Vygon S.A. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

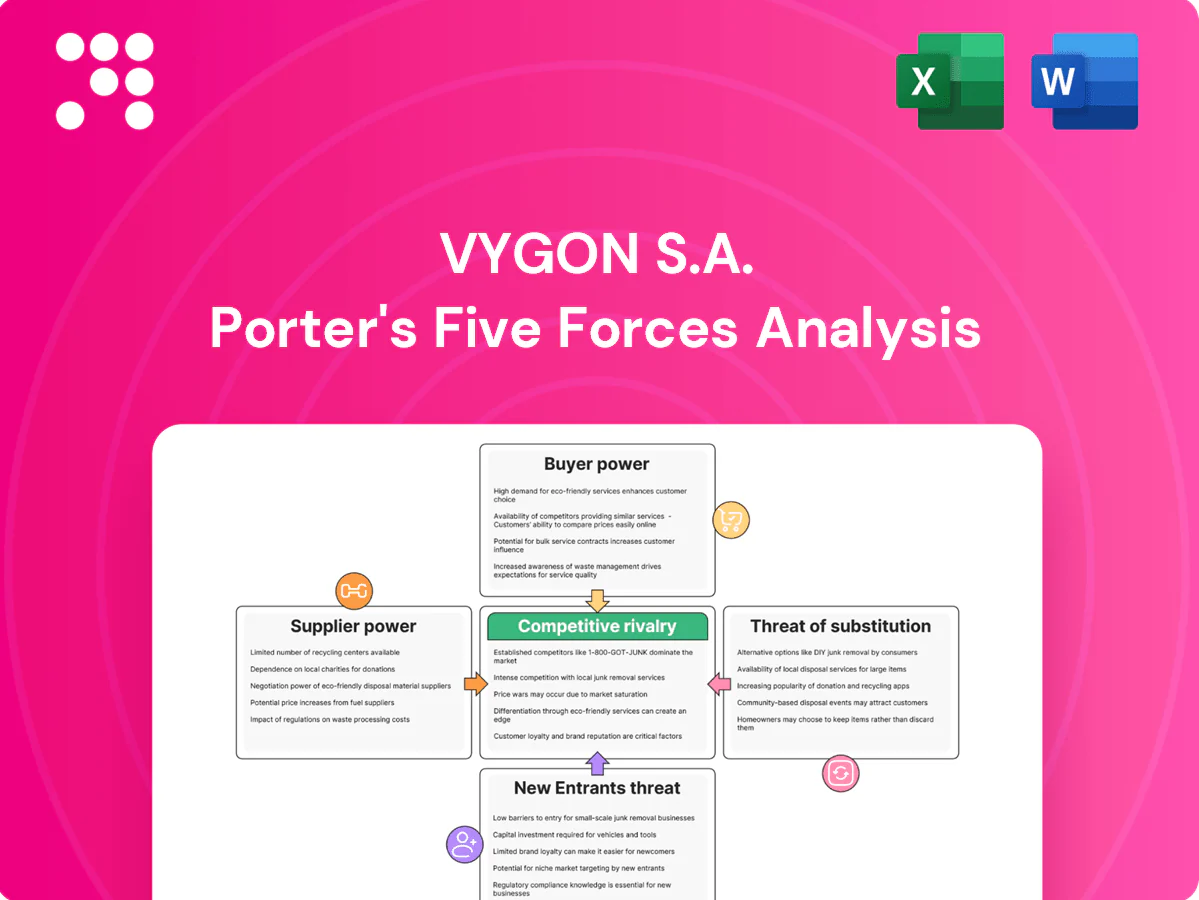

Vygon S.A. faces moderate supplier power, differentiated product strengths, and steady buyer demand, while regulatory barriers and niche specialization limit new entrants. Competitive rivalry is intense in select segments, and substitutes pose targeted threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable, consultant-grade insights.

