Vodafone Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Vodafone Group PESTLE Analysis—three concise sections reveal how politics, regulation, economy, tech and societal trends shape Vodafone’s prospects. Tailored for investors and strategists, it highlights risks and growth levers. Purchase the full report to access detailed, actionable insights and ready-to-use templates.

Political factors

Spectrum licensing and fees

Governments control spectrum allocation, renewal terms and pricing, directly shaping Vodafone’s capex and market-entry timing; Vodafone reported group capital expenditure of about €5.0bn in FY2024. Auctions and administrative renewals vary widely across Europe and Africa — European 5G auctions have raised billions (Germany 2019: €6.55bn, UK 2021: £1.36bn). Policy shifts toward shared or open-access spectrum can compress ARPUs and change competitive dynamics. Political favoritism or instability in some African markets can delay access or inflate costs, raising bid and rollout risk.

EU digital and telecom policy

EU directives on single market, wholesale access and cross-border services reshape pricing and M&A levers across 27 member states, in an EU telecom market of roughly €200bn annually; fragmentation still forces complex compliance. Roaming abolition (2017), caps on termination rates and net neutrality constrain monetization. Proposals for fair contributions by large traffic generators could improve returns. Digital Decade targets 5G by 2030 add investment pressure.

Geopolitical risk and supply chain

Sanctions, trade restrictions and vendor bans force changes to equipment choices and can delay rollouts, increasing procurement complexity and capex for operators like Vodafone.

Diversifying away from restricted vendors raises integration risk and higher unit costs during procurement and deployment, pressuring margins and timelines.

More than 95% of intercontinental data traffic travels via subsea cables, so geopolitical tensions and import/currency controls in some African markets can disrupt cable routing, security and network expansion.

Public investment and subsidies

State-backed broadband programs and 5G funds (eg UK Shared Rural Network ~£1bn) can co-finance rural coverage and lower Vodafone’s rollout cost while EU Digital Decade targets require 5G in all populated areas by 2025, but open-access and regulated pricing clauses can cap commercial upside. Political priorities like digital inclusion and defense-grade resilience shape eligibility, and election cycles often delay disbursements or refocus program scope.

- Co-finance: lowers capex burden

- Conditions: open access/pricing limit revenue upside

- Priorities: digital inclusion, resilience affect grant access

- Risk: election cycles can delay or reshape funds

Government data and security demands

Government demands for lawful interception, data localization and critical-infrastructure status force Vodafone to segment networks and deploy localized storage and routing, raising architecture complexity.

Overlapping national rules push compliance costs higher; GDPR fines can reach 4% of global turnover — on Vodafone Group revenue of ~€45bn (FY2024) that equals ~€1.8bn maximum exposure.

Non-compliance risks heavy fines, license revocation and mandated remediation, while regulators expect rapid cooperation during emergencies and cyber incidents.

Spectrum auctions, vendor bans and GDPR risk (€1.8bn) shape telco capex

Spectrum rules, auctions and vendor bans drive Vodafone’s capex and rollout timing (group capex ~€5.0bn FY2024); EU telecom rules, roaming/termination caps and net neutrality limit monetization. Sanctions, vendor restrictions and data localization raise procurement, integration and compliance costs; GDPR exposure ~4% of €45bn revenue (~€1.8bn). State funds (UK SRN ~£1bn) lower rollout cost but often restrict pricing/ access.

| Metric | Value |

|---|---|

| Group revenue FY2024 | €45bn |

| Group capex FY2024 | €5.0bn |

| GDPR max fine | ~€1.8bn (4%) |

| Notable auctions | Germany €6.55bn (2019); UK £1.36bn (2021) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Vodafone Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends tied to the UK, EU and key emerging markets.

Designed for executives, investors and strategists, it provides detailed sub-points, forward-looking insights and regulatory scenario guidance ready for business plans and pitch decks.

A concise, visually segmented Vodafone Group PESTLE summary that relieves meeting prep pain by providing shareable, editable insights on external risks and market positioning for quick team alignment.

