Viva Energy Group Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

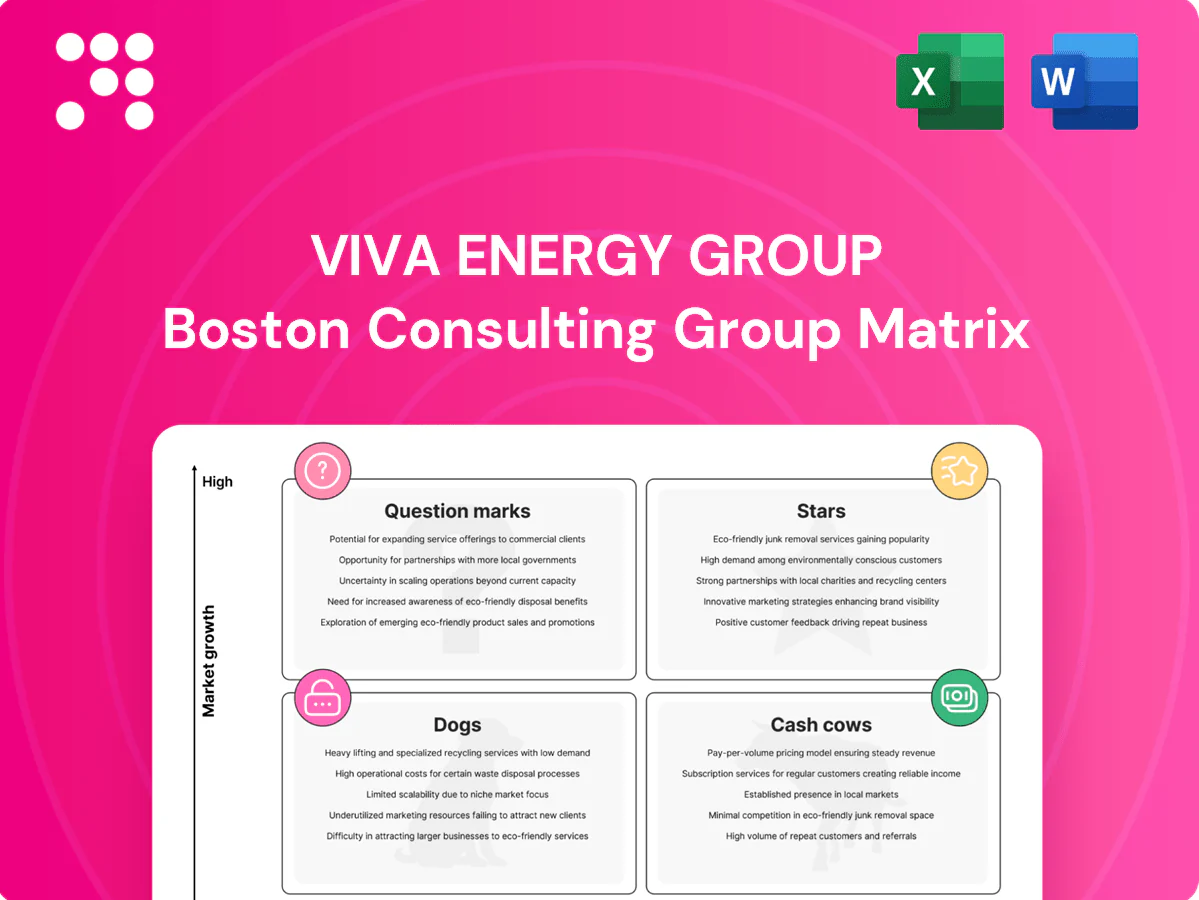

Want a quick, sharp read on Viva Energy Group’s product mix? This preview shows where things sit, but the full BCG Matrix lays out Stars, Cash Cows, Question Marks and Dogs with quadrant-by-quadrant data and clear strategic moves. Buy the complete report for a Word deep-dive plus an Excel summary you can present or act on—no guesswork, just recommendations you can use. Purchase now to get instant access and a roadmap for smarter allocation and faster decisions.