Suppliers Bargaining Power

Specialized medical-grade materials

Many Vygon devices depend on medical-grade polymers, silicone and specialty resins sourced from a limited pool of certified suppliers, with qualification and biocompatibility testing typically taking 3–12 months and tying materials to specific vendors. This concentration raises switching costs and can extend lead times to several months; dual-sourcing is feasible but slowed by validation burdens.

Sterilization and cleanroom dependencies

Sterilization capacity for ethylene oxide and gamma irradiation is constrained and tightly regulated, so approved providers hold pricing and timing leverage; regional outages and compliance actions (notably 2022–24 plant suspensions) have periodically disrupted medtech supply chains and pushed contract sterilization rates higher. Cleanroom consumables and validated packaging further lock customers in, and Vygon eases risk via multi-site approvals but cannot fully eliminate the bottleneck.

Quality and compliance lock-in

Suppliers holding ISO 13485 and MDR/FDA-ready documentation strengthen bargaining power for Vygon since requalification under EU MDR (effective 26 May 2021) is time-consuming and costly in a global medical device market worth about 600 billion USD in 2024. Design history files often embed supplier-specific specs, so switching risks regulatory delays, product change notices and extended market entry timelines, enabling suppliers to secure better terms on critical components.

Scale vs. supplier concentration

Vygon’s global scale (presence in 100+ countries in 2024) delivers volume leverage and supports multi-year supply agreements, reducing supplier bargaining in standard disposables, while niche components such as specialty catheters and bespoke connectors remain supplied by few vendors, increasing supplier power; overall balance varies by category and moderates average supplier influence.

- Scale: 100+ countries (2024)

- Niche concentration: few specialized suppliers

- Contracts: multi-year agreements

- Mitigation: strategic partnerships stabilize pricing

Logistics and geopolitical exposure

Resin market volatility in 2024, higher energy and recurring transport disruptions have driven input cost spikes, with suppliers commonly passing through increases and invoking force majeure clauses; EU MDR UDI traceability has added upstream administrative burdens, so Vygon must maintain buffer stocks and pursue nearshoring to reduce exposure.

- Resin, energy, transport: 2024 volatility raised input risk

- Suppliers: pass-throughs and force majeure increase bargaining power

- EU MDR: UDI traceability adds upstream admin costs

- Mitigation: buffer stocks and nearshoring recommended

Concentrated suppliers and sterilization bottlenecks elevate medtech supplier leverage

Concentration of certified polymer, silicone and specialty-resin suppliers (qualification 3–12 months) raises switching costs and extends lead times; sterilization capacity constraints and 2022–24 plant suspensions increased supplier leverage. ISO 13485/MDR-ready vendors command premium due to requalification hurdles; Vygon scale (100+ countries, 2024) offsets power for common disposables but not niche components.

| Metric | 2024 value |

|---|---|

| Global presence | 100+ countries |

| Medtech market | 600 billion USD |

| Supplier qualification | 3–12 months |

What is included in the product

Tailored Porter's Five Forces for Vygon S.A. uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, identifying disruptive risks and strategic levers to defend margins and market share.

Concise one-sheet Porter's Five Forces for Vygon S.A.—instantly visualize supplier, buyer, entrant, substitute and rivalry pressures to pinpoint strategic pain points and drop straight into pitch decks or decision templates.

Customers Bargaining Power

Hospital and GPO consolidation

Large hospitals, purchasing groups and national tenders negotiate aggressively on price, with public procurement representing around 14% of EU GDP in 2024, amplifying buyer leverage. Bundled contracts and formularies further concentrate spend and favor suppliers who can offer breadth and terms. Vygon must compete on total value and service, as losing a tender can materially dent regional volumes.

Clinical switching costs

Clinician preference, training, and unit protocols create moderate clinical switching costs for Vygon, anchoring use in ICUs and neonatology. Validated kits and device compatibility in critical care reduce buyer churn, especially given procurement contract cycles of typically 3–5 years. If alternative products meet validation standards, hospitals can switch at contract renewal points. Ongoing education and dedicated support programs materially improve account retention.

