Viva Energy Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

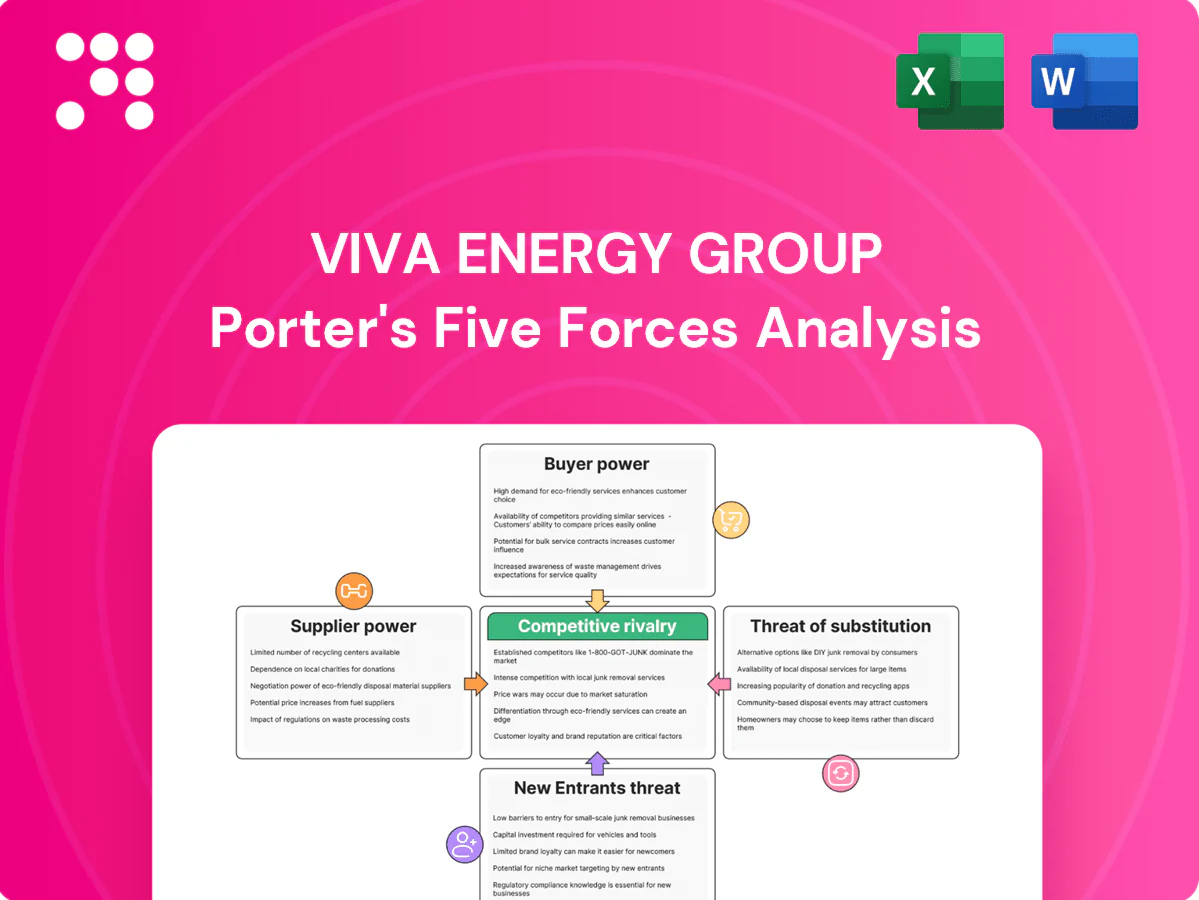

Viva Energy Group faces intense supplier bargaining, regulated retail margins, and moderate threat from new entrants and substitutes, shaping a challenging competitive landscape. This snapshot highlights key pressures and strategic levers driving margins and resilience. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentrated crude and product sources

Crude and refined product supply is concentrated among global producers and Asian refiners, giving upstream sellers leverage on price and terms; OPEC+ accounted for about 40% of global crude production in 2024.

OPEC+ policy and regional refinery outages can tighten supply, elevating spot premiums and margin pressure.

Viva mitigates via import optionality and diversified sourcing but exposure remains, with currency swings and freight cost pass-throughs adding volatility.

Specialty inputs and additives

Fuel additives, lubricants base oils and specialty chemicals are concentrated: the global fuel additives market was about USD 12.5 billion in 2024 and the lubricant market ~USD 38.7 billion, with top suppliers controlling roughly 60% of specialty supply, so switching needs requalification and spec compliance, raising switching costs. Long-term contracts stabilize availability but lock in margins; any supplier disruption can degrade product quality and risk regulatory non-compliance.

