Vonovia Porter's Five Forces Analysis

Don't Miss the Bigger Picture

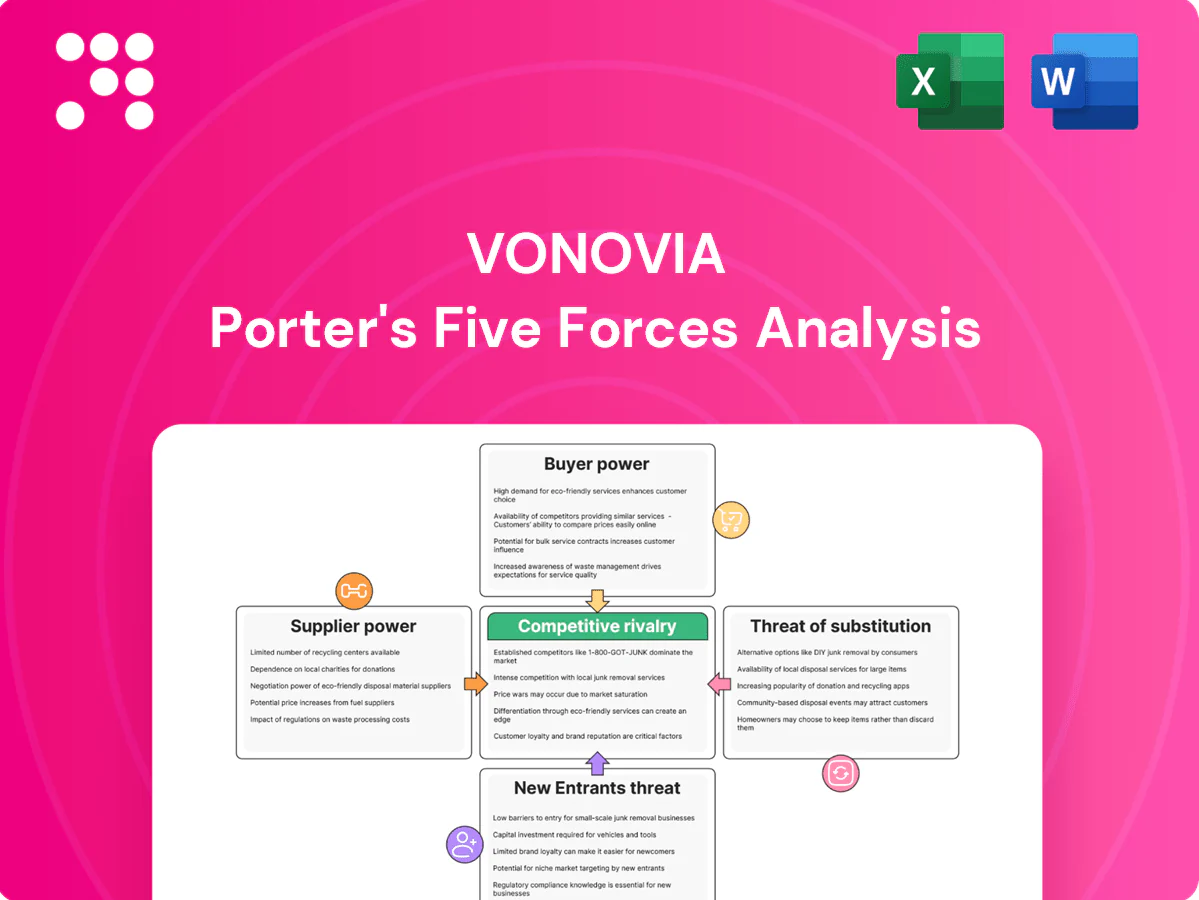

Vonovia faces intense rivalry and concentrated buyer power amid regulatory and financing pressures, while barriers to entry and substitute threats moderate competitive intensity—this snapshot highlights key strategic tensions and risk drivers. The complete report reveals the real forces shaping Vonovia’s industry and delivers force-by-force ratings, visuals, and actionable insights for investors and strategists.

Suppliers Bargaining Power

Concentrated contractors and trades

Renovation, modernization and maintenance depend heavily on regional contractors who are often capacity-constrained; in tight 2024 labor markets electricians, plumbers and façade specialists commanded higher prices and longer lead times, lifting supplier leverage.