Stars

Integrated retail + convenience expansion

High growth in convenience margins, supported by Viva Energy's established forecourt footprint of over 1,200 sites, gives the group a clear lead to scale fast. Strong brand-driven traffic exists, but targeted investment in store upgrades, data analytics, and offer mix is required to convert footfall into higher basket spend. Maintain share and momentum now—this segment can evolve into a powerhouse cash engine. Spend to win while the convenience category reshapes.

Premium fuels and lubricants

Customers trade up as newer engines and fleet efficiency push premium fuels to roughly 15% of Australian retail volumes in 2024, growing at about a 4–6% annual rate; Viva’s Ampol/Viva brand and B2B contracts are converting this faster-growing slice into share. Promo and placement remain decisive; marketing and forecourt distribution investments drive incremental litres. Cash in equals cash out now — classic Star: high capex and working capital offsetting revenue. Hold pricing power, keep distribution tight, and it matures into a cash generator.

Aviation fuel recovery corridors

Air travel has rebounded strongly, with IATA reporting 2024 global passenger volumes above 2019 levels (around 103%), and air freight corridors growing faster than base fuels demand. Viva Energy’s airport access and integrated supply chain secure share in key corridors, but scaling capacity and converting wins into long-term contracts will require working capital. It reads like a leader in a rising tide—keep investing in reliability to lock growth into durable contracts.

Marine fuels at major ports

Shipping volumes and demand for IMO-compliant fuels rose in 2024, and scale at the wharf determines margin capture; Viva Energy’s integrated logistics and port presence let it seize high-value demand spikes when they occur. The business still requires capital to secure long-term supply contracts and storage capacity, keeping it investment-heavy. If Viva sustains offensive capacity build-out, marine fuels can transition into a steady milk cow.

- 2024 trend: compliance fuel demand up

- Scale advantage: port logistics capture spikes

- Capital need: supply and storage investment

- Strategic path: offense → predictable cash flows

National import, storage, and terminal network

Viva Energy’s national import, storage and terminal network is hard to replicate, underpinning growing demand for secure supply after 2024 tightness in Australian fuel markets; high utilisation and broad reach drive share leadership across key corridors. Ongoing capex is required to maintain safety and throughput, so invest now to bank dominance later.

- 2024 context: Australia fuel tightness reinforced value of terminals

- Network scale = durable barrier to entry

- High utilisation → share leadership

- Continuous capex required for safety and throughput

Scale, premium fuels and airports: capex now to unlock future cash engines

High-growth convenience (1,200+ forecourts) and premium fuels (~15% of Australian retail volumes in 2024, +4–6% pa) make Viva’s Stars investment-heavy but scalable; air pax at ~103% of 2019 (IATA 2024) boosts airport fuels; terminals/network tightness post‑2024 sustain share but require ongoing capex—spend to convert to future cash engines.

| Metric | 2024 | Note |

|---|---|---|

| Forecourts | 1,200+ | Convenience scale |

| Premium fuel share | 15% | Growth 4–6% pa |

| Air pax | ~103% of 2019 | IATA 2024 |

What is included in the product

Comprehensive BCG Matrix for Viva Energy Group mapping Stars, Cash Cows, Question Marks and Dogs with strategic investment recommendations.

One-page BCG matrix for Viva Energy Group, easing portfolio decisions and highlighting where to invest or divest.

Cash Cows

Geelong Refinery – core transport fuels

Geelong Refinery is Australia’s largest refinery with capacity around 7.5 billion litres per year (≈125 kbpd), serving a mature domestic transport fuels market with relatively stable volumes. Scale and integration deliver solid refining margins when operated reliably, underpinning Viva Energy’s downstream cash generation. Low growth, high market share makes it a classic cash cow; focus should be on optimizing reliability, sweating the asset and returning cash to shareholders.

Shell‑branded retail fuel sales

Everyday petrol and diesel sales through Viva Energy’s Shell‑branded network are steady, low‑growth cash cows delivering reliable margin through high throughput; the network spans over 1,800 Shell‑branded service stations across Australia as of 2024. Brand recognition and dense site coverage keep market share high with modest promotional spend; focus on maximising forecourt throughput to fund new growth initiatives. Milk this segment to finance the next strategic bets while maintaining operational efficiency.

