -20 /bbl |

| Service cost share | ~30% |

| Fed funds / US10yr | 5.25–5.50% / ~4.2% |

| 2024 divestitures | ~$20bn |

What You See Is What You Get

Vitesse Energy PESTLE Analysis

The preview shown here is the exact Vitesse Energy PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, sociocultural, technological, legal and environmental assessment tailored to Vitesse Energy. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase. Downloadable immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and technological advances are shaping Vitesse Energy’s strategic landscape in our targeted PESTLE analysis. This concise, expert-grade report highlights risks and growth levers you can act on now. Purchase the full PESTLE to access detailed, ready-to-use insights and strengthen your investment or strategy decisions.

Political factors

Federal energy policy shifts

Changes in federal leasing, permitting and emissions policy can quickly shift development pace and costs for Bakken assets, where regional crude output stood around 1.2 million b/d in 2024 versus US production ~12.8 million b/d. As a non-operator, Vitesse is exposed to partners’ compliance timing and cost pass-throughs. Administration swings drive pipeline approvals, methane rules and tax incentives, and policy predictability is critical for acquisition underwriting and free-cash-flow visibility.

State-level regimes ND and MT

North Dakota (Bakken ~1.1 million b/d) and Montana (~40 kb/d) set drilling, spacing, flaring and reclamation rules that dictate well timing and economics; ND Industrial Commission rulings directly shape Bakken development intensity. Changes to severance tax rates or flaring limits materially shift operator netbacks and capex cadence, altering non-operated AFE timing. Regulatory stability supports predictable non-op AFE cycles and capital planning.

Infrastructure politics and pipelines

Pipeline permitting and controversies such as Dakota Access Pipeline (DAPL) affect takeaway capacity and differentials; DAPL capacity is about 570,000 barrels per day. Political backing for midstream expansions can reduce bottlenecks and price discounts, while permitting delays widen differentials. Delays have historically shifted volumes to crude-by-rail—peaking at about 1.2 million bpd in 2014—raising costs and risks. Vitesse’s realized pricing depends on operators securing reliable transport routes.

Local government and community stance

County-level road-use agreements, impact fees and siting approvals in 2025 materially shape Vitesse Energy’s execution logistics, determining haul routes, timing and cost exposure; positive local relations can accelerate permit timelines and cut non-technical delays to weeks rather than months. Opposition raises mitigation, monitoring and community benefit obligations, increasing operating costs. Non-operators depend on partners’ on-the-ground engagement to preserve access and social license.

- Road-use & siting: local approvals dictate logistics

- Permitting: good relations shorten timelines

- Opposition: higher mitigation/monitoring costs

- Non-operators: rely on partner community engagement

Geopolitical supply shocks

Geopolitical supply shocks—notably OPEC+ cuts of ~2.2 million b/d and lingering Russia-related disruptions—drive WTI/Brent swings and crack-spread volatility, with intra-year price moves exceeding 20% in 2024. Those swings alter operator activity cycles, shifting Vitesse volumes and AFEs; higher sanctions-driven tightness can expand cash margins while demand shocks compress drilling and distributions.

- OPEC+ cuts ~2.2m b/d

- US crude ~13.1m b/d (2024)

- Price volatility >20% (2024)

Bakken costs surge as over 20% 2024 price swings and pipeline limits bite

Federal leasing, methane and tax policy shifts alter Bakken development costs and timing; regional output ~1.2m b/d (2024) vs US ~13.1m b/d. State/local rules (ND ~1.1m b/d, MT ~40kb/d) and road-use fees affect capex cadence for non-operators. Pipeline bottlenecks (DAPL 570kb/d) and OPEC+ cuts ~2.2m b/d drive >20% price swings in 2024, impacting realized pricing and AFEs.

| Factor | Key metric |

|---|---|

| Bakken output | ~1.2m b/d (2024) |

| DAPL capacity | 570k b/d |

| OPEC+ cuts | ~2.2m b/d |

| US crude | ~13.1m b/d (2024) |

What is included in the product

Explores how macro-environmental factors uniquely impact Vitesse Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific context. Designed for executives and investors to identify actionable threats, opportunities, and forward-looking scenarios for strategy and funding decisions.

