Voya Financial Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Voya Financial faces moderate buyer power, concentrated regulation-driven supplier dynamics, and strong rivalry from insurers and wealth managers, with digital entrants raising the threat of substitutes. This snapshot highlights key competitive pressures and strategic levers Voya can use to defend margins. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown and actionable insights.

Suppliers Bargaining Power

Dependence on tech and data vendors

Core systems, cloud providers and market data vendors underpin Voya’s recordkeeping and investment operations; in 2024 AWS, Azure and GCP held about 66% of cloud market share (AWS 32%, Azure 23%, GCP 11%) and Bloomberg reported ~325,000 terminal subscribers. Concentrated providers can push tougher terms and pass through cost increases, while costly, risky core-platform switches grant suppliers leverage. Multi-vendor strategies and selective in-house tools can blunt that power.

Reinsurers and capital market counterparties

Reinsurers and derivatives/collateral counterparties materially shape pricing and capacity for Voya’s insurance and guarantee products, with 2024 market retrenchment after large catastrophe years tightening terms and increasing collateral demands. Counterparty stress can reduce availability or raise cost on short notice. Long-term relationships and diversified counterparty panels limit single-counterparty exposure. Voya’s strong balance sheet and robust collateral management improve its negotiating leverage.

Distribution intermediaries and advisors

Broker-dealers, benefits consultants and advisors control access to the largest plan sponsors, with Cerulli Associates 2024 estimating they influence roughly 70% of defined-contribution plan placements. Preferred-shelf arrangements and consulting influence can extract revenue sharing or service concessions from providers. Voya’s brand and product breadth help secure placement, but dependence on intermediaries creates supplier-like bargaining power. Growing direct digital channels are reducing that reliance over time.

Talent and specialized service providers

Index licensors and benchmarks

Use of major indices requires costly, often inflexible licenses (typically 1–10 basis points annually); limited substitutes for flagship benchmarks concentrate supplier power and can squeeze margins. Custom indices and multi-index options lower dependency, and Voya’s scale—about $260 billion AUM in 2024—improves negotiation leverage across strategies.

- License cost: 1–10 bps

- Substitute scarcity: high for flagship benchmarks

- Mitigation: custom/multi-index solutions

- Scale leverage: ~260B AUM (2024)

Asset manager faces concentrated cloud/vendor power, talent squeeze; $260B AUM buffers risk

Voya faces concentrated supplier power from cloud providers (AWS/Azure/GCP ~66% combined in 2024), Bloomberg terminals (~325k subs), reinsurer tightening after cat years, and intermediaries influencing ~70% of DC placements. Talent scarcity (median pay $120k–$180k) and index license costs (1–10 bps) add pressure; Voya’s ~ $260B AUM and diversified counterparties mitigate risk.

