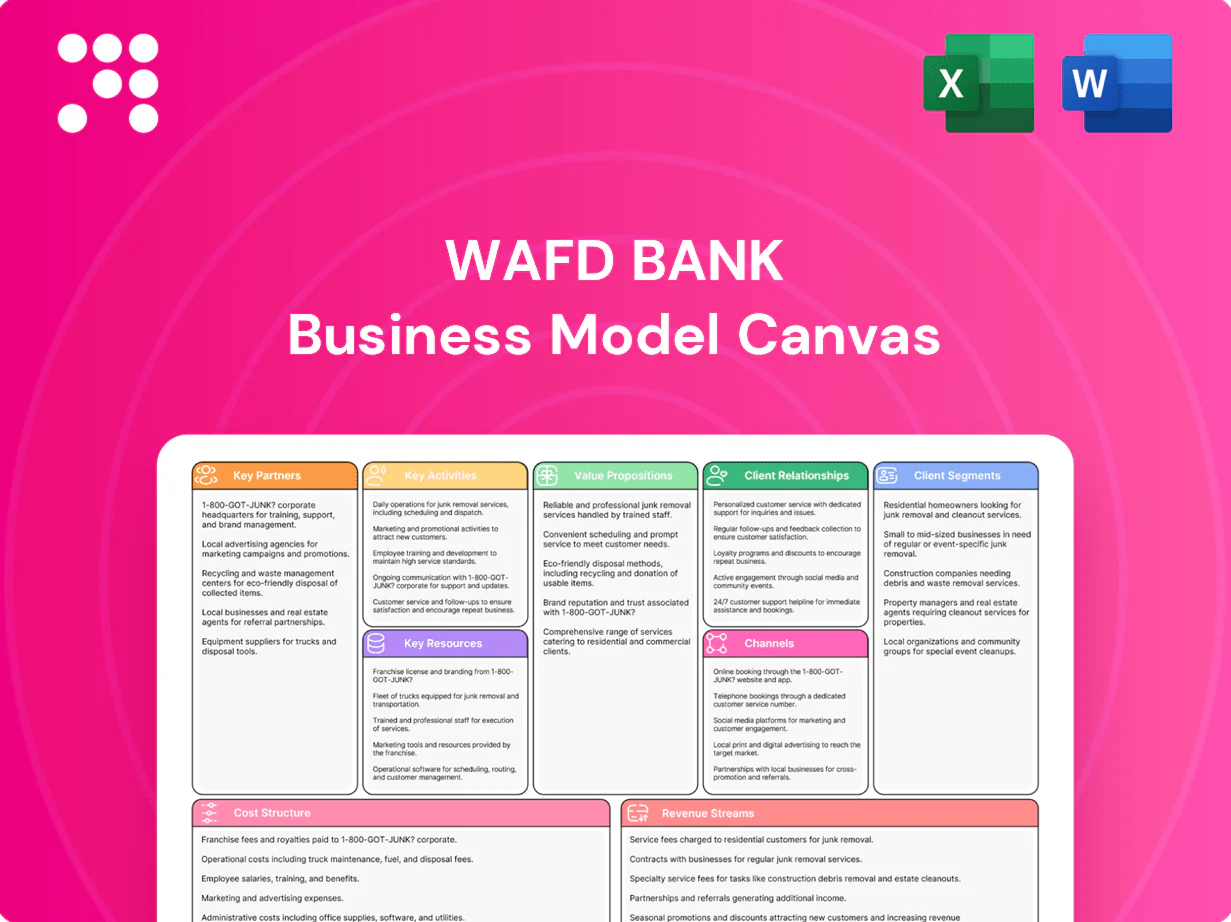

WaFd Bank Business Model Canvas

Strategic Business Model Canvas: Clear value, scalable deposits & lending growth

Discover WaFd Bank’s strategic playbook with our concise Business Model Canvas—clarifying how it creates customer value, scales deposits and lending, and leverages partnerships to grow. This professional, editable canvas is ideal for investors, strategists, and analysts. Purchase the full Word/Excel file to access all nine blocks, detailed insights, and actionable recommendations.

Partnerships

Payment Networks & Card Processors

Partnerships with Visa/Mastercard and merchant acquirers enable WaFd to issue cards and accept payments, leveraging 2024 global network volumes (Visa/Mastercard combined processed ~20 trillion USD in purchase volume) for secure rails, fraud tools and interchange settlement. These alliances expand customer utility and drove a notable portion of WaFd noninterest fee income in 2024, while co-brand and rewards partners lift card uptake and incremental spend.

