Vertex Pharmaceuticals Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

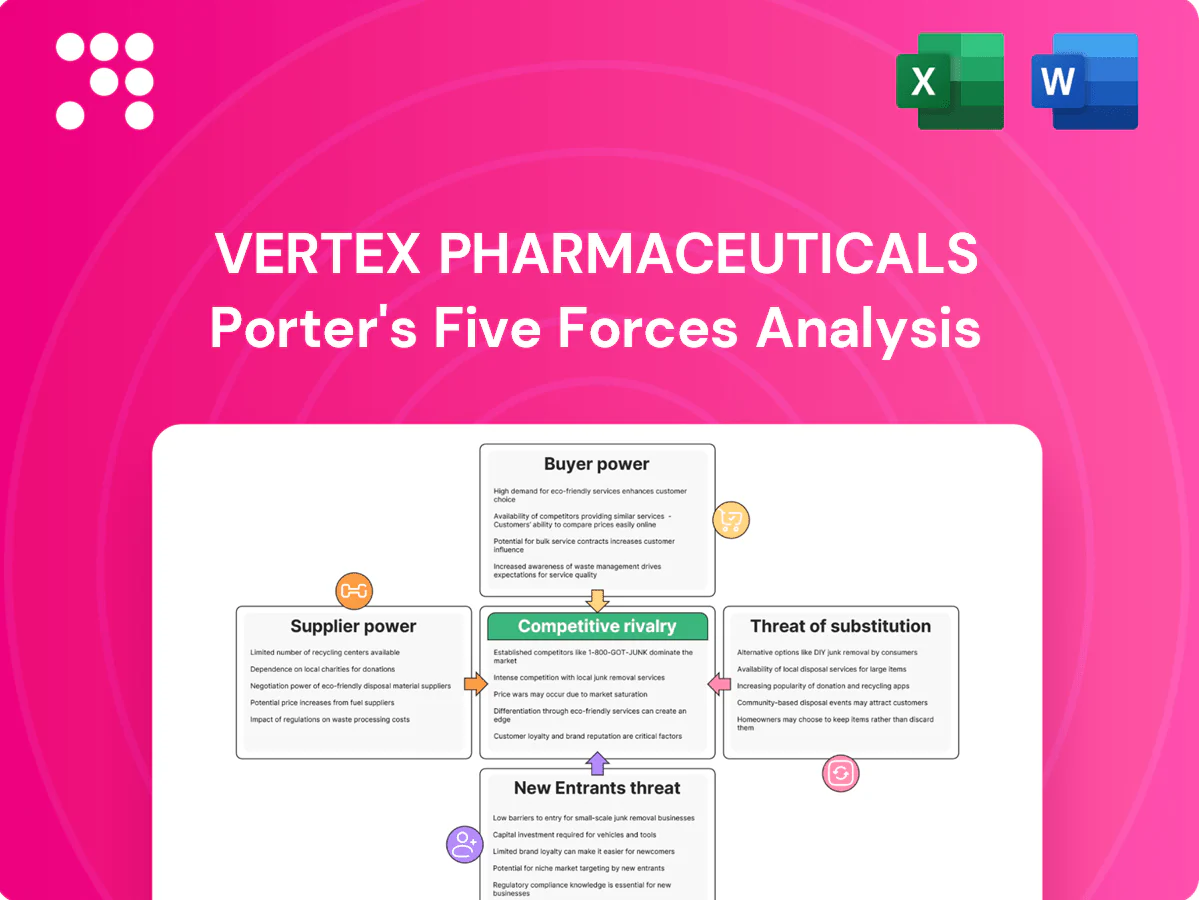

Vertex Pharmaceuticals faces strong supplier power for specialized inputs, moderate buyer leverage, intense rivalry among biotech peers, and high entry barriers tempered by emerging substitute therapies and platform competition. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vertex Pharmaceuticals’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty inputs

Concentrated specialty inputs for small molecules and advanced therapies force Vertex to rely on scarce high-purity APIs, lipids and gene-editing components sourced from fewer than five qualified vendors in many cases, increasing switching costs and lead times. Any quality deviation can delay production batches and regulatory filings. This supplier concentration grants vendors leverage over price and contractual terms in 2024.