Vonovia mitigates this with framework agreements and sizable in-house craft units supporting around 570,000 apartments and roughly 12,000 employees, but peak demand still raises costs and delays.

Supply bottlenecks in 2024 risked postponing capex plans and slowing rental uplift timelines, compressing projected returns.

Building materials volatility

In 2024 prices for energy‑intensive materials such as cement, steel and insulation remained volatile, driven by global commodity and energy markets and feeding directly into Vonovia’s refurbishment and new‑build budgets. Inflationary spikes have repeatedly compressed expected returns. Scale purchasing and hedging by Vonovia blunt but do not remove this variability. Stricter 2024 energy‑efficiency rules raise specs and boost supplier influence.

Utilities and energy providers

Heat, power and district energy for Vonovia are often tied to local monopolies or oligopolies, creating high supplier stickiness and straightforward cost pass-through; heat accounts for roughly 70% of building energy demand. Short-term tariff shifts and a 2024 EU ETS price near €90/tCO2 have raised supplier leverage and operating costs. Investments in heat pumps and PV can steadily cut dependence and exposure over time.

Technology and facility services

Technology and facility services for Vonovia rely on specialized vendors for smart metering, building automation and FM platforms, creating switching barriers from integration costs and data lock-in; Vonovia held about 565,000 residential units in 2024, making vendor leverage material. Long-term SLAs stabilize operations but strengthen supplier bargaining power; in-house teams and open standards can rebalance it.

Capital providers and refinancing

Banks, bondholders and public markets are key capital suppliers for Vonovia; ECB policy tightening (deposit rate ~4% in mid-2024) and wider credit spreads have raised refinancing costs, squeezing acquisition and development returns, while covenant terms can limit flexibility in downturns; Vonovia’s investment-grade positioning and strong asset backing mitigate but do not eliminate lenders’ leverage.

- ECB rate ~4% (mid-2024)

- Higher credit spreads ↑ refinancing cost

- Covenants constrain strategy in stress

- IG status + asset backing = partial buffer

Regional contractor constraints boost supplier leverage, raising renovation costs

Regional contractors and specialists were capacity‑constrained in 2024, boosting supplier leverage and raising renovation lead times and costs. Vonovia’s scale—~570,000 units and ~12,000 employees—plus in‑house craft teams and framework deals mitigate but do not remove pressure. Commodity and energy volatility (EU ETS ~€90/tCO2) and ECB rates (~4%) kept supplier influence high.

| Metric | 2024 |

|---|---|

| Residential units | ~570,000 |

| Employees | ~12,000 |

| EU ETS price | ~€90/tCO2 |

| ECB deposit rate | ~4% |

What is included in the product

Tailored Porter’s Five Forces analysis for Vonovia that uncovers key competitive drivers, evaluates supplier and tenant (buyer) power, and identifies threats from substitutes and new entrants affecting pricing and profitability. Includes strategic insights on disruptive trends and barriers protecting incumbents to support investor materials and internal strategy.

A concise one-sheet Vonovia Porter’s Five Forces that instantly visualizes strategic pressure with a spider chart, lets you customize force levels for regulatory or market shifts, and slots into decks or Excel dashboards—no macros, easy for non‑finance teams.

Customers Bargaining Power

Fragmented tenants, regulated rents

Individual tenants are numerous and exert low direct bargaining power against Vonovia, which manages roughly 565,000 residential units, about 80% in Germany. German rent regulation — the Mietpreisbremse capping new rents at about 10% above local comparables and common limits on increases (typically ~15% over three years) — materially restricts pricing freedom. This regulatory framework creates indirect buyer power via policy rather than negotiation and tenant-protection laws raise landlords’ switching and eviction costs.

Vacancy sensitivity in micro-markets

Aggregate demand for rental housing in Germany remains strong with roughly 50% of households renting and Vonovia holding about 570,000 units in 2024, but local oversupply or lower asset quality boosts tenant leverage in specific micro-markets. In weaker submarkets, incentives or targeted capex are often required to achieve lettings and maintain yields. Product differentiation through modernization and services reduces price sensitivity, while location and connectivity remain decisive for occupancy and rent growth.