Fintech & Core Banking Vendors

Core processors, digital banking platforms and API providers power WaFd’s accounts, payments and mobile features, while fintech collaborations accelerated onboarding, fraud detection and lending automation; WaFd reported approximately $19.5B in assets in 2024 supporting scalable integrations. Vendor SLAs and tighter integrations improved uptime and CX, and joint roadmaps cut time-to-market and IT costs through shared development and deployment pipelines.

Commercial Real Estate Ecosystem

Developers, brokers, and appraisers supply CRE deal flow and underwriting inputs, driving WaFd Bank’s project selection and risk models; in 2024 WaFd reported $18.2 billion in assets with CRE a material component of its commercial lending mix. Title, escrow, and legal partners accelerate closings and collateral perfection, reducing time-to-funding and legal exposure. Construction inspectors and GC networks support draw controls and on-site risk mitigation. These partnerships bolster CRE specialization and portfolio quality.

Treasury & Correspondent Banks

Correspondent banks and liquidity providers support WaFd with payments, wires and syndicated loan execution, enabling participation loans and risk distribution across partners. Access to Fed borrowing windows, FHLB advances and capital markets in 2024 (WaFd total assets ~27.5 billion) enhances balance sheet flexibility and funding diversity. Shared services with partners reduce unit costs for specialty transactions and syndications.

- Payments & wires: faster settlement

- Participation loans: risk distribution

- Fed/FHLB/capital markets: funding & flexibility

- Shared services: lower transaction costs

Community & Affinity Organizations

Community partners—local chambers, nonprofits and industry groups—extend WaFd Bank’s reach into households and SMBs across its ~200-branch footprint, supporting targeted deposit growth within core Western markets.

Financial education and CRA initiatives in 2024 reinforced trust and brand equity after WaFd reported roughly $18.6 billion in assets, driving stronger local engagement.

Affinity partnerships and co-marketing enable tailored product offers and improved acquisition and retention in priority communities.

- Local reach: chambers, nonprofits, industry groups

- Trust drivers: financial education, CRA work

- Product focus: affinity-targeted deposits

- Growth lever: co-marketing for acquisition/retention

Card networks and processors power payments and CRE lending across $27.5B footprint

Strategic card and network alliances enable card issuance and payments leveraging 2024 global network volumes (~20 trillion USD) and support WaFd’s card-led fee channels; core processors and fintech APIs power digital banking across WaFd’s ~200-branch footprint and ~$27.5B assets (2024). CRE brokers, appraisers and construction partners underpin commercial underwriting and draw controls; correspondent banks, FHLB and Fed access supply liquidity and syndication capacity.

| Partnership | 2024 Metric |

|---|---|

| Card networks | ~20T global volume |

| Bank footprint & tech | ~200 branches; $27.5B assets |

| Funding partners | Fed/FHLB/correspondents |

What is included in the product

A comprehensive Business Model Canvas for WaFd Bank detailing customer segments (retail, small business, commercial), multi-channel delivery (branches, digital, advisors), value propositions (relationship banking, local expertise, lending and deposit solutions), revenue streams and cost structure across the 9 BMC blocks. Includes competitive advantages, SWOT-linked insights and polished narrative for presentations, analysis, and investor discussions.

High-level view of WaFd Bank’s business model with editable cells to quickly surface customer pain points and streamline branch, digital and lending workflows for faster decision-making.

Activities

Deposit Gathering & Servicing

Design and price-saving and CD products to attract stable, low-cost funds, aligning yields with the 2024 federal funds target of 5.25–5.50% to manage spread pressures. Operate onboarding, KYC, and servicing across digital and branch channels to reduce acquisition cost and speed deposit conversion. Manage liquidity and interest expense through product-mix optimization and laddered CDs. Enhance retention with mobile features and relationship pricing tied to account balances and activity.

Lending & Underwriting

Lending & Underwriting at WaFd focuses on originating consumer, SMB, and CRE loans under prudent credit standards and risk-based pricing to reflect income, collateral, and cash-flow analysis. Documentation, closing, and ongoing portfolio monitoring are executed to enforce disciplined concentration and limit frameworks. As of 2024, WaFd Financial (NASDAQ: WAFD) applies these processes across its regional branch network and commercial lending platforms.