Logistics and shipping capacity

Tanker availability, pilots and port slots tightened in 2024 after Red Sea disruptions, giving logistics providers episodic pricing power and driving short-term freight and insurance spikes that flowed into procurement costs. Viva’s owned terminal network cushions domestic distribution, but long-haul bluewater shipping remains outsourced and exposed to market rates. Contracting and fuel hedges blunt volatility but do not remove exposure.

Equipment and maintenance OEMs

- Specialized parts = high supplier power

- Lead times/skills amplify leverage

- Compressed shutdowns strengthen vendors

- Framework contracts/inventory reduce risk

Regulatory and compliance “suppliers”

Regulatory and compliance "suppliers" such as fuel quality mandates (IMO 2020 0.5% sulphur, road diesel ≤10 ppm) and carbon schemes (Safeguard Mechanism covers facilities emitting ≥100,000 t CO2‑e) effectively supply permissions that can force capex or product reformulation, shifting power away from Viva Energy operators. Compliance costs are largely non‑negotiable; engagement and forecasting can soften but not eliminate impact.

- 0.5% IMO sulphur cap (2020)

- Diesel ≤10 ppm fuel quality

- Safeguard threshold ≥100,000 t CO2‑e

- Compliance costs non‑negotiable; engagement reduces but does not remove risk

OPEC+ holds 40% of crude; additives and lubricants heighten supply risk

Supplier power is high: OPEC+ supplied about 40% of global crude in 2024, constraining price and terms.

Specialty inputs concentrate risk: fuel additives market ~USD 12.5bn and lubricant market ~USD 38.7bn in 2024, with top suppliers ~60% share.

Logistics and OEM parts shortages tightened 2024 supply, raising short-term freight and turnaround costs.

| Factor | 2024 |

|---|---|

| OPEC+ crude share | ~40% |

| Fuel additives market | USD 12.5bn |

| Lubricant market | USD 38.7bn |

What is included in the product

Tailored Porter's Five Forces for Viva Energy Group uncover key competitive drivers—supplier and buyer power, threat of substitutes, new entrants, and industry rivalry—highlighting pricing pressure, supply chain concentration, regulatory barriers, and emerging energy transition threats that shape profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Viva Energy Group that clarifies competitive pressures at a glance—perfect for fast boardroom decisions. Customize force levels, export a spider chart, and drop the clean layout straight into pitch decks or strategic reports.

Customers Bargaining Power

Large B2B tenders

Large B2B tenders from mining, aviation, marine and industrial customers drive high-volume purchases, enabling buyers to extract discounts, service guarantees and bespoke logistics. Their scale and multi-supplier purchasing frameworks keep switching costs moderate and preserve supplier access. Long-term contracts reduce churn but intensify margin pressure on Viva Energy Group.

Retail motorists’ price sensitivity

Pump buyers are highly price sensitive as real-time price apps such as MotorMouth and PetrolSpy expose forecourt prices instantly, and 2024 price cycles commonly shift retail petrol by 5–15 cents per litre. Switching costs at the forecourt are effectively zero, so drivers can defect with a quick detour. Loyalty schemes and convenience retail reduce churn but do not eliminate price-driven switching. Intense price cycles thus amplify consumer bargaining power.

Other retailers and resellers

Independent service stations and resellers negotiate wholesale terms aggressively and can pivot suppliers if terminal access exists, boosting buyer power. Branding and supply-security arrangements with Viva Energy help retain sites, yet resellers routinely expect volume-based discounts. Contract expiries create renegotiation cliffs that can compress margins and trigger rapid price re-bids.

Demand cyclicality and fuel efficiency

- Higher buyer leverage due to lower volumes

- 2024 aviation demand ~95% of 2019 (IATA)

- Mixed product mix smooths but doesn’t eliminate price risk

Service and reliability expectations

On-time delivery, product quality and credit terms are primary negotiation levers; buyers demand high service levels and impose penalties for failures. Viva’s distribution network and Geelong Refinery supported reliability in 2024, but outages eroded its bargaining position. SLAs and published performance data are used to defend value and premium terms.