A concise, visually segmented PESTLE summary for Vitesse Energy that streamlines meeting prep, is easily editable for regional or business-line notes, and can be dropped into presentations or shared across teams to align on external risks and strategic positioning.

Economic factors

WTI price volatility and basis

Bakken realizations track WTI, which averaged about $78/bbl in H1 2025, with regional Williston basis differentials historically ranging from -5 to -20/bbl. Wider Williston discounts compress margins and slow capital-efficient development. Improved takeaway since 2024 narrowed basis toward -5/bbl, materially boosting free cash flow. A disciplined hedging program smooths cash yields amid WTI and basis swings.

Service cost inflation/deflation

Pressure pumping, rigs and tubulars can drive up to 30% or more of total well costs, so service-cost inflation directly raises operator AFEs and erodes returns. A 10% rise in service pricing can materially cut projected IRRs on new wells, while deflation can quickly re-open idle inventory and boost activity. As a non-operator, Vitesse’s exposure is indirect but still material to capital efficiency and unit economics. Cycle-aware acquisition pricing is therefore critical to preserve returns across commodity and service cycles.

Capital markets and rates

Rising benchmark rates (Fed funds 5.25–5.50% and US 10-yr around 4.2% in mid-2025) raise borrowing costs and compress E&P equity valuations, reducing drilling budgets and non-op growth when credit tightens. Companies with strong cash generation and net debt/EBITDA under ~1.5x show greater resilience and M&A optionality. Narrow market windows driven by yields dictate timing for asset acquisitions and divestitures.

M&A and mineral/working interest market

M&A and non-operated working interest availability and pricing set Vitesse Energy’s external growth ceiling; U.S. upstream divestiture volumes topped roughly $20bn in 2024, intensifying competitive bidding and compressing returns.

Disciplined underwriting preserves FCF per share while portfolio high-grading—targeting higher-margin wells—reduces decline and lifts cash margins.

Counterparty quality drives execution risk and timely payouts, materially affecting realized proceeds.

- Market volume: ~ $20bn (2024)

- Competitive bids compress IRR

- High-grading cuts decline, boosts margins

- Counterparty credit = payout certainty

Production declines and terminal value

Shale wells commonly exhibit 60–70% first-year declines, front-loading returns and compressing long-term production.

Maintaining a PDP-heavy vs PUD mix stabilizes near-term cash while PUDs drive growth; portfolio balance affects cashflow volatility.

Refrac and infill can extend asset life and lift EURs by ~20–40%, so decline-rate assumptions directly drive NAV and dividend sustainability.

- decline-rate: 60–70% 1st year

- EUR uplift (refrac/infill): ~20–40%

- PDP/PUD mix: tradeoff cash stability vs growth

Bakken costs surge as over 20% 2024 price swings and pipeline limits bite

WTI averaged ~$78/bbl H1 2025 with Williston basis -5 to -20/bbl; improved takeaway since 2024 narrowed basis toward -5, boosting FCF. Service inflation (pressure pumping/rigs/tubulars ~30% of well cost) and Fed funds 5.25–5.50%/US10yr ~4.2% raise breakevens; 2024 US upstream divestitures ~ $20bn. First-year declines 60–70%; refrac/infill can lift EURs ~20–40%.

| Metric | Value |

|---|---|

| WTI H1 2025 | $78/bbl |

| Williston basis | -5 to -20 /bbl |

| Service cost share | ~30% |

| Fed funds / US10yr | 5.25–5.50% / ~4.2% |

| 2024 divestitures | ~$20bn |

What You See Is What You Get

Vitesse Energy PESTLE Analysis

The preview shown here is the exact Vitesse Energy PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, sociocultural, technological, legal and environmental assessment tailored to Vitesse Energy. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase. Downloadable immediately after payment.