Price transparency in commoditized lines

IV access and standard catheters face intense price benchmarking as GPOs cover roughly 85% of US hospitals, driving multi-sourcing and reverse auctions that compress supplier margins by an estimated 10–25%. Buyers use bundled contracts and spot auctions to drive down costs, so differentiation through validated safety features and infection-reduction data—often commanding premiums up to ~15–20%—is critical. Value analysis committees scrutinize every SKU, delisting products lacking clear cost‑outcome evidence.

Regulatory and reimbursement pressures

Hospitals under budget caps and DRG systems, used in over 40 countries, push for lower device costs; payers require evidence of outcomes and total cost of care to justify any premium. Vygon’s clinical data can mitigate price pressure by demonstrating reduced complications or LOS, yet public and private procurement often award the compliant lowest-cost options.

- DRG coverage: over 40 countries

- Evidence-driven premium justification required

- Procurement frequently prioritizes lowest-cost compliant bids

Service, availability, and customization

Buyers of Vygon demand reliable supply, sterile kit customization, and rapid technical support; stock-outs shift leverage to customers who can impose penalties or switch suppliers, especially in hospital procurement. Strong after-sales service and clinical training reduce pure price focus, while local warehousing and faster replenishment materially improve responsiveness and lock in contracts.

- Reliable supply

- Sterile kit customization

- Rapid support

- After-sales & training reduce price pressure

- Local warehousing improves responsiveness

Buyers squeeze margins 10-25%; safety premiums ≈15-20%

Large buyers (public procurement ≈14% of EU GDP in 2024) and GPOs (≈85% of US hospitals) exert strong price pressure, compressing margins 10–25%. Clinical switching costs and 3–5 year contracts limit churn; DRG coverage in 40+ countries forces outcome evidence for premiums (≈15–20%). Reliable supply, training and local warehousing materially reduce buyer leverage.

| Metric | Value |

|---|---|

| Public procurement (EU) | ≈14% GDP (2024) |

| GPO coverage (US) | ≈85% hospitals |

| DRG adoption | 40+ countries |

| Margin compression | 10–25% |

| Premium for safety | ≈15–20% |

Same Document Delivered

Vygon S.A. Porter's Five Forces Analysis

This preview shows the exact Vygon S.A. Porter's Five Forces Analysis you'll receive after purchase—fully formatted, complete and ready to use. It contains the full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with no placeholders. Purchase grants instant access to this identical document.

Don't Miss the Bigger Picture

Vygon S.A. faces moderate supplier power, differentiated product strengths, and steady buyer demand, while regulatory barriers and niche specialization limit new entrants. Competitive rivalry is intense in select segments, and substitutes pose targeted threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable, consultant-grade insights.

Suppliers Bargaining Power

Specialized medical-grade materials

Many Vygon devices depend on medical-grade polymers, silicone and specialty resins sourced from a limited pool of certified suppliers, with qualification and biocompatibility testing typically taking 3–12 months and tying materials to specific vendors. This concentration raises switching costs and can extend lead times to several months; dual-sourcing is feasible but slowed by validation burdens.

Sterilization and cleanroom dependencies

Sterilization capacity for ethylene oxide and gamma irradiation is constrained and tightly regulated, so approved providers hold pricing and timing leverage; regional outages and compliance actions (notably 2022–24 plant suspensions) have periodically disrupted medtech supply chains and pushed contract sterilization rates higher. Cleanroom consumables and validated packaging further lock customers in, and Vygon eases risk via multi-site approvals but cannot fully eliminate the bottleneck.

Quality and compliance lock-in

Suppliers holding ISO 13485 and MDR/FDA-ready documentation strengthen bargaining power for Vygon since requalification under EU MDR (effective 26 May 2021) is time-consuming and costly in a global medical device market worth about 600 billion USD in 2024. Design history files often embed supplier-specific specs, so switching risks regulatory delays, product change notices and extended market entry timelines, enabling suppliers to secure better terms on critical components.