Drivers price-sensitive (5–15 c/L); B2B holds leverage; aviation demand ≈95%

Large B2B tenders and resellers secure volume discounts and bespoke logistics, keeping switching costs moderate; forecourt consumers are price-sensitive with near-zero switching costs amplified by price apps and 2024 price cycles of 5–15 c/L. Long-term contracts and loyalty schemes limit churn but intensify margin pressure; 2024 aviation demand ~95% of 2019 (IATA), lowering volumes and raising buyer leverage.

| Buyer | 2024 metric | Switching cost | Bargaining power |

|---|---|---|---|

| B2B/resellers | Volume contracts, discounts | Moderate | High |

| Retail drivers | Price cycles 5–15 c/L | Low | Very high |

What You See Is What You Get

Viva Energy Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Viva Energy Group examines competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and the risk of substitutes, with data-driven insights and strategic implications. It identifies key industry pressures, regulatory and commodity sensitivities, and profitability levers. Strategic recommendations and risk mitigations are included. This preview is the exact document you’ll receive instantly after purchase.

From Overview to Strategy Blueprint

Viva Energy Group faces intense supplier bargaining, regulated retail margins, and moderate threat from new entrants and substitutes, shaping a challenging competitive landscape. This snapshot highlights key pressures and strategic levers driving margins and resilience. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentrated crude and product sources

Crude and refined product supply is concentrated among global producers and Asian refiners, giving upstream sellers leverage on price and terms; OPEC+ accounted for about 40% of global crude production in 2024.

OPEC+ policy and regional refinery outages can tighten supply, elevating spot premiums and margin pressure.

Viva mitigates via import optionality and diversified sourcing but exposure remains, with currency swings and freight cost pass-throughs adding volatility.

Specialty inputs and additives

Fuel additives, lubricants base oils and specialty chemicals are concentrated: the global fuel additives market was about USD 12.5 billion in 2024 and the lubricant market ~USD 38.7 billion, with top suppliers controlling roughly 60% of specialty supply, so switching needs requalification and spec compliance, raising switching costs. Long-term contracts stabilize availability but lock in margins; any supplier disruption can degrade product quality and risk regulatory non-compliance.

Logistics and shipping capacity

Tanker availability, pilots and port slots tightened in 2024 after Red Sea disruptions, giving logistics providers episodic pricing power and driving short-term freight and insurance spikes that flowed into procurement costs. Viva’s owned terminal network cushions domestic distribution, but long-haul bluewater shipping remains outsourced and exposed to market rates. Contracting and fuel hedges blunt volatility but do not remove exposure.

Equipment and maintenance OEMs

- Specialized parts = high supplier power

- Lead times/skills amplify leverage

- Compressed shutdowns strengthen vendors

- Framework contracts/inventory reduce risk

Regulatory and compliance “suppliers”

Regulatory and compliance "suppliers" such as fuel quality mandates (IMO 2020 0.5% sulphur, road diesel ≤10 ppm) and carbon schemes (Safeguard Mechanism covers facilities emitting ≥100,000 t CO2‑e) effectively supply permissions that can force capex or product reformulation, shifting power away from Viva Energy operators. Compliance costs are largely non‑negotiable; engagement and forecasting can soften but not eliminate impact.

- 0.5% IMO sulphur cap (2020)

- Diesel ≤10 ppm fuel quality

- Safeguard threshold ≥100,000 t CO2‑e

- Compliance costs non‑negotiable; engagement reduces but does not remove risk

OPEC+ holds 40% of crude; additives and lubricants heighten supply risk

Supplier power is high: OPEC+ supplied about 40% of global crude in 2024, constraining price and terms.

Specialty inputs concentrate risk: fuel additives market ~USD 12.5bn and lubricant market ~USD 38.7bn in 2024, with top suppliers ~60% share.

Logistics and OEM parts shortages tightened 2024 supply, raising short-term freight and turnaround costs.

| Factor | 2024 |

|---|---|

| OPEC+ crude share | ~40% |

| Fuel additives market | USD 12.5bn |

| Lubricant market | USD 38.7bn |

What is included in the product

Tailored Porter's Five Forces for Viva Energy Group uncover key competitive drivers—supplier and buyer power, threat of substitutes, new entrants, and industry rivalry—highlighting pricing pressure, supply chain concentration, regulatory barriers, and emerging energy transition threats that shape profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Viva Energy Group that clarifies competitive pressures at a glance—perfect for fast boardroom decisions. Customize force levels, export a spider chart, and drop the clean layout straight into pitch decks or strategic reports.