Risk & Compliance Management

Operate enterprise programs across credit, market, liquidity and operational risk covering WaFd's $16.2B in assets (2024), with an emphasis on portfolio-level credit governance and concentration limits. Maintain BSA/AML, KYC and consumer compliance controls processing thousands of SARs and KYC reviews annually. Conduct stress testing, provisioning and capital planning (CET1 ~12.4%) and use analytics and audit findings to ensure resilience and regulatory adherence.

Digital Product & CX Development

Build and iterate mobile, online banking, and payments experiences while implementing APIs, strong authentication, and layered fraud prevention to protect customer flows. Use UX research and analytics to shorten journeys and reduce friction, coordinating releases with vendor roadmaps and mandatory security reviews to ensure compliance and uptime. Prioritize measurable CX KPIs and sprint-based delivery.

- API-led integration

- Auth & fraud controls

- UX research-driven iteration

- Vendor & security alignment

Wealth & Treasury Solutions

Wealth & Treasury Solutions delivers advisory, brokerage and financial planning for affluent clients while providing treasury management, cash and merchant services to business customers; WaFd reported roughly $20 billion in assets in 2024, underpinning scale for these services. The unit prioritizes cross-selling to deepen relationships and diversify fee revenue, and maintains fiduciary standards with tailored client reporting and consolidated performance statements.

- Affluent advisory, brokerage, planning

- Treasury, cash, merchant services for businesses

- Cross-sell to boost fee diversification

- Fiduciary compliance and customized reporting

Align low-cost deposits to fed funds 5.25-5.50% and scale lending on $16.2B assets

Design low‑cost deposits aligned to the 2024 federal funds target 5.25–5.50% to manage net interest spread. Originate consumer, SMB and CRE loans across regional branches against $16.2B in assets (2024) with risk‑based underwriting. Run enterprise risk, BSA/AML and stress testing (CET1 ~12.4%) while scaling digital banking, APIs and wealth/treasury cross‑sell.

| Metric | 2024 |

|---|---|

| Total assets | $16.2B |

| CET1 ratio | ~12.4% |

| Fed funds target | 5.25–5.50% |

Preview Before You Purchase

Business Model Canvas

The WaFd Bank Business Model Canvas shown here is the actual deliverable, not a mockup or sample. It’s a direct snapshot of the final document you’ll receive upon purchase, fully populated and professionally formatted. After buying, you’ll instantly download this same file—ready to edit, present, or share in Word and Excel. No surprises, just the complete canvas as previewed.

Strategic Business Model Canvas: Clear value, scalable deposits & lending growth

Discover WaFd Bank’s strategic playbook with our concise Business Model Canvas—clarifying how it creates customer value, scales deposits and lending, and leverages partnerships to grow. This professional, editable canvas is ideal for investors, strategists, and analysts. Purchase the full Word/Excel file to access all nine blocks, detailed insights, and actionable recommendations.

Partnerships

Payment Networks & Card Processors

Partnerships with Visa/Mastercard and merchant acquirers enable WaFd to issue cards and accept payments, leveraging 2024 global network volumes (Visa/Mastercard combined processed ~20 trillion USD in purchase volume) for secure rails, fraud tools and interchange settlement. These alliances expand customer utility and drove a notable portion of WaFd noninterest fee income in 2024, while co-brand and rewards partners lift card uptake and incremental spend.

Fintech & Core Banking Vendors

Core processors, digital banking platforms and API providers power WaFd’s accounts, payments and mobile features, while fintech collaborations accelerated onboarding, fraud detection and lending automation; WaFd reported approximately $19.5B in assets in 2024 supporting scalable integrations. Vendor SLAs and tighter integrations improved uptime and CX, and joint roadmaps cut time-to-market and IT costs through shared development and deployment pipelines.

Commercial Real Estate Ecosystem

Developers, brokers, and appraisers supply CRE deal flow and underwriting inputs, driving WaFd Bank’s project selection and risk models; in 2024 WaFd reported $18.2 billion in assets with CRE a material component of its commercial lending mix. Title, escrow, and legal partners accelerate closings and collateral perfection, reducing time-to-funding and legal exposure. Construction inspectors and GC networks support draw controls and on-site risk mitigation. These partnerships bolster CRE specialization and portfolio quality.