CRO/CMO dependence

Vertex relies on external CROs and CMOs for trials and some manufacturing steps, creating supplier leverage as regulatory-grade capacity is limited and not easily substitutable in 2024.

Priority access typically requires volume and long-term commitments, with vendors demanding minimums that lock in capacity and pricing.

Vendors can push escalators and tighter SLAs, pressuring margins and operational flexibility for Vertex.

Platform and IP licensors

Platform and IP licensors — covering gene editing, delivery vectors and enabling tech — often impose royalty and milestone structures that can reach hundreds of millions in aggregate, creating ongoing financial burdens and limited outside options for Vertex when unique patents are involved. Renegotiations become costly as programs advance, concentrating bargaining power with IP holders and raising sunk-cost risks for late-stage assets.

Skilled talent as a supplier

Vertex R&D depends on scarce scientists in CFTR biology, gene editing, and protein chemistry, with tight labor markets in biotech hubs (Boston, San Francisco) fueling a 2024 uptick in hiring premiums and turnover; elevated retention packages and recruiting costs raise input pricing and give talent greater leverage over compensation and schedule flexibility.

- Scarce CFTR/gene-editing expertise

- Tight biotech hubs labor markets

- 2024 hiring premiums up, raising costs

- Higher retention = greater supplier power

Regulatory-grade materials compliance

Regulatory-grade materials compliance forces audit-ready documentation and strict cGMP adherence, narrowing qualified supplier pools and strengthening the negotiating position of approved vendors; Vertex reported roughly $9.0 billion in 2024 revenue, reinforcing its reliance on validated suppliers. Dual-sourcing is feasible but validation typically requires 6–18 months, so remediation or supplier switches add measurable cost and schedule risk.

- cGMP audits limit pool

- Validation 6–18 months

- Remediation = added cost/schedule risk

- Approved suppliers gain leverage

Supplier concentration and cGMP bottlenecks raise switching costs for $9.0B

Supplier concentration for high‑purity APIs, lipids and gene‑editing components (often <5 qualified vendors) gives vendors pricing and contractual leverage; quality deviations and 6–18 month validation windows raise switching costs. Limited CRO/CMO capacity and cGMP constraints reinforce supplier power. Talent premiums in biotech hubs and Vertex’s ~$9.0B 2024 revenue increase dependence on validated suppliers.

| Metric | Value |

|---|---|

| 2024 revenue | $9.0B |

| Qualified suppliers | <5 (many inputs) |

| Validation time | 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Vertex Pharmaceuticals revealing competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, and disruptive risks shaping pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces overview for Vertex Pharmaceuticals—instantly highlights competitive pressures and regulatory risk to speed strategic decisions; customizable pressure levels and a spider chart make it easy to model scenarios and drop directly into investor decks or boardroom slides.

Customers Bargaining Power

Payers and HTA gatekeepers

Insurers and national systems (public payers fund about 73% of health spending in OECD countries) drive access and pricing for Vertex rare-disease drugs. HTA bodies such as NICE and ICER (often using $100,000–$150,000 per QALY thresholds) scrutinize value and budget impact. Outcomes-based and risk-sharing contracts temper list prices. Concentrated payer power—top US insurers cover a majority of commercially insured lives—limits net pricing leverage.

Limited alternatives for CF

CFTR modulators have few therapeutic substitutes, with elexacaftor/tezacaftor/ivacaftor eligible for roughly 90% of the ~100,000 people with cystic fibrosis worldwide, limiting switching. Strong clinical differentiation and robust outcomes data have lowered buyer power and supported premium pricing. Single-indication dependence increases payer scrutiny of total spend. Negotiations frequently focus on eligibility criteria and treatment duration.