| Metric | 2024 Value |

|---|---|

| Cloud share (AWS/Azure/GCP) | ~66% |

| Bloomberg subs | ~325,000 |

| Reinsurer/market tightening | Heightened |

| Intermediary influence on DC | ~70% |

| Talent median pay | $120k–$180k |

| Index license cost | 1–10 bps |

| AUM | $260B |

What is included in the product

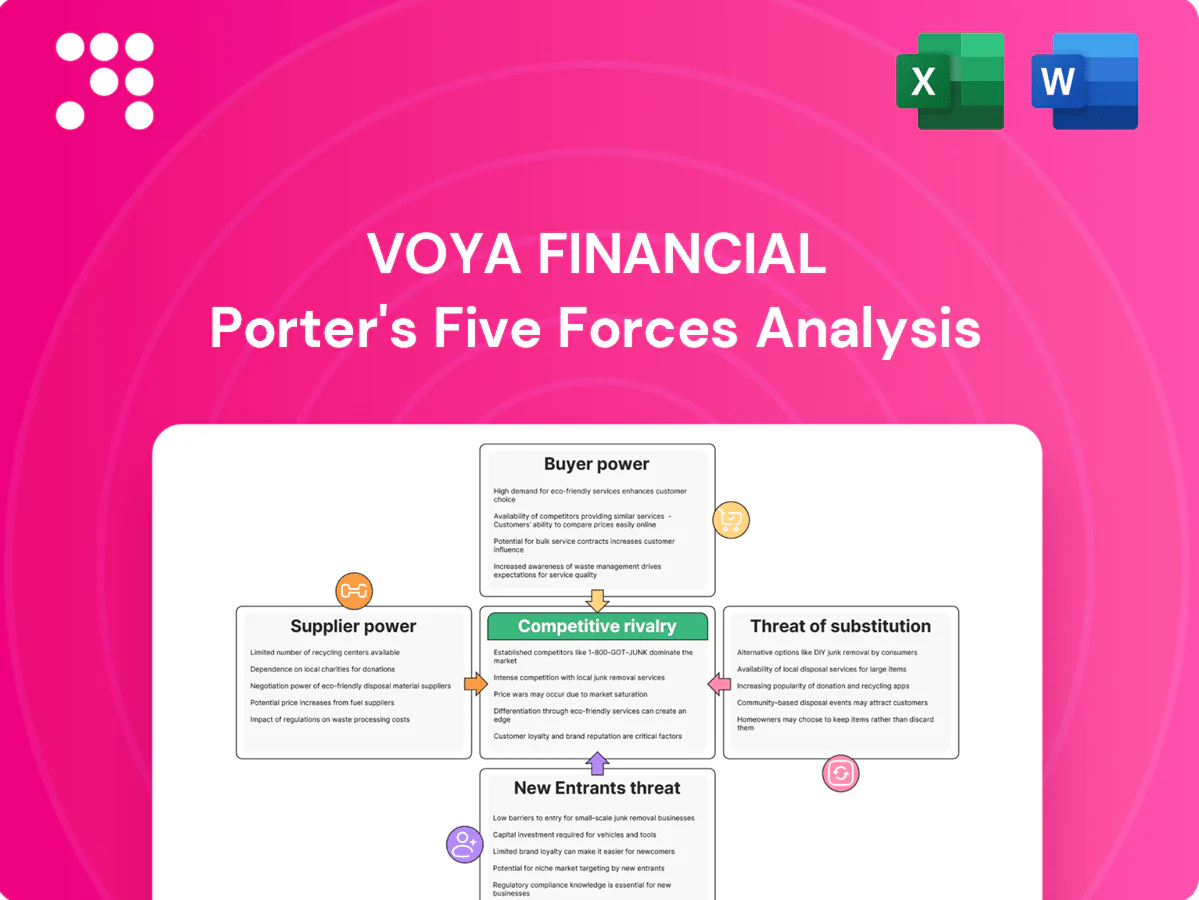

Concise Porter's Five Forces analysis of Voya Financial highlighting competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, plus regulatory and technological disruptors shaping profitability.

A concise one-sheet Porter's Five Forces for Voya Financial that visualizes competitive pressure with an editable spider chart, customizable scores for changing market conditions, and a clean layout ready for decks—no macros required.

Customers Bargaining Power

Concentrated plan sponsors

In 2024 concentrated plan sponsors—large employers and institutions—ran competitive RFPs that increasingly demanded low fees and high service levels, using scale to exert aggressive pricing pressure. Their size and need for customization and integration raise switching costs yet elevate performance and reporting expectations. Strong referenceability and demonstrable outcomes remain key defenses for Voya to sustain pricing.

Transparent fee environment

Regulatory disclosure and benchmarking have made retirement/investment fees highly visible, with passive funds reaching about 50% of US fund assets in 2024 (Morningstar), so buyers routinely compare bps across rivals. This transparency and fee pressure favor passive and low-fee options, compressing margins. Voya must demonstrate value via outcomes, UX, and financial wellness services to sustain fee levels.

Advisor and consultant influence

Gatekeepers such as advisors and consultants shape Voya’s shortlists and negotiate fees and SLAs, with consultants often demanding penalties for underperformance; Voya reported approximately $293 billion AUM in 2024, making consultant endorsements material to its growth. Strong advisor relationships and demonstrable, data-backed outcomes drive recommendations, while loss of consultant favor can sharply reduce pipeline and new institutional flows.

Participant choice and inertia

End participants can pick funds, advice tiers, and insurance add-ons, and while inertia historically limits churn, 2024 trends show digital comparators increasing visibility into fees and performance, heightening sensitivity; targeted education and behavioral nudges lift engagement and cross-sell, while poor UX can prompt both plan-level and participant-level switching.

- Choice: funds, advice, insurance

- Inertia vs digital comparators

- Education/nudges boost engagement

- Poor UX triggers switching

Demand for integrated health-wealth solutions

Employers increasingly demand bundled retirement, benefits, and financial-wellness solutions, using integrated packages to extract discounts and stronger contract terms from providers.

Integration increases client stickiness but raises delivery complexity and implementation costs for firms like Voya; Voya’s multi-line capabilities and distribution scale help offset raw price pressure.