Economic factors

Consumer spending cycles

Macro slowdowns pressure ARPU and device sales, with Vodafone Group reporting c.273 million mobile customers by 2024 and management noting weaker handset demand; inflation (EU CPI ~3.9% in 2024) raises operating costs. Prepaid-heavy African markets show higher price elasticity, while bundled fixed-mobile offers in Europe help stabilize churn. Promotional intensity spikes in weak demand, compressing margins.

Interest rates and leverage

Higher interest rates (Bank of England ~5.25% in 2024) raise financing costs for spectrum, fibre and 5G deployments, squeezing returns as Vodafone carried ~€17.0bn net debt at end-FY24; refinancing windows therefore materially affect free cash flow. Asset carve-outs or tower monetisations can de-lever but reduce future optionality. Rate declines would reopen M&A and network-sharing economics.

Currency volatility

Euro, sterling and multiple African currencies create both translation and transaction risk for Vodafone, with devaluations able to erode reported euro revenues and raise the euro cost of imported network equipment; hedging programs reduce but do not eliminate exposure, leaving residual FX impacts on margins. Pricing power to pass through cost increases differs by market, weakening where competition and regulation are strongest, and strengthening in less contestable markets.

Competitive intensity and consolidation

Vodafone reported about 271 million mobile customers at end-March 2024; price wars in saturated European markets cap topline growth and ARPU expansion. Consolidation can restore pricing power and improve returns but faces EU/UK regulatory scrutiny. MVNOs and cable+mobile bundles continue to squeeze margins, while allowed network sharing and fiber co-investment can materially cut unit costs.

- Market saturation: high mobile penetration in EU limits net adds

- Consolidation: potential margin recovery vs regulatory hurdles

- Competitive pressure: MVNOs and cable bundles compress ARPU

- Cost levers: network sharing and fiber co-invest reduce capex/unit

Enterprise digitalization demand

- IoT: c.100m Vodafone connections (2024)

- Private networks: rising enterprise adoption, long sales cycles

- Cloud & cybersecurity: key upsell drivers

- Public sector: multi-year contracts = revenue resilience

Spectrum auctions, vendor bans and GDPR risk (€1.8bn) shape telco capex

Macro slowdown and EU CPI ~3.9% (2024) pressure ARPU and handset sales; Vodafone had ~271m mobile customers end‑Mar 2024. BoE rate ~5.25% and ~€17.0bn net debt raise financing costs for 5G/fibre. FX volatility and saturated EU markets compress margins; IoT ~100m supports B2B.