Specialty pharmacy and treatment centers

Distribution of Vertex CF therapies flows primarily through specialty pharmacies and CF centers of excellence, with the three largest PBMs covering roughly 80% of commercial lives in 2024, giving intermediaries strong influence over formulary placement and adherence programs. Their continued consolidation pressures service fees and contracting terms, though the high value placed on continuity of care and comprehensive patient support for CF treatments tempers extreme concessions.

Patient advocacy influence

Rare-disease communities (NORD: ~7,000 disorders; WHO: ~300 million people worldwide) are highly organized and vocal, often pressuring payers and regulators to secure coverage; for Vertex, which markets four approved CF modulators (Kalydeco, Orkambi, Symdeko, Trikafta), this advocacy can bolster reimbursement and sustain premium pricing, while public scrutiny on affordability drives demands for broader discounts, producing a balanced customer power dynamic.

- 7,000 rare diseases (NORD)

- ~300M affected worldwide (WHO)

- 4 CF modulators at Vertex

Global reference pricing

Global reference pricing and tendering in international markets compress price ceilings, and cross-border price corridors limit Vertex’s ability to capture premiums; as of 2024, more than 100 countries use external reference pricing, amplifying downward pressure. Launch sequencing is used to protect U.S. net price, but coordinated buyer actions and tenders raise buyer power outside the U.S. and pull down global average realized prices.

- Reference pricing: 100+ countries (2024)

- Impact: constrains premium capture across markets

- Strategy: launch sequencing to shield U.S. net price

- Result: higher buyer power abroad lowers global averages

Payers, PBMs control CF modulator access — 73% OECD public share

Insurers and public payers (73% of OECD health spending) and concentrated PBMs (~80% US commercial lives, 2024) drive access and net pricing. CF modulators cover ~90% of ~100,000 people with cystic fibrosis, limiting substitutes but increasing payer scrutiny. External reference pricing in 100+ countries and HTA thresholds ($100–150k/QALY) constrain global price capture.

| Metric | Value |

|---|---|

| Public payer share (OECD) | 73% |

| PBM coverage (US, 2024) | ~80% |

| CF eligible | ~90% of ~100,000 |

| Countries with ERP (2024) | 100+ |

Same Document Delivered

Vertex Pharmaceuticals Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is a comprehensive Porter's Five Forces analysis of Vertex Pharmaceuticals, covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with data-driven insights. The file is fully formatted and ready for immediate download and use.

Go Beyond the Preview—Access the Full Strategic Report

Vertex Pharmaceuticals faces strong supplier power for specialized inputs, moderate buyer leverage, intense rivalry among biotech peers, and high entry barriers tempered by emerging substitute therapies and platform competition. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vertex Pharmaceuticals’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty inputs

Concentrated specialty inputs for small molecules and advanced therapies force Vertex to rely on scarce high-purity APIs, lipids and gene-editing components sourced from fewer than five qualified vendors in many cases, increasing switching costs and lead times. Any quality deviation can delay production batches and regulatory filings. This supplier concentration grants vendors leverage over price and contractual terms in 2024.

CRO/CMO dependence

Vertex relies on external CROs and CMOs for trials and some manufacturing steps, creating supplier leverage as regulatory-grade capacity is limited and not easily substitutable in 2024.

Priority access typically requires volume and long-term commitments, with vendors demanding minimums that lock in capacity and pricing.

Vendors can push escalators and tighter SLAs, pressuring margins and operational flexibility for Vertex.

Platform and IP licensors

Platform and IP licensors — covering gene editing, delivery vectors and enabling tech — often impose royalty and milestone structures that can reach hundreds of millions in aggregate, creating ongoing financial burdens and limited outside options for Vertex when unique patents are involved. Renegotiations become costly as programs advance, concentrating bargaining power with IP holders and raising sunk-cost risks for late-stage assets.

Skilled talent as a supplier

Vertex R&D depends on scarce scientists in CFTR biology, gene editing, and protein chemistry, with tight labor markets in biotech hubs (Boston, San Francisco) fueling a 2024 uptick in hiring premiums and turnover; elevated retention packages and recruiting costs raise input pricing and give talent greater leverage over compensation and schedule flexibility.