- Buyers leverage bundles to negotiate discounts

- Integration = higher retention but higher delivery cost

- Voya’s multi-line scale mitigates pure price competition

Aggressive RFPs, 50% passive, consultant influence and $293B provider sway compress fees

In 2024 concentrated plan sponsors ran aggressive RFPs demanding low fees and high service, creating strong pricing pressure. Regulatory disclosure and passive funds reaching about 50% of US fund assets (Morningstar) compressed margins and fueled fee benchmarking. Gatekeepers matter: Voya reported approximately $293 billion AUM in 2024, making consultant endorsements material. Bundling raises stickiness but raises delivery cost.

| Metric | 2024 value |

|---|---|

| Voya AUM | $293B |

| Passive share (US funds) | ~50% (Morningstar) |

| Consultant influence | High |

Preview the Actual Deliverable

Voya Financial Porter's Five Forces Analysis

This preview shows the exact Voya Financial Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted and professionally written, ready for download and use the moment you buy. It delivers the complete competitive assessment, implications and actionable insights to support strategic and investment decisions.

Go Beyond the Preview—Access the Full Strategic Report

Voya Financial faces moderate buyer power, concentrated regulation-driven supplier dynamics, and strong rivalry from insurers and wealth managers, with digital entrants raising the threat of substitutes. This snapshot highlights key competitive pressures and strategic levers Voya can use to defend margins. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown and actionable insights.

Suppliers Bargaining Power

Dependence on tech and data vendors

Core systems, cloud providers and market data vendors underpin Voya’s recordkeeping and investment operations; in 2024 AWS, Azure and GCP held about 66% of cloud market share (AWS 32%, Azure 23%, GCP 11%) and Bloomberg reported ~325,000 terminal subscribers. Concentrated providers can push tougher terms and pass through cost increases, while costly, risky core-platform switches grant suppliers leverage. Multi-vendor strategies and selective in-house tools can blunt that power.

Reinsurers and capital market counterparties

Reinsurers and derivatives/collateral counterparties materially shape pricing and capacity for Voya’s insurance and guarantee products, with 2024 market retrenchment after large catastrophe years tightening terms and increasing collateral demands. Counterparty stress can reduce availability or raise cost on short notice. Long-term relationships and diversified counterparty panels limit single-counterparty exposure. Voya’s strong balance sheet and robust collateral management improve its negotiating leverage.

Distribution intermediaries and advisors

Broker-dealers, benefits consultants and advisors control access to the largest plan sponsors, with Cerulli Associates 2024 estimating they influence roughly 70% of defined-contribution plan placements. Preferred-shelf arrangements and consulting influence can extract revenue sharing or service concessions from providers. Voya’s brand and product breadth help secure placement, but dependence on intermediaries creates supplier-like bargaining power. Growing direct digital channels are reducing that reliance over time.

Talent and specialized service providers

Index licensors and benchmarks

Use of major indices requires costly, often inflexible licenses (typically 1–10 basis points annually); limited substitutes for flagship benchmarks concentrate supplier power and can squeeze margins. Custom indices and multi-index options lower dependency, and Voya’s scale—about $260 billion AUM in 2024—improves negotiation leverage across strategies.

- License cost: 1–10 bps

- Substitute scarcity: high for flagship benchmarks

- Mitigation: custom/multi-index solutions

- Scale leverage: ~260B AUM (2024)

Asset manager faces concentrated cloud/vendor power, talent squeeze; $260B AUM buffers risk

Voya faces concentrated supplier power from cloud providers (AWS/Azure/GCP ~66% combined in 2024), Bloomberg terminals (~325k subs), reinsurer tightening after cat years, and intermediaries influencing ~70% of DC placements. Talent scarcity (median pay $120k–$180k) and index license costs (1–10 bps) add pressure; Voya’s ~ $260B AUM and diversified counterparties mitigate risk.

| Metric | 2024 Value |

|---|---|

| Cloud share (AWS/Azure/GCP) | ~66% |

| Bloomberg subs | ~325,000 |

| Reinsurer/market tightening | Heightened |

| Intermediary influence on DC | ~70% |

| Talent median pay | $120k–$180k |

| Index license cost | 1–10 bps |

| AUM | $260B |

What is included in the product

Concise Porter's Five Forces analysis of Voya Financial highlighting competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, plus regulatory and technological disruptors shaping profitability.

A concise one-sheet Porter's Five Forces for Voya Financial that visualizes competitive pressure with an editable spider chart, customizable scores for changing market conditions, and a clean layout ready for decks—no macros required.

Customers Bargaining Power

Concentrated plan sponsors

In 2024 concentrated plan sponsors—large employers and institutions—ran competitive RFPs that increasingly demanded low fees and high service levels, using scale to exert aggressive pricing pressure. Their size and need for customization and integration raise switching costs yet elevate performance and reporting expectations. Strong referenceability and demonstrable outcomes remain key defenses for Voya to sustain pricing.