Tenant associations and political influence

Organized tenant bodies, including the Deutscher Mieterbund (~1.5 million members), shape public debate and regulation that targets large landlords like Vonovia, which holds roughly 565,000 residential units, increasing collective leverage beyond individual renters. Political scrutiny on affordability—evident in tightened Mietpreisbremse rules—constrains rent growth and fee structures. Media visibility amplifies tenant concerns into rapid policy responses and reputational risk, heightening buyer power over pricing and service terms.

Service expectations and ESG

Tenants increasingly demand energy efficiency, comfort and digital services; for Vonovia — owner/manager of about 415,000 residential units in 2024 — poor service or disruptive retrofits can trigger churn and reputational costs. Delivering measurable ESG benefits raises willingness to pay and lowers buyer power; misalignment invites complaints and regulatory scrutiny.

- Tenants: prioritize efficiency, comfort, digital access

- Risk: retrofit disruption → churn

- ESG: measurable gains → higher willingness to pay

- Misalignment → complaints/regulatory attention

Alternative housing choices

Cooperatives, municipal housing and suburban alternatives expand tenant options and, together with remote/hybrid work enabling moves for affordability, weaken Vonovias pricing power where credible substitutes exist. Germanys rentership remains around 56% (2024), but vacancy in major supply-constrained cities often stays below 2%, preserving landlord leverage.

- Cooperatives: alternative tenure

- Municipal housing: capped rents

- Suburbs: affordability via relocation

- Vacancy <2% in tight cities: lower buyer power

Major landlord: low tenant bargaining power, strong regulatory and collective pressure

Individual tenants exert low direct bargaining power vs Vonovia (≈570,000 units, 2024) but strong indirect power via regulation: Mietpreisbremse caps new rents ≈10% above local comparables and typical limits ≈15% over 3 years; organized tenant groups (Deutscher Mieterbund ≈1.5M) and ESG demands raise collective leverage. Vacancy <2% in tight cities sustains local landlord power.

| Metric | Value (2024) |

|---|---|

| Vonovia units | ≈570,000 |

| Rentership Germany | 56% |

| Vacancy (tight cities) | <2% |

| Mietpreisbremse cap | ≈+10% |

| Increase limit | ≈15% / 3 yrs |

| Deutscher Mieterbund | ≈1.5M members |

Preview Before You Purchase

Vonovia Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is the complete Vonovia Porter's Five Forces analysis, professionally formatted and ready to use. You’ll get instant access to this identical file upon buying.

Don't Miss the Bigger Picture

Vonovia faces intense rivalry and concentrated buyer power amid regulatory and financing pressures, while barriers to entry and substitute threats moderate competitive intensity—this snapshot highlights key strategic tensions and risk drivers. The complete report reveals the real forces shaping Vonovia’s industry and delivers force-by-force ratings, visuals, and actionable insights for investors and strategists.

Suppliers Bargaining Power

Concentrated contractors and trades

Renovation, modernization and maintenance depend heavily on regional contractors who are often capacity-constrained; in tight 2024 labor markets electricians, plumbers and façade specialists commanded higher prices and longer lead times, lifting supplier leverage.

Vonovia mitigates this with framework agreements and sizable in-house craft units supporting around 570,000 apartments and roughly 12,000 employees, but peak demand still raises costs and delays.

Supply bottlenecks in 2024 risked postponing capex plans and slowing rental uplift timelines, compressing projected returns.

Building materials volatility

In 2024 prices for energy‑intensive materials such as cement, steel and insulation remained volatile, driven by global commodity and energy markets and feeding directly into Vonovia’s refurbishment and new‑build budgets. Inflationary spikes have repeatedly compressed expected returns. Scale purchasing and hedging by Vonovia blunt but do not remove this variability. Stricter 2024 energy‑efficiency rules raise specs and boost supplier influence.

Utilities and energy providers

Heat, power and district energy for Vonovia are often tied to local monopolies or oligopolies, creating high supplier stickiness and straightforward cost pass-through; heat accounts for roughly 70% of building energy demand. Short-term tariff shifts and a 2024 EU ETS price near €90/tCO2 have raised supplier leverage and operating costs. Investments in heat pumps and PV can steadily cut dependence and exposure over time.