Treasury & Correspondent Banks

Correspondent banks and liquidity providers support WaFd with payments, wires and syndicated loan execution, enabling participation loans and risk distribution across partners. Access to Fed borrowing windows, FHLB advances and capital markets in 2024 (WaFd total assets ~27.5 billion) enhances balance sheet flexibility and funding diversity. Shared services with partners reduce unit costs for specialty transactions and syndications.

- Payments & wires: faster settlement

- Participation loans: risk distribution

- Fed/FHLB/capital markets: funding & flexibility

- Shared services: lower transaction costs

Community & Affinity Organizations

Community partners—local chambers, nonprofits and industry groups—extend WaFd Bank’s reach into households and SMBs across its ~200-branch footprint, supporting targeted deposit growth within core Western markets.

Financial education and CRA initiatives in 2024 reinforced trust and brand equity after WaFd reported roughly $18.6 billion in assets, driving stronger local engagement.

Affinity partnerships and co-marketing enable tailored product offers and improved acquisition and retention in priority communities.

- Local reach: chambers, nonprofits, industry groups

- Trust drivers: financial education, CRA work

- Product focus: affinity-targeted deposits

- Growth lever: co-marketing for acquisition/retention

Card networks and processors power payments and CRE lending across $27.5B footprint

Strategic card and network alliances enable card issuance and payments leveraging 2024 global network volumes (~20 trillion USD) and support WaFd’s card-led fee channels; core processors and fintech APIs power digital banking across WaFd’s ~200-branch footprint and ~$27.5B assets (2024). CRE brokers, appraisers and construction partners underpin commercial underwriting and draw controls; correspondent banks, FHLB and Fed access supply liquidity and syndication capacity.

| Partnership | 2024 Metric |

|---|---|

| Card networks | ~20T global volume |

| Bank footprint & tech | ~200 branches; $27.5B assets |

| Funding partners | Fed/FHLB/correspondents |

What is included in the product

A comprehensive Business Model Canvas for WaFd Bank detailing customer segments (retail, small business, commercial), multi-channel delivery (branches, digital, advisors), value propositions (relationship banking, local expertise, lending and deposit solutions), revenue streams and cost structure across the 9 BMC blocks. Includes competitive advantages, SWOT-linked insights and polished narrative for presentations, analysis, and investor discussions.

High-level view of WaFd Bank’s business model with editable cells to quickly surface customer pain points and streamline branch, digital and lending workflows for faster decision-making.

Activities

Deposit Gathering & Servicing

Design and price-saving and CD products to attract stable, low-cost funds, aligning yields with the 2024 federal funds target of 5.25–5.50% to manage spread pressures. Operate onboarding, KYC, and servicing across digital and branch channels to reduce acquisition cost and speed deposit conversion. Manage liquidity and interest expense through product-mix optimization and laddered CDs. Enhance retention with mobile features and relationship pricing tied to account balances and activity.

Lending & Underwriting

Lending & Underwriting at WaFd focuses on originating consumer, SMB, and CRE loans under prudent credit standards and risk-based pricing to reflect income, collateral, and cash-flow analysis. Documentation, closing, and ongoing portfolio monitoring are executed to enforce disciplined concentration and limit frameworks. As of 2024, WaFd Financial (NASDAQ: WAFD) applies these processes across its regional branch network and commercial lending platforms.

Risk & Compliance Management

Operate enterprise programs across credit, market, liquidity and operational risk covering WaFd's $16.2B in assets (2024), with an emphasis on portfolio-level credit governance and concentration limits. Maintain BSA/AML, KYC and consumer compliance controls processing thousands of SARs and KYC reviews annually. Conduct stress testing, provisioning and capital planning (CET1 ~12.4%) and use analytics and audit findings to ensure resilience and regulatory adherence.

Digital Product & CX Development

Build and iterate mobile, online banking, and payments experiences while implementing APIs, strong authentication, and layered fraud prevention to protect customer flows. Use UX research and analytics to shorten journeys and reduce friction, coordinating releases with vendor roadmaps and mandatory security reviews to ensure compliance and uptime. Prioritize measurable CX KPIs and sprint-based delivery.

- API-led integration

- Auth & fraud controls

- UX research-driven iteration

- Vendor & security alignment

Wealth & Treasury Solutions

Wealth & Treasury Solutions delivers advisory, brokerage and financial planning for affluent clients while providing treasury management, cash and merchant services to business customers; WaFd reported roughly $20 billion in assets in 2024, underpinning scale for these services. The unit prioritizes cross-selling to deepen relationships and diversify fee revenue, and maintains fiduciary standards with tailored client reporting and consolidated performance statements.