B2B fuel supply to mining, transport, and industry

B2B fuel supply to mining, transport and industry is a cash cow for Viva Energy: long-term contracts and predictable volumes underpin pricing discipline and steady margins in 2024, with incumbency and service excellence defending relationships. Working capital is light once supply chains and credit terms are established, enabling cash harvest strategies. Focus on tightening service levels and extending contract tenors to sustain cash extraction.

Lubricants for fleet and industrial

Lubricants for fleet and industrial sit in a mature category with sticky B2B customers and decent margins; industry growth is slow (around 1–3% p.a.) while cash generation remains steady, funding broader Viva Energy needs.

Strong distribution networks and technical support create high switching costs that keep competitors at bay; maintain assortment, drive product mix toward higher-margin formulations and bank the surplus.

- Category: mature

- Customers: sticky

- Margins: decent

- Growth: ~1–3% p.a.

- Strategy: maintain assortment, drive mix, bank cash

Bitumen supply to road projects

Bitumen supply to road projects is a cash cow for Viva Energy: infrastructure demand is lumpy but overall mature, delivering predictable volumes and margins.

Established supply contracts and storage terminals give Viva a clear edge in tenders, keeping promotional spend low and emphasizing operations.

Focus on throughput efficiency, inventory turns and maintenance to sustain cash generation and clip the coupon on steady returns.

125 kbpd refinery & ~1,800 sites: steady, low‑growth cash flow

Viva Energy cash cows: Geelong refinery (≈125 kbpd / 7.5bn L p.a.) and Shell retail (≈1,800 sites in 2024) plus B2B fuels, lubricants and bitumen generate stable, low‑growth cash flow. Margins steady; prioritize reliability, throughput, contract extension and mix uplift to maximise cash return to shareholders.

| Segment | 2024 metric | Growth | Priority |

|---|---|---|---|

| Refining | 125 kbpd / 7.5bn L | 0–1% p.a. | Reliability |

| Retail | ~1,800 sites | 0–1% p.a. | Throughput |

| Lubricants | Sticky B2B | 1–3% p.a. | Mix |

What You See Is What You Get

Viva Energy Group BCG Matrix

The Viva Energy Group BCG Matrix you're previewing on this page is the exact file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored to Viva Energy’s portfolio. Once bought, the same document is yours to download, edit, print, or present immediately. Built for clarity and strategic use, it plugs straight into your planning or investor materials.

Visual. Strategic. Downloadable.

Want a quick, sharp read on Viva Energy Group’s product mix? This preview shows where things sit, but the full BCG Matrix lays out Stars, Cash Cows, Question Marks and Dogs with quadrant-by-quadrant data and clear strategic moves. Buy the complete report for a Word deep-dive plus an Excel summary you can present or act on—no guesswork, just recommendations you can use. Purchase now to get instant access and a roadmap for smarter allocation and faster decisions.

Stars

Integrated retail + convenience expansion

High growth in convenience margins, supported by Viva Energy's established forecourt footprint of over 1,200 sites, gives the group a clear lead to scale fast. Strong brand-driven traffic exists, but targeted investment in store upgrades, data analytics, and offer mix is required to convert footfall into higher basket spend. Maintain share and momentum now—this segment can evolve into a powerhouse cash engine. Spend to win while the convenience category reshapes.

Premium fuels and lubricants

Customers trade up as newer engines and fleet efficiency push premium fuels to roughly 15% of Australian retail volumes in 2024, growing at about a 4–6% annual rate; Viva’s Ampol/Viva brand and B2B contracts are converting this faster-growing slice into share. Promo and placement remain decisive; marketing and forecourt distribution investments drive incremental litres. Cash in equals cash out now — classic Star: high capex and working capital offsetting revenue. Hold pricing power, keep distribution tight, and it matures into a cash generator.

Aviation fuel recovery corridors

Air travel has rebounded strongly, with IATA reporting 2024 global passenger volumes above 2019 levels (around 103%), and air freight corridors growing faster than base fuels demand. Viva Energy’s airport access and integrated supply chain secure share in key corridors, but scaling capacity and converting wins into long-term contracts will require working capital. It reads like a leader in a rising tide—keep investing in reliability to lock growth into durable contracts.