| Metric | 2024 |

|---|---|

| Mobile customers | ~271m |

| Net debt | €17.0bn |

| EU CPI | 3.9% |

| BoE rate | 5.25% |

| IoT | ~100m |

Preview Before You Purchase

Vodafone Group PESTLE Analysis

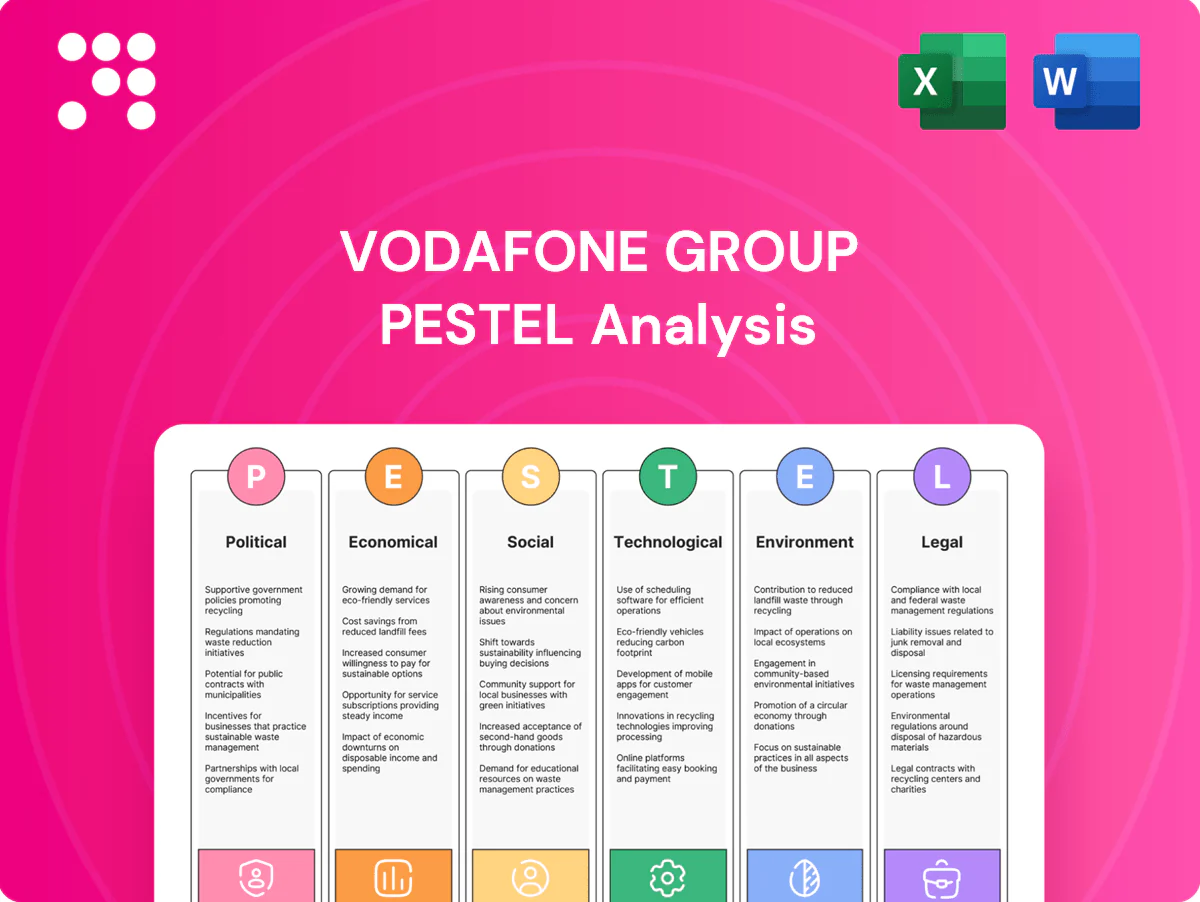

The Vodafone Group PESTLE analysis examines political, economic, social, technological, legal, and environmental factors shaping Vodafone’s strategy and risk profile. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Insights, data and recommendations are presented in the same structure you’ll download immediately after payment.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Vodafone Group PESTLE Analysis—three concise sections reveal how politics, regulation, economy, tech and societal trends shape Vodafone’s prospects. Tailored for investors and strategists, it highlights risks and growth levers. Purchase the full report to access detailed, actionable insights and ready-to-use templates.

Political factors

Spectrum licensing and fees

Governments control spectrum allocation, renewal terms and pricing, directly shaping Vodafone’s capex and market-entry timing; Vodafone reported group capital expenditure of about €5.0bn in FY2024. Auctions and administrative renewals vary widely across Europe and Africa — European 5G auctions have raised billions (Germany 2019: €6.55bn, UK 2021: £1.36bn). Policy shifts toward shared or open-access spectrum can compress ARPUs and change competitive dynamics. Political favoritism or instability in some African markets can delay access or inflate costs, raising bid and rollout risk.

EU digital and telecom policy

EU directives on single market, wholesale access and cross-border services reshape pricing and M&A levers across 27 member states, in an EU telecom market of roughly €200bn annually; fragmentation still forces complex compliance. Roaming abolition (2017), caps on termination rates and net neutrality constrain monetization. Proposals for fair contributions by large traffic generators could improve returns. Digital Decade targets 5G by 2030 add investment pressure.

Geopolitical risk and supply chain

Sanctions, trade restrictions and vendor bans force changes to equipment choices and can delay rollouts, increasing procurement complexity and capex for operators like Vodafone.

Diversifying away from restricted vendors raises integration risk and higher unit costs during procurement and deployment, pressuring margins and timelines.

More than 95% of intercontinental data traffic travels via subsea cables, so geopolitical tensions and import/currency controls in some African markets can disrupt cable routing, security and network expansion.