Technology and facility services

Technology and facility services for Vonovia rely on specialized vendors for smart metering, building automation and FM platforms, creating switching barriers from integration costs and data lock-in; Vonovia held about 565,000 residential units in 2024, making vendor leverage material. Long-term SLAs stabilize operations but strengthen supplier bargaining power; in-house teams and open standards can rebalance it.

Capital providers and refinancing

Banks, bondholders and public markets are key capital suppliers for Vonovia; ECB policy tightening (deposit rate ~4% in mid-2024) and wider credit spreads have raised refinancing costs, squeezing acquisition and development returns, while covenant terms can limit flexibility in downturns; Vonovia’s investment-grade positioning and strong asset backing mitigate but do not eliminate lenders’ leverage.

- ECB rate ~4% (mid-2024)

- Higher credit spreads ↑ refinancing cost

- Covenants constrain strategy in stress

- IG status + asset backing = partial buffer

Regional contractor constraints boost supplier leverage, raising renovation costs

Regional contractors and specialists were capacity‑constrained in 2024, boosting supplier leverage and raising renovation lead times and costs. Vonovia’s scale—~570,000 units and ~12,000 employees—plus in‑house craft teams and framework deals mitigate but do not remove pressure. Commodity and energy volatility (EU ETS ~€90/tCO2) and ECB rates (~4%) kept supplier influence high.

| Metric | 2024 |

|---|---|

| Residential units | ~570,000 |

| Employees | ~12,000 |

| EU ETS price | ~€90/tCO2 |

| ECB deposit rate | ~4% |

What is included in the product

Tailored Porter’s Five Forces analysis for Vonovia that uncovers key competitive drivers, evaluates supplier and tenant (buyer) power, and identifies threats from substitutes and new entrants affecting pricing and profitability. Includes strategic insights on disruptive trends and barriers protecting incumbents to support investor materials and internal strategy.

A concise one-sheet Vonovia Porter’s Five Forces that instantly visualizes strategic pressure with a spider chart, lets you customize force levels for regulatory or market shifts, and slots into decks or Excel dashboards—no macros, easy for non‑finance teams.

Customers Bargaining Power

Fragmented tenants, regulated rents

Individual tenants are numerous and exert low direct bargaining power against Vonovia, which manages roughly 565,000 residential units, about 80% in Germany. German rent regulation — the Mietpreisbremse capping new rents at about 10% above local comparables and common limits on increases (typically ~15% over three years) — materially restricts pricing freedom. This regulatory framework creates indirect buyer power via policy rather than negotiation and tenant-protection laws raise landlords’ switching and eviction costs.

Vacancy sensitivity in micro-markets

Aggregate demand for rental housing in Germany remains strong with roughly 50% of households renting and Vonovia holding about 570,000 units in 2024, but local oversupply or lower asset quality boosts tenant leverage in specific micro-markets. In weaker submarkets, incentives or targeted capex are often required to achieve lettings and maintain yields. Product differentiation through modernization and services reduces price sensitivity, while location and connectivity remain decisive for occupancy and rent growth.

Tenant associations and political influence

Organized tenant bodies, including the Deutscher Mieterbund (~1.5 million members), shape public debate and regulation that targets large landlords like Vonovia, which holds roughly 565,000 residential units, increasing collective leverage beyond individual renters. Political scrutiny on affordability—evident in tightened Mietpreisbremse rules—constrains rent growth and fee structures. Media visibility amplifies tenant concerns into rapid policy responses and reputational risk, heightening buyer power over pricing and service terms.

Service expectations and ESG

Tenants increasingly demand energy efficiency, comfort and digital services; for Vonovia — owner/manager of about 415,000 residential units in 2024 — poor service or disruptive retrofits can trigger churn and reputational costs. Delivering measurable ESG benefits raises willingness to pay and lowers buyer power; misalignment invites complaints and regulatory scrutiny.

- Tenants: prioritize efficiency, comfort, digital access

- Risk: retrofit disruption → churn

- ESG: measurable gains → higher willingness to pay

- Misalignment → complaints/regulatory attention

Alternative housing choices

Cooperatives, municipal housing and suburban alternatives expand tenant options and, together with remote/hybrid work enabling moves for affordability, weaken Vonovias pricing power where credible substitutes exist. Germanys rentership remains around 56% (2024), but vacancy in major supply-constrained cities often stays below 2%, preserving landlord leverage.