- Affluent advisory, brokerage, planning

- Treasury, cash, merchant services for businesses

- Cross-sell to boost fee diversification

- Fiduciary compliance and customized reporting

Align low-cost deposits to fed funds 5.25-5.50% and scale lending on $16.2B assets

Design low‑cost deposits aligned to the 2024 federal funds target 5.25–5.50% to manage net interest spread. Originate consumer, SMB and CRE loans across regional branches against $16.2B in assets (2024) with risk‑based underwriting. Run enterprise risk, BSA/AML and stress testing (CET1 ~12.4%) while scaling digital banking, APIs and wealth/treasury cross‑sell.

| Metric | 2024 |

|---|---|

| Total assets | $16.2B |

| CET1 ratio | ~12.4% |

| Fed funds target | 5.25–5.50% |

Preview Before You Purchase

Business Model Canvas

The WaFd Bank Business Model Canvas shown here is the actual deliverable, not a mockup or sample. It’s a direct snapshot of the final document you’ll receive upon purchase, fully populated and professionally formatted. After buying, you’ll instantly download this same file—ready to edit, present, or share in Word and Excel. No surprises, just the complete canvas as previewed.

Description

Strategic Business Model Canvas: Clear value, scalable deposits & lending growth

Discover WaFd Bank’s strategic playbook with our concise Business Model Canvas—clarifying how it creates customer value, scales deposits and lending, and leverages partnerships to grow. This professional, editable canvas is ideal for investors, strategists, and analysts. Purchase the full Word/Excel file to access all nine blocks, detailed insights, and actionable recommendations.

Partnerships

Payment Networks & Card Processors

Partnerships with Visa/Mastercard and merchant acquirers enable WaFd to issue cards and accept payments, leveraging 2024 global network volumes (Visa/Mastercard combined processed ~20 trillion USD in purchase volume) for secure rails, fraud tools and interchange settlement. These alliances expand customer utility and drove a notable portion of WaFd noninterest fee income in 2024, while co-brand and rewards partners lift card uptake and incremental spend.

Fintech & Core Banking Vendors

Core processors, digital banking platforms and API providers power WaFd’s accounts, payments and mobile features, while fintech collaborations accelerated onboarding, fraud detection and lending automation; WaFd reported approximately $19.5B in assets in 2024 supporting scalable integrations. Vendor SLAs and tighter integrations improved uptime and CX, and joint roadmaps cut time-to-market and IT costs through shared development and deployment pipelines.

Commercial Real Estate Ecosystem

Developers, brokers, and appraisers supply CRE deal flow and underwriting inputs, driving WaFd Bank’s project selection and risk models; in 2024 WaFd reported $18.2 billion in assets with CRE a material component of its commercial lending mix. Title, escrow, and legal partners accelerate closings and collateral perfection, reducing time-to-funding and legal exposure. Construction inspectors and GC networks support draw controls and on-site risk mitigation. These partnerships bolster CRE specialization and portfolio quality.

Treasury & Correspondent Banks

Correspondent banks and liquidity providers support WaFd with payments, wires and syndicated loan execution, enabling participation loans and risk distribution across partners. Access to Fed borrowing windows, FHLB advances and capital markets in 2024 (WaFd total assets ~27.5 billion) enhances balance sheet flexibility and funding diversity. Shared services with partners reduce unit costs for specialty transactions and syndications.

- Payments & wires: faster settlement

- Participation loans: risk distribution

- Fed/FHLB/capital markets: funding & flexibility

- Shared services: lower transaction costs

Community & Affinity Organizations

Community partners—local chambers, nonprofits and industry groups—extend WaFd Bank’s reach into households and SMBs across its ~200-branch footprint, supporting targeted deposit growth within core Western markets.

Financial education and CRA initiatives in 2024 reinforced trust and brand equity after WaFd reported roughly $18.6 billion in assets, driving stronger local engagement.

Affinity partnerships and co-marketing enable tailored product offers and improved acquisition and retention in priority communities.