Marine fuels at major ports

Shipping volumes and demand for IMO-compliant fuels rose in 2024, and scale at the wharf determines margin capture; Viva Energy’s integrated logistics and port presence let it seize high-value demand spikes when they occur. The business still requires capital to secure long-term supply contracts and storage capacity, keeping it investment-heavy. If Viva sustains offensive capacity build-out, marine fuels can transition into a steady milk cow.

- 2024 trend: compliance fuel demand up

- Scale advantage: port logistics capture spikes

- Capital need: supply and storage investment

- Strategic path: offense → predictable cash flows

National import, storage, and terminal network

Viva Energy’s national import, storage and terminal network is hard to replicate, underpinning growing demand for secure supply after 2024 tightness in Australian fuel markets; high utilisation and broad reach drive share leadership across key corridors. Ongoing capex is required to maintain safety and throughput, so invest now to bank dominance later.

- 2024 context: Australia fuel tightness reinforced value of terminals

- Network scale = durable barrier to entry

- High utilisation → share leadership

- Continuous capex required for safety and throughput

Scale, premium fuels and airports: capex now to unlock future cash engines

High-growth convenience (1,200+ forecourts) and premium fuels (~15% of Australian retail volumes in 2024, +4–6% pa) make Viva’s Stars investment-heavy but scalable; air pax at ~103% of 2019 (IATA 2024) boosts airport fuels; terminals/network tightness post‑2024 sustain share but require ongoing capex—spend to convert to future cash engines.

| Metric | 2024 | Note |

|---|---|---|

| Forecourts | 1,200+ | Convenience scale |

| Premium fuel share | 15% | Growth 4–6% pa |

| Air pax | ~103% of 2019 | IATA 2024 |

What is included in the product

Comprehensive BCG Matrix for Viva Energy Group mapping Stars, Cash Cows, Question Marks and Dogs with strategic investment recommendations.

One-page BCG matrix for Viva Energy Group, easing portfolio decisions and highlighting where to invest or divest.

Cash Cows

Geelong Refinery – core transport fuels

Geelong Refinery is Australia’s largest refinery with capacity around 7.5 billion litres per year (≈125 kbpd), serving a mature domestic transport fuels market with relatively stable volumes. Scale and integration deliver solid refining margins when operated reliably, underpinning Viva Energy’s downstream cash generation. Low growth, high market share makes it a classic cash cow; focus should be on optimizing reliability, sweating the asset and returning cash to shareholders.

Shell‑branded retail fuel sales

Everyday petrol and diesel sales through Viva Energy’s Shell‑branded network are steady, low‑growth cash cows delivering reliable margin through high throughput; the network spans over 1,800 Shell‑branded service stations across Australia as of 2024. Brand recognition and dense site coverage keep market share high with modest promotional spend; focus on maximising forecourt throughput to fund new growth initiatives. Milk this segment to finance the next strategic bets while maintaining operational efficiency.

B2B fuel supply to mining, transport, and industry

B2B fuel supply to mining, transport and industry is a cash cow for Viva Energy: long-term contracts and predictable volumes underpin pricing discipline and steady margins in 2024, with incumbency and service excellence defending relationships. Working capital is light once supply chains and credit terms are established, enabling cash harvest strategies. Focus on tightening service levels and extending contract tenors to sustain cash extraction.

Lubricants for fleet and industrial

Lubricants for fleet and industrial sit in a mature category with sticky B2B customers and decent margins; industry growth is slow (around 1–3% p.a.) while cash generation remains steady, funding broader Viva Energy needs.

Strong distribution networks and technical support create high switching costs that keep competitors at bay; maintain assortment, drive product mix toward higher-margin formulations and bank the surplus.

- Category: mature

- Customers: sticky

- Margins: decent

- Growth: ~1–3% p.a.

- Strategy: maintain assortment, drive mix, bank cash

Bitumen supply to road projects

Bitumen supply to road projects is a cash cow for Viva Energy: infrastructure demand is lumpy but overall mature, delivering predictable volumes and margins.

Established supply contracts and storage terminals give Viva a clear edge in tenders, keeping promotional spend low and emphasizing operations.