- Scarce CFTR/gene-editing expertise

- Tight biotech hubs labor markets

- 2024 hiring premiums up, raising costs

- Higher retention = greater supplier power

Regulatory-grade materials compliance

Regulatory-grade materials compliance forces audit-ready documentation and strict cGMP adherence, narrowing qualified supplier pools and strengthening the negotiating position of approved vendors; Vertex reported roughly $9.0 billion in 2024 revenue, reinforcing its reliance on validated suppliers. Dual-sourcing is feasible but validation typically requires 6–18 months, so remediation or supplier switches add measurable cost and schedule risk.

- cGMP audits limit pool

- Validation 6–18 months

- Remediation = added cost/schedule risk

- Approved suppliers gain leverage

Supplier concentration and cGMP bottlenecks raise switching costs for $9.0B

Supplier concentration for high‑purity APIs, lipids and gene‑editing components (often <5 qualified vendors) gives vendors pricing and contractual leverage; quality deviations and 6–18 month validation windows raise switching costs. Limited CRO/CMO capacity and cGMP constraints reinforce supplier power. Talent premiums in biotech hubs and Vertex’s ~$9.0B 2024 revenue increase dependence on validated suppliers.

| Metric | Value |

|---|---|

| 2024 revenue | $9.0B |

| Qualified suppliers | <5 (many inputs) |

| Validation time | 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Vertex Pharmaceuticals revealing competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, and disruptive risks shaping pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces overview for Vertex Pharmaceuticals—instantly highlights competitive pressures and regulatory risk to speed strategic decisions; customizable pressure levels and a spider chart make it easy to model scenarios and drop directly into investor decks or boardroom slides.

Customers Bargaining Power

Payers and HTA gatekeepers

Insurers and national systems (public payers fund about 73% of health spending in OECD countries) drive access and pricing for Vertex rare-disease drugs. HTA bodies such as NICE and ICER (often using $100,000–$150,000 per QALY thresholds) scrutinize value and budget impact. Outcomes-based and risk-sharing contracts temper list prices. Concentrated payer power—top US insurers cover a majority of commercially insured lives—limits net pricing leverage.

Limited alternatives for CF

CFTR modulators have few therapeutic substitutes, with elexacaftor/tezacaftor/ivacaftor eligible for roughly 90% of the ~100,000 people with cystic fibrosis worldwide, limiting switching. Strong clinical differentiation and robust outcomes data have lowered buyer power and supported premium pricing. Single-indication dependence increases payer scrutiny of total spend. Negotiations frequently focus on eligibility criteria and treatment duration.

Specialty pharmacy and treatment centers

Distribution of Vertex CF therapies flows primarily through specialty pharmacies and CF centers of excellence, with the three largest PBMs covering roughly 80% of commercial lives in 2024, giving intermediaries strong influence over formulary placement and adherence programs. Their continued consolidation pressures service fees and contracting terms, though the high value placed on continuity of care and comprehensive patient support for CF treatments tempers extreme concessions.

Patient advocacy influence

Rare-disease communities (NORD: ~7,000 disorders; WHO: ~300 million people worldwide) are highly organized and vocal, often pressuring payers and regulators to secure coverage; for Vertex, which markets four approved CF modulators (Kalydeco, Orkambi, Symdeko, Trikafta), this advocacy can bolster reimbursement and sustain premium pricing, while public scrutiny on affordability drives demands for broader discounts, producing a balanced customer power dynamic.

- 7,000 rare diseases (NORD)

- ~300M affected worldwide (WHO)

- 4 CF modulators at Vertex

Global reference pricing

Global reference pricing and tendering in international markets compress price ceilings, and cross-border price corridors limit Vertex’s ability to capture premiums; as of 2024, more than 100 countries use external reference pricing, amplifying downward pressure. Launch sequencing is used to protect U.S. net price, but coordinated buyer actions and tenders raise buyer power outside the U.S. and pull down global average realized prices.