Scale vs. supplier concentration

Vygon’s global scale (presence in 100+ countries in 2024) delivers volume leverage and supports multi-year supply agreements, reducing supplier bargaining in standard disposables, while niche components such as specialty catheters and bespoke connectors remain supplied by few vendors, increasing supplier power; overall balance varies by category and moderates average supplier influence.

- Scale: 100+ countries (2024)

- Niche concentration: few specialized suppliers

- Contracts: multi-year agreements

- Mitigation: strategic partnerships stabilize pricing

Logistics and geopolitical exposure

Resin market volatility in 2024, higher energy and recurring transport disruptions have driven input cost spikes, with suppliers commonly passing through increases and invoking force majeure clauses; EU MDR UDI traceability has added upstream administrative burdens, so Vygon must maintain buffer stocks and pursue nearshoring to reduce exposure.

- Resin, energy, transport: 2024 volatility raised input risk

- Suppliers: pass-throughs and force majeure increase bargaining power

- EU MDR: UDI traceability adds upstream admin costs

- Mitigation: buffer stocks and nearshoring recommended

Concentrated suppliers and sterilization bottlenecks elevate medtech supplier leverage

Concentration of certified polymer, silicone and specialty-resin suppliers (qualification 3–12 months) raises switching costs and extends lead times; sterilization capacity constraints and 2022–24 plant suspensions increased supplier leverage. ISO 13485/MDR-ready vendors command premium due to requalification hurdles; Vygon scale (100+ countries, 2024) offsets power for common disposables but not niche components.

| Metric | 2024 value |

|---|---|

| Global presence | 100+ countries |

| Medtech market | 600 billion USD |

| Supplier qualification | 3–12 months |

What is included in the product

Tailored Porter's Five Forces for Vygon S.A. uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, identifying disruptive risks and strategic levers to defend margins and market share.

Concise one-sheet Porter's Five Forces for Vygon S.A.—instantly visualize supplier, buyer, entrant, substitute and rivalry pressures to pinpoint strategic pain points and drop straight into pitch decks or decision templates.

Customers Bargaining Power

Hospital and GPO consolidation

Large hospitals, purchasing groups and national tenders negotiate aggressively on price, with public procurement representing around 14% of EU GDP in 2024, amplifying buyer leverage. Bundled contracts and formularies further concentrate spend and favor suppliers who can offer breadth and terms. Vygon must compete on total value and service, as losing a tender can materially dent regional volumes.

Clinical switching costs

Clinician preference, training, and unit protocols create moderate clinical switching costs for Vygon, anchoring use in ICUs and neonatology. Validated kits and device compatibility in critical care reduce buyer churn, especially given procurement contract cycles of typically 3–5 years. If alternative products meet validation standards, hospitals can switch at contract renewal points. Ongoing education and dedicated support programs materially improve account retention.

Price transparency in commoditized lines

IV access and standard catheters face intense price benchmarking as GPOs cover roughly 85% of US hospitals, driving multi-sourcing and reverse auctions that compress supplier margins by an estimated 10–25%. Buyers use bundled contracts and spot auctions to drive down costs, so differentiation through validated safety features and infection-reduction data—often commanding premiums up to ~15–20%—is critical. Value analysis committees scrutinize every SKU, delisting products lacking clear cost‑outcome evidence.

Regulatory and reimbursement pressures

Hospitals under budget caps and DRG systems, used in over 40 countries, push for lower device costs; payers require evidence of outcomes and total cost of care to justify any premium. Vygon’s clinical data can mitigate price pressure by demonstrating reduced complications or LOS, yet public and private procurement often award the compliant lowest-cost options.

- DRG coverage: over 40 countries

- Evidence-driven premium justification required

- Procurement frequently prioritizes lowest-cost compliant bids

Service, availability, and customization

Buyers of Vygon demand reliable supply, sterile kit customization, and rapid technical support; stock-outs shift leverage to customers who can impose penalties or switch suppliers, especially in hospital procurement. Strong after-sales service and clinical training reduce pure price focus, while local warehousing and faster replenishment materially improve responsiveness and lock in contracts.