Transparent fee environment

Regulatory disclosure and benchmarking have made retirement/investment fees highly visible, with passive funds reaching about 50% of US fund assets in 2024 (Morningstar), so buyers routinely compare bps across rivals. This transparency and fee pressure favor passive and low-fee options, compressing margins. Voya must demonstrate value via outcomes, UX, and financial wellness services to sustain fee levels.

Advisor and consultant influence

Gatekeepers such as advisors and consultants shape Voya’s shortlists and negotiate fees and SLAs, with consultants often demanding penalties for underperformance; Voya reported approximately $293 billion AUM in 2024, making consultant endorsements material to its growth. Strong advisor relationships and demonstrable, data-backed outcomes drive recommendations, while loss of consultant favor can sharply reduce pipeline and new institutional flows.

Participant choice and inertia

End participants can pick funds, advice tiers, and insurance add-ons, and while inertia historically limits churn, 2024 trends show digital comparators increasing visibility into fees and performance, heightening sensitivity; targeted education and behavioral nudges lift engagement and cross-sell, while poor UX can prompt both plan-level and participant-level switching.

- Choice: funds, advice, insurance

- Inertia vs digital comparators

- Education/nudges boost engagement

- Poor UX triggers switching

Demand for integrated health-wealth solutions

Employers increasingly demand bundled retirement, benefits, and financial-wellness solutions, using integrated packages to extract discounts and stronger contract terms from providers.

Integration increases client stickiness but raises delivery complexity and implementation costs for firms like Voya; Voya’s multi-line capabilities and distribution scale help offset raw price pressure.

- Buyers leverage bundles to negotiate discounts

- Integration = higher retention but higher delivery cost

- Voya’s multi-line scale mitigates pure price competition

Aggressive RFPs, 50% passive, consultant influence and $293B provider sway compress fees

In 2024 concentrated plan sponsors ran aggressive RFPs demanding low fees and high service, creating strong pricing pressure. Regulatory disclosure and passive funds reaching about 50% of US fund assets (Morningstar) compressed margins and fueled fee benchmarking. Gatekeepers matter: Voya reported approximately $293 billion AUM in 2024, making consultant endorsements material. Bundling raises stickiness but raises delivery cost.

| Metric | 2024 value |

|---|---|

| Voya AUM | $293B |

| Passive share (US funds) | ~50% (Morningstar) |

| Consultant influence | High |

Preview the Actual Deliverable

Voya Financial Porter's Five Forces Analysis

This preview shows the exact Voya Financial Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted and professionally written, ready for download and use the moment you buy. It delivers the complete competitive assessment, implications and actionable insights to support strategic and investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Voya Financial faces moderate buyer power, concentrated regulation-driven supplier dynamics, and strong rivalry from insurers and wealth managers, with digital entrants raising the threat of substitutes. This snapshot highlights key competitive pressures and strategic levers Voya can use to defend margins. Ready to move beyond the basics? Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown and actionable insights.

Suppliers Bargaining Power

Dependence on tech and data vendors

Core systems, cloud providers and market data vendors underpin Voya’s recordkeeping and investment operations; in 2024 AWS, Azure and GCP held about 66% of cloud market share (AWS 32%, Azure 23%, GCP 11%) and Bloomberg reported ~325,000 terminal subscribers. Concentrated providers can push tougher terms and pass through cost increases, while costly, risky core-platform switches grant suppliers leverage. Multi-vendor strategies and selective in-house tools can blunt that power.

Reinsurers and capital market counterparties

Reinsurers and derivatives/collateral counterparties materially shape pricing and capacity for Voya’s insurance and guarantee products, with 2024 market retrenchment after large catastrophe years tightening terms and increasing collateral demands. Counterparty stress can reduce availability or raise cost on short notice. Long-term relationships and diversified counterparty panels limit single-counterparty exposure. Voya’s strong balance sheet and robust collateral management improve its negotiating leverage.

Distribution intermediaries and advisors

Broker-dealers, benefits consultants and advisors control access to the largest plan sponsors, with Cerulli Associates 2024 estimating they influence roughly 70% of defined-contribution plan placements. Preferred-shelf arrangements and consulting influence can extract revenue sharing or service concessions from providers. Voya’s brand and product breadth help secure placement, but dependence on intermediaries creates supplier-like bargaining power. Growing direct digital channels are reducing that reliance over time.