- Reference pricing: 100+ countries (2024)

- Impact: constrains premium capture across markets

- Strategy: launch sequencing to shield U.S. net price

- Result: higher buyer power abroad lowers global averages

Payers, PBMs control CF modulator access — 73% OECD public share

Insurers and public payers (73% of OECD health spending) and concentrated PBMs (~80% US commercial lives, 2024) drive access and net pricing. CF modulators cover ~90% of ~100,000 people with cystic fibrosis, limiting substitutes but increasing payer scrutiny. External reference pricing in 100+ countries and HTA thresholds ($100–150k/QALY) constrain global price capture.

| Metric | Value |

|---|---|

| Public payer share (OECD) | 73% |

| PBM coverage (US, 2024) | ~80% |

| CF eligible | ~90% of ~100,000 |

| Countries with ERP (2024) | 100+ |

Same Document Delivered

Vertex Pharmaceuticals Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is a comprehensive Porter's Five Forces analysis of Vertex Pharmaceuticals, covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with data-driven insights. The file is fully formatted and ready for immediate download and use.

Description

Go Beyond the Preview—Access the Full Strategic Report

Vertex Pharmaceuticals faces strong supplier power for specialized inputs, moderate buyer leverage, intense rivalry among biotech peers, and high entry barriers tempered by emerging substitute therapies and platform competition. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Vertex Pharmaceuticals’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty inputs

Concentrated specialty inputs for small molecules and advanced therapies force Vertex to rely on scarce high-purity APIs, lipids and gene-editing components sourced from fewer than five qualified vendors in many cases, increasing switching costs and lead times. Any quality deviation can delay production batches and regulatory filings. This supplier concentration grants vendors leverage over price and contractual terms in 2024.

CRO/CMO dependence

Vertex relies on external CROs and CMOs for trials and some manufacturing steps, creating supplier leverage as regulatory-grade capacity is limited and not easily substitutable in 2024.

Priority access typically requires volume and long-term commitments, with vendors demanding minimums that lock in capacity and pricing.

Vendors can push escalators and tighter SLAs, pressuring margins and operational flexibility for Vertex.

Platform and IP licensors

Platform and IP licensors — covering gene editing, delivery vectors and enabling tech — often impose royalty and milestone structures that can reach hundreds of millions in aggregate, creating ongoing financial burdens and limited outside options for Vertex when unique patents are involved. Renegotiations become costly as programs advance, concentrating bargaining power with IP holders and raising sunk-cost risks for late-stage assets.

Skilled talent as a supplier

Vertex R&D depends on scarce scientists in CFTR biology, gene editing, and protein chemistry, with tight labor markets in biotech hubs (Boston, San Francisco) fueling a 2024 uptick in hiring premiums and turnover; elevated retention packages and recruiting costs raise input pricing and give talent greater leverage over compensation and schedule flexibility.

- Scarce CFTR/gene-editing expertise

- Tight biotech hubs labor markets

- 2024 hiring premiums up, raising costs

- Higher retention = greater supplier power

Regulatory-grade materials compliance

Regulatory-grade materials compliance forces audit-ready documentation and strict cGMP adherence, narrowing qualified supplier pools and strengthening the negotiating position of approved vendors; Vertex reported roughly $9.0 billion in 2024 revenue, reinforcing its reliance on validated suppliers. Dual-sourcing is feasible but validation typically requires 6–18 months, so remediation or supplier switches add measurable cost and schedule risk.