Public investment and subsidies

State-backed broadband programs and 5G funds (eg UK Shared Rural Network ~£1bn) can co-finance rural coverage and lower Vodafone’s rollout cost while EU Digital Decade targets require 5G in all populated areas by 2025, but open-access and regulated pricing clauses can cap commercial upside. Political priorities like digital inclusion and defense-grade resilience shape eligibility, and election cycles often delay disbursements or refocus program scope.

- Co-finance: lowers capex burden

- Conditions: open access/pricing limit revenue upside

- Priorities: digital inclusion, resilience affect grant access

- Risk: election cycles can delay or reshape funds

Government data and security demands

Government demands for lawful interception, data localization and critical-infrastructure status force Vodafone to segment networks and deploy localized storage and routing, raising architecture complexity.

Overlapping national rules push compliance costs higher; GDPR fines can reach 4% of global turnover — on Vodafone Group revenue of ~€45bn (FY2024) that equals ~€1.8bn maximum exposure.

Non-compliance risks heavy fines, license revocation and mandated remediation, while regulators expect rapid cooperation during emergencies and cyber incidents.

Spectrum auctions, vendor bans and GDPR risk (€1.8bn) shape telco capex

Spectrum rules, auctions and vendor bans drive Vodafone’s capex and rollout timing (group capex ~€5.0bn FY2024); EU telecom rules, roaming/termination caps and net neutrality limit monetization. Sanctions, vendor restrictions and data localization raise procurement, integration and compliance costs; GDPR exposure ~4% of €45bn revenue (~€1.8bn). State funds (UK SRN ~£1bn) lower rollout cost but often restrict pricing/ access.

| Metric | Value |

|---|---|

| Group revenue FY2024 | €45bn |

| Group capex FY2024 | €5.0bn |

| GDPR max fine | ~€1.8bn (4%) |

| Notable auctions | Germany €6.55bn (2019); UK £1.36bn (2021) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Vodafone Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends tied to the UK, EU and key emerging markets.

Designed for executives, investors and strategists, it provides detailed sub-points, forward-looking insights and regulatory scenario guidance ready for business plans and pitch decks.

A concise, visually segmented Vodafone Group PESTLE summary that relieves meeting prep pain by providing shareable, editable insights on external risks and market positioning for quick team alignment.

Economic factors

Consumer spending cycles

Macro slowdowns pressure ARPU and device sales, with Vodafone Group reporting c.273 million mobile customers by 2024 and management noting weaker handset demand; inflation (EU CPI ~3.9% in 2024) raises operating costs. Prepaid-heavy African markets show higher price elasticity, while bundled fixed-mobile offers in Europe help stabilize churn. Promotional intensity spikes in weak demand, compressing margins.

Interest rates and leverage

Higher interest rates (Bank of England ~5.25% in 2024) raise financing costs for spectrum, fibre and 5G deployments, squeezing returns as Vodafone carried ~€17.0bn net debt at end-FY24; refinancing windows therefore materially affect free cash flow. Asset carve-outs or tower monetisations can de-lever but reduce future optionality. Rate declines would reopen M&A and network-sharing economics.

Currency volatility

Euro, sterling and multiple African currencies create both translation and transaction risk for Vodafone, with devaluations able to erode reported euro revenues and raise the euro cost of imported network equipment; hedging programs reduce but do not eliminate exposure, leaving residual FX impacts on margins. Pricing power to pass through cost increases differs by market, weakening where competition and regulation are strongest, and strengthening in less contestable markets.

Competitive intensity and consolidation

Vodafone reported about 271 million mobile customers at end-March 2024; price wars in saturated European markets cap topline growth and ARPU expansion. Consolidation can restore pricing power and improve returns but faces EU/UK regulatory scrutiny. MVNOs and cable+mobile bundles continue to squeeze margins, while allowed network sharing and fiber co-investment can materially cut unit costs.