Focus on throughput efficiency, inventory turns and maintenance to sustain cash generation and clip the coupon on steady returns.

125 kbpd refinery & ~1,800 sites: steady, low‑growth cash flow

Viva Energy cash cows: Geelong refinery (≈125 kbpd / 7.5bn L p.a.) and Shell retail (≈1,800 sites in 2024) plus B2B fuels, lubricants and bitumen generate stable, low‑growth cash flow. Margins steady; prioritize reliability, throughput, contract extension and mix uplift to maximise cash return to shareholders.

| Segment | 2024 metric | Growth | Priority |

|---|---|---|---|

| Refining | 125 kbpd / 7.5bn L | 0–1% p.a. | Reliability |

| Retail | ~1,800 sites | 0–1% p.a. | Throughput |

| Lubricants | Sticky B2B | 1–3% p.a. | Mix |

What You See Is What You Get

Viva Energy Group BCG Matrix

The Viva Energy Group BCG Matrix you're previewing on this page is the exact file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored to Viva Energy’s portfolio. Once bought, the same document is yours to download, edit, print, or present immediately. Built for clarity and strategic use, it plugs straight into your planning or investor materials.

Description

Visual. Strategic. Downloadable.

Want a quick, sharp read on Viva Energy Group’s product mix? This preview shows where things sit, but the full BCG Matrix lays out Stars, Cash Cows, Question Marks and Dogs with quadrant-by-quadrant data and clear strategic moves. Buy the complete report for a Word deep-dive plus an Excel summary you can present or act on—no guesswork, just recommendations you can use. Purchase now to get instant access and a roadmap for smarter allocation and faster decisions.

Stars

Integrated retail + convenience expansion

High growth in convenience margins, supported by Viva Energy's established forecourt footprint of over 1,200 sites, gives the group a clear lead to scale fast. Strong brand-driven traffic exists, but targeted investment in store upgrades, data analytics, and offer mix is required to convert footfall into higher basket spend. Maintain share and momentum now—this segment can evolve into a powerhouse cash engine. Spend to win while the convenience category reshapes.

Premium fuels and lubricants

Customers trade up as newer engines and fleet efficiency push premium fuels to roughly 15% of Australian retail volumes in 2024, growing at about a 4–6% annual rate; Viva’s Ampol/Viva brand and B2B contracts are converting this faster-growing slice into share. Promo and placement remain decisive; marketing and forecourt distribution investments drive incremental litres. Cash in equals cash out now — classic Star: high capex and working capital offsetting revenue. Hold pricing power, keep distribution tight, and it matures into a cash generator.

Aviation fuel recovery corridors

Air travel has rebounded strongly, with IATA reporting 2024 global passenger volumes above 2019 levels (around 103%), and air freight corridors growing faster than base fuels demand. Viva Energy’s airport access and integrated supply chain secure share in key corridors, but scaling capacity and converting wins into long-term contracts will require working capital. It reads like a leader in a rising tide—keep investing in reliability to lock growth into durable contracts.

Marine fuels at major ports

Shipping volumes and demand for IMO-compliant fuels rose in 2024, and scale at the wharf determines margin capture; Viva Energy’s integrated logistics and port presence let it seize high-value demand spikes when they occur. The business still requires capital to secure long-term supply contracts and storage capacity, keeping it investment-heavy. If Viva sustains offensive capacity build-out, marine fuels can transition into a steady milk cow.

- 2024 trend: compliance fuel demand up

- Scale advantage: port logistics capture spikes

- Capital need: supply and storage investment

- Strategic path: offense → predictable cash flows

National import, storage, and terminal network

Viva Energy’s national import, storage and terminal network is hard to replicate, underpinning growing demand for secure supply after 2024 tightness in Australian fuel markets; high utilisation and broad reach drive share leadership across key corridors. Ongoing capex is required to maintain safety and throughput, so invest now to bank dominance later.