- cGMP audits limit pool

- Validation 6–18 months

- Remediation = added cost/schedule risk

- Approved suppliers gain leverage

Supplier concentration and cGMP bottlenecks raise switching costs for $9.0B

Supplier concentration for high‑purity APIs, lipids and gene‑editing components (often <5 qualified vendors) gives vendors pricing and contractual leverage; quality deviations and 6–18 month validation windows raise switching costs. Limited CRO/CMO capacity and cGMP constraints reinforce supplier power. Talent premiums in biotech hubs and Vertex’s ~$9.0B 2024 revenue increase dependence on validated suppliers.

| Metric | Value |

|---|---|

| 2024 revenue | $9.0B |

| Qualified suppliers | <5 (many inputs) |

| Validation time | 6–18 months |

What is included in the product

Tailored Porter's Five Forces analysis for Vertex Pharmaceuticals revealing competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, and disruptive risks shaping pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces overview for Vertex Pharmaceuticals—instantly highlights competitive pressures and regulatory risk to speed strategic decisions; customizable pressure levels and a spider chart make it easy to model scenarios and drop directly into investor decks or boardroom slides.

Customers Bargaining Power

Payers and HTA gatekeepers

Insurers and national systems (public payers fund about 73% of health spending in OECD countries) drive access and pricing for Vertex rare-disease drugs. HTA bodies such as NICE and ICER (often using $100,000–$150,000 per QALY thresholds) scrutinize value and budget impact. Outcomes-based and risk-sharing contracts temper list prices. Concentrated payer power—top US insurers cover a majority of commercially insured lives—limits net pricing leverage.

Limited alternatives for CF

CFTR modulators have few therapeutic substitutes, with elexacaftor/tezacaftor/ivacaftor eligible for roughly 90% of the ~100,000 people with cystic fibrosis worldwide, limiting switching. Strong clinical differentiation and robust outcomes data have lowered buyer power and supported premium pricing. Single-indication dependence increases payer scrutiny of total spend. Negotiations frequently focus on eligibility criteria and treatment duration.

Specialty pharmacy and treatment centers

Distribution of Vertex CF therapies flows primarily through specialty pharmacies and CF centers of excellence, with the three largest PBMs covering roughly 80% of commercial lives in 2024, giving intermediaries strong influence over formulary placement and adherence programs. Their continued consolidation pressures service fees and contracting terms, though the high value placed on continuity of care and comprehensive patient support for CF treatments tempers extreme concessions.

Patient advocacy influence

Rare-disease communities (NORD: ~7,000 disorders; WHO: ~300 million people worldwide) are highly organized and vocal, often pressuring payers and regulators to secure coverage; for Vertex, which markets four approved CF modulators (Kalydeco, Orkambi, Symdeko, Trikafta), this advocacy can bolster reimbursement and sustain premium pricing, while public scrutiny on affordability drives demands for broader discounts, producing a balanced customer power dynamic.

- 7,000 rare diseases (NORD)

- ~300M affected worldwide (WHO)

- 4 CF modulators at Vertex

Global reference pricing

Global reference pricing and tendering in international markets compress price ceilings, and cross-border price corridors limit Vertex’s ability to capture premiums; as of 2024, more than 100 countries use external reference pricing, amplifying downward pressure. Launch sequencing is used to protect U.S. net price, but coordinated buyer actions and tenders raise buyer power outside the U.S. and pull down global average realized prices.

- Reference pricing: 100+ countries (2024)

- Impact: constrains premium capture across markets

- Strategy: launch sequencing to shield U.S. net price

- Result: higher buyer power abroad lowers global averages

Payers, PBMs control CF modulator access — 73% OECD public share

Insurers and public payers (73% of OECD health spending) and concentrated PBMs (~80% US commercial lives, 2024) drive access and net pricing. CF modulators cover ~90% of ~100,000 people with cystic fibrosis, limiting substitutes but increasing payer scrutiny. External reference pricing in 100+ countries and HTA thresholds ($100–150k/QALY) constrain global price capture.

| Metric | Value |

|---|---|

| Public payer share (OECD) | 73% |

| PBM coverage (US, 2024) | ~80% |

| CF eligible | ~90% of ~100,000 |

| Countries with ERP (2024) | 100+ |

Same Document Delivered

Vertex Pharmaceuticals Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It is a comprehensive Porter's Five Forces analysis of Vertex Pharmaceuticals, covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with data-driven insights. The file is fully formatted and ready for immediate download and use.