Talent and specialized service providers

Index licensors and benchmarks

Use of major indices requires costly, often inflexible licenses (typically 1–10 basis points annually); limited substitutes for flagship benchmarks concentrate supplier power and can squeeze margins. Custom indices and multi-index options lower dependency, and Voya’s scale—about $260 billion AUM in 2024—improves negotiation leverage across strategies.

- License cost: 1–10 bps

- Substitute scarcity: high for flagship benchmarks

- Mitigation: custom/multi-index solutions

- Scale leverage: ~260B AUM (2024)

Asset manager faces concentrated cloud/vendor power, talent squeeze; $260B AUM buffers risk

Voya faces concentrated supplier power from cloud providers (AWS/Azure/GCP ~66% combined in 2024), Bloomberg terminals (~325k subs), reinsurer tightening after cat years, and intermediaries influencing ~70% of DC placements. Talent scarcity (median pay $120k–$180k) and index license costs (1–10 bps) add pressure; Voya’s ~ $260B AUM and diversified counterparties mitigate risk.

| Metric | 2024 Value |

|---|---|

| Cloud share (AWS/Azure/GCP) | ~66% |

| Bloomberg subs | ~325,000 |

| Reinsurer/market tightening | Heightened |

| Intermediary influence on DC | ~70% |

| Talent median pay | $120k–$180k |

| Index license cost | 1–10 bps |

| AUM | $260B |

What is included in the product

Concise Porter's Five Forces analysis of Voya Financial highlighting competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, plus regulatory and technological disruptors shaping profitability.

A concise one-sheet Porter's Five Forces for Voya Financial that visualizes competitive pressure with an editable spider chart, customizable scores for changing market conditions, and a clean layout ready for decks—no macros required.

Customers Bargaining Power

Concentrated plan sponsors

In 2024 concentrated plan sponsors—large employers and institutions—ran competitive RFPs that increasingly demanded low fees and high service levels, using scale to exert aggressive pricing pressure. Their size and need for customization and integration raise switching costs yet elevate performance and reporting expectations. Strong referenceability and demonstrable outcomes remain key defenses for Voya to sustain pricing.

Transparent fee environment

Regulatory disclosure and benchmarking have made retirement/investment fees highly visible, with passive funds reaching about 50% of US fund assets in 2024 (Morningstar), so buyers routinely compare bps across rivals. This transparency and fee pressure favor passive and low-fee options, compressing margins. Voya must demonstrate value via outcomes, UX, and financial wellness services to sustain fee levels.

Advisor and consultant influence

Gatekeepers such as advisors and consultants shape Voya’s shortlists and negotiate fees and SLAs, with consultants often demanding penalties for underperformance; Voya reported approximately $293 billion AUM in 2024, making consultant endorsements material to its growth. Strong advisor relationships and demonstrable, data-backed outcomes drive recommendations, while loss of consultant favor can sharply reduce pipeline and new institutional flows.

Participant choice and inertia

End participants can pick funds, advice tiers, and insurance add-ons, and while inertia historically limits churn, 2024 trends show digital comparators increasing visibility into fees and performance, heightening sensitivity; targeted education and behavioral nudges lift engagement and cross-sell, while poor UX can prompt both plan-level and participant-level switching.

- Choice: funds, advice, insurance

- Inertia vs digital comparators

- Education/nudges boost engagement

- Poor UX triggers switching

Demand for integrated health-wealth solutions

Employers increasingly demand bundled retirement, benefits, and financial-wellness solutions, using integrated packages to extract discounts and stronger contract terms from providers.

Integration increases client stickiness but raises delivery complexity and implementation costs for firms like Voya; Voya’s multi-line capabilities and distribution scale help offset raw price pressure.

- Buyers leverage bundles to negotiate discounts

- Integration = higher retention but higher delivery cost

- Voya’s multi-line scale mitigates pure price competition

Aggressive RFPs, 50% passive, consultant influence and $293B provider sway compress fees

In 2024 concentrated plan sponsors ran aggressive RFPs demanding low fees and high service, creating strong pricing pressure. Regulatory disclosure and passive funds reaching about 50% of US fund assets (Morningstar) compressed margins and fueled fee benchmarking. Gatekeepers matter: Voya reported approximately $293 billion AUM in 2024, making consultant endorsements material. Bundling raises stickiness but raises delivery cost.

| Metric | 2024 value |

|---|---|

| Voya AUM | $293B |

| Passive share (US funds) | ~50% (Morningstar) |

| Consultant influence | High |

Preview the Actual Deliverable

Voya Financial Porter's Five Forces Analysis

This preview shows the exact Voya Financial Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted and professionally written, ready for download and use the moment you buy. It delivers the complete competitive assessment, implications and actionable insights to support strategic and investment decisions.