- Reliable supply

- Sterile kit customization

- Rapid support

- After-sales & training reduce price pressure

- Local warehousing improves responsiveness

Buyers squeeze margins 10-25%; safety premiums ≈15-20%

Large buyers (public procurement ≈14% of EU GDP in 2024) and GPOs (≈85% of US hospitals) exert strong price pressure, compressing margins 10–25%. Clinical switching costs and 3–5 year contracts limit churn; DRG coverage in 40+ countries forces outcome evidence for premiums (≈15–20%). Reliable supply, training and local warehousing materially reduce buyer leverage.

| Metric | Value |

|---|---|

| Public procurement (EU) | ≈14% GDP (2024) |

| GPO coverage (US) | ≈85% hospitals |

| DRG adoption | 40+ countries |

| Margin compression | 10–25% |

| Premium for safety | ≈15–20% |

Same Document Delivered

Vygon S.A. Porter's Five Forces Analysis

This preview shows the exact Vygon S.A. Porter's Five Forces Analysis you'll receive after purchase—fully formatted, complete and ready to use. It contains the full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with no placeholders. Purchase grants instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Vygon S.A. faces moderate supplier power, differentiated product strengths, and steady buyer demand, while regulatory barriers and niche specialization limit new entrants. Competitive rivalry is intense in select segments, and substitutes pose targeted threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for actionable, consultant-grade insights.

Suppliers Bargaining Power

Specialized medical-grade materials

Many Vygon devices depend on medical-grade polymers, silicone and specialty resins sourced from a limited pool of certified suppliers, with qualification and biocompatibility testing typically taking 3–12 months and tying materials to specific vendors. This concentration raises switching costs and can extend lead times to several months; dual-sourcing is feasible but slowed by validation burdens.

Sterilization and cleanroom dependencies

Sterilization capacity for ethylene oxide and gamma irradiation is constrained and tightly regulated, so approved providers hold pricing and timing leverage; regional outages and compliance actions (notably 2022–24 plant suspensions) have periodically disrupted medtech supply chains and pushed contract sterilization rates higher. Cleanroom consumables and validated packaging further lock customers in, and Vygon eases risk via multi-site approvals but cannot fully eliminate the bottleneck.

Quality and compliance lock-in

Suppliers holding ISO 13485 and MDR/FDA-ready documentation strengthen bargaining power for Vygon since requalification under EU MDR (effective 26 May 2021) is time-consuming and costly in a global medical device market worth about 600 billion USD in 2024. Design history files often embed supplier-specific specs, so switching risks regulatory delays, product change notices and extended market entry timelines, enabling suppliers to secure better terms on critical components.

Scale vs. supplier concentration

Vygon’s global scale (presence in 100+ countries in 2024) delivers volume leverage and supports multi-year supply agreements, reducing supplier bargaining in standard disposables, while niche components such as specialty catheters and bespoke connectors remain supplied by few vendors, increasing supplier power; overall balance varies by category and moderates average supplier influence.

- Scale: 100+ countries (2024)

- Niche concentration: few specialized suppliers

- Contracts: multi-year agreements

- Mitigation: strategic partnerships stabilize pricing

Logistics and geopolitical exposure

Resin market volatility in 2024, higher energy and recurring transport disruptions have driven input cost spikes, with suppliers commonly passing through increases and invoking force majeure clauses; EU MDR UDI traceability has added upstream administrative burdens, so Vygon must maintain buffer stocks and pursue nearshoring to reduce exposure.