- Market saturation: high mobile penetration in EU limits net adds

- Consolidation: potential margin recovery vs regulatory hurdles

- Competitive pressure: MVNOs and cable bundles compress ARPU

- Cost levers: network sharing and fiber co-invest reduce capex/unit

Enterprise digitalization demand

- IoT: c.100m Vodafone connections (2024)

- Private networks: rising enterprise adoption, long sales cycles

- Cloud & cybersecurity: key upsell drivers

- Public sector: multi-year contracts = revenue resilience

Spectrum auctions, vendor bans and GDPR risk (€1.8bn) shape telco capex

Macro slowdown and EU CPI ~3.9% (2024) pressure ARPU and handset sales; Vodafone had ~271m mobile customers end‑Mar 2024. BoE rate ~5.25% and ~€17.0bn net debt raise financing costs for 5G/fibre. FX volatility and saturated EU markets compress margins; IoT ~100m supports B2B.

| Metric | 2024 |

|---|---|

| Mobile customers | ~271m |

| Net debt | €17.0bn |

| EU CPI | 3.9% |

| BoE rate | 5.25% |

| IoT | ~100m |

Preview Before You Purchase

Vodafone Group PESTLE Analysis

The Vodafone Group PESTLE analysis examines political, economic, social, technological, legal, and environmental factors shaping Vodafone’s strategy and risk profile. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Insights, data and recommendations are presented in the same structure you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Vodafone Group PESTLE Analysis—three concise sections reveal how politics, regulation, economy, tech and societal trends shape Vodafone’s prospects. Tailored for investors and strategists, it highlights risks and growth levers. Purchase the full report to access detailed, actionable insights and ready-to-use templates.

Political factors

Spectrum licensing and fees

Governments control spectrum allocation, renewal terms and pricing, directly shaping Vodafone’s capex and market-entry timing; Vodafone reported group capital expenditure of about €5.0bn in FY2024. Auctions and administrative renewals vary widely across Europe and Africa — European 5G auctions have raised billions (Germany 2019: €6.55bn, UK 2021: £1.36bn). Policy shifts toward shared or open-access spectrum can compress ARPUs and change competitive dynamics. Political favoritism or instability in some African markets can delay access or inflate costs, raising bid and rollout risk.

EU digital and telecom policy

EU directives on single market, wholesale access and cross-border services reshape pricing and M&A levers across 27 member states, in an EU telecom market of roughly €200bn annually; fragmentation still forces complex compliance. Roaming abolition (2017), caps on termination rates and net neutrality constrain monetization. Proposals for fair contributions by large traffic generators could improve returns. Digital Decade targets 5G by 2030 add investment pressure.

Geopolitical risk and supply chain

Sanctions, trade restrictions and vendor bans force changes to equipment choices and can delay rollouts, increasing procurement complexity and capex for operators like Vodafone.

Diversifying away from restricted vendors raises integration risk and higher unit costs during procurement and deployment, pressuring margins and timelines.

More than 95% of intercontinental data traffic travels via subsea cables, so geopolitical tensions and import/currency controls in some African markets can disrupt cable routing, security and network expansion.

Public investment and subsidies

State-backed broadband programs and 5G funds (eg UK Shared Rural Network ~£1bn) can co-finance rural coverage and lower Vodafone’s rollout cost while EU Digital Decade targets require 5G in all populated areas by 2025, but open-access and regulated pricing clauses can cap commercial upside. Political priorities like digital inclusion and defense-grade resilience shape eligibility, and election cycles often delay disbursements or refocus program scope.

- Co-finance: lowers capex burden

- Conditions: open access/pricing limit revenue upside

- Priorities: digital inclusion, resilience affect grant access

- Risk: election cycles can delay or reshape funds

Government data and security demands

Government demands for lawful interception, data localization and critical-infrastructure status force Vodafone to segment networks and deploy localized storage and routing, raising architecture complexity.

Overlapping national rules push compliance costs higher; GDPR fines can reach 4% of global turnover — on Vodafone Group revenue of ~€45bn (FY2024) that equals ~€1.8bn maximum exposure.

Non-compliance risks heavy fines, license revocation and mandated remediation, while regulators expect rapid cooperation during emergencies and cyber incidents.