Customers Bargaining Power

Large B2B tenders

Large B2B tenders from mining, aviation, marine and industrial customers drive high-volume purchases, enabling buyers to extract discounts, service guarantees and bespoke logistics. Their scale and multi-supplier purchasing frameworks keep switching costs moderate and preserve supplier access. Long-term contracts reduce churn but intensify margin pressure on Viva Energy Group.

Retail motorists’ price sensitivity

Pump buyers are highly price sensitive as real-time price apps such as MotorMouth and PetrolSpy expose forecourt prices instantly, and 2024 price cycles commonly shift retail petrol by 5–15 cents per litre. Switching costs at the forecourt are effectively zero, so drivers can defect with a quick detour. Loyalty schemes and convenience retail reduce churn but do not eliminate price-driven switching. Intense price cycles thus amplify consumer bargaining power.

Other retailers and resellers

Independent service stations and resellers negotiate wholesale terms aggressively and can pivot suppliers if terminal access exists, boosting buyer power. Branding and supply-security arrangements with Viva Energy help retain sites, yet resellers routinely expect volume-based discounts. Contract expiries create renegotiation cliffs that can compress margins and trigger rapid price re-bids.

Demand cyclicality and fuel efficiency

- Higher buyer leverage due to lower volumes

- 2024 aviation demand ~95% of 2019 (IATA)

- Mixed product mix smooths but doesn’t eliminate price risk

Service and reliability expectations

On-time delivery, product quality and credit terms are primary negotiation levers; buyers demand high service levels and impose penalties for failures. Viva’s distribution network and Geelong Refinery supported reliability in 2024, but outages eroded its bargaining position. SLAs and published performance data are used to defend value and premium terms.

Drivers price-sensitive (5–15 c/L); B2B holds leverage; aviation demand ≈95%

Large B2B tenders and resellers secure volume discounts and bespoke logistics, keeping switching costs moderate; forecourt consumers are price-sensitive with near-zero switching costs amplified by price apps and 2024 price cycles of 5–15 c/L. Long-term contracts and loyalty schemes limit churn but intensify margin pressure; 2024 aviation demand ~95% of 2019 (IATA), lowering volumes and raising buyer leverage.

| Buyer | 2024 metric | Switching cost | Bargaining power |

|---|---|---|---|

| B2B/resellers | Volume contracts, discounts | Moderate | High |

| Retail drivers | Price cycles 5–15 c/L | Low | Very high |

What You See Is What You Get

Viva Energy Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Viva Energy Group examines competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and the risk of substitutes, with data-driven insights and strategic implications. It identifies key industry pressures, regulatory and commodity sensitivities, and profitability levers. Strategic recommendations and risk mitigations are included. This preview is the exact document you’ll receive instantly after purchase.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Viva Energy Group faces intense supplier bargaining, regulated retail margins, and moderate threat from new entrants and substitutes, shaping a challenging competitive landscape. This snapshot highlights key pressures and strategic levers driving margins and resilience. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment and strategy decisions.

Suppliers Bargaining Power

Concentrated crude and product sources

Crude and refined product supply is concentrated among global producers and Asian refiners, giving upstream sellers leverage on price and terms; OPEC+ accounted for about 40% of global crude production in 2024.

OPEC+ policy and regional refinery outages can tighten supply, elevating spot premiums and margin pressure.

Viva mitigates via import optionality and diversified sourcing but exposure remains, with currency swings and freight cost pass-throughs adding volatility.

Specialty inputs and additives

Fuel additives, lubricants base oils and specialty chemicals are concentrated: the global fuel additives market was about USD 12.5 billion in 2024 and the lubricant market ~USD 38.7 billion, with top suppliers controlling roughly 60% of specialty supply, so switching needs requalification and spec compliance, raising switching costs. Long-term contracts stabilize availability but lock in margins; any supplier disruption can degrade product quality and risk regulatory non-compliance.

Logistics and shipping capacity

Tanker availability, pilots and port slots tightened in 2024 after Red Sea disruptions, giving logistics providers episodic pricing power and driving short-term freight and insurance spikes that flowed into procurement costs. Viva’s owned terminal network cushions domestic distribution, but long-haul bluewater shipping remains outsourced and exposed to market rates. Contracting and fuel hedges blunt volatility but do not remove exposure.