- Resin, energy, transport: 2024 volatility raised input risk

- Suppliers: pass-throughs and force majeure increase bargaining power

- EU MDR: UDI traceability adds upstream admin costs

- Mitigation: buffer stocks and nearshoring recommended

Concentrated suppliers and sterilization bottlenecks elevate medtech supplier leverage

Concentration of certified polymer, silicone and specialty-resin suppliers (qualification 3–12 months) raises switching costs and extends lead times; sterilization capacity constraints and 2022–24 plant suspensions increased supplier leverage. ISO 13485/MDR-ready vendors command premium due to requalification hurdles; Vygon scale (100+ countries, 2024) offsets power for common disposables but not niche components.

| Metric | 2024 value |

|---|---|

| Global presence | 100+ countries |

| Medtech market | 600 billion USD |

| Supplier qualification | 3–12 months |

What is included in the product

Tailored Porter's Five Forces for Vygon S.A. uncovering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, identifying disruptive risks and strategic levers to defend margins and market share.

Concise one-sheet Porter's Five Forces for Vygon S.A.—instantly visualize supplier, buyer, entrant, substitute and rivalry pressures to pinpoint strategic pain points and drop straight into pitch decks or decision templates.

Customers Bargaining Power

Hospital and GPO consolidation

Large hospitals, purchasing groups and national tenders negotiate aggressively on price, with public procurement representing around 14% of EU GDP in 2024, amplifying buyer leverage. Bundled contracts and formularies further concentrate spend and favor suppliers who can offer breadth and terms. Vygon must compete on total value and service, as losing a tender can materially dent regional volumes.

Clinical switching costs

Clinician preference, training, and unit protocols create moderate clinical switching costs for Vygon, anchoring use in ICUs and neonatology. Validated kits and device compatibility in critical care reduce buyer churn, especially given procurement contract cycles of typically 3–5 years. If alternative products meet validation standards, hospitals can switch at contract renewal points. Ongoing education and dedicated support programs materially improve account retention.

Price transparency in commoditized lines

IV access and standard catheters face intense price benchmarking as GPOs cover roughly 85% of US hospitals, driving multi-sourcing and reverse auctions that compress supplier margins by an estimated 10–25%. Buyers use bundled contracts and spot auctions to drive down costs, so differentiation through validated safety features and infection-reduction data—often commanding premiums up to ~15–20%—is critical. Value analysis committees scrutinize every SKU, delisting products lacking clear cost‑outcome evidence.

Regulatory and reimbursement pressures

Hospitals under budget caps and DRG systems, used in over 40 countries, push for lower device costs; payers require evidence of outcomes and total cost of care to justify any premium. Vygon’s clinical data can mitigate price pressure by demonstrating reduced complications or LOS, yet public and private procurement often award the compliant lowest-cost options.

- DRG coverage: over 40 countries

- Evidence-driven premium justification required

- Procurement frequently prioritizes lowest-cost compliant bids

Service, availability, and customization

Buyers of Vygon demand reliable supply, sterile kit customization, and rapid technical support; stock-outs shift leverage to customers who can impose penalties or switch suppliers, especially in hospital procurement. Strong after-sales service and clinical training reduce pure price focus, while local warehousing and faster replenishment materially improve responsiveness and lock in contracts.

- Reliable supply

- Sterile kit customization

- Rapid support

- After-sales & training reduce price pressure

- Local warehousing improves responsiveness

Buyers squeeze margins 10-25%; safety premiums ≈15-20%

Large buyers (public procurement ≈14% of EU GDP in 2024) and GPOs (≈85% of US hospitals) exert strong price pressure, compressing margins 10–25%. Clinical switching costs and 3–5 year contracts limit churn; DRG coverage in 40+ countries forces outcome evidence for premiums (≈15–20%). Reliable supply, training and local warehousing materially reduce buyer leverage.

| Metric | Value |

|---|---|

| Public procurement (EU) | ≈14% GDP (2024) |

| GPO coverage (US) | ≈85% hospitals |

| DRG adoption | 40+ countries |

| Margin compression | 10–25% |

| Premium for safety | ≈15–20% |

Same Document Delivered

Vygon S.A. Porter's Five Forces Analysis

This preview shows the exact Vygon S.A. Porter's Five Forces Analysis you'll receive after purchase—fully formatted, complete and ready to use. It contains the full assessment of competitive rivalry, buyer and supplier power, threat of substitutes, and barriers to entry with no placeholders. Purchase grants instant access to this identical document.