Spectrum auctions, vendor bans and GDPR risk (€1.8bn) shape telco capex

Spectrum rules, auctions and vendor bans drive Vodafone’s capex and rollout timing (group capex ~€5.0bn FY2024); EU telecom rules, roaming/termination caps and net neutrality limit monetization. Sanctions, vendor restrictions and data localization raise procurement, integration and compliance costs; GDPR exposure ~4% of €45bn revenue (~€1.8bn). State funds (UK SRN ~£1bn) lower rollout cost but often restrict pricing/ access.

| Metric | Value |

|---|---|

| Group revenue FY2024 | €45bn |

| Group capex FY2024 | €5.0bn |

| GDPR max fine | ~€1.8bn (4%) |

| Notable auctions | Germany €6.55bn (2019); UK £1.36bn (2021) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Vodafone Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends tied to the UK, EU and key emerging markets.

Designed for executives, investors and strategists, it provides detailed sub-points, forward-looking insights and regulatory scenario guidance ready for business plans and pitch decks.

A concise, visually segmented Vodafone Group PESTLE summary that relieves meeting prep pain by providing shareable, editable insights on external risks and market positioning for quick team alignment.

Economic factors

Consumer spending cycles

Macro slowdowns pressure ARPU and device sales, with Vodafone Group reporting c.273 million mobile customers by 2024 and management noting weaker handset demand; inflation (EU CPI ~3.9% in 2024) raises operating costs. Prepaid-heavy African markets show higher price elasticity, while bundled fixed-mobile offers in Europe help stabilize churn. Promotional intensity spikes in weak demand, compressing margins.

Interest rates and leverage

Higher interest rates (Bank of England ~5.25% in 2024) raise financing costs for spectrum, fibre and 5G deployments, squeezing returns as Vodafone carried ~€17.0bn net debt at end-FY24; refinancing windows therefore materially affect free cash flow. Asset carve-outs or tower monetisations can de-lever but reduce future optionality. Rate declines would reopen M&A and network-sharing economics.

Currency volatility

Euro, sterling and multiple African currencies create both translation and transaction risk for Vodafone, with devaluations able to erode reported euro revenues and raise the euro cost of imported network equipment; hedging programs reduce but do not eliminate exposure, leaving residual FX impacts on margins. Pricing power to pass through cost increases differs by market, weakening where competition and regulation are strongest, and strengthening in less contestable markets.

Competitive intensity and consolidation

Vodafone reported about 271 million mobile customers at end-March 2024; price wars in saturated European markets cap topline growth and ARPU expansion. Consolidation can restore pricing power and improve returns but faces EU/UK regulatory scrutiny. MVNOs and cable+mobile bundles continue to squeeze margins, while allowed network sharing and fiber co-investment can materially cut unit costs.

- Market saturation: high mobile penetration in EU limits net adds

- Consolidation: potential margin recovery vs regulatory hurdles

- Competitive pressure: MVNOs and cable bundles compress ARPU

- Cost levers: network sharing and fiber co-invest reduce capex/unit

Enterprise digitalization demand

- IoT: c.100m Vodafone connections (2024)

- Private networks: rising enterprise adoption, long sales cycles

- Cloud & cybersecurity: key upsell drivers

- Public sector: multi-year contracts = revenue resilience

Spectrum auctions, vendor bans and GDPR risk (€1.8bn) shape telco capex

Macro slowdown and EU CPI ~3.9% (2024) pressure ARPU and handset sales; Vodafone had ~271m mobile customers end‑Mar 2024. BoE rate ~5.25% and ~€17.0bn net debt raise financing costs for 5G/fibre. FX volatility and saturated EU markets compress margins; IoT ~100m supports B2B.

| Metric | 2024 |

|---|---|

| Mobile customers | ~271m |

| Net debt | €17.0bn |

| EU CPI | 3.9% |

| BoE rate | 5.25% |

| IoT | ~100m |

Preview Before You Purchase

Vodafone Group PESTLE Analysis

The Vodafone Group PESTLE analysis examines political, economic, social, technological, legal, and environmental factors shaping Vodafone’s strategy and risk profile. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Insights, data and recommendations are presented in the same structure you’ll download immediately after payment.