Equipment and maintenance OEMs

- Specialized parts = high supplier power

- Lead times/skills amplify leverage

- Compressed shutdowns strengthen vendors

- Framework contracts/inventory reduce risk

Regulatory and compliance “suppliers”

Regulatory and compliance "suppliers" such as fuel quality mandates (IMO 2020 0.5% sulphur, road diesel ≤10 ppm) and carbon schemes (Safeguard Mechanism covers facilities emitting ≥100,000 t CO2‑e) effectively supply permissions that can force capex or product reformulation, shifting power away from Viva Energy operators. Compliance costs are largely non‑negotiable; engagement and forecasting can soften but not eliminate impact.

- 0.5% IMO sulphur cap (2020)

- Diesel ≤10 ppm fuel quality

- Safeguard threshold ≥100,000 t CO2‑e

- Compliance costs non‑negotiable; engagement reduces but does not remove risk

OPEC+ holds 40% of crude; additives and lubricants heighten supply risk

Supplier power is high: OPEC+ supplied about 40% of global crude in 2024, constraining price and terms.

Specialty inputs concentrate risk: fuel additives market ~USD 12.5bn and lubricant market ~USD 38.7bn in 2024, with top suppliers ~60% share.

Logistics and OEM parts shortages tightened 2024 supply, raising short-term freight and turnaround costs.

| Factor | 2024 |

|---|---|

| OPEC+ crude share | ~40% |

| Fuel additives market | USD 12.5bn |

| Lubricant market | USD 38.7bn |

What is included in the product

Tailored Porter's Five Forces for Viva Energy Group uncover key competitive drivers—supplier and buyer power, threat of substitutes, new entrants, and industry rivalry—highlighting pricing pressure, supply chain concentration, regulatory barriers, and emerging energy transition threats that shape profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Viva Energy Group that clarifies competitive pressures at a glance—perfect for fast boardroom decisions. Customize force levels, export a spider chart, and drop the clean layout straight into pitch decks or strategic reports.

Customers Bargaining Power

Large B2B tenders

Large B2B tenders from mining, aviation, marine and industrial customers drive high-volume purchases, enabling buyers to extract discounts, service guarantees and bespoke logistics. Their scale and multi-supplier purchasing frameworks keep switching costs moderate and preserve supplier access. Long-term contracts reduce churn but intensify margin pressure on Viva Energy Group.

Retail motorists’ price sensitivity

Pump buyers are highly price sensitive as real-time price apps such as MotorMouth and PetrolSpy expose forecourt prices instantly, and 2024 price cycles commonly shift retail petrol by 5–15 cents per litre. Switching costs at the forecourt are effectively zero, so drivers can defect with a quick detour. Loyalty schemes and convenience retail reduce churn but do not eliminate price-driven switching. Intense price cycles thus amplify consumer bargaining power.

Other retailers and resellers

Independent service stations and resellers negotiate wholesale terms aggressively and can pivot suppliers if terminal access exists, boosting buyer power. Branding and supply-security arrangements with Viva Energy help retain sites, yet resellers routinely expect volume-based discounts. Contract expiries create renegotiation cliffs that can compress margins and trigger rapid price re-bids.

Demand cyclicality and fuel efficiency

- Higher buyer leverage due to lower volumes

- 2024 aviation demand ~95% of 2019 (IATA)

- Mixed product mix smooths but doesn’t eliminate price risk

Service and reliability expectations

On-time delivery, product quality and credit terms are primary negotiation levers; buyers demand high service levels and impose penalties for failures. Viva’s distribution network and Geelong Refinery supported reliability in 2024, but outages eroded its bargaining position. SLAs and published performance data are used to defend value and premium terms.

Drivers price-sensitive (5–15 c/L); B2B holds leverage; aviation demand ≈95%

Large B2B tenders and resellers secure volume discounts and bespoke logistics, keeping switching costs moderate; forecourt consumers are price-sensitive with near-zero switching costs amplified by price apps and 2024 price cycles of 5–15 c/L. Long-term contracts and loyalty schemes limit churn but intensify margin pressure; 2024 aviation demand ~95% of 2019 (IATA), lowering volumes and raising buyer leverage.

| Buyer | 2024 metric | Switching cost | Bargaining power |

|---|---|---|---|

| B2B/resellers | Volume contracts, discounts | Moderate | High |

| Retail drivers | Price cycles 5–15 c/L | Low | Very high |

What You See Is What You Get

Viva Energy Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Viva Energy Group examines competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and the risk of substitutes, with data-driven insights and strategic implications. It identifies key industry pressures, regulatory and commodity sensitivities, and profitability levers. Strategic recommendations and risk mitigations are included. This preview is the exact document you’ll receive instantly after purchase.