- Cooperatives: alternative tenure

- Municipal housing: capped rents

- Suburbs: affordability via relocation

- Vacancy <2% in tight cities: lower buyer power

Major landlord: low tenant bargaining power, strong regulatory and collective pressure

Individual tenants exert low direct bargaining power vs Vonovia (≈570,000 units, 2024) but strong indirect power via regulation: Mietpreisbremse caps new rents ≈10% above local comparables and typical limits ≈15% over 3 years; organized tenant groups (Deutscher Mieterbund ≈1.5M) and ESG demands raise collective leverage. Vacancy <2% in tight cities sustains local landlord power.

| Metric | Value (2024) |

|---|---|

| Vonovia units | ≈570,000 |

| Rentership Germany | 56% |

| Vacancy (tight cities) | <2% |

| Mietpreisbremse cap | ≈+10% |

| Increase limit | ≈15% / 3 yrs |

| Deutscher Mieterbund | ≈1.5M members |

Preview Before You Purchase

Vonovia Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is the complete Vonovia Porter's Five Forces analysis, professionally formatted and ready to use. You’ll get instant access to this identical file upon buying.

Description

Don't Miss the Bigger Picture

Vonovia faces intense rivalry and concentrated buyer power amid regulatory and financing pressures, while barriers to entry and substitute threats moderate competitive intensity—this snapshot highlights key strategic tensions and risk drivers. The complete report reveals the real forces shaping Vonovia’s industry and delivers force-by-force ratings, visuals, and actionable insights for investors and strategists.

Suppliers Bargaining Power

Concentrated contractors and trades

Renovation, modernization and maintenance depend heavily on regional contractors who are often capacity-constrained; in tight 2024 labor markets electricians, plumbers and façade specialists commanded higher prices and longer lead times, lifting supplier leverage.

Vonovia mitigates this with framework agreements and sizable in-house craft units supporting around 570,000 apartments and roughly 12,000 employees, but peak demand still raises costs and delays.

Supply bottlenecks in 2024 risked postponing capex plans and slowing rental uplift timelines, compressing projected returns.

Building materials volatility

In 2024 prices for energy‑intensive materials such as cement, steel and insulation remained volatile, driven by global commodity and energy markets and feeding directly into Vonovia’s refurbishment and new‑build budgets. Inflationary spikes have repeatedly compressed expected returns. Scale purchasing and hedging by Vonovia blunt but do not remove this variability. Stricter 2024 energy‑efficiency rules raise specs and boost supplier influence.

Utilities and energy providers

Heat, power and district energy for Vonovia are often tied to local monopolies or oligopolies, creating high supplier stickiness and straightforward cost pass-through; heat accounts for roughly 70% of building energy demand. Short-term tariff shifts and a 2024 EU ETS price near €90/tCO2 have raised supplier leverage and operating costs. Investments in heat pumps and PV can steadily cut dependence and exposure over time.

Technology and facility services

Technology and facility services for Vonovia rely on specialized vendors for smart metering, building automation and FM platforms, creating switching barriers from integration costs and data lock-in; Vonovia held about 565,000 residential units in 2024, making vendor leverage material. Long-term SLAs stabilize operations but strengthen supplier bargaining power; in-house teams and open standards can rebalance it.

Capital providers and refinancing

Banks, bondholders and public markets are key capital suppliers for Vonovia; ECB policy tightening (deposit rate ~4% in mid-2024) and wider credit spreads have raised refinancing costs, squeezing acquisition and development returns, while covenant terms can limit flexibility in downturns; Vonovia’s investment-grade positioning and strong asset backing mitigate but do not eliminate lenders’ leverage.