- 2024 context: Australia fuel tightness reinforced value of terminals

- Network scale = durable barrier to entry

- High utilisation → share leadership

- Continuous capex required for safety and throughput

Scale, premium fuels and airports: capex now to unlock future cash engines

High-growth convenience (1,200+ forecourts) and premium fuels (~15% of Australian retail volumes in 2024, +4–6% pa) make Viva’s Stars investment-heavy but scalable; air pax at ~103% of 2019 (IATA 2024) boosts airport fuels; terminals/network tightness post‑2024 sustain share but require ongoing capex—spend to convert to future cash engines.

| Metric | 2024 | Note |

|---|---|---|

| Forecourts | 1,200+ | Convenience scale |

| Premium fuel share | 15% | Growth 4–6% pa |

| Air pax | ~103% of 2019 | IATA 2024 |

What is included in the product

Comprehensive BCG Matrix for Viva Energy Group mapping Stars, Cash Cows, Question Marks and Dogs with strategic investment recommendations.

One-page BCG matrix for Viva Energy Group, easing portfolio decisions and highlighting where to invest or divest.

Cash Cows

Geelong Refinery – core transport fuels

Geelong Refinery is Australia’s largest refinery with capacity around 7.5 billion litres per year (≈125 kbpd), serving a mature domestic transport fuels market with relatively stable volumes. Scale and integration deliver solid refining margins when operated reliably, underpinning Viva Energy’s downstream cash generation. Low growth, high market share makes it a classic cash cow; focus should be on optimizing reliability, sweating the asset and returning cash to shareholders.

Shell‑branded retail fuel sales

Everyday petrol and diesel sales through Viva Energy’s Shell‑branded network are steady, low‑growth cash cows delivering reliable margin through high throughput; the network spans over 1,800 Shell‑branded service stations across Australia as of 2024. Brand recognition and dense site coverage keep market share high with modest promotional spend; focus on maximising forecourt throughput to fund new growth initiatives. Milk this segment to finance the next strategic bets while maintaining operational efficiency.

B2B fuel supply to mining, transport, and industry

B2B fuel supply to mining, transport and industry is a cash cow for Viva Energy: long-term contracts and predictable volumes underpin pricing discipline and steady margins in 2024, with incumbency and service excellence defending relationships. Working capital is light once supply chains and credit terms are established, enabling cash harvest strategies. Focus on tightening service levels and extending contract tenors to sustain cash extraction.

Lubricants for fleet and industrial

Lubricants for fleet and industrial sit in a mature category with sticky B2B customers and decent margins; industry growth is slow (around 1–3% p.a.) while cash generation remains steady, funding broader Viva Energy needs.

Strong distribution networks and technical support create high switching costs that keep competitors at bay; maintain assortment, drive product mix toward higher-margin formulations and bank the surplus.

- Category: mature

- Customers: sticky

- Margins: decent

- Growth: ~1–3% p.a.

- Strategy: maintain assortment, drive mix, bank cash

Bitumen supply to road projects

Bitumen supply to road projects is a cash cow for Viva Energy: infrastructure demand is lumpy but overall mature, delivering predictable volumes and margins.

Established supply contracts and storage terminals give Viva a clear edge in tenders, keeping promotional spend low and emphasizing operations.

Focus on throughput efficiency, inventory turns and maintenance to sustain cash generation and clip the coupon on steady returns.

125 kbpd refinery & ~1,800 sites: steady, low‑growth cash flow

Viva Energy cash cows: Geelong refinery (≈125 kbpd / 7.5bn L p.a.) and Shell retail (≈1,800 sites in 2024) plus B2B fuels, lubricants and bitumen generate stable, low‑growth cash flow. Margins steady; prioritize reliability, throughput, contract extension and mix uplift to maximise cash return to shareholders.

| Segment | 2024 metric | Growth | Priority |

|---|---|---|---|

| Refining | 125 kbpd / 7.5bn L | 0–1% p.a. | Reliability |

| Retail | ~1,800 sites | 0–1% p.a. | Throughput |

| Lubricants | Sticky B2B | 1–3% p.a. | Mix |

What You See Is What You Get

Viva Energy Group BCG Matrix

The Viva Energy Group BCG Matrix you're previewing on this page is the exact file you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored to Viva Energy’s portfolio. Once bought, the same document is yours to download, edit, print, or present immediately. Built for clarity and strategic use, it plugs straight into your planning or investor materials.