- Local reach: chambers, nonprofits, industry groups

- Trust drivers: financial education, CRA work

- Product focus: affinity-targeted deposits

- Growth lever: co-marketing for acquisition/retention

Card networks and processors power payments and CRE lending across $27.5B footprint

Strategic card and network alliances enable card issuance and payments leveraging 2024 global network volumes (~20 trillion USD) and support WaFd’s card-led fee channels; core processors and fintech APIs power digital banking across WaFd’s ~200-branch footprint and ~$27.5B assets (2024). CRE brokers, appraisers and construction partners underpin commercial underwriting and draw controls; correspondent banks, FHLB and Fed access supply liquidity and syndication capacity.

| Partnership | 2024 Metric |

|---|---|

| Card networks | ~20T global volume |

| Bank footprint & tech | ~200 branches; $27.5B assets |

| Funding partners | Fed/FHLB/correspondents |

What is included in the product

A comprehensive Business Model Canvas for WaFd Bank detailing customer segments (retail, small business, commercial), multi-channel delivery (branches, digital, advisors), value propositions (relationship banking, local expertise, lending and deposit solutions), revenue streams and cost structure across the 9 BMC blocks. Includes competitive advantages, SWOT-linked insights and polished narrative for presentations, analysis, and investor discussions.

High-level view of WaFd Bank’s business model with editable cells to quickly surface customer pain points and streamline branch, digital and lending workflows for faster decision-making.

Activities

Deposit Gathering & Servicing

Design and price-saving and CD products to attract stable, low-cost funds, aligning yields with the 2024 federal funds target of 5.25–5.50% to manage spread pressures. Operate onboarding, KYC, and servicing across digital and branch channels to reduce acquisition cost and speed deposit conversion. Manage liquidity and interest expense through product-mix optimization and laddered CDs. Enhance retention with mobile features and relationship pricing tied to account balances and activity.

Lending & Underwriting

Lending & Underwriting at WaFd focuses on originating consumer, SMB, and CRE loans under prudent credit standards and risk-based pricing to reflect income, collateral, and cash-flow analysis. Documentation, closing, and ongoing portfolio monitoring are executed to enforce disciplined concentration and limit frameworks. As of 2024, WaFd Financial (NASDAQ: WAFD) applies these processes across its regional branch network and commercial lending platforms.

Risk & Compliance Management

Operate enterprise programs across credit, market, liquidity and operational risk covering WaFd's $16.2B in assets (2024), with an emphasis on portfolio-level credit governance and concentration limits. Maintain BSA/AML, KYC and consumer compliance controls processing thousands of SARs and KYC reviews annually. Conduct stress testing, provisioning and capital planning (CET1 ~12.4%) and use analytics and audit findings to ensure resilience and regulatory adherence.

Digital Product & CX Development

Build and iterate mobile, online banking, and payments experiences while implementing APIs, strong authentication, and layered fraud prevention to protect customer flows. Use UX research and analytics to shorten journeys and reduce friction, coordinating releases with vendor roadmaps and mandatory security reviews to ensure compliance and uptime. Prioritize measurable CX KPIs and sprint-based delivery.

- API-led integration

- Auth & fraud controls

- UX research-driven iteration

- Vendor & security alignment

Wealth & Treasury Solutions

Wealth & Treasury Solutions delivers advisory, brokerage and financial planning for affluent clients while providing treasury management, cash and merchant services to business customers; WaFd reported roughly $20 billion in assets in 2024, underpinning scale for these services. The unit prioritizes cross-selling to deepen relationships and diversify fee revenue, and maintains fiduciary standards with tailored client reporting and consolidated performance statements.

- Affluent advisory, brokerage, planning

- Treasury, cash, merchant services for businesses

- Cross-sell to boost fee diversification

- Fiduciary compliance and customized reporting

Align low-cost deposits to fed funds 5.25-5.50% and scale lending on $16.2B assets

Design low‑cost deposits aligned to the 2024 federal funds target 5.25–5.50% to manage net interest spread. Originate consumer, SMB and CRE loans across regional branches against $16.2B in assets (2024) with risk‑based underwriting. Run enterprise risk, BSA/AML and stress testing (CET1 ~12.4%) while scaling digital banking, APIs and wealth/treasury cross‑sell.

| Metric | 2024 |

|---|---|

| Total assets | $16.2B |

| CET1 ratio | ~12.4% |

| Fed funds target | 5.25–5.50% |

Preview Before You Purchase

Business Model Canvas

The WaFd Bank Business Model Canvas shown here is the actual deliverable, not a mockup or sample. It’s a direct snapshot of the final document you’ll receive upon purchase, fully populated and professionally formatted. After buying, you’ll instantly download this same file—ready to edit, present, or share in Word and Excel. No surprises, just the complete canvas as previewed.