- ECB rate ~4% (mid-2024)

- Higher credit spreads ↑ refinancing cost

- Covenants constrain strategy in stress

- IG status + asset backing = partial buffer

Regional contractor constraints boost supplier leverage, raising renovation costs

Regional contractors and specialists were capacity‑constrained in 2024, boosting supplier leverage and raising renovation lead times and costs. Vonovia’s scale—~570,000 units and ~12,000 employees—plus in‑house craft teams and framework deals mitigate but do not remove pressure. Commodity and energy volatility (EU ETS ~€90/tCO2) and ECB rates (~4%) kept supplier influence high.

| Metric | 2024 |

|---|---|

| Residential units | ~570,000 |

| Employees | ~12,000 |

| EU ETS price | ~€90/tCO2 |

| ECB deposit rate | ~4% |

What is included in the product

Tailored Porter’s Five Forces analysis for Vonovia that uncovers key competitive drivers, evaluates supplier and tenant (buyer) power, and identifies threats from substitutes and new entrants affecting pricing and profitability. Includes strategic insights on disruptive trends and barriers protecting incumbents to support investor materials and internal strategy.

A concise one-sheet Vonovia Porter’s Five Forces that instantly visualizes strategic pressure with a spider chart, lets you customize force levels for regulatory or market shifts, and slots into decks or Excel dashboards—no macros, easy for non‑finance teams.

Customers Bargaining Power

Fragmented tenants, regulated rents

Individual tenants are numerous and exert low direct bargaining power against Vonovia, which manages roughly 565,000 residential units, about 80% in Germany. German rent regulation — the Mietpreisbremse capping new rents at about 10% above local comparables and common limits on increases (typically ~15% over three years) — materially restricts pricing freedom. This regulatory framework creates indirect buyer power via policy rather than negotiation and tenant-protection laws raise landlords’ switching and eviction costs.

Vacancy sensitivity in micro-markets

Aggregate demand for rental housing in Germany remains strong with roughly 50% of households renting and Vonovia holding about 570,000 units in 2024, but local oversupply or lower asset quality boosts tenant leverage in specific micro-markets. In weaker submarkets, incentives or targeted capex are often required to achieve lettings and maintain yields. Product differentiation through modernization and services reduces price sensitivity, while location and connectivity remain decisive for occupancy and rent growth.

Tenant associations and political influence

Organized tenant bodies, including the Deutscher Mieterbund (~1.5 million members), shape public debate and regulation that targets large landlords like Vonovia, which holds roughly 565,000 residential units, increasing collective leverage beyond individual renters. Political scrutiny on affordability—evident in tightened Mietpreisbremse rules—constrains rent growth and fee structures. Media visibility amplifies tenant concerns into rapid policy responses and reputational risk, heightening buyer power over pricing and service terms.

Service expectations and ESG

Tenants increasingly demand energy efficiency, comfort and digital services; for Vonovia — owner/manager of about 415,000 residential units in 2024 — poor service or disruptive retrofits can trigger churn and reputational costs. Delivering measurable ESG benefits raises willingness to pay and lowers buyer power; misalignment invites complaints and regulatory scrutiny.

- Tenants: prioritize efficiency, comfort, digital access

- Risk: retrofit disruption → churn

- ESG: measurable gains → higher willingness to pay

- Misalignment → complaints/regulatory attention

Alternative housing choices

Cooperatives, municipal housing and suburban alternatives expand tenant options and, together with remote/hybrid work enabling moves for affordability, weaken Vonovias pricing power where credible substitutes exist. Germanys rentership remains around 56% (2024), but vacancy in major supply-constrained cities often stays below 2%, preserving landlord leverage.

- Cooperatives: alternative tenure

- Municipal housing: capped rents

- Suburbs: affordability via relocation

- Vacancy <2% in tight cities: lower buyer power

Major landlord: low tenant bargaining power, strong regulatory and collective pressure

Individual tenants exert low direct bargaining power vs Vonovia (≈570,000 units, 2024) but strong indirect power via regulation: Mietpreisbremse caps new rents ≈10% above local comparables and typical limits ≈15% over 3 years; organized tenant groups (Deutscher Mieterbund ≈1.5M) and ESG demands raise collective leverage. Vacancy <2% in tight cities sustains local landlord power.

| Metric | Value (2024) |

|---|---|

| Vonovia units | ≈570,000 |

| Rentership Germany | 56% |

| Vacancy (tight cities) | <2% |

| Mietpreisbremse cap | ≈+10% |

| Increase limit | ≈15% / 3 yrs |

| Deutscher Mieterbund | ≈1.5M members |

Preview Before You Purchase

Vonovia Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is the complete Vonovia Porter's Five Forces analysis, professionally formatted and ready to use. You’ll get instant access to this identical file upon buying.